BALY - Bally's: Continued Pressure On Investor Returns With High Leverage

2023-12-03 10:35:51 ET

Summary

- Bally's Corporation's Q3 earnings missed estimates, but clipped record quarterly sales and growth in casino and resorts revenues.

- The company's use of leverage to finance asset growth hasn't been well received by the market in my view, producing a dislocation in market returns to equity returns.

- Analysis of the facts indicates BALY lacks the economic data to compound wealth for its owners over the coming 1–3 years.

Investment updates

Investors should be fairly compensated for the capital they put at risk when investing with a company. Stock market investors are not providers of capital per se- unless in IPOs or secondary offerings, etc.-but they do provide capital indirectly through reinvestment of retained earnings. Consequently, investors mark the valuations of corporate securities higher or lower based on the capitalized earnings produced on this equity capital. A firm earning high rates on the capital of its investors should be valued as such.

Bally's Corporation ( BALY ) is a casino & resorts company I initiated coverage on for us in September. I rated the company a hold, noting its asset-heavy model and flat business returns, despite high growth rates. The critical issues were:

Table 1.

| Critical issue |

| Findings |

| Capital-hungry business |

| Needs substantial reinvestment of profits + leverage to maintain its competitive position. |

| Sales last 3-years growth of CAGR 20% |

| Requiring ~$1.45 capital investment per $1 of new sales. |

| Subpar earnings produced on new investments |

|

| Trading cheap at 5.8x earnings (at the time) and 25% cash flow yield |

| But the economics seemed to justify this valuation. |

| Rating |

| Hold |

The deep dive I published last time extensively detailed BALY's business returns, capital intensity, and ability to unlock value. A thoughtful analysis of how this transposes to the investor is also in order following the company's Q3 numbers, posted earlier this month.

This report will analyse the economic watermarks BALY must deliver to its equity holders to create market value along with insights from its Q3.

The critical investment facts governing the BALY debate are summarized into the following headings:

(1). Leverage driving business growth + profits earned on investor equity,

(2). The rate of incremental returns on equity lags the trailing rate of return,

(3). FCF positive but saddled with debt. There is $896mm of equity holding up $6.9Bn of assets.

(4). Progress at its Chicago facility

Net-net, I continue to rate BALY's a hold for the reasons outlined in this updated investment thesis.

Figure 1.

{kind=link}

Figure 1a.

{kind=link}

Q3 earnings insights

The firm missed consensus estimates at the top and bottom lines in Q3. It put up quarterly revenues of $632mm, up 9.5% YoY, and pulled this to adj. EBITDAR of $173.2mm on a net loss of $1.15 per share.

This was actually a record quarterly sale for the company, underscored by 9.3% growth in casino + resorts revenues to $359m. Meanwhile, interactive revenues were up 7.2% YoY internationally and 13% in the US + Canada, as seen below.

Table 1.

| Segment (in thousands) |

| Q3 '23 |

| Q3 '22 |

| Casinos & Resorts Revenue |

| $359,026 |

| $328,540 |

| Interactive: |

| International Interactive Revenue |

| 243,884 |

| 227,579 |

| North America Interactive Revenue |

| 29,567 |

| 22,130 |

| Net (loss) / income |

| (61,802) |

| 593 |

Source: BALY 10-Q

For me the takeout was the opening of its Chicago Temporary Casino in September. This was a highly anticipated event, and management reported a smooth opening:

(i). >155,000 visitors in first 30 days,

(ii). Around 790 slot machines and 56 table games,

(iii). Repeat visitations from its Bally's Reward customers.

Once the Chicago facility is done, BALY will have interests in 17 casinos dotted across 11 states. Even still, management has updated guidance following the Q3 numbers and now forecasts $2.4-$2.5Bn in sales for FY'23 on EBITDAR of $655mm at the upper end. The changes bakes in the delayed opening of the Chicago facility in full. Wall Street is eyeing 8-9% growth for BALY's top line in both '23 and '24, in line with management's view. My assumptions also have the company to push 8-9% at the top this year. But with the economics discussed below, my judgement is it won't roll over to market value.

Figure 1b.

