BANC - Banc of California: Top-Line Outlook Remains Bright Despite Recent Performance

2023-03-08 20:08:32 ET

Summary

- The balance sheet positioning hasn't changed much in the fourth quarter; therefore, the margin’s rate sensitivity is likely to remain unchanged relative to the last quarter.

- California's strong economy and recent hiring efforts will likely support loan growth this year.

- The December 2023 target price suggests a small upside from the current market price. Moreover, BANC is offering a low dividend yield.

The declining trend of Banc of California's (BANC) loan portfolio will likely reverse this year thanks to strong regional economies. Further, the margin will likely continue to expand this year, which will boost the top line. However, the bottom line will likely decline in 2023 due to inflation and the normalization of provision expenses. Overall, I'm expecting Banc of California to report earnings of $1.70 per share for 2023, down 10% year-over-year. Compared to my last report on the company, I’ve slightly reduced my earnings estimate following the fourth quarter’s disappointing results. The December 2023 target price suggests a small upside from the current market price. Therefore, I'm downgrading Banc of California to a hold rating.

Margin’s Rate Sensitivity in 2023 Likely to be Similar to Last Year

Banc of California’s net interest margin has been barely correlated with interest rates in previous years, as shown below.

SEC Filings

However, the correlation improved last year (see above) because the deposit mix significantly improved throughout 2021. As the deposit mix shift slowed in 2022, I'm expecting the deposit beta in 2023 to be similar to the deposit beta in 2022. The results of the management’s rate sensitivity analysis given in the 10-K filing show that a 200-basis points hike in interest rates could boost the net interest income by just 2.1% over twelve months.

On the plus side, new loan production will provide a material boost to the margin. Banc of California issued new loans at a rate of 6.81% (average) in the fourth quarter of 2022, which is much higher than the average portfolio yield of 4.92%, as mentioned in the earnings presentation . Therefore, new loans can be expected to significantly raise the loan portfolio’s average loan yield in the near term.

Further, the reinvestment rates in treasuries are also much higher now than in the prior quarter. Short-term treasury yields have jumped up, as shown below.

U.S. Treasury Department

Considering these factors, I'm expecting the margin to grow by 10 basis points in 2023.

Negative Loan Growth Trend Likely to Reverse

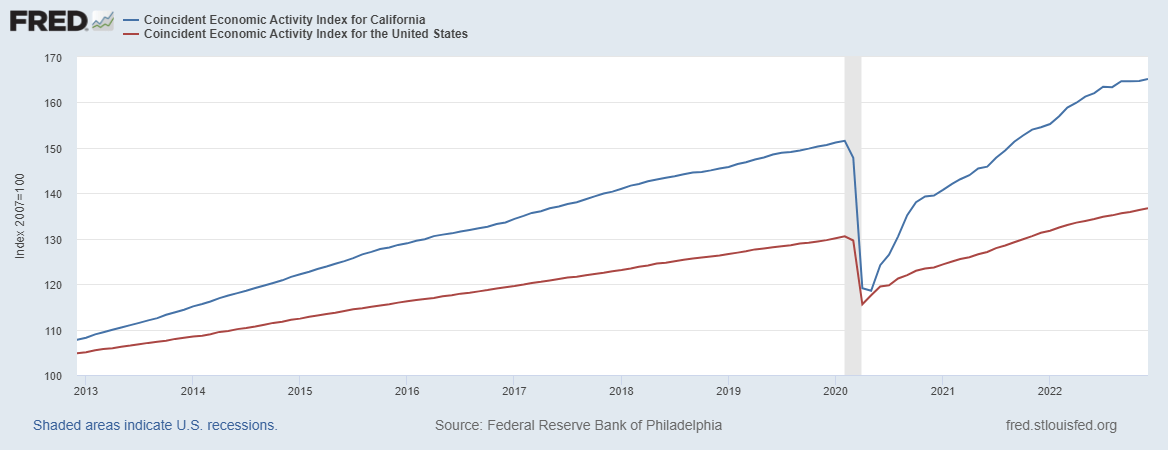

For a second consecutive quarter, the loan portfolio's performance missed my expectation. The portfolio’s size declined by 2.3% during the last quarter, which led to an overall decline of 1.8% for the year. In my opinion, there is a chance that this negative trend will reverse this year because of a positive regional economy. Banc of California operates throughout California with its presence concentrated in the southern part of the state from San Diego to Santa Barbara. The state's economic activity has recently been commendable when compared with the rest of the country.

