BAESY - BAE Systems: Steps Up Shareholder Payout Drag On Executing Orders

- BAE Systems' total yield is stepping up to more than 4% per year with dividends and buybacks.

- Order intake creates huge backstop for the company, but execution in this higher-threat environment is not happening due to supply-chain issues.

- C&I is up because of acquisition effects.

- Tempest is likely going to be the more successful European NGF programme but BAE is expensive considering execution still matters.

BAE Systems ( BAESF ) ( BAESY ) is one of the several European defense stocks that have been a major beneficiary in the current higher-threat geopolitical environment. It remains elevated, and while it is obvious that defense is a safe end-market come whatever may, we think limits on execution make the increased backlog rather little comfort, and not enough to justify the elevated levels that BAE trades on. While we aren't so impressed by execution, we acknowledge that for the dividend investor, the capital return program is becoming increasingly generous. On an income basis, the yield is good and highly defensible, we just don't see capital upside here where we do in other areas.

H1 2022 Results

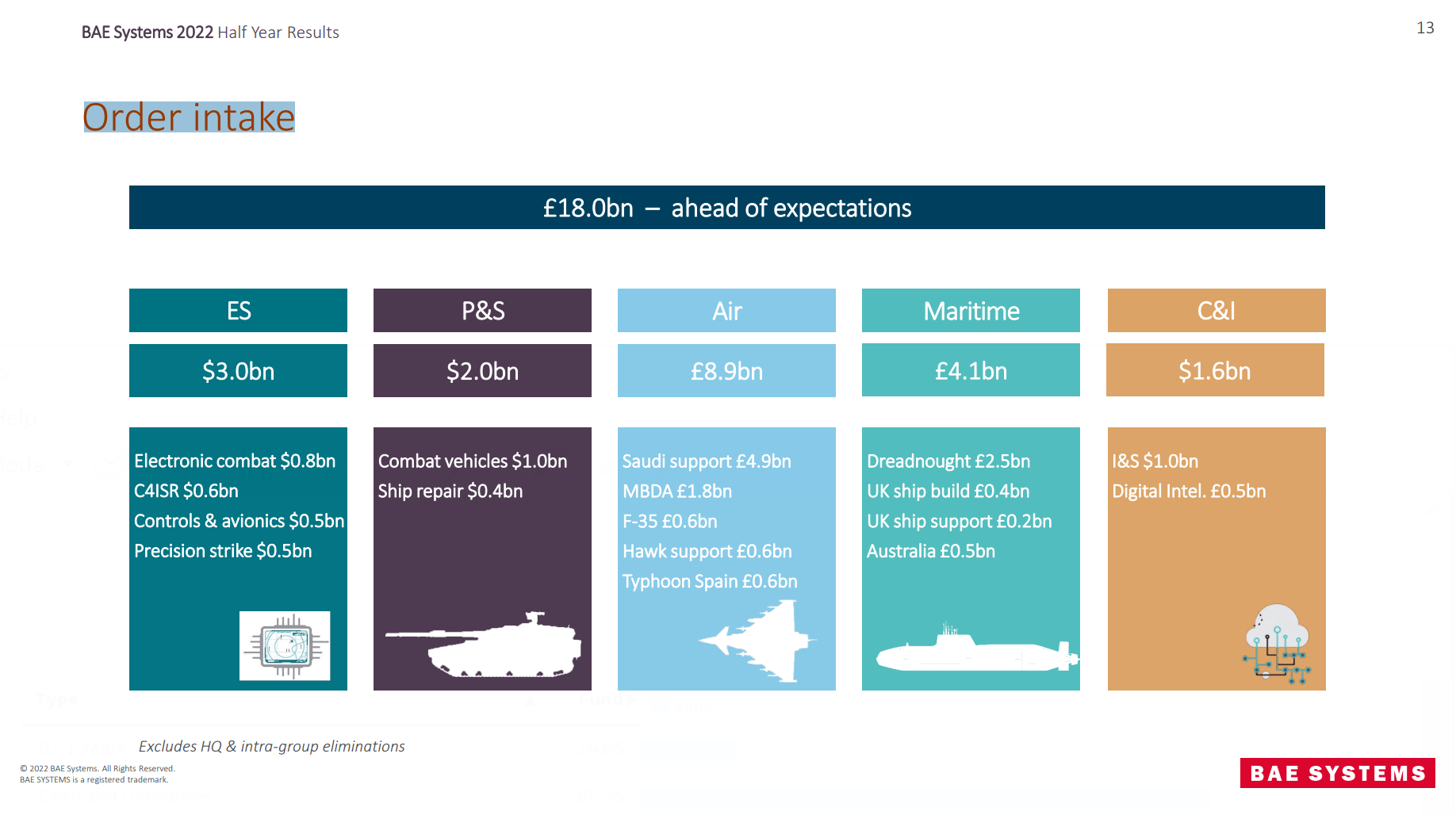

The H1 results have recently come out, and they give us a fair bit to discuss. Firstly, we note the massive growth in order intake thanks to the Ukraine invasion, which has had countries like Germany but several others expanding (or in the remarkable German case renewing) their fleets a geopolitical threats become more apparent. Air was indeed the biggest beneficiary, beyond even its sales representation in the mix, followed closely by maritime. This makes a lot of sense, given that land support is unlikely to be deployed by most NATO countries who don't border the east, where threats are becoming increasingly perceived, obviously to the detriment of everyone except defense companies.

