BAESY - BAE Systems: Should Have Gone Long But Not Going To 'Buy' Now

Summary

- I started coverage on BAE systems officially back in November of last year. My first rating was a "Hold", which proved to be the wrong one.

- The stock has outperformed by around 2x since the time, seeing a bounce due to continued macro and good results. However, I don't see a 'Buy' being realistic here.

- While the industry is seeing strong trends here, I caution investors at going in too "late", as I see this being. I will show you why I'm still a "Hold".

Dear readers/followers,

I like updating on stocks, even when, as in this case, I took the wrong stance at the time of my last article. Since my initial piece, BAE Systems ( BAESY ) (BAESF) has outperformed. It doesn't really matter that my portfolio overall has done better than BAE, or that there are better upsides to be had, when a company does a 2x on S&P500, that's something you should have been invested in. I'm invested in several of BAE's peers and competitors, but not in BAE itself.

So, let's review what we have here, and what we can expect from the company going forward.

BAE Systems - Updating on the company for 2023

So, as we went through in the last piece, BAE Systems is a global defense contractor and defense company, with operations in the UK, USA and other parts of the world. It sells it projects to worldwide militaries, primarily Australia, Canada, Japan, India, Saudi Arabia, Turkey, Qatar, Oman, and also Sweden.

It's a relatively young business, at least in its current corporate structure, because it is essentially the merged British munitions/military company operations, together with what at the time was GE shipbuilding and electronics. For almost 25 years, the company has been in its current operations. It has a strong set of traditions, as BAE is pretty much what remains of what the company that built the Spitfire planes, and the like.

The company also was a prominent part of major recent projects, like the popular F-35, The Eurofighter, and other products that are prominently used in militaries across the world.

On a high level, BAE is exactly what you'd expect a defense play like this to be. What do we want? We want a well-filled order book, superb overall sales, solid underlying EBIT and margins as resilient as possible towards the current trend, a solid bottom-line FCF, and a good dividend paid from the company on an annual, stable, and historical basis.

BAE has all of this and more - with some very small exceptions.

The reason I took to calling this a "Hold" was due to valuation, not anything fundamentally wrong with the company. There is such a massive influx of orders and interest to these companies, that their cash flow multiples and other valuation indicators are currently far through the roof. You could make a case for why these trends, as they are now, will be sustained for perhaps a decade or more as the world "rearms" itself to face the threats of Russia and potentially China. However, the thing with growth bubbles is that they always seem to continue for a long time. A good example is the recent tech bubble. You'd have been hard-pressed to find many analysts (apart from me) that called for a reversal in the trends of work-from-home, digitization and remote office working that saw unicorn companies trade at unjustifiable multiples.

However, that's exactly what happened.

So, follow me here.

