XOP - Baker Hughes: The LNG Boom Can Be A Catalyst For This Stock

2023-08-13 07:14:21 ET

Summary

- Investment in liquefied natural gas has greatly stepped up since 2022 when Europe lost its access to piped gas from Russia.

- As a supplier of gas turbines and other related equipment, Baker Hughes is positioned to benefit from the LNG trend.

- Baker Hughes' oilfield service business is also benefiting from a renaissance in upstream capex, particularly internationally and offshore.

- I am structurally bullish on the oilfield services sector, including Baker Hughes' competitors Schlumberger and Halliburton, among others.

Investment thesis

Baker Hughes Company ( BKR ) is one of the largest providers of oilfield services and equipment ("OFS") globally. It competes with the other two OFS majors, Schlumberger ( SLB ) and Halliburton ( HAL ), as well as multiple lower tier and regional OFS players.

Structurally, I am very bullish on OFS stocks ( OIH ), particularly those with offshore or international exposure, or even select North America onshore service providers that differentiate themselves through state-of-the-art technology or a more robust customer base.

In addition to checking the offshore and international boxes, Baker Hughes also has a large industrial and energy technology ("IET") business that supplies equipment (e.g., gas turbines) and services to the liquefied natural gas ("LNG") value chain.

As bullish as you may be on oil, you have to acknowledge that a recession will temporarily bring down oil prices and investment. However, that isn't the case for LNG infrastructure, at least not since February 2022, when the Russia-Ukraine war started and led to Russian gas supplies to Europe getting cut off.

In a sudden change of heart, governments started to worry about energy security, which has led to a record number of LNG final investment decisions ("FIDs"), both on the export (liquefaction plants) and import (regasification) sides (shipyard orders for LNG tankers are also at record highs). In a paradoxical move, perhaps underscoring how politically driven the whole energy transition debate has become, the EU parliament even voted last year to label natural gas as green .

Oil isn't robust to consumer (gasoline, jet fuel) or industry (petrochemical) demand but natural gas is less cyclical due to its use for power generation and heating. As Europe and Asia are short on gas, that gas has to be brought from elsewhere and this requires investment in LNG infrastructure. No matter which way things go for oil, the LNG boom will continue to be a tailwind for Baker Hughes.

Why should you invest in OFS stocks?

I have laid out the macro foundations of my OFS thesis in prior articles:

OIH: OPEC Cuts Bolster The Case For Oilfield Services (NYSEARCA:OIH)

Oilfield Services Update: Offshore And International Make Up For North America Weakness

The cornerstone of the OFS bull thesis is that we find ourselves in the early stages of a multiyear capex cycle, not unlike 2002-2014, and will see increased spend across the energy value chain while the services capacity remains tight due to 2014-2020 attrition.

The initial recovery in energy equities post-pandemic left the OFS sector behind:

Back in 2021, the mainstream narrative was that upstream producers ( XOP ) would shy away from new investment while gradually depleting their developed production base to maximize oil price realizations and cash flows. Under this "capital discipline" model, OFS would see limited gains.

However, this narrative wasn't fully correct. Since 2022, OFS stocks have performed relatively better than upstream:

Apart from the energy security wake up call, there are a couple other reasons why the narrative has shifted from "capital discipline" to "capex supercycle":

- Much of the international expansion is driven by national oil companies ("NOCs") that are fulfilling government mandates; for example, Brazil's Petrobras ( PBR ) has gotten attention with its record orders for offshore rigs (RIG) and floating production systems. As much as Petrobras is trying to maximize its profits, it is also ensuring that Brazil ( EWZ ) has adequate oil supply for the coming decades.

- The ability of North America's independents to maintain production with "flat capex" turned out to be a bit of a hoax in my opinion. It's now clear that they accomplished this in 2021-2022 largely by tapping into their drilled but uncompleted well inventories which are now at abnormally low levels.

- Signs that U.S. shale is peaking , or at least plateauing, are incentivizing long-cycle international investments that may take up to 5-10 years to develop and therefore require some certainty that short-cycle supply won't ramp up and impair the pricing economics.

- The attractiveness of offshore investments has improved because of the opportunities to leverage existing infrastructure (brownfield investments) and other efficiencies; SLB now famously claims that 85% of the offshore FIDs have oil price breakevens below $50.