Source: BALY Q3 Investor Presentation

Based on this analysis, the critical economic assumptions are:

(1). The rate of earnings on equity is highly skewed by leverage

Talking points:

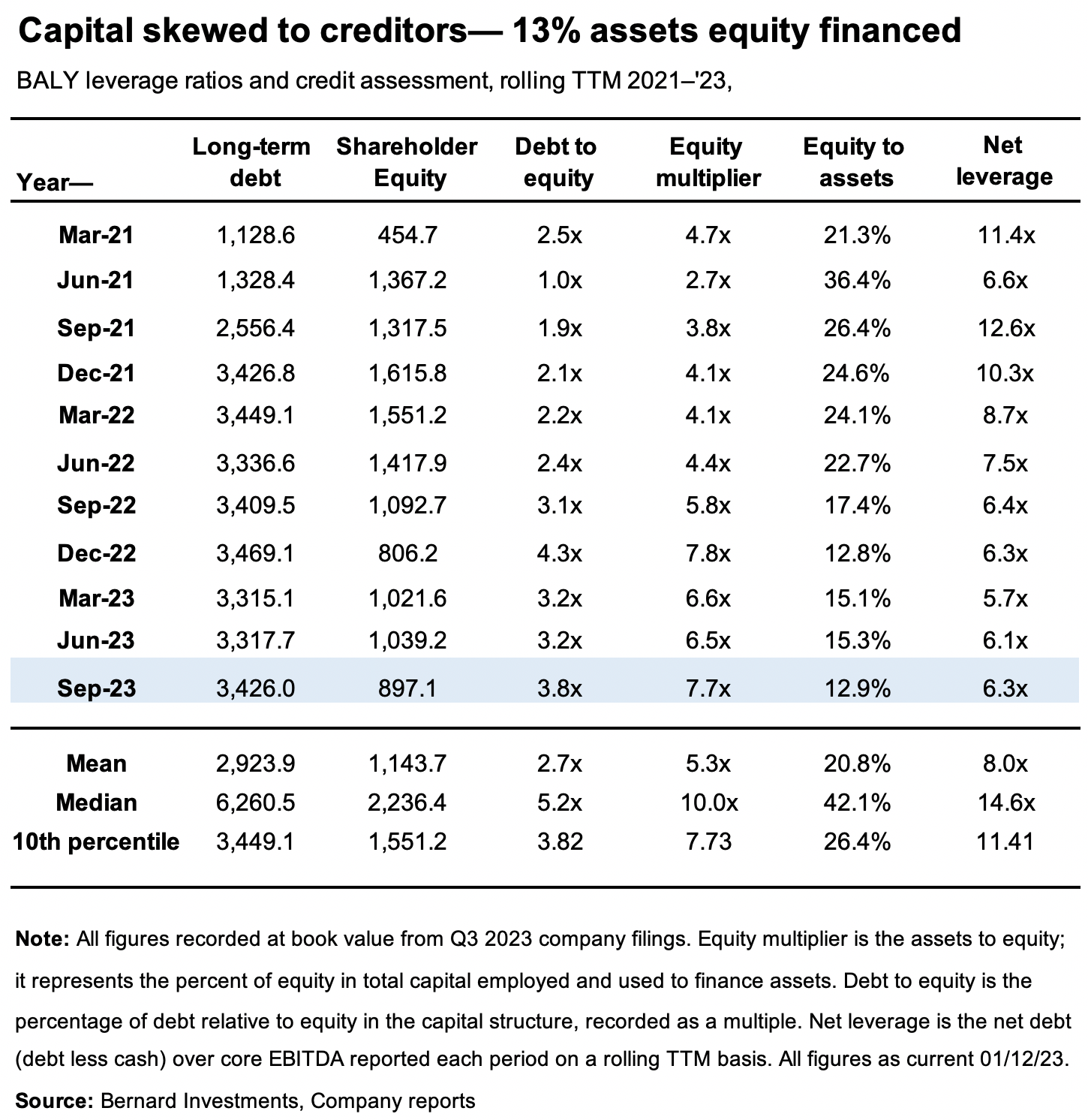

- BALY is highly leveraged with $3.4Bn total liabilities, equal to 3.8x net assets of $897mm. A total of $4.3Bn of investor capital has been employed into the business as of Q3. The firm has levered this amount ~1.4x into capital at risk in its operations (Figure 2).