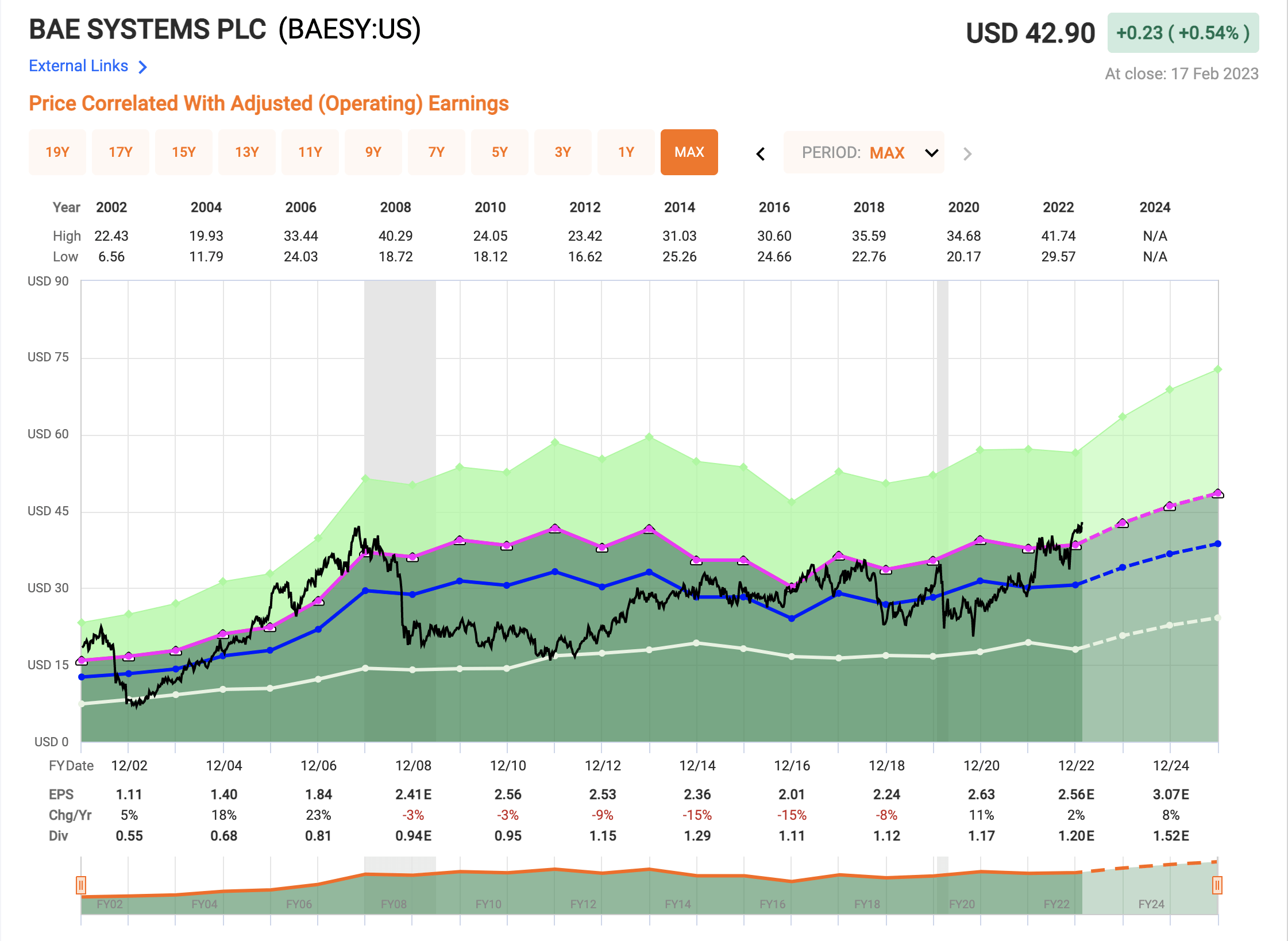

BAE is a company that over the past 20 years has averaged a growth rate of around 4.77% - so sub-5%. That's what I would consider "below par".

If BAE traded around 9-13x P/E, I'd be the first one shouting to "Buy" the business - it has a good 2.5%+ yield, it's BBB+ rated, it has contracts all over the world, and its earnings, while cyclical, have an underlying stability. But I want to show you what can happen in a period of 10 years when nothing really changes in terms of order flow and EPS.

{kind=link}

Do you see how long it took for BAE to recover from the valuations applied during the financial crisis? What's more, and let me make this perfectly clear, at any time in the last 20+ years , if you invested at a 15x+ P/E valuation, the net long-term result would have been negative or substandard TSR.

For instance, if you held the stock since it crashed prior to the financial crisis, you'd have returned a whopping 2.3% annual RoR, missing out on several hundred percent worth of growth in the meantime that we saw from the index.

In short, valuation matters - more on that in a bit. In fact, if you're a bit pickier in the period that you look at, you can see that on a 15-year basis following the recession, the company has averaged EPS returns of 1.59% - no more than that.

The latest results were still solid, and I expect nothing different in the next few quarters or years. As we can see from forecasts for BAE, the expectation here is significant and long-term outperformance due to unprecedented levels of demand not seen since 2001-2008.

Now, the company is set to report quarterly in a few days - but I don't see these quarterlies significantly changing my thesis on the company. If this turns out to be the case, I will revisit and edit this piece to accurately reflect this.

