BANC - Banc of California: A Top Dividend Growth Stock For 2024

2023-12-14 14:10:06 ET

Summary

- Banc of California recently completed its merger with PacWest Bancorp, making it a leading bank in the state of California.

- The merger allows Banc of California to reduce expenses and optimize its balance sheet by repaying high-cost wholesale funding.

- The regional bank is a strong choice for dividend investors, with potential for significant dividend growth in the future.

- Shares are priced at a 29% discount to book value, well below the historical average.

Just about two weeks ago, at the end of November, Banc of California ( BANC ) completed its transformational merger with PacWest Bancorp. PacWest Bancorp ran into trouble during the regional banking crisis that was precipitated by the failure of Silicon Valley Bank in the first-quarter. PacWest Bancorp ultimately sold itself to Banc of California in an all-stock deal valued at approximately $1.0B which created the third-largest bank in California. The new bank has a lever to boost profitability by focusing on balance sheet optimization and the repayment of high-cost funding. Banc of California is also set, in my opinion, to see strong dividend growth following the merger which I believe makes BANC a top choice for dividend investors!

Recently completed merger with PacWest Bancorp

As I detailed in the introduction, the merger between Banc of California and PacWest Bancorp closed at the end of November and Banc of California, as part of its merger deal, secured another $400M in equity from affiliates of funds managed by Warburg Pincus, a global private equity firm. Banc of California agreed to acquire PacWest Bancorp in an all-stock deal in the third-quarter and the regional bank's shares were exchanged at a fixed 0.6569x exchange ratio. Owners of PacWest Bancorp have since become owners of Banc of California and shares of PACW have been delisted.

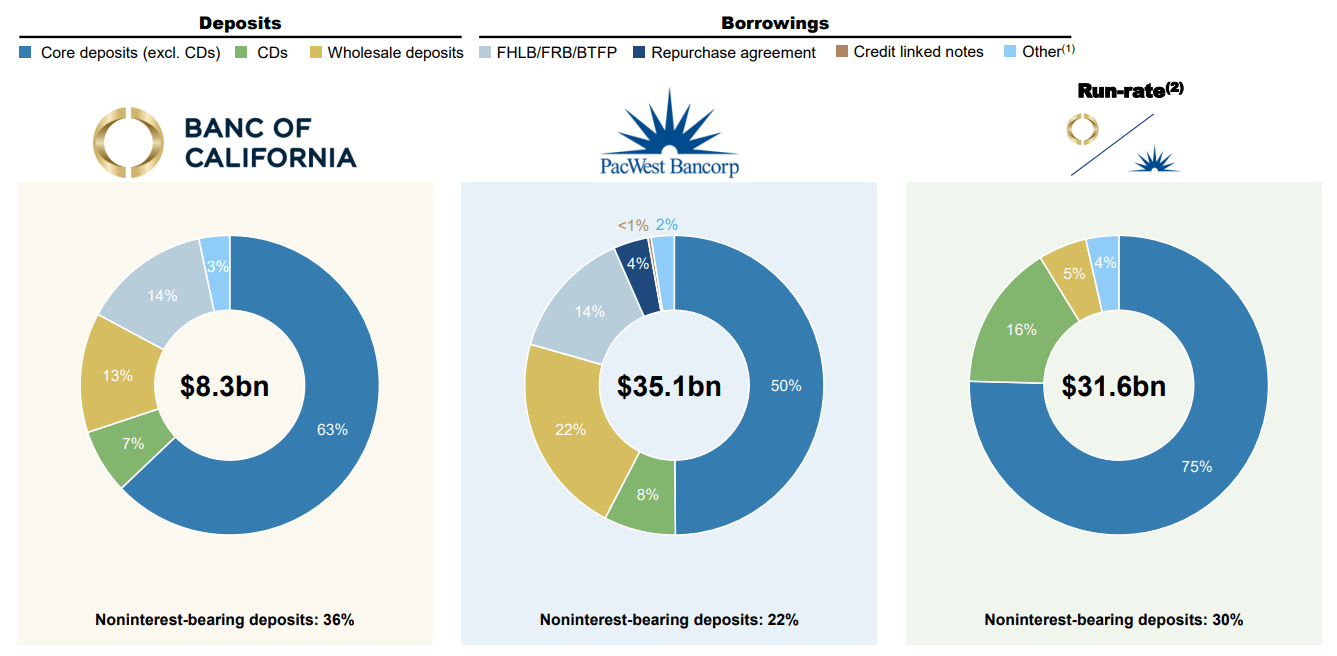

The merger made Banc of California the third-largest bank in the state of California with approximately $32B in deposits (expected at the time of the merger announcement).

