OSI - Badger Meter: Shares Are Awfully Pricey Right Now

2023-03-11 04:53:53 ET

Summary

- Badger Meter continues to grow, and most of its bottom line figures have been faring well despite economic concerns.

- The firm's balance sheet is solid, and management has demonstrated time and again that the business is a high-quality operator.

- But shares are pricey and likely have limited upside, if any, at this point in time.

One of the things that makes investing exciting is also the same thing that makes it frustrating from time to time. This is the fact that you can't always be right and that some of your valuation assessments will just turn out to be wrong. This is part of the game and will likely always be part of the game. One company where I was definitely wrong on in retrospect is Badger Meter ( BMI ), an enterprise that focuses largely on providing flow measurement, water quality, and other tools, software, and analytics solutions to its customers. Although financial performance remains somewhat mixed, the general trend for investors has been positive. As a result, shares of the company have risen drastically. But now, I feel compelled to sound the alarm. For well over a year now, going on two years in fact, my call in the company has been incorrect. But given how shares are priced right now, I do think investors should tread very cautiously. Even though the company has risen nicely, shares look drastically overpriced at this point in time.

A lofty measurement

Back in the middle of July of 2021, I found myself taking a rather neutral stance on Badger Meter. Leading up to that point, the company had demonstrated consistent and steady growth for much of the prior few years. Considering the pandemic that we were going through, the firm established itself as a resilient operation and it had no debt, with a surplus of cash on its books. This made me realize that the company was a high-quality business. Normally, a high-quality firm can justify some sort of premium on its valuation. But considering how pricey shares were, I could not rate the business any higher than a 'hold'.

{kind=link}

To be clear, high quality does not necessarily equate to rapid growth. But when it comes to the 2022 fiscal year , growth was rather impressive. Sales came in for that year at $565.6 million. That's 12% higher than the $505.2 million reported for the 2021 fiscal year. That sales increase would have been even greater at 13.2% had it not been for foreign currency fluctuations. The greatest growth for the company stemmed from the customers that it serves in the utility water market. These were up 13.6% year over year, thanks to strong market demand and the continued adoption of cellular AMI solutions. Increased meter volumes also contributed to the company's top line expansion. Meanwhile, sales of products into the global flow instrumentation and markets rose by about 4.3%, though that sales increase would have been 7.1% had it not been for foreign currency fluctuations.

On the bottom line, the picture also got better. Net income of $66.5 million translated to a year-over-year growth rate of 9.2%. A reduction in the company's selling, engineering, and administrative costs from 25.1% of sales to 23.5% of sales was helpful in improving the company's bottom line. Other profitability metrics mostly followed suit. Operating cash flow was the exception, dropping from $87.5 million down to $82.5 million. But if we adjust for changes in working capital, we would see that number rise from $87.8 million to $89.7 million. Meanwhile, EBITDA for the firm increased from $106.5 million to $113.4 million.