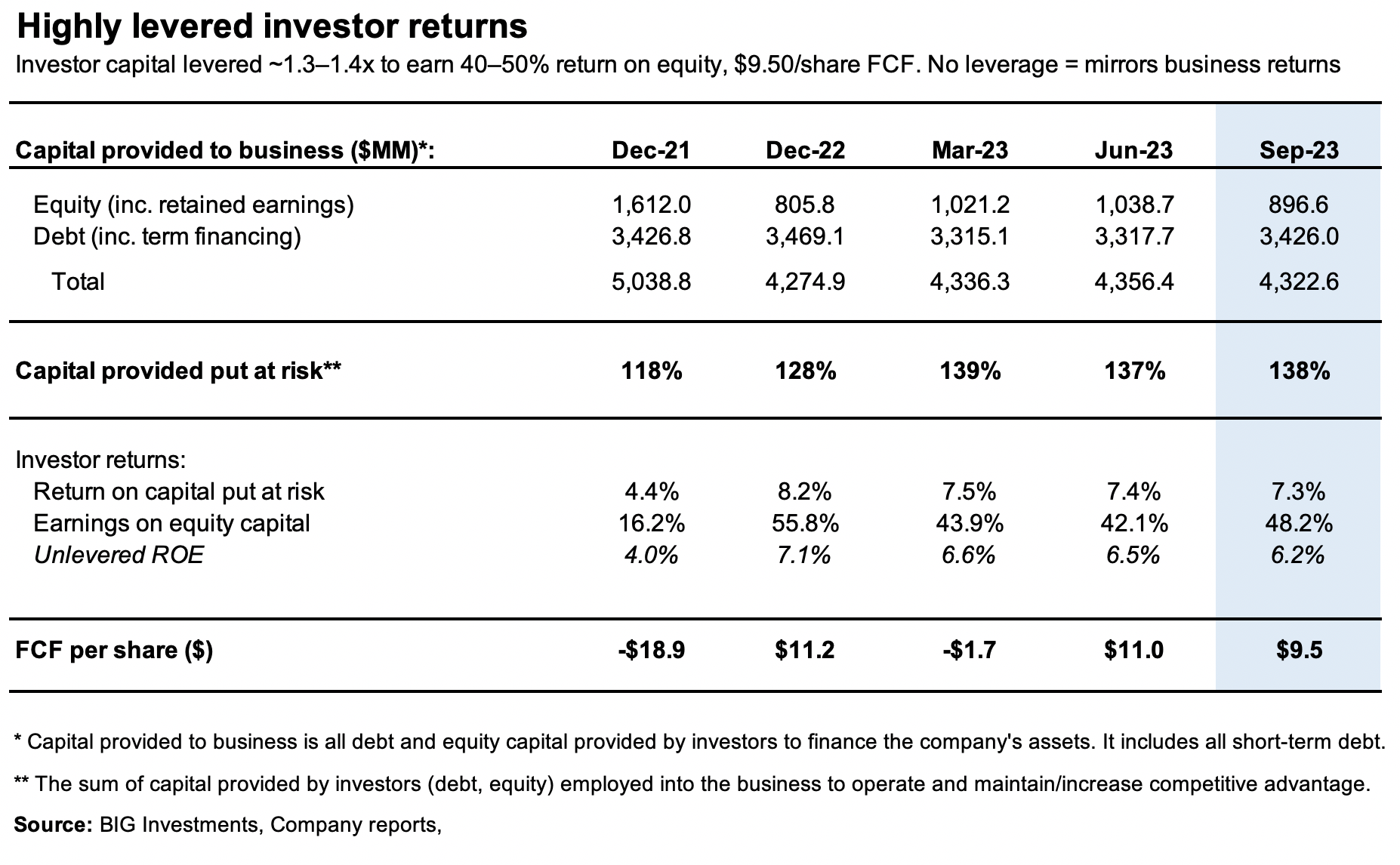

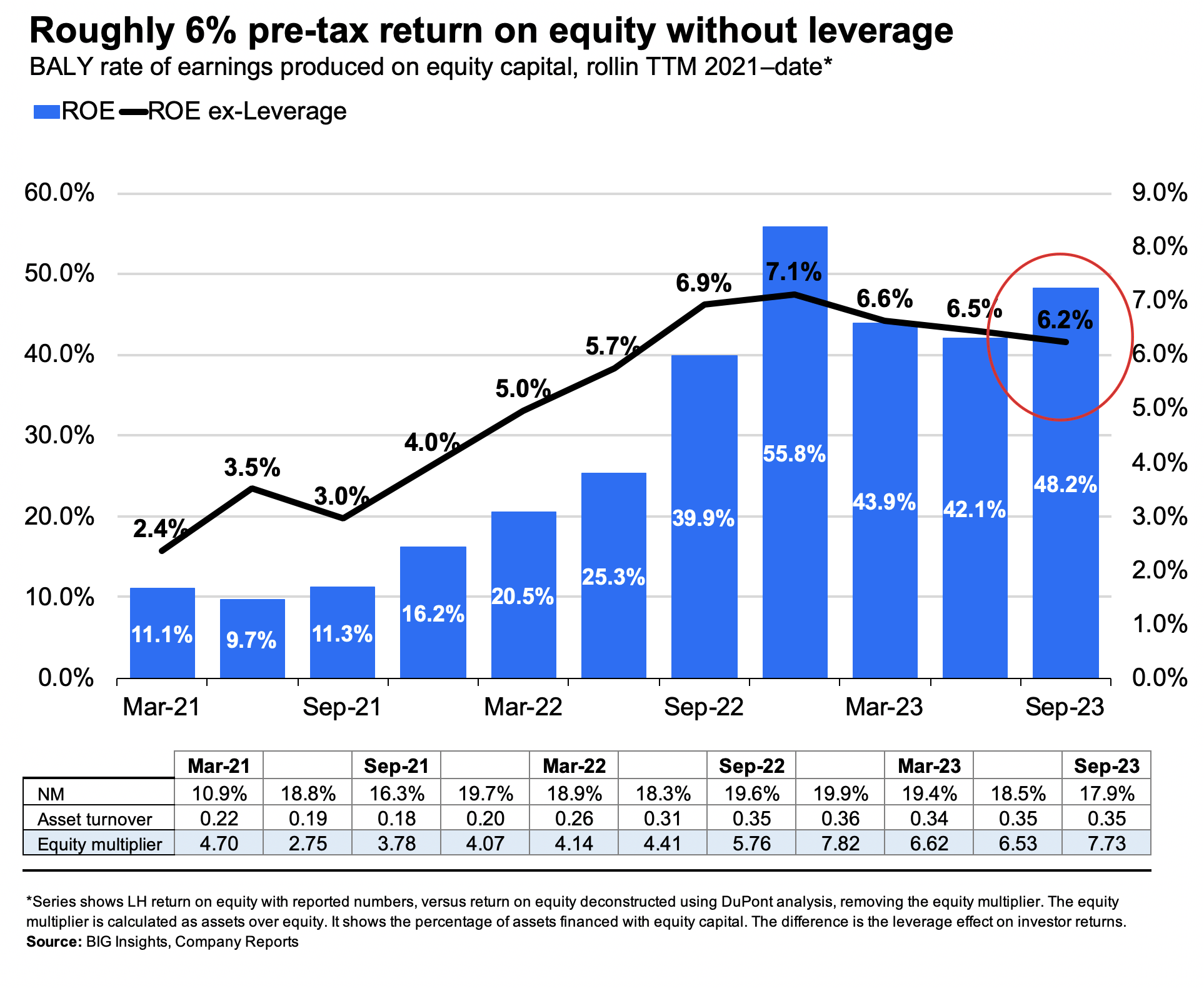

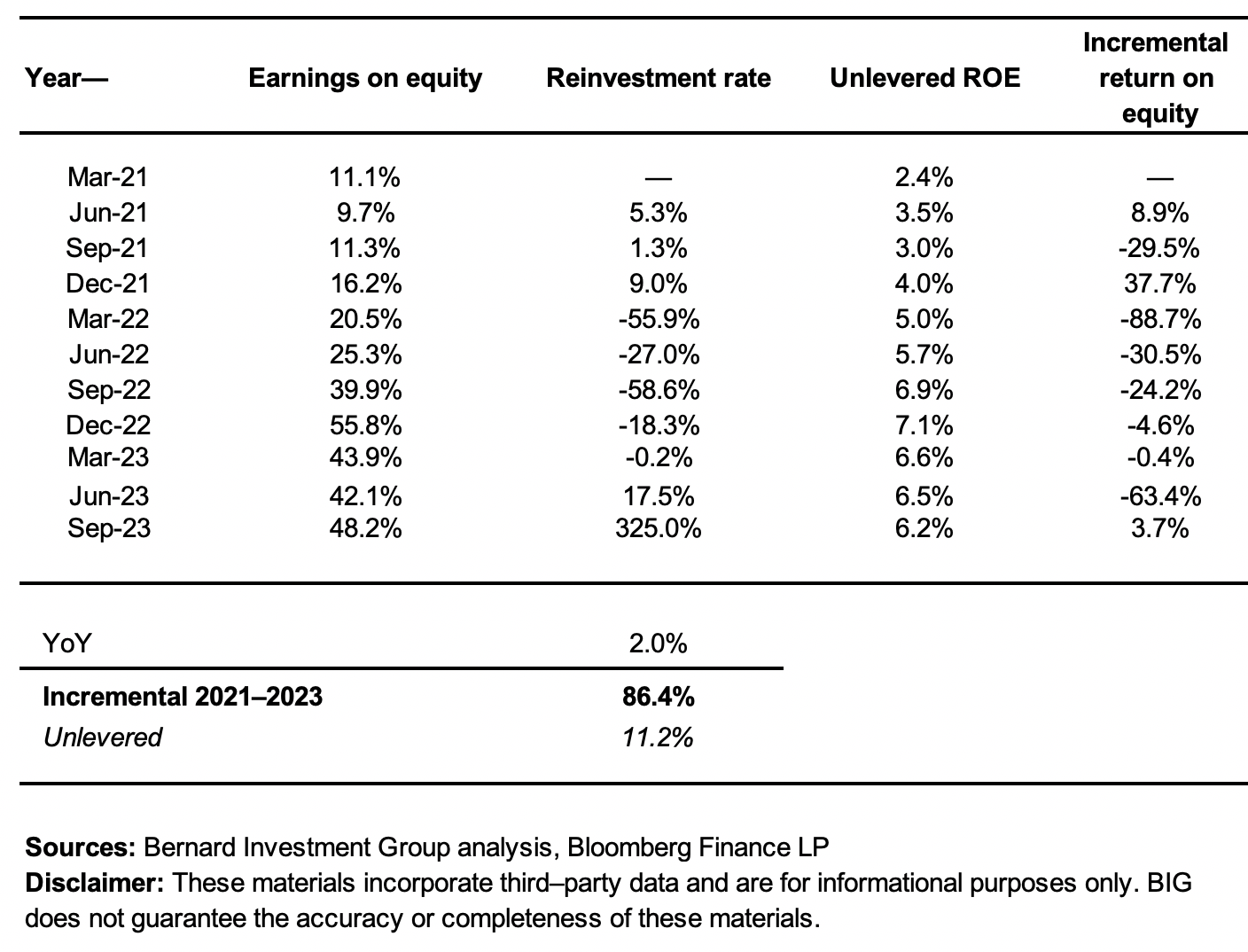

- Consequently, pre-tax returns on equity capital are superb, ranging from 16-55% since December 2021 on a rolling TTM basis, settling at 48% in Q3. The returns have compounded linearly since Q2 2021 as well, including the 55% outlier FY'22 (Figure 3).

The presumption, on face value, is that BALY is on the shareholders' side, creating immense value at these rates of return. A company earning 40-50% on equity capital is tremendously rare and will likely be, as the late, great, Charlie Munger conned, ' drowning in cash' .

But BALY's market returns have not at all mirrored its equity returns or business returns-on the contrary, actually. What is missing?

In my opinion, the company's use of leverage to finance asset growth has not been received well by the market. Evidence supporting this view includes the following:

- Net assets of $19.6/share in Q3 produced c.$9.50/share in trailing pre-tax earnings, a 48% return on investor capital.

- However, equity of $19.60/share is holding up total assets of $151/share. Highly leveraged assets to equity therefore of 7.7x (Figure 3). As such, only 13% of the firm's assets are financed (owned) by equity holders.

- The unlevered ROE squashes from 48% to 6.2% when removing the effect of leverage. This implies creditors are receiving the bulk of returns on capital in my opinion. It is no wonder investors haven't bothered here-why own a slice of 'equity', to- (1) pay bondholders, and (2) when adj. return on equity is <10%.

