BALL - Ball Corporation: Aerospace Divestment Should Create Shareholder Value

2023-10-26 02:48:34 ET

Summary

- Ball Corporation plans to divest its Aerospace segment for net proceeds of $4.5 billion, creating more focus on its Beverage Packaging segment.

- The company has been able to grow quite consistently in the company's history, with mostly stable margins.

- I believe that the current stock price reflects Ball Corporation's fair prospects, constituting a hold rating.

Ball Corporation ( BALL ) is planning to divest its Aerospace segment. The divestment seems to be a value creating prospect for the company, as BAE Systems seems to pay a very good earnings multiple for the business. Ball Corporation will be left with the company’s stable Beverage Packaging segment, creating more focus on the segment. I believe that the company is currently priced fairly, constituting a hold-rating.

The Company & Stock

Ball Corporation operates through two main segments – Beverage Packaging and Aerospace. The Beverage Packaging segment focuses on aluminium packaging mostly for the beverage industry. The segment’s customers include large companies such as Coca-Cola, Carlsberg, PepsiCo, Heineken, Kroger, and Constellation Brands. On the other hand, the Aerospace segment manufactures and sells spacecraft sensors and radio frequency systems among other technologies for customers such as NASA, Boeing, and Raytheon. Of the segments, the Beverage Packaging segment represents the clear majority of revenues with around 81% in the last twelve months:

Sales Segments (Ball Corporation Agreement To Sell Ball Aerospace Presentation)

In August, Ball Corporation announced that the company is divesting the Aerospace segment in a sale to BAE Systems. The companies agreed on a price of $5.6 billion in cash, that corresponds to after-tax proceeds of $4.5 billion for Ball Corporation. The price for the segment seems very good in my opinion – the agreed-upon price corresponds to an EV/EBIT of 27.1 with trailing numbers as of Q2 according to Ball Corporations divestment presentation . The company’s trailing EV/EBIT currently stands at 18.9, significantly below the divestment multiple. In addition, the divestment adds to Ball Corporation’s focus around the beverage segment. Ball Corporation plans to use the proceeds of the divestment for $2 billion in debt reduction, and a similar amount for share repurchases.

The stock market doesn’t seem to appreciate Ball Corporation’s divestment as the stock has been falling since August:

{kind=link}

One-Year Stock Chart (Seeking Alpha)

Financials

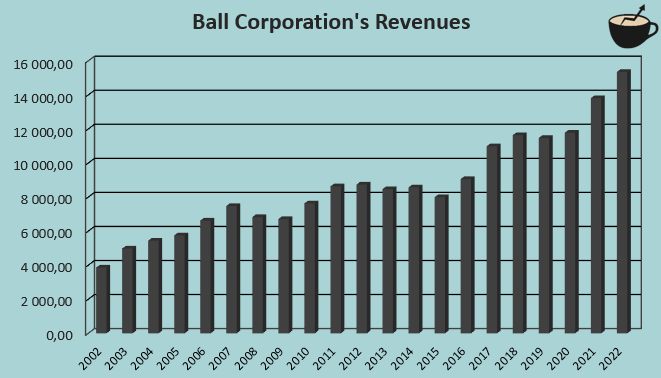

Historically, Ball Corporation’s growth has been quite good. The company has achieved a compounded annual growth rate of 7.1% from 2002 to 2022 mostly with organic efforts, as the company’s cash acquisitions are quite infrequent.

{kind=link}

Author's Calculation Using TIKR Data

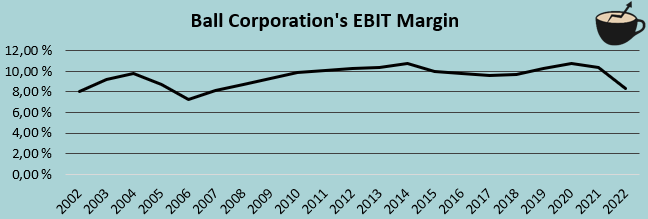

Ball Corporation has achieved a mostly stable EBIT margin throughout the company’s long-term history. From 2002 to 2022, the company’s average EBIT margin has been 9.5%:

{kind=link}

Author's Calculation Using TIKR Data

The company has seen slight margin pressure as the trailing margin currently stands at 8.6% and was 8.4% in 2022.

Ball Corporation’s balance sheet is currently quite heavy on debt. The company has around $9.4 billion of long-term debt, of which $1.9 billion is in the current portion. In addition, the company has $0.4 billion in short-term borrowings. Compared to the company’s current market capitalization of $14.4 billion, the debt balance seems quite large. After the divestment of the Aerospace segment, the debt balance is planned to be partly paid off, but still leaving a leveraged balance sheet for the company.