{kind=link}

The merger was widely seen as a major win for Banc of California… which initially estimated that the acquisition of PacWest Bancorp will lead to 20%+ EPS accretion in FY 2024 and 3% accretion to tangible book value following the close of the merger.

Expense reduction and removal of a high-cost funding source

Banc of California has potential to reduce its leverage and optimize the balance sheet by repaying high-cost debt. Banks, including Banc of California, have seen an increase in leverage and a surge in high-cost funding during the financial crisis in the first-quarter and they have now an opportunity to repay borrowings with high interest rates.

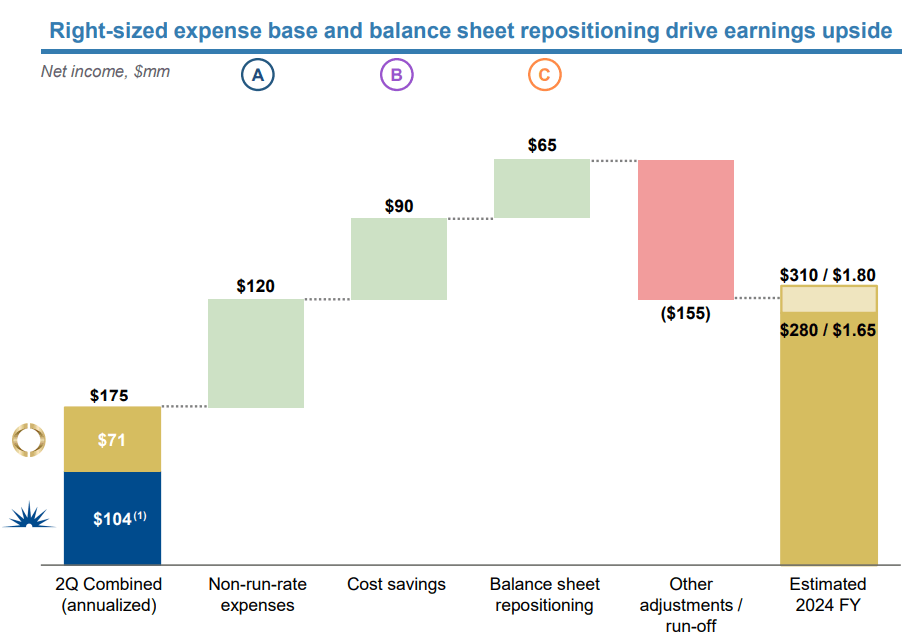

While the merger is also expected to generate a decent amount of cost-savings -- which were estimated to be around $90M annually in July -- I believe the balance sheet repositioning could lead to strong earnings tailwinds following the completion of the Banc of California-PacWest Bancorp merger.