As a result, the unlevered returns BALY earned on investor capital closely mirror the business returns produced on capital at risk in the business, at 4-6% from 2021-date (Figure 2). Both are underwhelming in a 4-5% risk-free rate world. The propensity for BALY to compound the wealth of equity investors is significantly hampered by these forces in my opinion.

Figure 2.

{kind=link}

Figure 3.

{kind=link}

(2). Further explanations in the incremental analysis

The critical issue is that:

- leverage appointed on the balance sheet has magnified the returns on existing shareholder equity,

- but with no transposition to increased market value.

BALY has stretched trailing ROE from 11% in 2021 to 48% in Q3 '23. Such a result is astounding. But, as discovered earlier, is driven through the 7.7x leverage of assets to equity.

The notions on return on equity and leverage are crystal-clear. Leverage increase ROE for the company, not necessarily for the equity investor. These additional insights add further clarity:

- Unlevered pre-tax returns are far less compelling, at a 5-6% 2-year rolling average (Figure 4). The firm's reinvestment of post-tax earnings has narrowed in sequentially over this time too, as liabilities employed on the balance sheet were deployed into the business instead.

- Critically, incremental returns < historical pre-tax returns on capital. The incremental pre-tax profits earned on equity have continued to slide lower on a sequential basis for the last 2 years on aggregate. For instance, the 48% trailing ROE reflects the entire pre-tax earnings on all equity. In contrast, BALY compounded pre-tax earnings at 2% on incremental capital from '22-'23 in the TTM. Leverage masks this dislocation.

- Since 2020, the incremental return on investor equity tallied 86%, adjusted to 11% unlevered (behind the benchmark indices). Meanwhile, the equity multiplier is 7.7x with a debt-to-equity ratio of 3.8x (Figure 5).

Based on these economics, the incremental value BALY looks to have created on face value, is a highly leveraged version for equity holders. The adjusted returns are far less compelling.

Figure 4.

{kind=link}

Figure 5.