{kind=link}

Additionally, the local unemployment rates are quite low, especially in Santa Barbara, compared to the national average.

Further, the management mentioned in the conference call that it plans on continuing to hire new talent this year, which will boost loan growth.

Considering these factors, I'm expecting the loan portfolio to increase by 4% in 2023. Compared to my last report on Banc of California, I haven't changed my growth estimate for 2023. However, my loan balance estimate is much lower than before because the portfolio declined in the fourth quarter of 2022, while I had been expecting positive growth.

Meanwhile, I'm expecting deposits to grow in line with loans. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 286 |

| 248 |

| 225 |

| 254 |

| 314 |

| 332 |

| Provision for loan losses |

| 30 |

| 36 |

| 30 |

| 7 |

| (32) |

| 14 |

| Non-interest income |

| 24 |

| 12 |

| 19 |

| 19 |

| 17 |

| 23 |

| Non-interest expense |

| 233 |

| 196 |

| 199 |

| 183 |

| 194 |

| 198 |

| Net income - Class A |

| 23 |

| 3 |

| (1) |

| 50 |

| 115 |

| 103 |

| EPS - Diluted -Class A ($) |

| 0.45 |

| 0.05 |

| -0.02 |

| 0.95 |

| 1.89 |

| 1.70 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD million unless otherwise specified) |

In my last report on Banc of California, I estimated earnings of $1.75 per share for 2023. I’ve slightly reduced my earnings estimate as I've decreased my loan balance and non-interest income estimates following the fourth quarter’s disappointing results.

My estimates are based on certain macroeconomic assumptions that may not come to fruition. Therefore, actual earnings can differ materially from my estimates.

Downgrading to a Hold Rating

Banc of California is offering a dividend yield of 2.4% at the current quarterly dividend rate of $0.10 per share. The earnings and dividend estimates suggest a payout ratio of 24% for 2023, which is easily sustainable. Therefore, the dividend appears secure.

I’m using the historical price-to-tangible book (“P/TB”) and the peer average price-to-earnings (“P/E”) multiples to value Banc of California. BANC stock has traded at an average P/TB ratio of 1.19 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2023 ($) |

| 15.1 |

| 15.1 |

| 15.1 |

| 15.1 |

| 15.1 |

| Target Price ($) |

| 15.0 |

| 16.5 |

| 18.0 |

| 19.5 |

| 21.1 |

| Market Price ($) |

| 16.9 |

| 16.9 |

| 16.9 |

| 16.9 |

| 16.9 |

| Upside/(Downside) |

| (10.9)% |

| (2.0)% |

| 7.0% |

| 15.9% |

| 24.9% |

| Source: Author's Estimates |

Historically, Banc of California’s P/E multiple has been very erratic. Therefore, it's best to take the peer average to value the company instead of the historical average. As of the close of March 7, the peer average P/E ratio was around 10.4x, as shown below.

| BANC |

| PFBC |

| FBMS |

| TMP |

| HFWA |

| BRKL |

| Peer Average |

| EPS 2023 ($) |

| 1.70 |

| 1.70 |

| 1.70 |

| 1.70 |

| 1.70 |

| Target Price ($) |

| 14.2 |

| 15.9 |

| 17.6 |

| 19.3 |

| 21.0 |

| Market Price ($) |

| 16.9 |

| 16.9 |

| 16.9 |

| 16.9 |

| 16.9 |

| Upside/(Downside) |

| (15.7)% |

| (5.7)% |

| 4.4% |

| 14.4% |

| 24.5% |

Equally weighting the target prices from the two valuation methods gives a combined target price of $17.8 , which implies a 5.7% upside from the current market price. Adding the forward dividend yield gives a total expected return of 8.1%.

In my last report on Banc of California, I adopted a buy rating with a December 2023 target price of $17.1. Since then, the stock price has rallied strongly. As a result, the stock is now offering only a small upside. Therefore, I'm downgrading Banc of California stock to a hold rating.

For further details see:

Banc of California: Top-Line Outlook Remains Bright Despite Recent Performance