BAESY - BAE Systems: Big Order Book Is The Value Driver

2023-07-19 13:53:00 ET

Summary

- BAE Systems is a global company that provides defense, aerospace, and security solutions.

- Revenue has grown at a CAGR of 2%, although should improve to 4-6% as its order book increases.

- Margins are attractive and sticky, allowing the business to fund consistent distributions.

- Improving defense spending could be offset by macro conditions, but we doubt it due to the large order book.

- BAE's valuation does not imply an upside following the recent rally.

Investment thesis

Our current investment thesis is:

- BAE is a high-quality business with growth accelerating as its order book improves.

- Margins are attractive and should fund consistent distributions.

- Its commercial profile is improving as demand for defense improves.

- BAE's valuation does not suggest upside based on its historical trading.

Company description

BAE Systems ( OTCPK:BAESF ) is a global company that provides defense, aerospace, and security solutions.

The company operates through five segments, which include Electronic Systems, Cyber & Intelligence, Platforms & Services (US), Air, and Maritime.

Its products and services range from electronic warfare systems, navigation systems, cyber-harden aircraft, radars, and missile systems to combat vehicles, weapons, and munitions, ship repair services, and the management of government-owned munitions facilities.

Share price

BAE's share price performance has been mild for most of the decade, recently jumping on improved outlook and financial positioning.

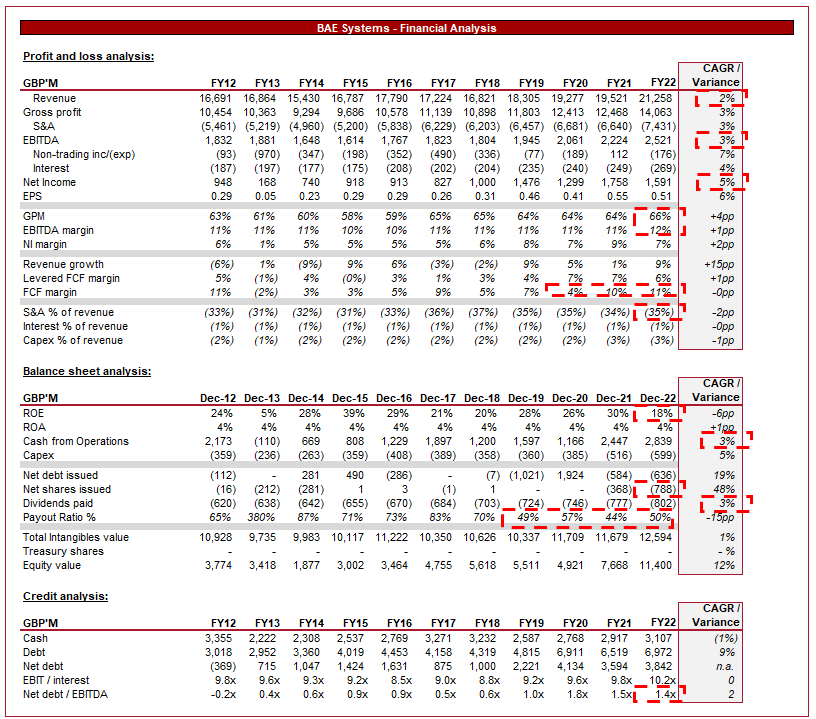

Financial analysis

BAE financial performance (Capital IQ)

{kind=link}

Presented above is BAE's financial performance for the last decade.

Revenue

Revenue growth has been mild with a 2% CAGR across the last 10 years. This is a reflection of what is a mature industry, during a period of military consolidation in the UK following the exit from Iraq and Libya (Although operations do continue against ISIL and others in the region).

Although defense is primarily a national industry globally, BAE is a top 10 prime contractor to the US, as well as the largest contractor in Australia and the UK. This is a reflection of the company's industry-leading capabilities, allowing it to access key markets to support British allies.

Revenue by geography (BAE)

The value here is that BAE is not reliant on the UK's defense policy, benefiting from diversification.

BAE can do this due to its wide range of expertise in complementary segments, as well as a strong track record of availability and delivery. There are very few companies globally that have the breadth of capabilities that BAE does, as well as the infrastructure to deliver flexibly. The majority of whom are US-based.

BAE key expertise (BAE Systems)

We are currently seeing geopolitical tensions rise following the Russian invasion of Ukraine and continued hostilities between the US and China. The former has caused a significant degree of uncertainty around Europe, with the threat of Russian encroachment into further European territory becoming a serious risk. BAE recently received orders from the UK Government to increase its munitions manufacturing due to a global shortage . Further, military-capable countries are supporting Ukraine with both old and leading equipment. The latter has taken a further step, as dominance over the Semiconductor market is bringing questions around Taiwan's safety to the forefront of political discourse. Countries around the world are looking to increase their military capabilities and are already increasing their spending. The largest example of this is likely the Germans, who are looking to increase their spending finally (following the Russian invasion) as a means of modernizing the dire Bundeswehr. BAE is positioned well to benefit from this increased spending.