{kind=link}

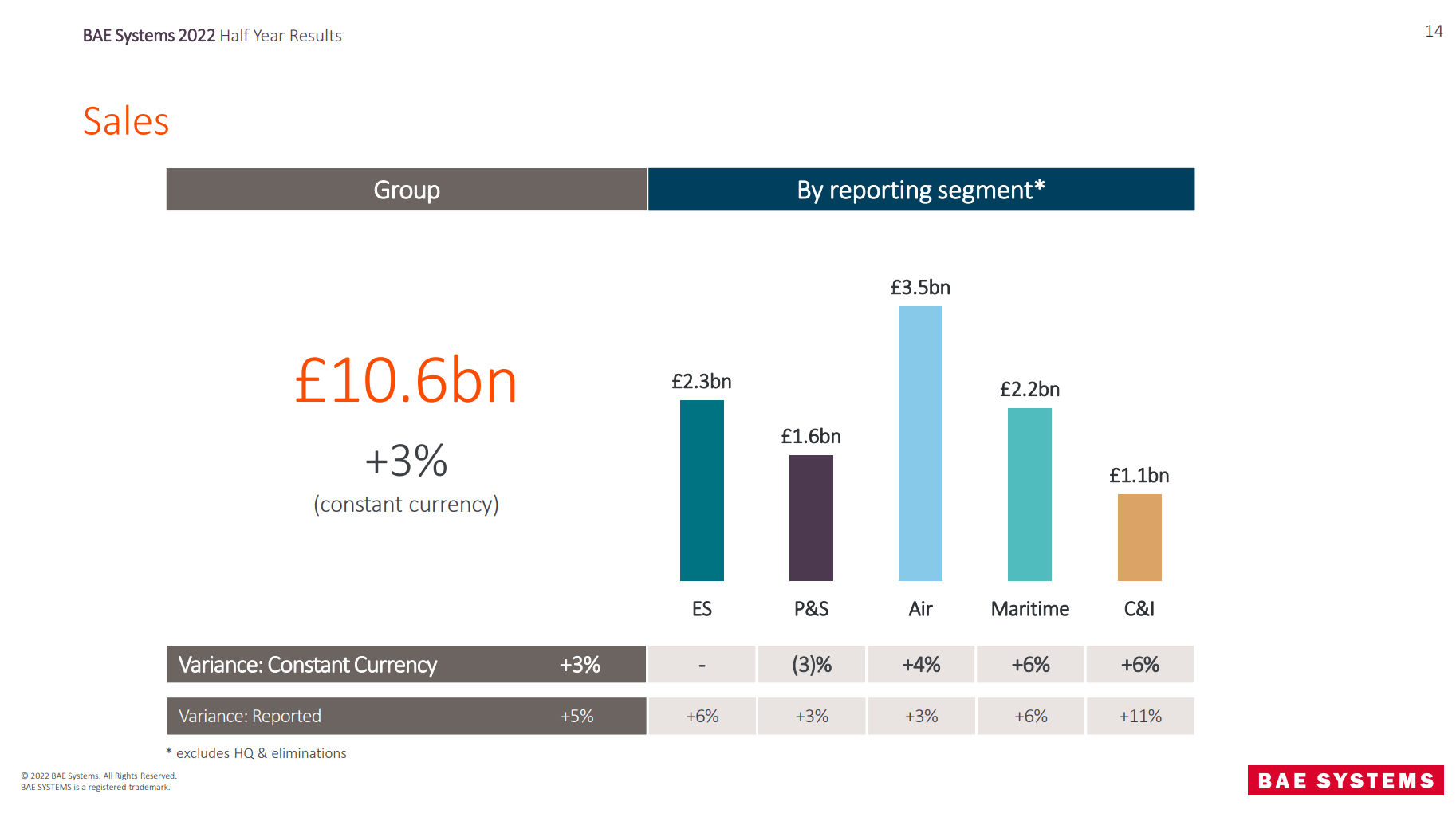

While order intake is massive, and almost doubled relative to a resilient 2021 with backlogs now swelling, execution did not follow and the backlog is being liquidated at the same rate as before.

{kind=link}

The electronics segment ((ES)) was highly bothered by semiconductor shortages, and could not execute growth despite the demand picture. Likewise, labor shortages affected the land defense business (P&S). Air managed to move forward despite new problems with titanium shortages thanks to completed Typhoon deliveries with Qatar and execution in the F-35 program. Maritime grew on volumes, which is nice, and finally C&I grew on acquisition effects and its growth should be ignored.