{kind=link}

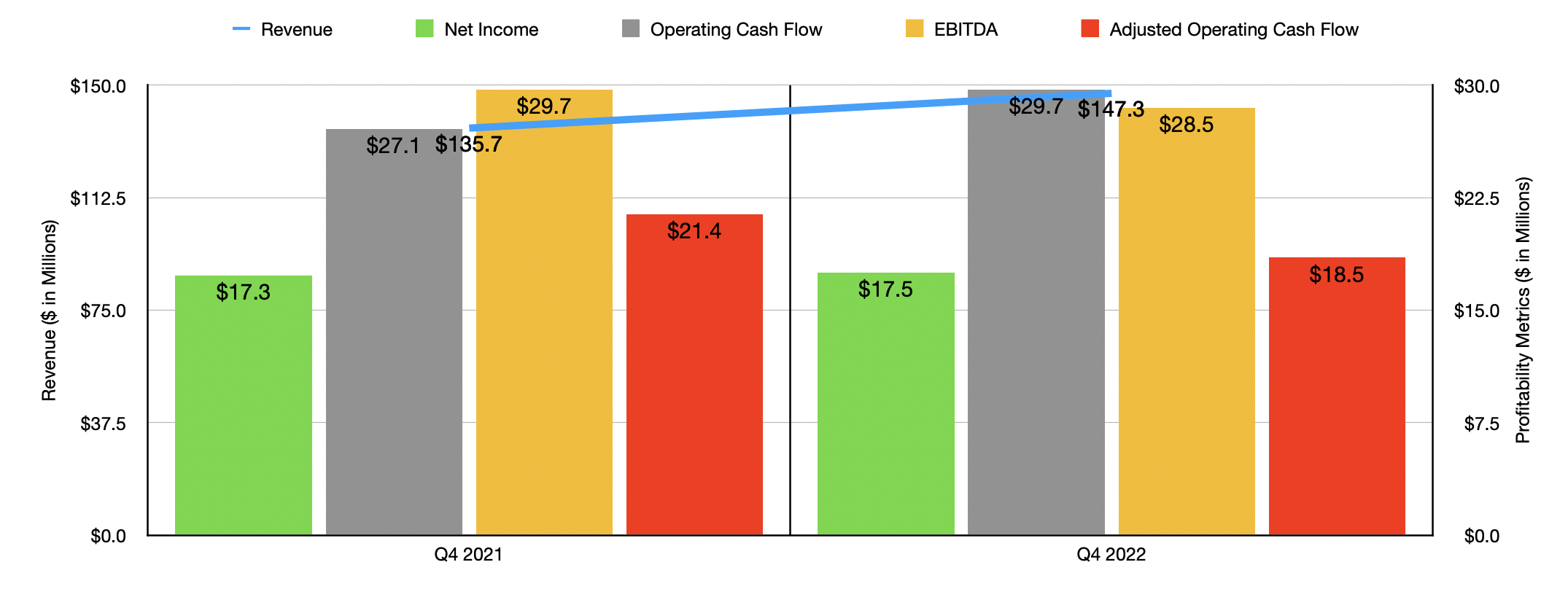

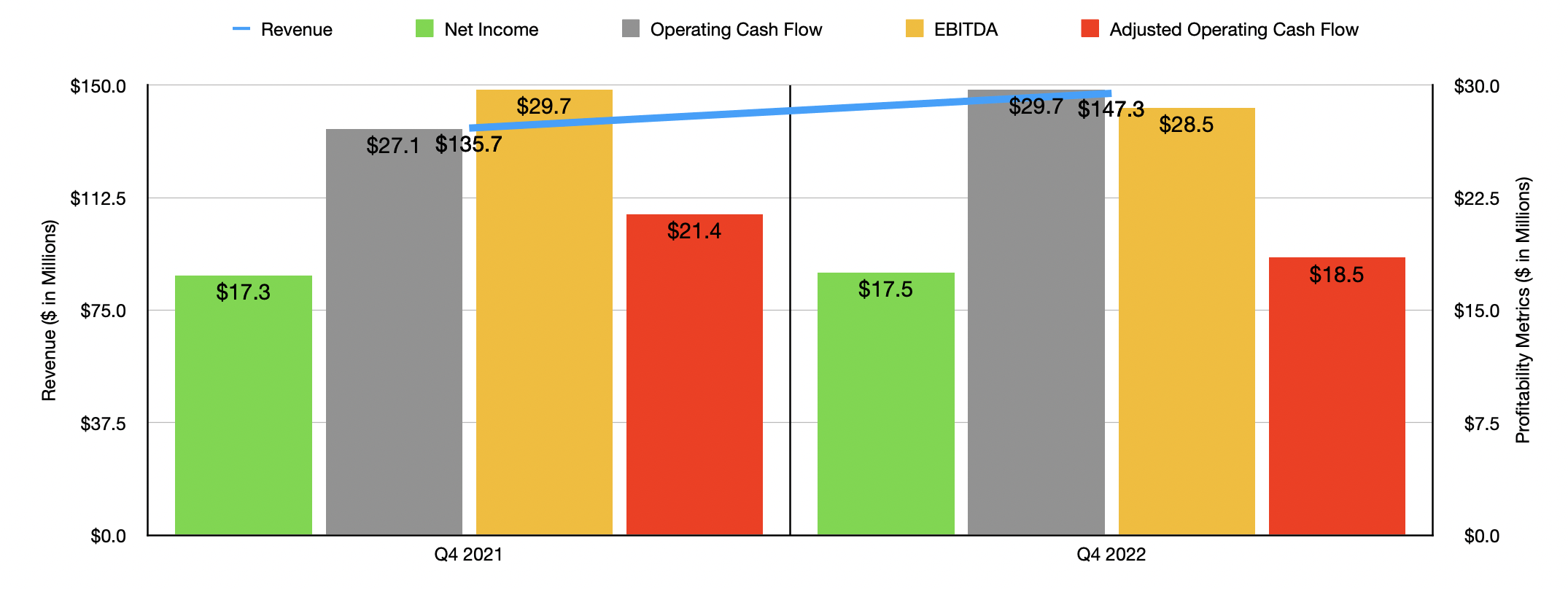

It would make sense for investors to be worried about current and changing market conditions. But all the data that we have seen so far suggests that the picture is not all that bad. At least not for this particular enterprise. Revenue, for instance, came in strong in the final quarter of the 2022 fiscal year, hitting $147.3 million. That's 8.5% higher than the $135.7 million reported one year earlier. Net income inched up from $17.3 million to $17.5 million. Operating cash flow grew from $27.1 million to $29.7 million. Though if we adjust for changes in working capital, we would have seen it drop from $21.4 million to $18.5 million. Meanwhile, EBITDA inched down from $29.7 million to $28.5 million.

