BBAR - Banco BBVA Argentina: Caution Warranted Ahead Of More 'Shock Therapy'

2024-01-05 16:08:05 ET

Summary

- Like the rest of the banking sector, Banco BBVA Argentina S.A. is on course for a highly volatile near-term path.

- The guidance bar also seems a tad high, and the bank may need to reset expectations sooner rather than later.

- There are compelling reasons to own Banco BBVA Argentina stock long term, but re-rated valuations limit the safety margin.

The " shock therapy " has begun in Argentina following new President Javier Milei’s election victory. Alongside a significant cutback in fiscal spending, the new administration also unveiled a one-off devaluation of the peso to ARS800 per dollar - about in line with the parallel rate. While positive for corporates with dollarized revenue streams, the impact is trickier for banks like Banco BBVA Argentina S.A. (BBAR). On the one hand, the bank will gain somewhat from the FX depreciation via its dollar-linked asset portfolio. Not all of its equity is dollar-hedged, though, so the P&L positives likely won't fully outweigh the negatives. Plus, there's the second-order impact of heightened inflationary pressures post-devaluation - note inflation has already been a major detractor to the bank's net monetary position in recent quarters.

Despite the near-term uncertainty, Argentine banks have re-rated – perhaps for good reason. A more market-friendly government means a decline in risk premia over time, while Milei’s willingness to implement painful spending cuts bodes well for eventual macro stabilization. Also positive is the optionality from reduced regulatory constraints, which in turn, could open up new fee-related revenue streams going forward.

That said, the path ahead won’t to be an easy one, and I expect a particularly challenging near-term outlook on both sides of the balance sheet as Milei forges ahead with some big fiscal adjustments. BBVA Argentina may be more than adequately equipped to navigate the volatility, but the market has likely already factored in the fundamental positives at the current premium to book . On balance, I would remain sidelined here.

Puts and Takes from the Latest Peso Devaluation

Of the initial “shock therapy” measures imposed by Argentina’s new government, the big devaluation of its official exchange rate is the most relevant for banks. On the one hand, BBVA Argentina will see some P&L benefits via foreign exchange gains on its dollar-linked portfolio. Relative to other sectors, though, banks aren’t as hedged against currency fluctuations – a result of regulatory limitations on their direct dollar exposure. Argentine banks aren’t fully hedged against inflation either, a likely near-term consequence of this one-off reset. While BBVA Argentina’s upsized inflation-linked dual bond portfolio (i.e., bonds that payout the higher of inflation and peso devaluation) certainly helps, I see more P&L headwinds than tailwinds in the fallout.

{kind=link}

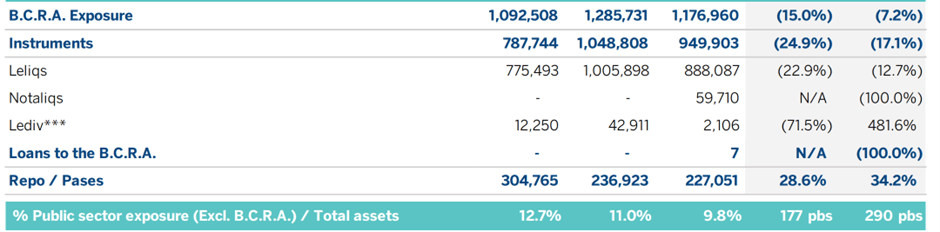

The other key concern is the fate of Argentina’s central bank (i.e., the "BCRA"). After all, Milei had been vocal about abolishing the BCRA in the election run-up. A complete phaseout scenario seems unlikely, though, given: a) the central bank is protected by the constitution; and b) Milei doesn't have control of Congress. Instead, a more likely scenario might be a handicapped BCRA with fewer regulatory functions and a lot less control on the monetary side, especially with regard to central bank bonds ("Leliqs"). Lower Leliq issuances may/may not be a good thing, but a looser regulatory environment would be unreservedly positive, given the many restrictions on banks’ ability to hedge their currency exposures currently.

