BBDO - Banco Bradesco: Macro Woes Leave Shares Undervalued

2023-10-10 07:58:29 ET

Summary

- Banco Bradesco is facing no shortage of headwinds right now, with pressure on net interest income, sluggish fee income growth and high provisioning expenses chief among them.

- Net interest income will get some support now that rates in Brazil are tentatively heading lower, and I'm hopeful that better-than-expected economic performance will help with credit quality.

- These shares look cheap relative to their recent historical marks, though a combination of macro, Bradesco-specific, and general emerging market risks are things to consider.

Banco Bradesco (BBD)(BBDO) is navigating difficult terrain. Brazil's economic prospects have been surprising to the upside in 2023, but the highly restrictive monetary policy enacted to combat post-COVID inflation has been taking its toll on the bank, with elevated bad debt expenses, high funding costs and weak loan growth all serious headwinds right now. As a result, the ADRs have posted a meaningful decline this past 12 months, even as the Brazilian Real has clocked in modest gains against the dollar.

Where Bradesco goes from here is an open question. Interest rates in Brazil are now tentatively falling, and that may help lift the pressure from funding costs. At the same time, Brazil's hitherto better than expected economic performance may limit further steep rises in its cost of credit. These shares look like decent value right now at a slight discount to book value, though more cautious investors may wish for a higher margin of safety given the potential risks of investing in Brazilian equities.

Banking Headwinds Depressing Profitability

In common with other large Brazilian banks, Bradesco operates a diversified business with significant lines of non-interest income. Fee & commission income, plus the contribution from its insurance and savings business, account for around 45% of its revenue.

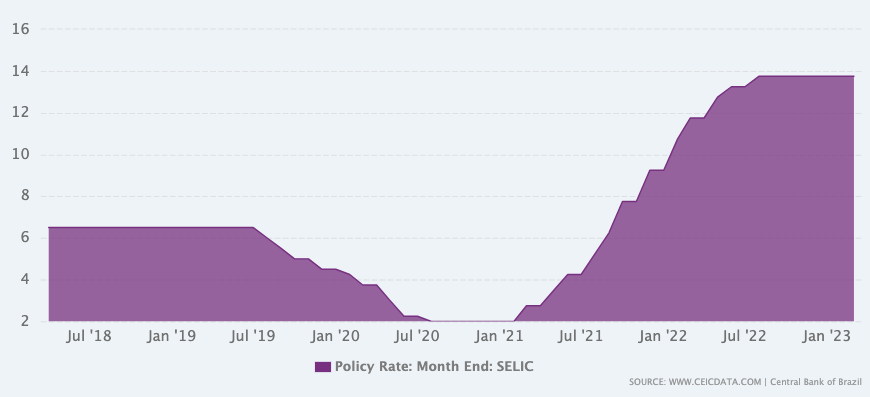

While that offers some stability from the ups and downs of the credit cycle, interest income is still Bradesco's main earnings driver, and as of late this has been under strain. There are a couple of headwinds affecting the banking business. Firstly, the Brazilian central bank's ("BCB") steep interest rate hikes (Fig 1) have resulted in higher funding costs, putting downward pressure on net interest income ("NII") as funding costs have outpaced what Bradesco earns on investment securities. At the same time, higher interest rates are depressing demand for credit, which means sluggish real-terms loan growth (Fig 2). Although loan yields have also headed higher, acting as an offset, overall NII growth has been pretty sluggish over recent quarters (Fig 3), especially in inflation-adjusted terms.

Compounding all of this is the credit quality situation, with Bradesco recording a surge in provisioning expenses to cover potential bad debt. Cost of credit in H1 was up nearly double on the comparable period in 2022, while in Q2 it was up sequentially by around 7% (Fig 4).

Fig 1. (Source: ceicdata.com) Fig 2. (Data Source: Banco Bradesco Quarterly Reports) Fig 3. (Data Source: Banco Bradesco Quarterly Reports) Fig 4. (Data Source: Banco Bradesco Quarterly Reports) Fig 5. (Data Source: Banco Bradesco Quarterly Reports)

{kind=link}

On the non-NII side of things, the bank's fee & commission income is facing some secular headwinds - mainly in terms of account fees and asset management - and growth has also been very lackluster in real terms (Fig 5). While still growing, I'd also note that card fees look vulnerable as well given the BCB's instant payment system, Pix, operates at structurally lower cost and has seen rapid take-up since launching in 2020.

Tentative Reasons For Optimism

The above notwithstanding, there are some small signs of improvement here. Firstly, although inflation has been ticking up a little in recent months, real interest rates are still in the high single-digit area. The BCB has cut rates by 100bps from a high of 13.75%, and that should help out a little in terms of Bradesco's funding costs. Market NII had been improving sequentially anyway (Fig 6) - as expected given its assets take time to reprice to a higher rate environment - and that should continue over the coming quarters.