Valuation

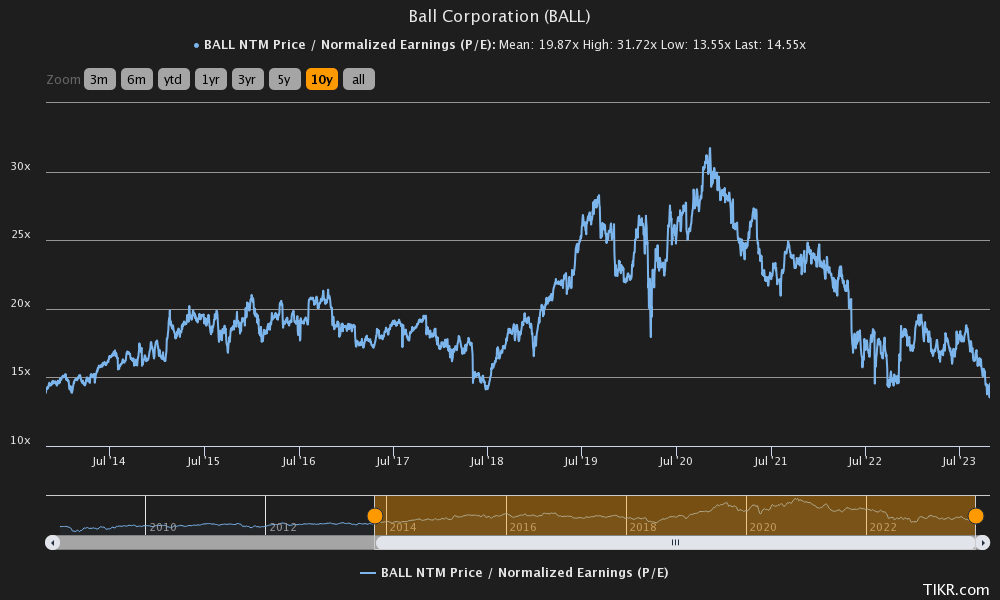

Currently Ball Corporation trades at a forward P/E of 14.6, below the company’s ten-year average of 19.9:

{kind=link}

Historical Forward P/E (TIKR)

The P/E ratio alone doesn’t tell too much about a company’s valuation. To further analyse the valuation, I constructed a discounted cash flow model as usual.

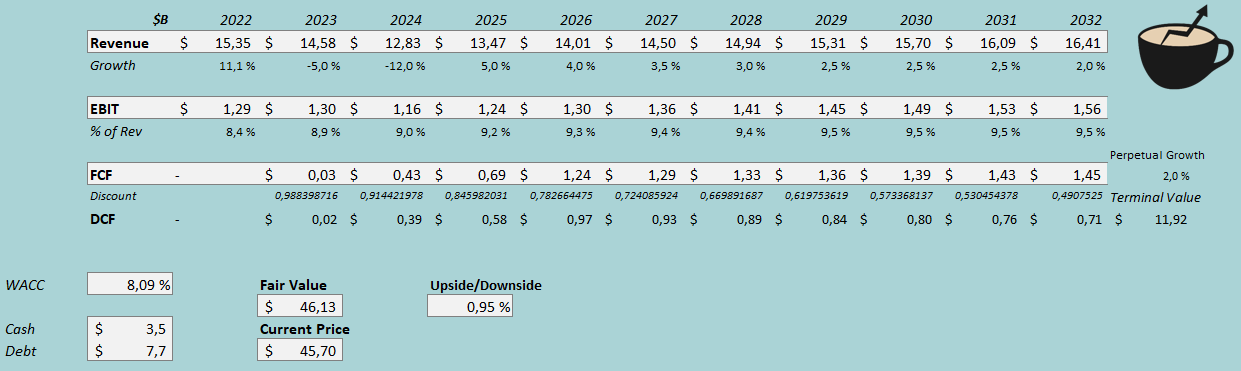

In the model, I estimate Ball Corporation’s revenues to fall by 5% in 2023, implying quite stable revenues in H2 as in H1 the company’s revenues fell by -10.1%. After the year, I estimate the divestment of the Aerospace segment to happen at the start of 2024 to simplify the model. I added the sale proceeds into the cash balance, and moved $2 billion of the sum into debt decreases. For the revenues, I estimate -12% for the year, signifying very slight organic growth as currently the Aerospace represents 14% of total revenues. After 2024, I estimate Ball Corporation’s growth to be 5%, that slows down in steps into a perpetual growth rate of 2%.

I believe that the company can still achieve a very slightly higher EBIT figure than in 2022, as in the first half the company’s EBIT margin increased slightly – the estimated margin represents a margin expansion of half a percentage point. After the year, I estimate the margin to scale further into the achieved 2002-2022 EBIT margin of 9.5%, achieved in 2029. As Ball Corporation should still have extensive investments until 2025 fueling future growth, worsening the cash flows significantly. From 2026 forward, I estimate the cash flow conversion to be very good.

The mentioned estimates along with a cost of capital of 8.09% craft the following DCF model with a fair value estimate of $46.13, very near the price at the time of writing:

{kind=link}

DCF Model (Author's Calculation)

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Ball Corporation had $115 million in interest expenses. With the company’s interest-bearing debts, Ball Corporation’s interest rate comes up to an annualized figure of 4.72%. Ball Corporation has a substantial amount of debt. Although the company plans to pay off around a fifth of the debt after the divestment of the Aerospace segment, the debt-to-equity ratio still seems to stay quite high. I estimate a long-term debt-to-equity ratio of 30% for the company.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.91% . Professor Aswath Damodaran estimates the United States’ equity risk premium at 5.91% in his latest estimate , made in July. Yahoo Finance estimates Ball Corporation’s beta at a figure of 0.85 . After the divestment, the beta could move into either direction as the nature of Ball Corporation’s operations changes. I believe that the beta would decrease slightly, but I don’t see a substantial change as likely, and use Yahoo Finance’s estimate in the CAPM. Finally, I add a small liquidity premium of 0.1% into the cost of equity, crafting the figure at 10.03% and the WACC at 8.09%.

Takeaway

The divestment of the Aerospace segment is a positive prospect for Ball Corporation, at least in my opinion. The company will have a clearer focus on the Beverage Packaging business in the future. The company has been able to grow its revenues organically and is currently investing quite heavily for the future. I believe that the future has been priced into Ball Corporation’s stock price, though. My DCF model estimates the stock to be fairly valued.

For further details see:

Ball Corporation: Aerospace Divestment Should Create Shareholder Value