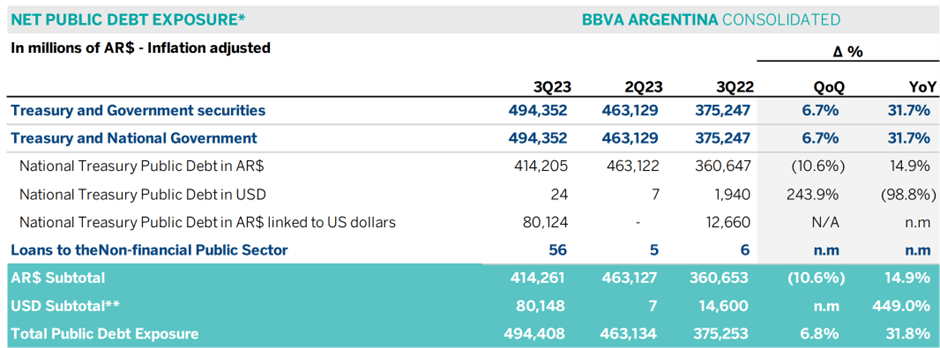

In any case, the pressing issue for banks is managing their Leliqs exposure post-Milei win. Per Q3 reporting , BBVA Argentina is already well into the process of de-risking its Leliq exposure – in line with its banking peers. There’s still reinvestment risk, though, as depending on how quickly it runs down its remaining Leliqs (ideally in favor of inflation or dollar-linked securities), the P&L impact could be material into Q4. Plus, next year’s (positive in real terms) ROE target is a high bar in the context of ongoing triple-digit % inflationary pressures, so any missteps here would add downside risk to current targets.

{kind=link}

Robust Fundamentals, but Mind the Post-Election Uncertainties

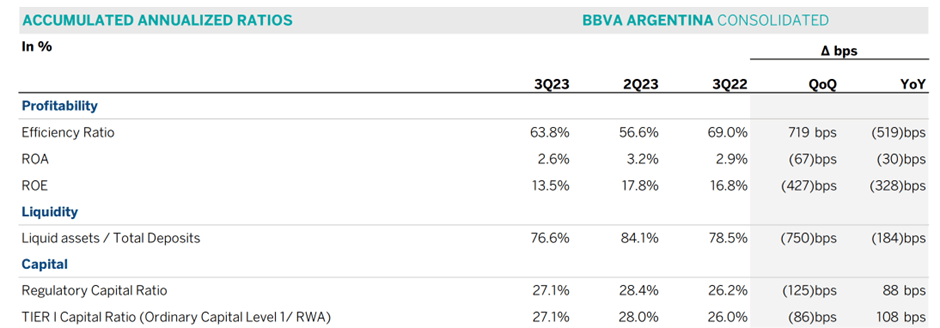

The good news, per monthly BCRA data for the banking system, is that underlying fundamentals are as strong as ever. And even with loan growth down, BBVA Argentina’s Q3 was resilient, as a rotation into public securities kept inflation-adjusted ROEs in the high-teens %. A new government might add uncertainty to banks’ capital deployment options, but the combination of strong capital ratios and intact asset quality, as well as efficiency levers, mean there’s probably enough buffer to withstand any adverse "shock therapy" impacts going forward.

{kind=link}

To be clear, this doesn’t mean the bank will meet its inflation-adjusted ROE guidance bar - fiscal consolidation typically hits loan growth, while adding to borrower stress and provisioning, so it’s still hard to see how the near-term P&L guidance isn’t reset lower. I wouldn’t get my hopes up for capital returns either, with Argentine banks only just re-normalizing dividends after COVID-related restrictions. The current schedule is conservative (~40% earnings payout) and leaves ample room for upside down the line but given the importance of capital buffers ahead of an uncertain operating backdrop, yields will probably remain relatively low.

Light at the End of a Long Tunnel

Putting aside the near-term headwinds, there’s compelling long-term optionality to owning banks here. After all, credit essentially tracks the overall economy - a factor that has worked against BBVA Argentina over the last decade. With the macro taking a turn for the worse last year amid heightened inflation and interest rate pressures, Argentina's (inflation-adjusted) decline in loans has also continued to deteriorate.

Bloomberg

Reversing this systemic trend won't be straightforward but a more market-friendly administration offers hope of a reversal. If successful, the optionality for Argentine banks would be immense - credit penetration levels are still among the lowest in Latin America at ~9% credit-to-GDP, implying vast untapped growth for banks in the long run. Also potentially accretive are new fee revenues should Milei further follow through on his election pledges for deregulation and an increased private sector presence (e.g., the recent privatization of state-owned Banco Nación de Argentina). The road to macro stability won’t be an easy one, though, and pending signs of a broader turnaround, I wouldn’t underwrite this part of the Argentine bank thesis just yet.

Caution Warranted Ahead of More "Shock Therapy"

Argentina may have a new market-friendly government in place, but the path to macro stabilization is far from a given. For banks, the readthrough is even trickier. To be clear, the sector is in a great place fundamentally - solid profitability, well-capitalized balance sheets and robust liquidity positions bode well for their resilience. But much of this has been priced in, I suspect, with even BBVA Argentina stock, among the cheapest in the sector, currently priced at a premium to book.

This leaves Banco BBVA Argentina S.A. investors vulnerable to near-term P&L risks from the peso devaluation and inflationary headwinds, as well as a potential slowdown in credit as fiscal consolidation takes hold. There is light at the end of this tunnel, but the risk/reward doesn’t strike me as particularly compelling here.

For further details see:

Banco BBVA Argentina: Caution Warranted Ahead Of More 'Shock Therapy'