Conclusions

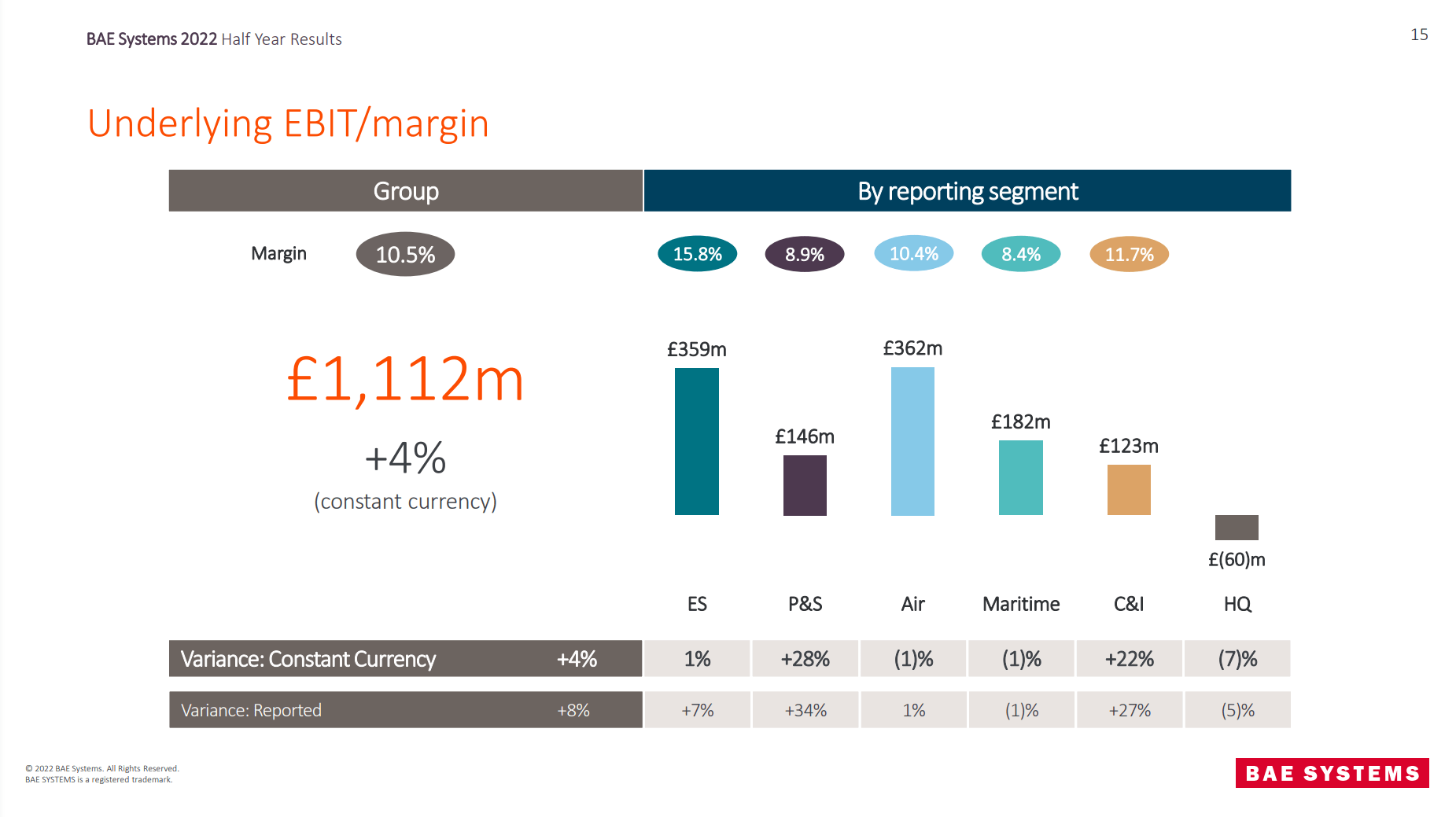

Order intake grew and the backlogs are massive. End-markets are durable too. But when there's no execution, does it make a difference? If anything, slow liquidation of backlog could render those signed contracts underpriced as inflation evolves. Moreover, execution wasn't very exciting on the margin side either. On a constant currency basis, every segment saw declines absolute EBIT. The only exception was the land defense business (P&S or platforms and services), which saw increased operational performance and more service type arrangements in the mix that typically command higher margin. This increase in EBIT is impressive, and hopefully sustainable, but the pressures on the rest of the business are likely to remain rendering the backlog unlikely to convert particularly more valuably into cash flows. Essentially, despite the core geopolitical tensions, BAE has not managed to grow results more considerably. We are not particularly impressed by the security of growing backlog; we never thought defense needed it.

{kind=link}

There are of course positives, but none that connect to or explain the current elevated level in price that BAE has sustained since the invasion where it rose over 50% YTD. The Tempest programme is better positioned that Dassault and Airbus' ( EADSF ) which has far more political issues in execution due to all the stakeholders. In fact, that programme has not made any progress really and is likely to fragment into a French camp and then the rest. So Tempest will probably dominate Europe once it comes online as a revenue generator in the 2030s. Also, the shareholder payout situation is also more favorable than before. The buyback yield is 5% over the next 3 years, and the dividend yield currently runs at 3.2% and had grown 10%, which is great for income investors. Also the price is still not exorbitantly high for the stock at 19x, but not that compelling either. But given that there are things on sale where fundamental performance is better positioned for improvement, we'd pass on BAE.

For further details see:

BAE Systems: Steps Up Shareholder Payout, Drag On Executing Orders