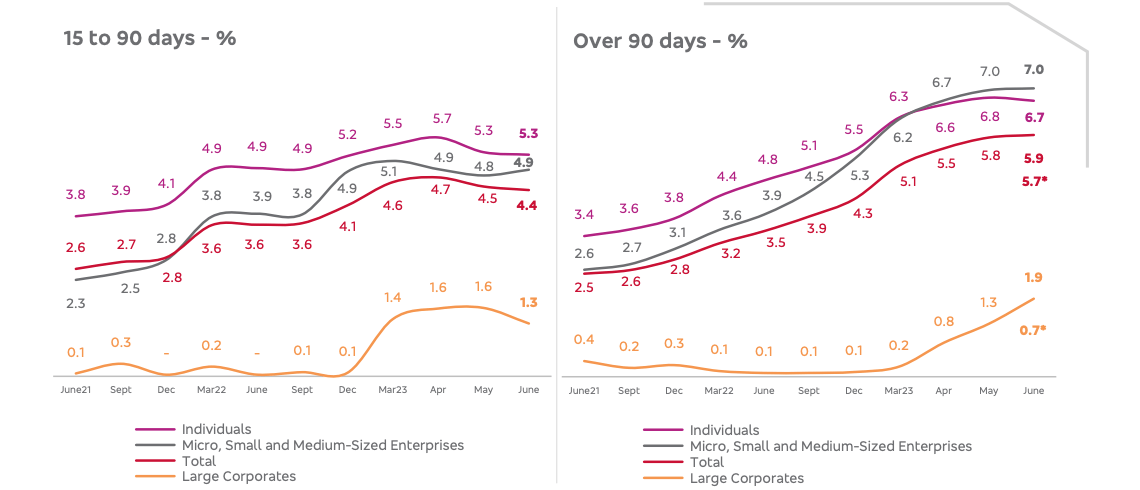

Brazil's economy is also performing better than expected, and I'm hoping that can help lift some of the pressure from bad debt expenses. While loans 90-plus days past due has continued to rise - increasing 10bps sequentially to 5.9% for the last quarter we have data for - the rate is at least slowing. Loans 15-90 days past due have also fallen the past couple of quarters due to tighter underwriting standards (Fig 7). At this point I would also add that I'm not overly concerned even if credit quality was to carry on deteriorating. While that would obviously continue to weigh on Bradesco's earnings, loan loss reserves look prudent here at around 9.5% of gross loans. Loans 60-plus days past due are also covered around 1.4x by allowances, while the bank looks well capitalized given its CET1 ratio of 12.9%.

Fig 6. (Data Source: Banco Bradesco Quarterly Reports) Fig 7. (Source: Banco Bradesco Q2 2023 Results Presentation) Fig 8. (Data Source: Banco Bradesco Quarterly Reports)

{kind=link}

{kind=link}

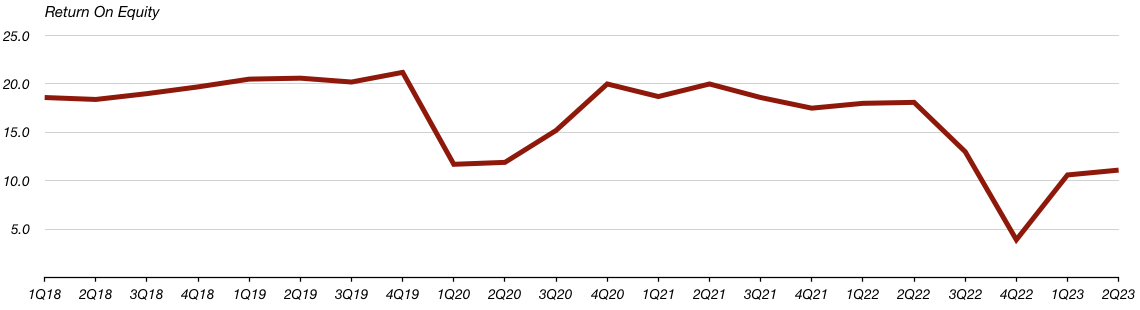

The final point I'd add is that insurance and savings business has been performing quite nicely recently. Bradesco is a major composite insurer in Brazil, and higher income there has been helping to offset the troubles in the bread-and-butter banking business. As a result, the bank's return on equity ("ROE") is still above 10% at the moment (Fig 8).