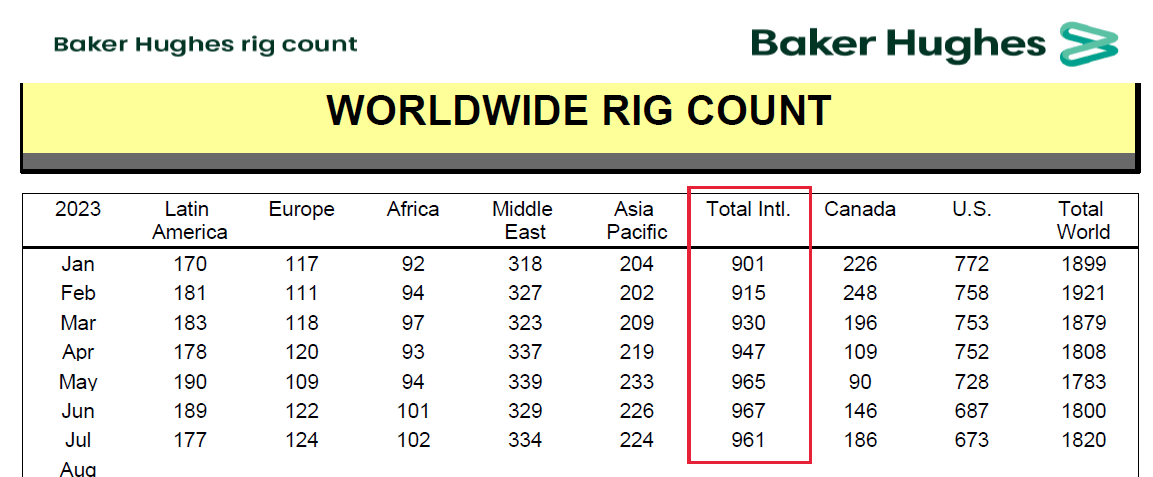

Right now, U.S. drilling rigs, considered a profit driver for much of the OFS industry, are down:

This weighs on the OFS sector although the U.S. is more of an outlier here. International rigs aren't down :

{kind=link}

Even U.S. offshore rigs aren't down:

The negative press for OFS is largely reflective of U.S. shale where mostly smaller, private operators were forced to reduce rigs:

Evercore; WSJ

Outside of North America, there are few signs that OFS demand is stalling.

The golden age of LNG

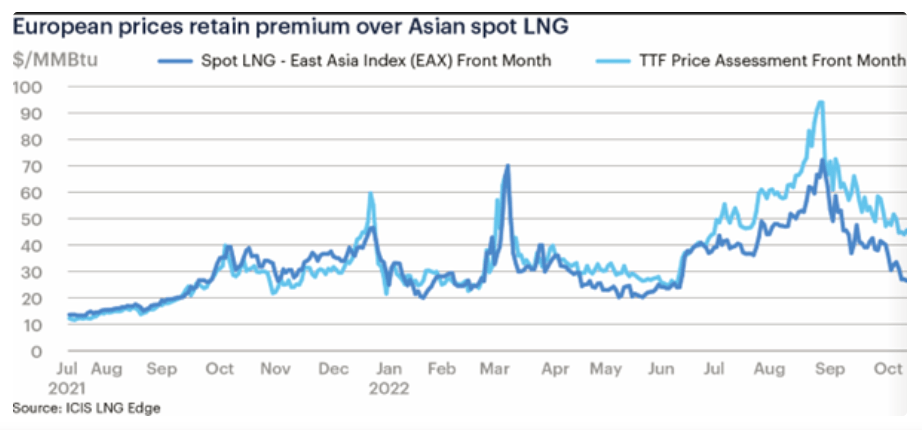

Natural gas makes a lot of sense as a transitional fuel. It emits almost 50% less carbon than coal, provides reliable baseload and is fairly abundant. Pipeline infrastructure achieves a lower transportation cost than LNG, but as the European woes last winter showed, pipelines also create mutual dependency on both sides of the trade. In contrast, LNG allows an importer to source from multiple potential suppliers and the spot trade as a proportion of total volumes has been increasing over time.

Unfortunately, it took European gas prices skyrocketing to $100 per MMBtu (equivalent to $600-barrel oil) for policymakers to understand the benefits:

{kind=link}

In the typical reactive fashion of our age, we are now looking at record investments in the LNG sector. According to the International Gas Union's 2023 LNG report (my highlights):