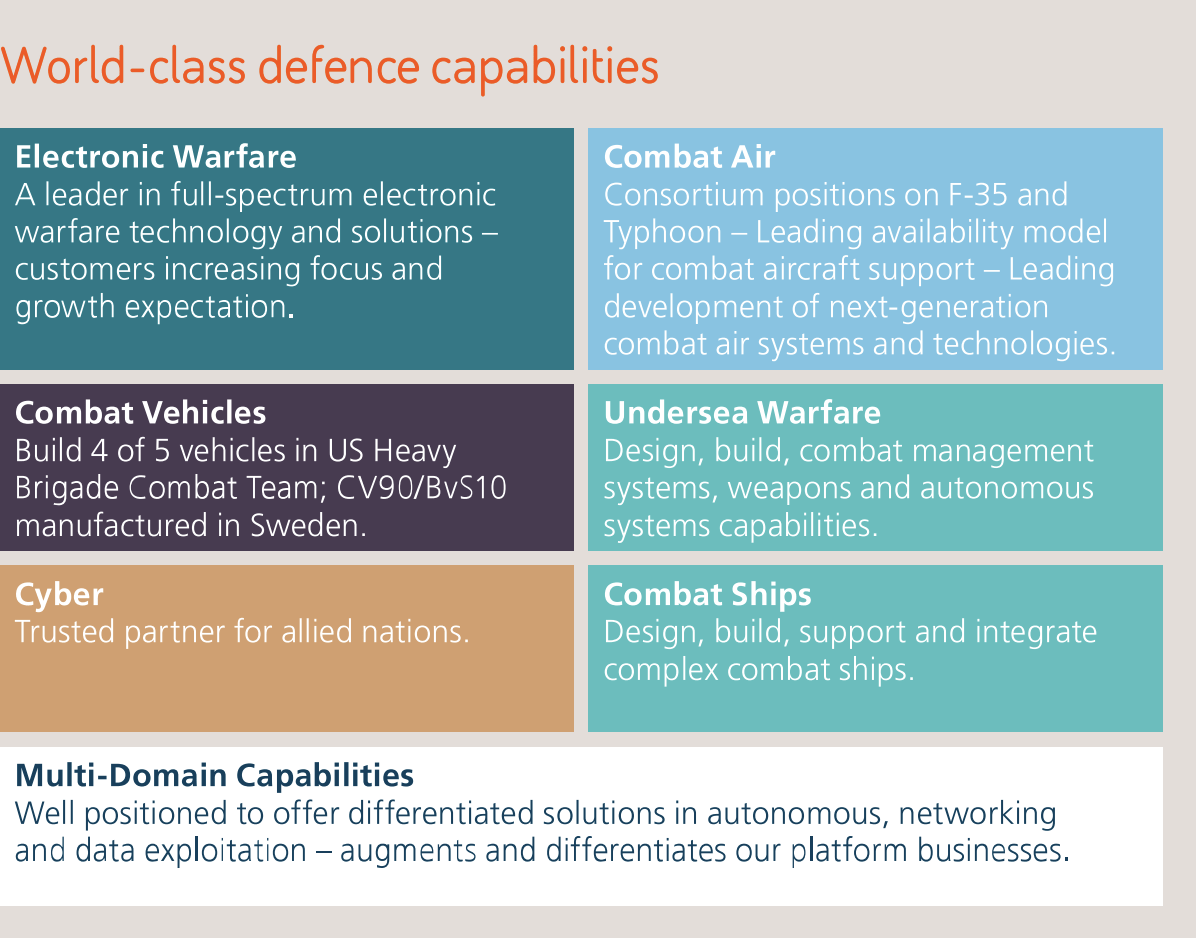

The advantages of BAE are clear. The company is a solidly-managed, dividend-paying military business with a great deal of interest in its products and services. It has several years' worth of attractive programs, with good visibility on what I would consider to be generators of profit and value. Like most of these businesses, the company's backlog is massive - £44B here, to be exact, and this is only a subset of expected through-life program values, meaning there will be service, maintenance, and other components for things like the F-35, Dreadnought subs, Typhoons, Frigates, and combat vehicles.

{kind=link}

BAE has good visibility on earnings for at least the next 2-3 years, barring unforeseen impacts from input costs and inflation. What's more, the company has an incredibly attractive overall portfolio, added to by a world-class diverse footprint in terms of sales, with most of its sales going either to US or UK.