{kind=link}

(3). FCF per share drying up

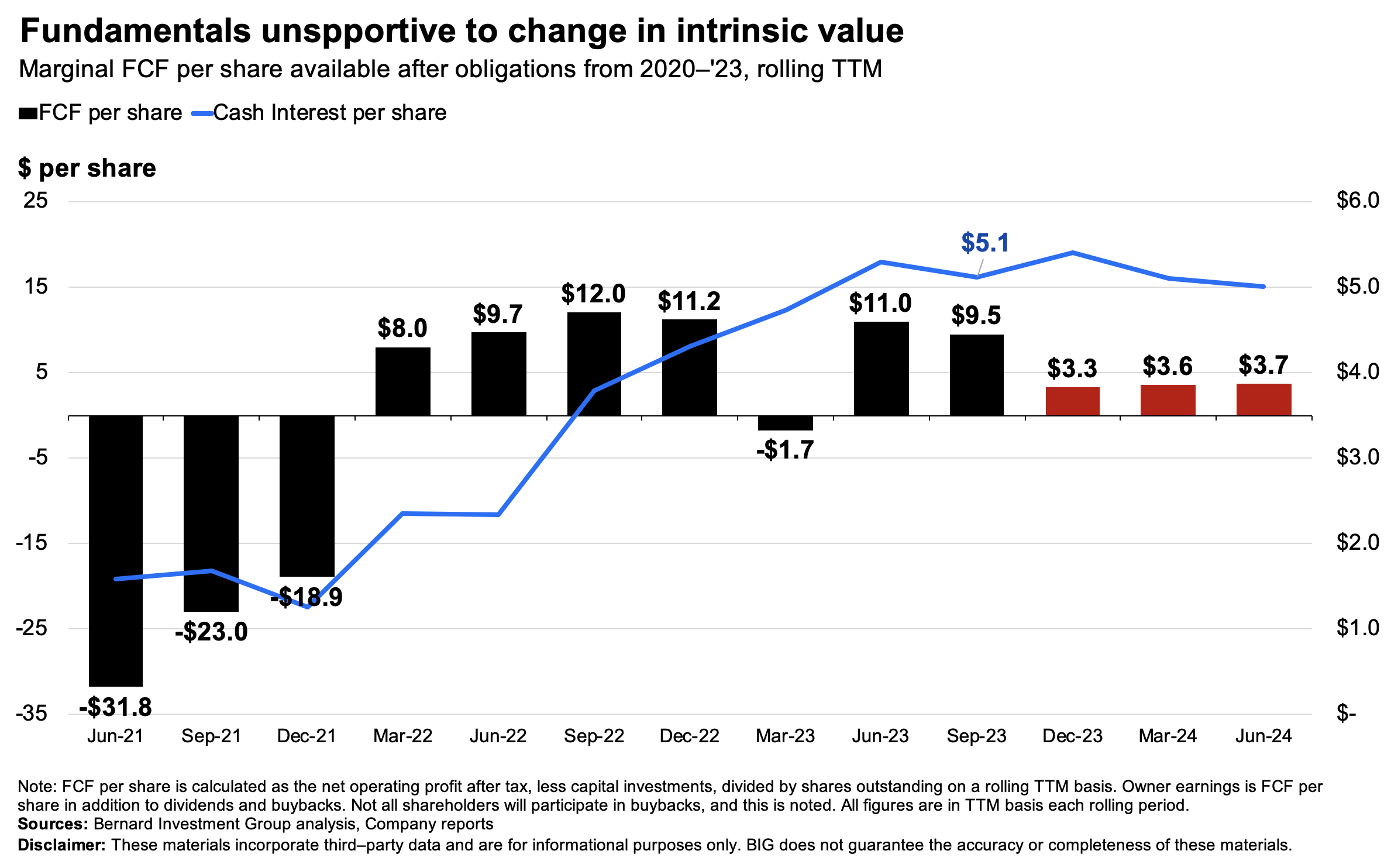

The firm's capital structure and asset intensity has clamped its ability to throw off cash to shareholders. I covered this extensively in the last publication. However, I'd also like to point out the following:

- After next to no sequential investments, BALY is FCF positive since 2022 due to 1) divestitures, and 2) working capital improvements.

- It spun off $9.50/share in FCF in the TTM, an astonishing 83% trailing FCF yield.

- It paid $5.10/share of cash interest as well (vs. $3.91 in cash per share on hand), reducing FCF to equity holders to $4.40/share.

- My assumptions have BALY to print $3-$4/share in FCF moving forward, a negative $2/share adjusted for cash interest assumptions.

Whilst the cumulative cash flows are noted, the reality is 1) much of this is/was attributed to creditors and 2) value obtained via owner earnings are less compelling.

Figure 6.

{kind=link}

Valuation + Conclusions

The stock sells at 9x forward earnings , 2x forward sales and 10x forward EBITDA, and is priced at a 0.6x discount to net asset value.

The following data points, based on earnings power and asset factors, evidence that BALY is fairly valued at its current market price in my opinion:

- Arithmetic shows potential value in paying 0.6x net capital- pay 0.6x $19.66/share = $12.98 in value, to receive 48% trailing return on capital. Implied investor return is magnified to 73% in paying 0.6x as well (9.48/12.48 = 73% ROE).

- Adjustments for leverage are still required-73% implied ROE after paying 0.6x reconciles to 9.5% ROE unlevered. Stark contrast.

- A 9.5% ROE implies a forward equity value of $21.50/share for BALY. At the same 0.6x multiple, the firm is worth $12.90/share in market value (0.6x21.50).

In addition, BALY trades at 10x trailing EBITDA of $1.15/share. The incremental pre-tax ROE was 3.7% in Q3. At the same 10x multiple, the company is worth $11.90/share after factoring in the return on equity.

Therefore, in my estimation, the company is worth around $11.90-$12.90/share today, otherwise 10x forward EBITDA and 0.6x forward book value respectively. These valuations sport a neutral view.

In short, there is lack of economic data to suggest BALY is positioned to compound wealth of its owners. The firm is saddled with debt, with a capital-intensive operation model. The leverage positively impacts earnings relative to equity, but the market is smarter than that, and sees right through it. Unlevered investor returns therefore closely match business returns (surprise surprise). In that vein, my judgement is to reiterate BALY a hold, noting it trades within range of my fair value estimate. Net-net, reiterate hold.

For further details see:

Bally's: Continued Pressure On Investor Returns With High Leverage