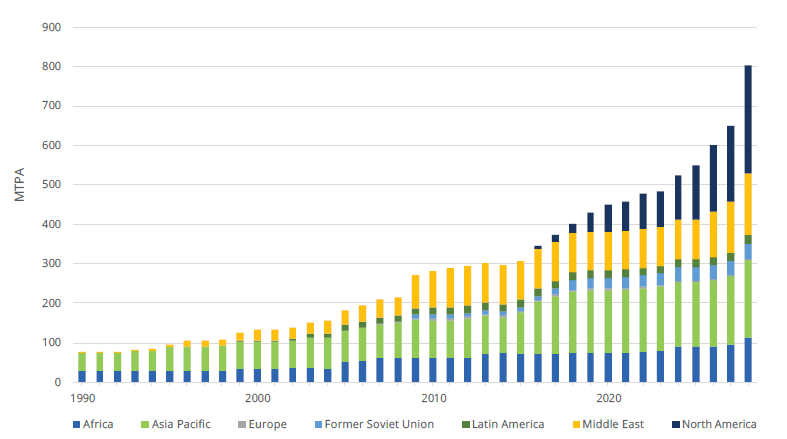

Currently, 997.1 MTPA of aspirational liquefaction capacity is in the pre-FID stage. Most proposed capacity is in North America (611.4 MTPA), with 333 MTPA situated in the US, 229.6 MTPA in Canada, and 48.8 MTPA in Mexico... Overall, the market upheaval caused by the Russia- Ukraine conflict has stimulated interest in liquefaction facilities as markets seek to re-establish energy security priorities , while balancing decarbonization goals.

For context, the 2022 LNG trade was about 400 MTPA (metric tons per annum) or about 50 bcf/d. Adding close to 1000 MTPA would basically triple the potential market size. For further reference, U.S. total gas supply runs at about 100 bcf/d and the global market (LNG and non-LNG) is probably about 400 bcf/d now. In other words, LNG could expand from 10-15% of the global gas market to more than 30%.

Investment is going strong on the regasification (import) side too:

Many other European markets are planning a wave of LNG import terminals following heightened geopolitical tensions as they look to reduce dependency on Russian gas and strengthen energy security . Four regasification projects were commissioned in Europe in 2022: one in Germany, two in the Netherlands and one in Finland. Four terminals have come online in Europe so far in 2023, with another three terminals and one expansion kicking off construction in the region and aiming to commission later in 2023. There has been a notable trend in Europe towards floating terminals given their ability for redeployment and speed to market compared to onshore terminals.

Much of the new liquefaction (export) capacity is expected to come from North America, mostly the U.S. but also from some important steps in Canada:

Rystad; International Gas Union

{kind=link}

The LNG trend isn't easy to convert into an investable idea. Many LNG projects are joint ventures among oil majors, utilities and even private investment. Some "pure play" ideas include Cheniere ( LNG ) on the liquefaction side or New Fortress Energy ( NFE ) and Excelerate Energy ( EE ) on the regasification side.

However, as much as spot volumes are growing, the majority of the LNG trade is still a long-term business with offtake contracts going up to 20 years. So for Cheniere, New Fortress or others the return on their capex will get realized over a longer time period. Instead, through Baker Hughes we can approach LNG from a different angle and focus on the LNG equipment orders that will be frontloaded.

In these times of "greenflation" and rising raw materials costs it is perhaps also prudent to side not with the developer but with the contractor - or even the supplier to the contractor as BKR doesn't itself construct the LNG terminals. Baker's competitors in the space are mostly general industrial firms such as Siemens on Mitsubishi, for which LNG would be a very low contribution to the profit line.

How does Baker Hughes profit from LNG?

LNG featured prominently during Baker Hughes' last earnings call :

The continued strength in long-term LNG contracts has been a key driver of the momentum in industry FIDs, which have now totaled 53 MTPA so far this year. This includes the recent FIDs for Phase 1 of Next Decade’s 17.6 MTPA Rio Grande project and Qatar Energy’s 16 MTPA North Field South project.

Based on the continued development of the LNG project pipeline, we still expect the market to exceed 65 MTPA of FIDs this year and should see a similar level of activity in 2024. We continue to see the potential for this LNG cycle to extend for several years with a pipeline of new international opportunities expanding project visibility out to 2026 and beyond.

The company is converting the macro pull into orders and backlog, including the Rio Grande FID which was announced recently by NextDecade ( NEXT ):

In IET, we saw another excellent quarter commercially, with $3.3 billion in orders, maintaining the strong momentum from the first quarter. Gas Tech Equipment achieved $1.6 billion in orders, driven by multiple areas, including almost $900 million of LNG awards in the quarter.

In LNG, Baker Hughes booked an order for three Main Refrigerant Compressors for NextDecade’s Rio Grande LNG project in Texas. Baker Hughes will supply Frame 7 turbines paired with centrifugal compressors across Rio Grande’s first three LNG trains in a parallel configuration arrangement, providing more operational flexibility.

