BAESY - BAE Systems: We Wouldn't Complain About Ball Aerospace

2023-08-17 15:21:15 ET

Summary

- BAE Systems plc is set to acquire Ball Corporation's aerospace division in an all-cash transaction valued at around $4.8 billion.

- The acquisition will increase BAE's exposure to intelligence systems, particularly satellite and geospatial intelligence systems.

- We see the price as fair, considering the high growth and cash generation of Ball's aerospace division.

- The market's negative reaction is overdone, and this is probably a decent buying opportunity.

BAE Systems plc ( BAESY , BAESF ) just announced that it will acquire Ball Corporation's ( BALL ) aerospace division in an all-cash transaction that values the business at $5.55 billion . Markets are not loving the price tag, apparently, but we don't especially object to the multiple, which seems to be fair value for a pretty high growth and cash generative business that increases BAE's exposure to intelligence systems with a particular focus on satellite and geospatial intelligence systems. The value looks less fair when not including a tax benefit associated with the transaction in favor of BAE, but in light of it and the growth profile of Ball Aerospace, things actually look pretty good. We think that the Ball addition adds secularly growing segments to the BAE portfolio, and really is no source of any special dis-synergy or a typical example of poor capital allocation.

Quick H1 Review

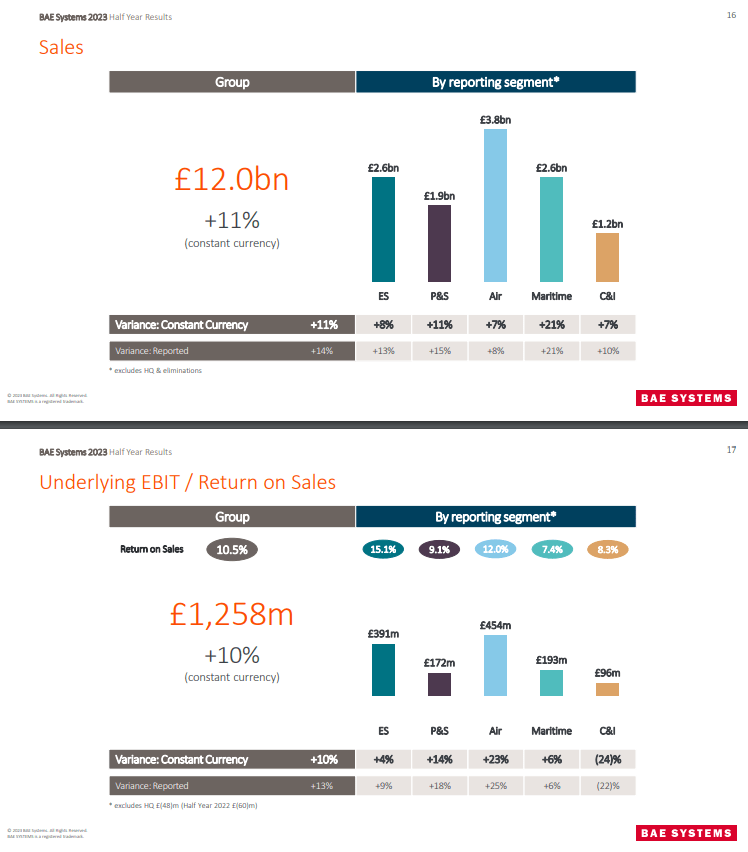

Let's start with a quick H1 review before discussing Ball.

{kind=link}

Let's start with where margin performance was relatively poor compared to sales. Maritime struggled on margin since it's making incremental revenue on the Dreadnought program which is currently self-funded in R&D and also in a more profit controlled stage of the life cycle. ES struggled due to fixed price contracts while seeing pass-through from semiconductor and electronics from last year's continued semiconductor shortage. C&I is down from major R&D investment.

Air is getting more funding from the UK government for the new Tempest program, which is likely to win out in Europe among the NGF initiatives. Mainly, the margin improvement is from the fact that as programs with a nation matures for the Typhoon in this case, associated risk allowances can be retired improving margins. But there will be more headwinds in sales from the contracts with Qatar as the programs mature and start to produce less revenue. The Typhoon is getting a bit old now, with Tempest being part of the next wave. There was around a 5% sales headwind from Qatar drop-off as a run-rate for FY 2023 compared to 2022, so the fact that there is overall growth in sales has been impressive. P&S did well with a recovery in U.S. ship repair and restock as the U.S. Navy toned down movements at this stage after the Ukraine war, allowing ship repair contribution to return to the mix. Also, the complexity of projects has gone down YoY in ship repair which is going to help the P&S business turnover more profits this year.

There's a decent amount in the pipeline thanks to new NATO additions, with Sweden getting interested in the CV90, and the generally greater concern around defense and more incentive for European nations to commit to the NATO targets for defense spending as part of members' budgets.

On Ball

The Ball acquisition creates some tax benefits which has reduced the expected price from around $5.5 billion to $4.8 billion. Excluding synergies, that pegs the multiple at around 15.4x EV/EBITDA. Considering potential synergies, that multiple could come down another 10% . It's not particularly cheap, but the CAGR of Ball's aerospace division, which is focused on satellites and geospatial intelligence as well as other sensors and intelligence systems, is high enough to warrant a double-digit multiple.

{kind=link}

{kind=link}

EBIT has doubled since 2017. 15x is not atypical of defense exposures, although it is a little more premium than the average which is around 12-13x EV/EBITDA.

Still, markets have some concerns given the more than 4% price declines of BAE Systems since open. That implies about $1.7 billion in dis-synergy and/or overpayment in the acquisition based on the valuation change today. $1.7 billion on the $4.8 billion is 35%. There is no way that a fair consideration for Ball would be $3 billion, or in other words that BAE overpaid by 50%, given that even 15.4x is not that much of a stretch.

What I hear from industry insiders as well is that Ball was pushing more mechanical and electrical engineers lately as well in recruiting, meaning that they are positioning more as an R&D firm with a broader talent pool and a deeper and more integrated intelligence offering. Given the nature of their services focused on sensors and intelligence systems, that makes some sense, and also explains their pretty low D&A intensity of around 20% of EBIT and their decent cash generation profile of around 65% on EBITDA.

It makes sense for BAE Systems plc to be doubling down on their internal investment on C&I, with some M&A to mature the business and position them to provide a next-generation suite of defense technology. We see no major problem with the price, and definitely think the markets are overreacting meaningfully with today's drop.

For further details see:

BAE Systems: We Wouldn't Complain About Ball Aerospace