{kind=link}

If you haven't looked into defense companies and spending and how this works, military spending is characterized by a decent amount of advance payments, an attractive mix of aftermarket and production value creation, and self-/customer-funded CapEx with a decent amount of franchise specificity. These characteristics tend to result in actual negative working capital , which is a rarity in any operating model. This is part of why I love investing in defense companies.

I have never lost money in a defense company investment. Ever. And I have invested in them for years - but the way I invest in them is when they're at the bottom of their cyclical trend - not at the top, which we're currently at.

Let's look at what this does in terms of the valuation appeal following the current outperformance.

BAE Systems - The valuation is not exciting

There's a fair bit of up and down to these stocks, including BAE, and long periods of time when the company really isn't performing in a stellar manner. Again, like most defense stocks. If you buy these things at a high price, you may be in for anemic returns for years, even decade/s if you're unlucky.

This is very similar to US defense stocks, where we can see several years of doldrums depending on how defense budgets and spending is looking. Peers like Lockheed Martin ( LMT ) and General Dynamics ( GD ) saw fairly similar trends as we see here in BAE, and this is not an advantage at this point.

I failed to foresee the most recent premiumization of BAE - last time I wrote about it, we were close to 15x - now we're closer to 17x. The reason this is so dangerous is that this company does not do well, historically speaking, in that sort of environment.

{kind=link}

The 5-year average for this company is closer to 12x - which is why I'm rating it a "Buy" at anything below 12x. I could even go so far as to go to 13x, given the 5-8% EPS growth that we're expecting in the next couple of years from the new orders BAE is seeing here.

But I am completely unwilling to go far beyond that. On a 15x P/E basis, at this time, even with growth taken into consideration, you're looking at a sub-8% annualized RoR, at 7.56%. That comes to 23.2% in 3 years. If you assign a 16-17x you can expect "great" returns of upwards of 10% annually.

Not so great, actually, given that you're essentially premiumizing a company by 3-5x multiples above normal to earnings, and are investing at an EPS yield of 6%.

My response to this is quite simple.

"No, thank you".

Targets and peer valuations are similar to the last time I presented BAE. Street targets for the native still call for a 5-7% upside from 15 analysts, most of which are a "BUY". However, I call your attention to the fact that these analysts tend to always premiumize BAE around 9-18% above where it trades, and the share price never reaches those targeted levels. As such, I would call them too exuberant for comfort here and would disregard such advice, focusing on the lowball targets in that range that come to around $35/share for the ADR - though even that is expensive enough based on historicals.

One flaw I do have as an investor is that I am insufficiently "quick" to change my view on companies that are going through a surge in interest, orders, or demand as a result of external factors or macro/micro. As a result, I as a rule tend to miss out on most of the surges in some stocks - including tech when it was boiling. I'm aware of this, and I'm weighing this up by allowing for what I see as realistic outperformance on the part of a company such as this.

So, BAE could outperform and stick to that 16-17x P/E - but you'd still only make barely double digits, and that's including the company's dividends, based on current forecasts.

Because of this limited growth rate combined with the historical relative instability, I see no reason to go higher than a 15x P/E on a forward basis here - I'd even prefer going lower. I can't say often enough how crucial it is that we focus on valuation as a core part of our investment strategy. Far too many people, and investors, miss out on looking not just at great businesses, but also at making sure they're getting them at great prices.

Because of all these things, I see BAE Systems as overvalued here, and my former thesis still stands. I don't change my targets easily, and I don't see a good reason to change them here.

Thesis

Here is my thesis on BAE Systems:

- The company is a solid international defense contractor with a presence in many attractive markets. It has a solid portfolio and a great long-term product upside. As a company, this business is as solid as it gets, with a well-covered dividend and great fundamentals.

- The valuation is absolutely core when you're looking to invest in a company like this - and the current valuation just isn't "there".

- Because of this, I consider the company a "Hold" here - not a "Buy".

- PT is $35 for the ADR to get a solid sort of upside here - and we don't have that.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The valuation criteria I follow aren't fulfilled here when normalizing and discounting the company "properly". For that reason, I'm not interested here.

For further details see:

BAE Systems: Should Have Gone Long, But Not Going To 'Buy' Now