With the increasing digitization of military and defense systems, there is an increasing need for cybersecurity solutions. We have seen the rise of military cyberattacks as a means of weakening opposing countries. The most famous example of this is Stuxnet, which is believed to be an American-Israeli malware that attacked Iran's nuclear development. BAE Systems has a strong cybersecurity division, which has won several large contracts in recent years. Further, the company recently acquired In-Space Missions, which gives the company access to Space.

In the most recent quarter, BAE announced a record order book, jumping an impressive 38% in a single year to £48.9bn (34% increase in backlog to £58.9bn). This is a reflection of heightened demand for military equipment as per our analysis, supporting the long-term health of the business. This should drive an outperformance in the coming 2-5 years, especially if this order book continues to grow as it has.

Economic considerations

Current economic conditions do not lend themselves favorably to BAE. We are experiencing heightened inflation and rising rates, which for consumers is contributing to a decline in activity. From a Government perspective, a slowdown economically usually leads to an increase in spending to support the economy, although this may come later once inflation comes down. This would mean reduced spending elsewhere potentially, Defense being one such option.

Further, as rates rise, the cost to finance defense also rises. Once again, this discourages spending, especially on a large scale, as the timeline for completion is long. Defense ministers are likely to defer spending until more favorable conditions.

This has the potential to impact the order book's growth, but underlying revenue will be supported by the current backlog, which will unwind as rates likely decline.

Margin

BAE's margins have remained flat across the historical period, with a slight improvement in NIM. This is a reflection of what is a competitive market, but primarily the nature of pricing Government contracts. The key here is that margins seem extremely sticky, which when partnered with contractual revenue, allows for predictability of income.

Balance sheet

BAE is conservatively financed, with an ND/EBITDA ratio of 1.4x. Our view is that a 3x level is a good maximum, but a company like BAE can afford slightly more due to the certainty of revenue and track record of delivery. This gives the company great flexibility to conduct M&A/organic growth, as well as improve distributions.

The increased FCF in the most recent years has allowed BAE to improve its distributions. The company has grown its dividend payments by 3% annually while reinitiating buybacks in FY21. With the increased order book, it is certainly possible buybacks become a mainstay, although given the lack of track record, this remains uncertain.

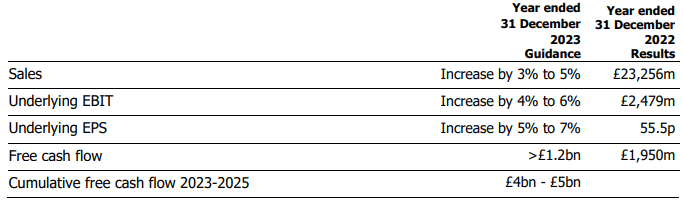

Outlook

{kind=link}

Presented above is Management's forecast for the coming year. Growth is expected to pick up, with margins also improving. Our view is that this is likely on the conservative side, as based on the order booked, we would suggest closer to 4.5-6.5%, although the top-end of this range would be predicated on an expansion of business above and beyond already achieved.

With FCF of c.£1.5bn, Management will likely rein in total distributions, although dividends can continue to grow at their current pace.

Valuation

Valuation (Seeking Alpha)

BAE is currently trading at a 14x LTM EV/EBITDA multiple. This is higher than its average multiple between FY16 to date.

The arguments implying an upside to the average are:

- BAE's order book is substantially larger, which creates greater certainty that growth will continue in the coming years.

- Management is forecasting some margin improvement.

- Geopolitical conditions have worsened.

The mean reversion argument would be:

- Future order book development may soften due to orders being brought forward. Without further quarters of data, it is difficult to argue either side.

- Distributions will likely decline in the coming year.

- The most recent share price rally has priced in the order book expansion.

- Economic risk is heightened and should be priced in.

Overall, our view is that BAE does deserve a premium valuation to the average, however, beyond this, we struggle to see the upside. The recent share price rally likely prices in the upside, leaving the business at its fair value.

Final thoughts

BAE is a high-quality business which in an industry where reliability and deep expertise are key, the company thrives. Revenue growth has been mild, but the recent increase in order book implies growth will improve. Margins are attractive and could improve in the coming year. The commercial profile of the business is attractive, as current market conditions do imply defense spending should improve. Our only issue is that the upside looks to be priced in.

For further details see:

BAE Systems: Big Order Book Is The Value Driver