BBDO - Banco Bradesco: Q3 Earnings The Bottom Is In (Rating Upgrade)

2023-11-15 05:56:25 ET

Summary

- Bradesco's Q3 results showed a mix of positive and negative aspects, including a reduction in delinquency but concerns about clients' net interest income.

- The bank's Return on Equity (ROE) remains the lowest among domestic peers.

- Despite an attractive valuation, no short-term triggers were identified to support a consistent re-pricing of the stock.

- Delinquency improvements were noted, but concerns about the Net Interest Income (NII) with clients arose due to a decline attributed to an unfavorable product mix.

- Upgrading from bearish to neutral due to recent stock decline, considering $3 target price, Bradesco's dividend potential, and fair valuation.

My initial bearish thesis on the Brazilian bank Bradesco (BBD) was rooted in its status as Brazil's least efficient and highest-defaulting major bank. This was primarily attributed to misguided risk management in recent years, resulting from a flawed lending strategy. The bank faced challenges stemming from excessive provisions made to cover debts associated with troubled companies, exemplified by the toxic loan provisioning related to the Lojas Americanas retail scandal in the recent past.

This year, Bradesco has been actively working to restore critical metrics to healthier levels. Recent quarters have shown some improvement, albeit modest. In the third quarter, Bradesco reported delinquency figures indicating stability, a positive sign for reducing financial risks, lowering expenses related to provisions, and potentially boosting market confidence. However, there was a retraction in customer net interest income due to changes in the product mix.

Since initiating my bearish position on Bradesco, shares have depreciated by approximately 15%, reaching the $3 per share target I had set.

{kind=link}

Consequently, despite the Q3 results not being exceptional and lingering concerns about Bradesco's recovery, I am upgrading my bearish position to neutral. I believe that, at the current valuation, the Brazilian bank's shares are reasonably priced.

Bradesco's 3Q23 Results

Bradesco recently released its third-quarter earnings, which, in my perspective, were not particularly encouraging. The bank reported a net income of R$4.6 billion in the financial domain, showing a resilient 2.3% increase from the previous quarter. Operating income also displayed a healthy trajectory, growing by 5% year-over-year.

{kind=link}

Despite this commendable performance, the Return on Equity ((ROE)) for the quarter remained at 11.3%, below the desired level, indicating a need for improvement. The loan portfolio expanded by 1%, primarily driven by robust growth in the corporate sector.

Notably, lousy debt provision expenses ((PDD)) reached R$9.2 billion, marking the first quarter-to-quarter drop in PDD (excluding the 4Q22 Americanas PDD) of this credit cycle that commenced in mid-2021. The reduction was influenced by the improved portfolio profile of the mass segment, with expenses concentrated in older vintages, while more recent credit vintages reported positive results.

Examining Bradesco's insurance unit, a net profit of R$2.3 billion was reported, showing a slight decline of 0.8% year-over-year but a substantial increase of 57.5% quarter-over-quarter. The insurance unit's impressive profitability ((ROE)) stood at 23.9%, accounting for 50.9% of the conglomerate's total profit.

The insurance operating result reached R$4.6 billion, down 4.5% year-over-year but marked by robust growth of 33.3% quarter-over-quarter. The unit's strong performance in all segments is attributed to sales expansion, an improvement in the commercialization index, and positive financial results.

Service revenues amounted to R$9.1 billion, showing positive trends with a 4.1% quarter-over-quarter and 2.9% year-over-year increase. Positive highlights include the financial advisory line, reaching R$526 million (113.8% year-over-year growth), fund management (8.5% year-over-year growth), and consortia (12% year-over-year growth). However, there were negative aspects, with revenues from current accounts falling by -3.8% year-over-year and billing and collections declining by -2.9% year-over-year.

Administrative expenses remained well-controlled, totaling R$13.7 billion, with a negligible increase of just 0.4% year-over-year and 0.8% quarter-over-quarter. The quarter was primarily impacted by the rise in personal expenses, reflecting the effects of the layoff that occurred in September 2023.

Progress in One Aspect, Setback in Another

Over the past few quarters, Bradesco needed to demonstrate improvement in two specific aspects: a halt to the deterioration in delinquency rates and a positive financial margin with the market, and these expectations were met.