{kind=link}

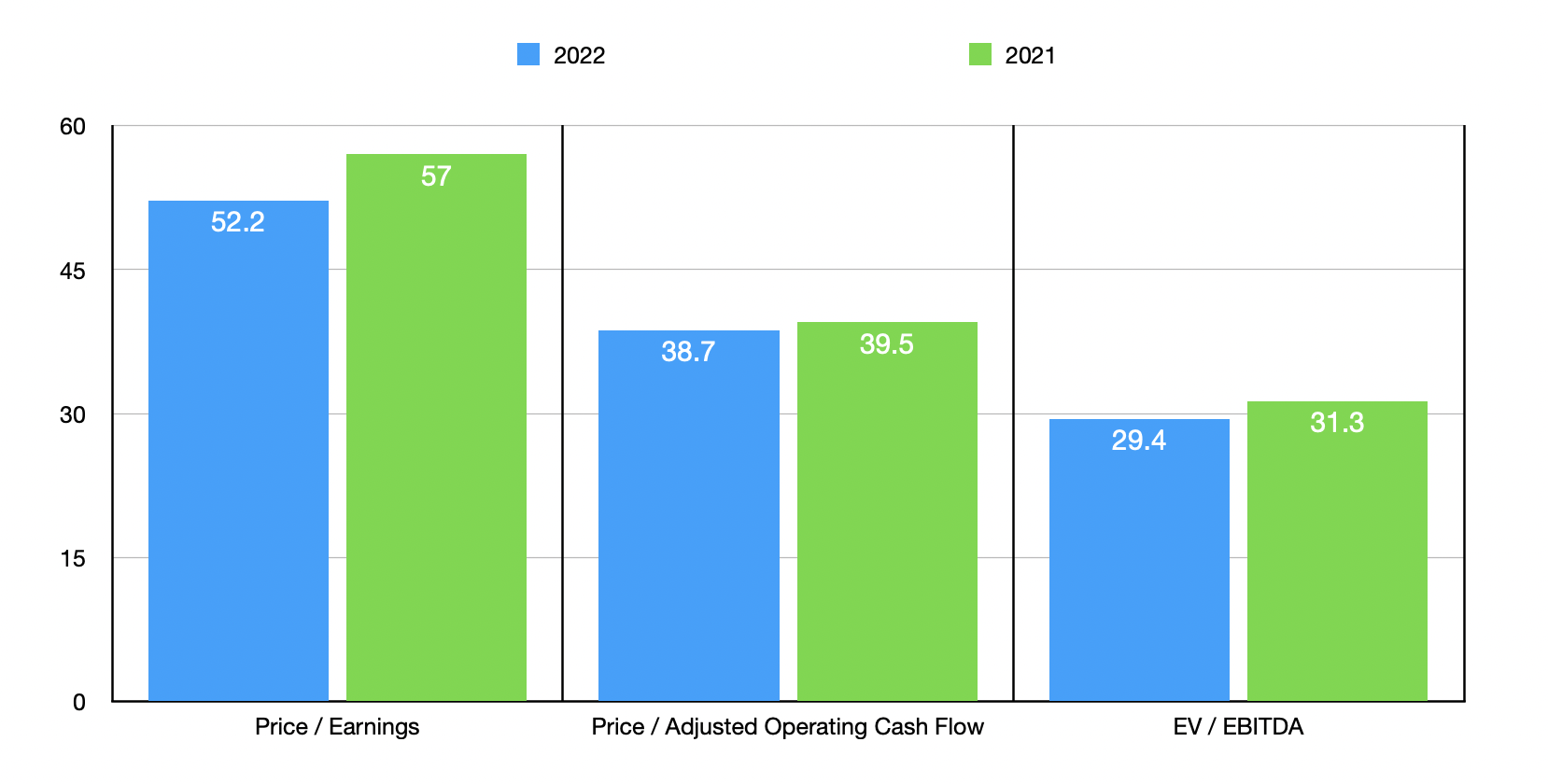

Using data from the 2022 fiscal year, I calculated that the company is trading at a price-to-earnings multiple of 52.2. Although astronomical, this is lower than the 57 reading that we get using data from the 2021 fiscal year. The price to adjusted operating cash flow multiple is a bit lower at 38.7. That stacks up against the 39.5 reading that we get using data from the year before. Meanwhile, the EV to EBITDA multiple for the company should be about 29.4. That's down from the 31.3 reading that we get using data from 2021. As part of my analysis, I decided to compare the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 10 to a high of 49.1. In this case, Badger Meter was the most expensive of the group. Using the EV to EBITDA approach, the company also looks expensive. The five firms I looked at had multiples ranging between 3.5 and 33.2. Four of those five firms were cheaper than our target. The only way in which shares of the company looked near the cheap side of the spectrum relative to similar firms was using the price to operating cash flow approach. The four firms that had positive results ranged from a low of 11.5 to a high of 772.8. Two of the four firms had multiples that were lower than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Badger Meter |

| 52.2 |

| 38.7 |

| 29.4 |

| NAPCO Security Technologies ( NSSC ) |

| 47.7 |

| 750.7 |

| 32.6 |

| Hollysys Automation Technologies ( HOLI ) |

| 10.2 |

| N/A |

| 3.5 |

| National Instruments Corp ( NATI ) |

| 48.5 |

| 157.0 |

| 25.4 |

| OSI Systems (OSIS) |

| 19.0 |

| 11.5 |

| 13.9 |

| Vontier Corp ( VNT ) |

| 10.9 |

| 13.4 |

| 9.2 |

Takeaway

Operationally speaking, Badger Meter is a solid business. The company has no debt on its books and enjoys $138.1 million in cash and cash equivalents. This makes it a very low-risk prospect from the perspective of a bankruptcy scenario. The company is also clearly a quality operator that would likely continue to grow for the foreseeable future. But this doesn't make the business a great prospect for investors to consider. If growth was coming in even stronger than it is today, you might be able to justify a lofty price for the stock. But the fact of the matter is that shares look very expensive at this moment. I wouldn't go so far as to downgrade the company to a 'sell' just because of how high quality it is. But if the stock rises much further from where it has without seeing a corresponding improvement in bottom line results, I could see things eventually coming to that. For now, the 'hold' rating I assigned the company previously still holds, if only barely.

For further details see:

Badger Meter: Shares Are Awfully Pricey Right Now