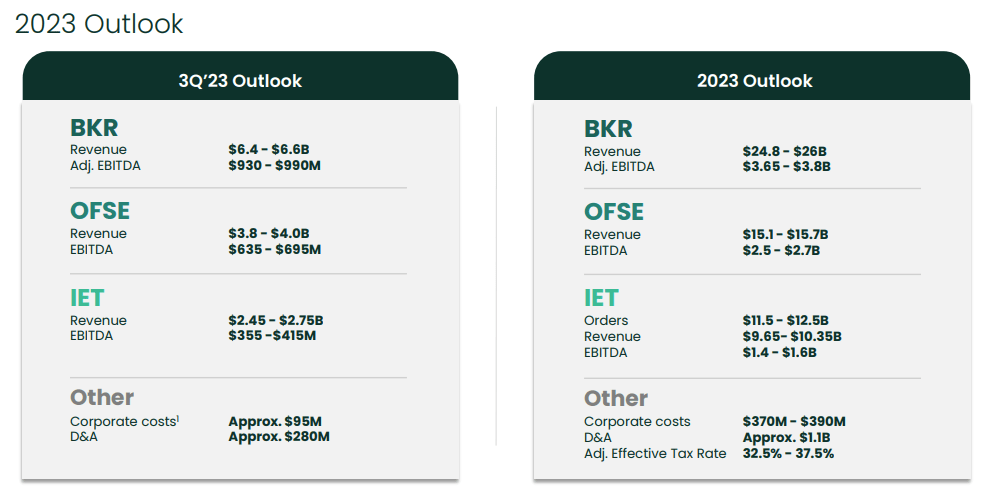

In fact, BKR went on to increase its guidance for the IET segment:

Our full-year outlook for IET remains constructive for orders, revenue, and EBITDA. For orders, we have increased our 2023 expectations by $1 billion to a range of $11.5 billion to $12.5 billion. We feel confident in meeting the upper end of the revised range and see the opportunity to exceed the high-end depending on the timing of certain large projects.

The IET segment which serves the LNG industry is still smaller than the OFS offering by EBITDA:

{kind=link}

However, IET is quite material and a differentiator from SLB or HAL. Further, Baker's management says that 73% of the OFS revenue is international, which means it should also benefit from the long-cycle upstream capex boom.

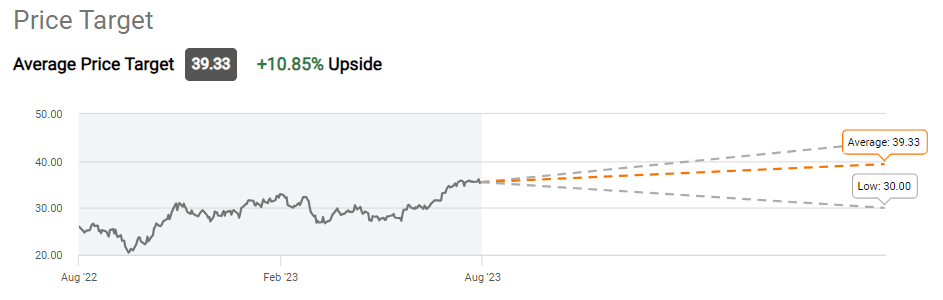

Valuation and risks

Wall Street gives only 10% upside to BKR:

{kind=link}

I think there may be more upside. Consensus revenue estimates are $28 billion for 2024 and almost $30 billion for 2025. During past OFS cycles, the OFS majors have been able to expand their EBITDA margins to 20%:

This implies BKR can achieve $5.5 to $6.0 billion EBITDA. Historically, when things were good (that is, EBITDA was already high), valuations were in the 8 to 10x range:

At 9x EBITDA of $5.5 billion, Baker's EV would be close to $50 billion. This implies 30% upside for the equity.

The risks? I think at a macro level the LNG exposure de-risks Baker Hughes compared to SLB or HAL. However, investors should watch if management is able to control the corporate overhead. So far, BKR hasn't been able to replicate the cost reductions seen by its peers:

Baker Hughes has been through a number of reorganization efforts, namely the failed merger with Halliburton in 2016 and the merger with GE's oil and gas unit in 2017 (which brought in the LNG business), followed by the spin off from GE.

These efforts can add cost, advisory fees for external consultants and be a distraction for the employees:

{kind=link}

This is what management said on the earnings call:

We continue to drive actions to optimize our corporate structure and drive higher margins and returns. While reducing costs is one lever, we are also fundamentally re-wiring the organization to simplify reporting lines, eliminate duplication, and taking measured steps to upgrade our financial reporting systems. We believe this will lead to more standardization, increased automation, and provide greater real-time information and analytical capabilities around our business performance.

We'll have to see when they are done "re-wiring the organization." In my view, achieving a steady organization state is a necessary condition to control the overhead.

Bottom line

Baker Hughes can be an interesting idea in the OFS space for up to 30% upside if things go well. While rivals SLB and HAL are more of bets on upstream oilfield spend, for BKR the exposure to rising investment in LNG infrastructure is a differentiator. The ongoing record FIDs in this space can be a catalyst for the stock.

For further details see:

Baker Hughes: The LNG Boom Can Be A Catalyst For This Stock