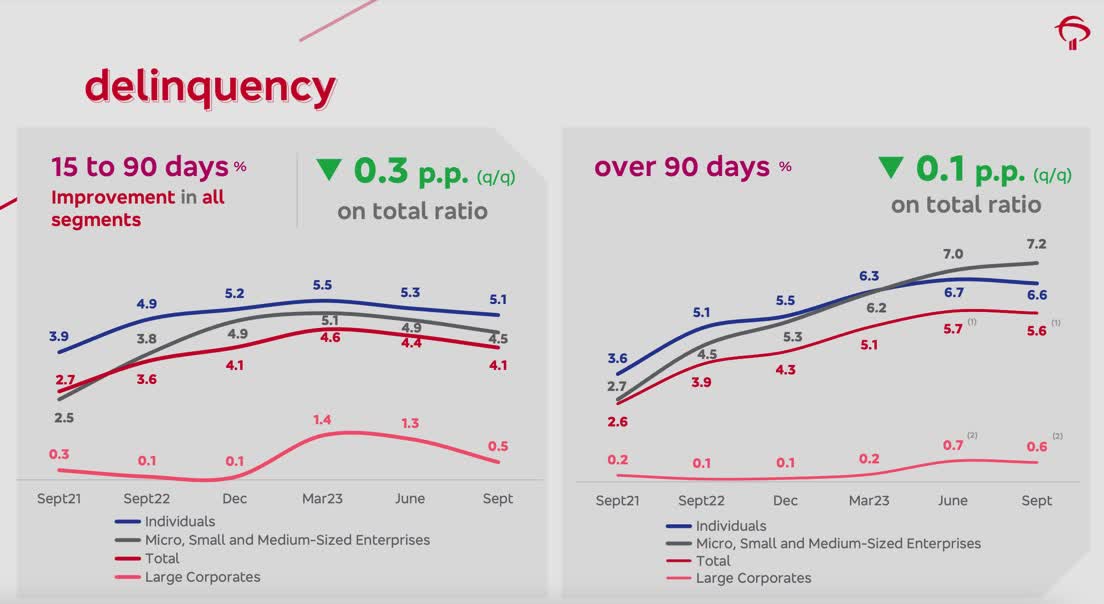

Although Bradesco improved its Non-Performing Loan (NPL) ratio by 10 basis points (excluding Americanas), the coverage ratio fell to 155.2%, causing apprehension. The NPL 90+ increased from 5.9% in 2Q23 to 6.1% in 3Q23, considering the impact of Americanas. Excluding this effect, the NPL 90+ would have decreased from 5.7% in 2Q23 to 5.6% in 3Q23, marking the first improvement in this credit cycle.

{kind=link}

The short-term default rate (15-90 days) improved across all segments, reflecting the better performance of new credit lines and potentially indicating a further improvement in the NPL 90+.

When compared to its main domestic peers, Bradesco's 90+ day delinquency rate is notably higher:

- Banco do Brasil ( BDORY ): 2.8%.

- Itaú Unibanco ( ITUB ): 3%.

- Santander Brasil ( BSBR ): 3%.

- Bradesco: 5.6%.

Despite these advancements, relief in Bradesco's defaults seems limited, given its significant exposure to low-quality credit lines. Looking ahead, a gradual improvement in the macroeconomic environment in the second half of this year could provide some relief.