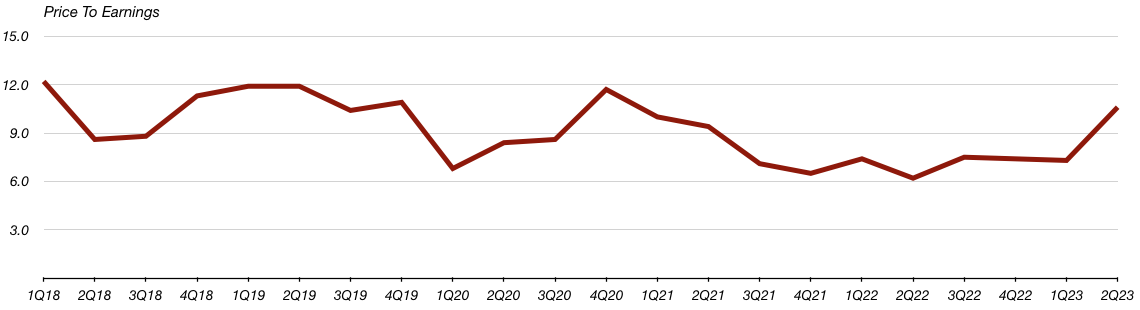

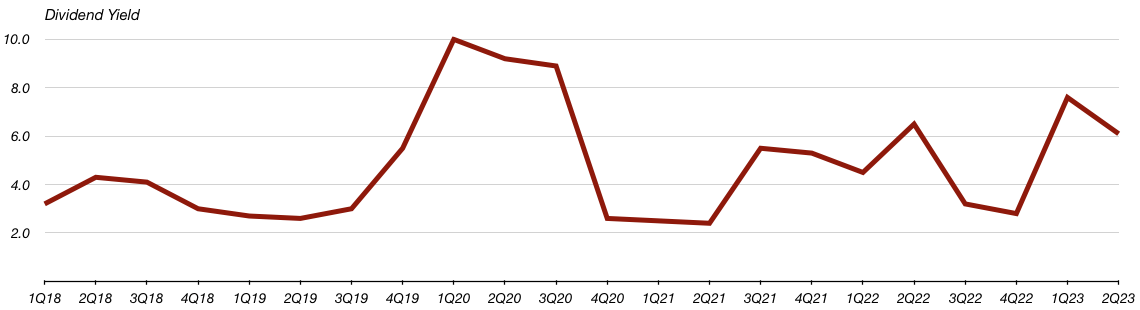

Valuation At The Lower End Of Its Range

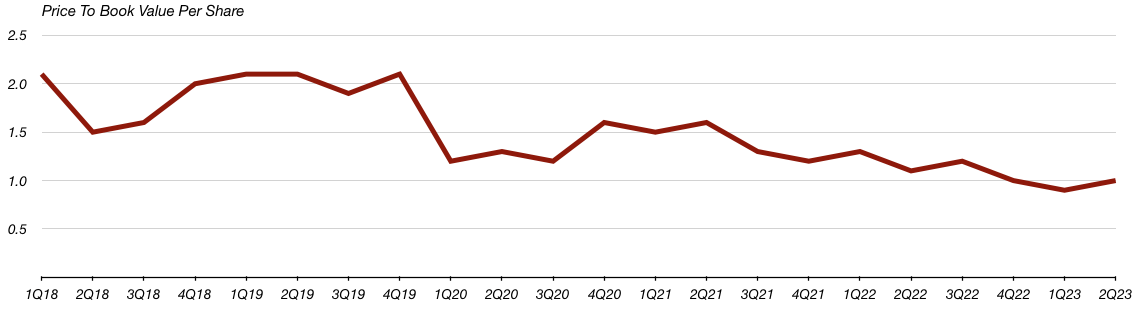

If there's a plus side to wading through some significant macro turbulence, it is that Bradesco's valuation is not too demanding right now. The ADRs representing the preferred shares trade for $2.80 each at time of writing, equal to around 0.95x book value per share ("BVPS"), a TTM P/E of 10.1x, and a dividend yield of around 6.4%.

Fig 9. (Data Source: Banco Bradesco Quarterly Reports) Fig 10. (Data Source: Banco Bradesco Quarterly Reports) Fig 11. (Data Source: Banco Bradesco Quarterly Reports)

{kind=link}

{kind=link}

{kind=link}

That is low relative to the stock's recent historical range (Fig 9)(Fig 10)(Fig 11). The caveat of course is that profitability is also relatively low right now, but that won't be the case forever. At some point the earnings environment will improve and ROE will expand, along with the stock's P/B multiple. A 1.2-1.3x multiple of BVPS wouldn't be aggressive here, even after applying a healthy discount due to the myriad of risks. That would drive a fair value closer to $3.60 for the ADRs.

Risks

Bradesco being a Brazilian bank, there are no shortage of potential risks. The main one right now is that the macro outlook in Brazil deteriorates. Stubbornly high inflation, monetary policy being kept highly restrictive and a knock-on economic downturn would pose a serious headwind to Bradesco's P/L.

Longer term, there are the usual risks that emerging market investors face, with currency depreciation versus the USD and regulatory/political risks being the most obvious ones, and I'd say applying a much higher cost of equity here would be prudent. More specific to Bradesco, my main concern is long-term headwinds to a number of its fee income lines. Asset management (margin compression) and card & account fees (Pix) face structural headwinds that will limit growth. While these are all things that potential investors will need to seriously chew on, I think there's enough in the current valuation to make up for the risk.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Banco Bradesco: Macro Woes Leave Shares Undervalued