{kind=link}

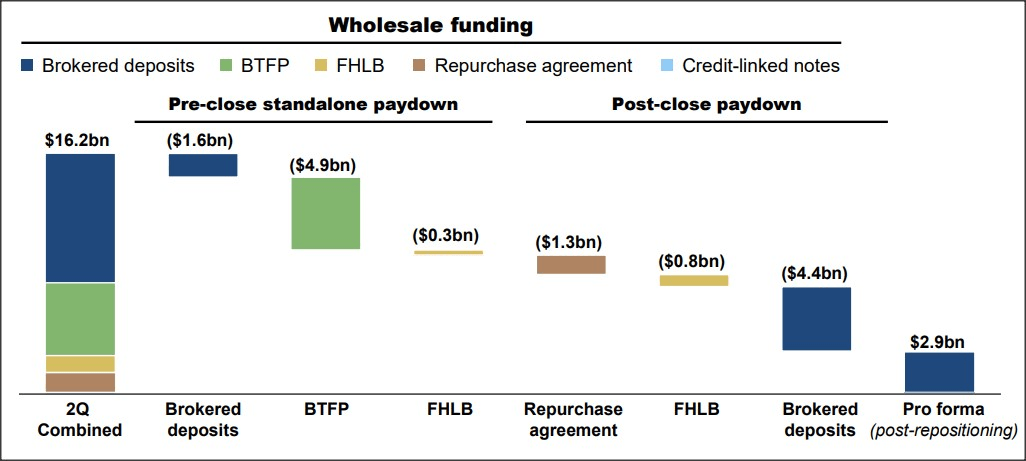

PacWest Bancorp sold $1.5B of its securities portfolio ahead of the merger while Banc of California sold $448M of securities. Besides shrinking its securities portfolio, Banc of California has agreed to sell $1.8B worth of single-family residential mortgages to JPMorgan Chase ( Source ) as part of a broader strategy to repay $13B of high-cost wholesale funding... which had an average weighted cost of 5.0%. The bank's wholesale funding was mostly made up of brokered deposits, liquidity from the Federal Reserve's Bank Term Funding Program/BTFP and loans from the Federal Home Loan Banks.

To reduce its borrowings, Banc of California is using proceeds from asset sales, excess cash and the $400M raised from Warburg Pincus. The reduced size of Banc of California's balance sheet as well as a synergy effects resulting from the merger are estimated to boost the bank's EPS by at least 20% next year.

{kind=link}

Banc of California is a dividend growth play

At the beginning of FY 2023, Banc of California raised its dividend by a massive 67% to $0.10 per-share quarterly. Considering that the regional bank has gotten a good deal with PacWest Bancorp, I believe we could see a material dividend raise in the first quarter of FY 2024.

Banc of California has a dividend payout ratio of about 20% which implies that the regional bank has enough margin to deliver a dividend increase in February. My estimate is for a 40-50% increase to $0.14-0.15 per-share quarterly which would translate to a forward dividend yield of 4.5-4.9%.

Banc of California's valuation

Banc of California has started to trade at a material discount to book value following the Q1'23 crash in the regional banking market and the lender has not yet recovered, likely due to the fact that the bank is concentrated in the high-cost state of California and because investors need to absorb the PacWest Bancorp merger. Shares of Banc of California are priced at a 29% discount to book value despite the regional lender trading at an average price-to-book ratio of 1.05X in the last five years. Additionally, Banc of California snapped up PacWest Bancorp at a good price and the bank expects the acquisition to add massively to its earnings next year.

One thing that I don't like with Banc of California, NIM risks

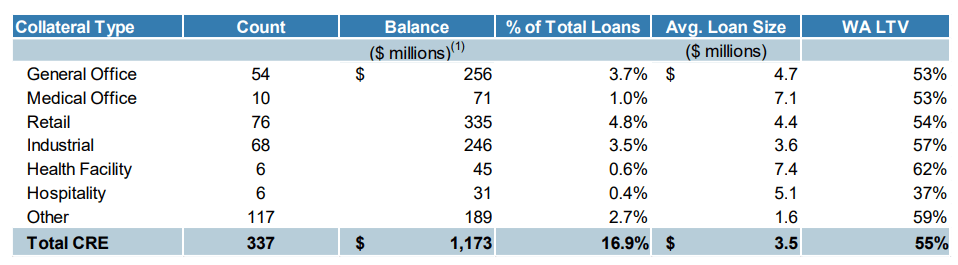

Rarely will you find an investment where you will like everything you see. With regard to Banc of California, I don't like the regional bank's exposure to commercial real estate which, as we all know, has drifted towards major trouble due to a combination of changing work habits (remote working) and high interest rates.

Banc of California had about 16.9% of all loans exposed to the commercial real estate market, with the second-largest balance falling into the general office category… which is possibly the most challenged commercial real estate sub-sector right now.

{kind=link}

Other risks include the concentration in the California market which makes the regional lender dependent on the economy in the state. Lower interest rates in the market going forward may also be considered a risk factor as it builds pressure on Banc of California's net interest margin.

Final thoughts

Banc of California just completed its merger with PacWest Bancorp and the deal created the third-largest bank in the state of California. Besides expected EPS and tangible book value accretion in FY 2024, there are two major reasons for investors to consider Banc of California: 1) Balance sheet optimization is set to lead to a reduction in high-cost wholesale funding, creating a catalyst for earnings and book value growth, and 2) The regional lender will most likely announce its first-quarter dividend in February which will likely result, given the acquisition context and this year's huge dividend raise, in a significant dividend upsize. On top of all of these benefits, Banc of California trades at a significant, 29% discount to book value, creating room for a revaluation as well!

For further details see:

Banc of California: A Top Dividend Growth Stock For 2024