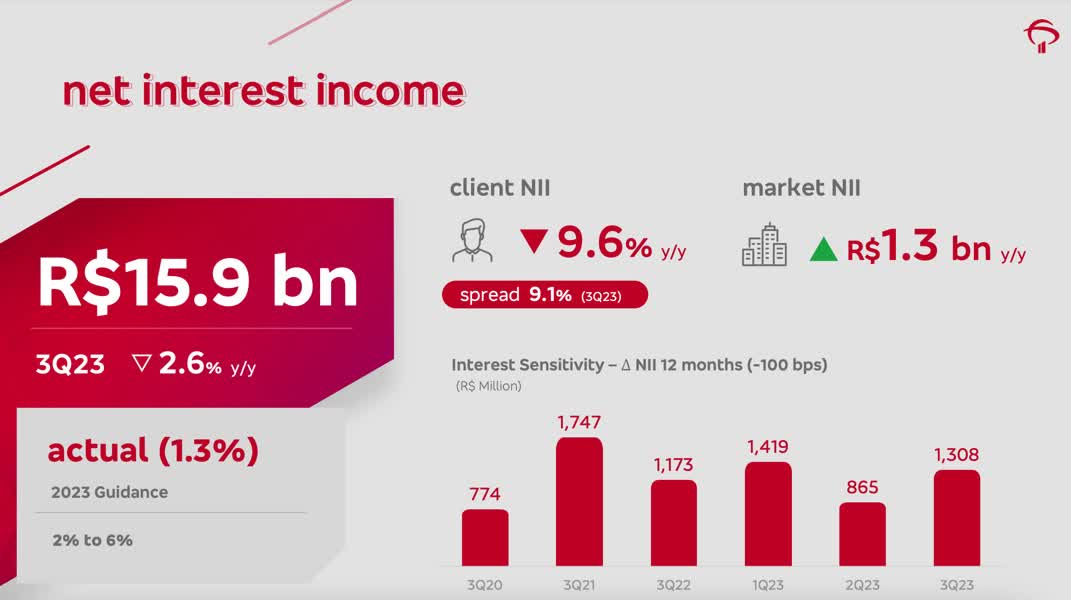

However, a new concern emerged regarding the Net Interest Income ((NII)) with clients, which experienced a 4.9% quarter-over-quarter decline, the most significant drop since 2017, ending the quarter at R$15.8 billion (a 5% increase in the quarter but a 10% decrease from 3Q22). This drop is attributed to an unfavorable product mix, lower spreads, and slower growth in the loan portfolio.

{kind=link}

The balance sheet was impacted by a reduced lending volume to micro and small companies, which typically offer higher returns due to their higher risk. In the third quarter, loans to small and medium-sized companies decreased by 1.1%, while loans to large companies increased by 3.2%. During the earnings call , Bradesco executives indicated that origination in this segment is expected to increase in the fourth quarter.

Valuation and Dividends

Assessing the third quarter of 2023, indications suggest that Bradesco will encounter substantial challenges in restoring profitable growth in net interest income and the loan portfolio.

The recovery of profitability, as measured by Return on Equity ((ROE)) currently at 11.5% - the lowest among domestic peers - to levels nearing 20%, might take longer than I initially expected. It will likely trail behind its primary domestic peers, particularly Banco do Brasil and Itaú, which already exhibit an ROE surpassing 20%. Despite an attractive valuation compared to its domestic peers, at a forward price-to-earnings (P/E) ratio of 11.63x, which falls to 8.57x for 2024, and a price-to-book (P/B) ratio of 0.99x, no short-term triggers have been identified that would support a consistent re-pricing of the stock.

Seeking Alpha

For 2024, Bradesco's forecast envisions a gradual recovery in revenue driven by the normalization of the market margin due to the reduction in the interest rate in Brazil (Selic). Growth in the margin with clients is anticipated due to higher credit volumes, wider spreads, and increased tariff revenues. The insurance unit is expected to maintain solid results. Regarding expenses, stability in credit provisions and containment of administrative expenses are anticipated.

With my target price for Bradesco set at $3 per share, I now perceive the bank as fairly valued. Consequently, for 2023, considering the bank's payout of meager 3% and my forecast of an annual net profit of $3.58 billion, the dividend per share is estimated to be around $0.15, implying a yield of 5.1%. Applying an ROI of 5%, the fair value is precisely $3.07.

Bradesco's filings, Seeking Alpha, table compiled by the author

Conclusion

Bradesco's third-quarter results presented a mixed picture, with positive aspects, such as a reduction in the increase in delinquency, juxtaposed with concerns about clients' net interest income. However, the overarching issue persists - Bradesco's Return on Equity ((ROE)) remains the lowest among domestic peers, and the prospect of a return to above 20% seems distant.

Consistent with my previous article, where I had taken a bearish stance on Bradesco with a target price of $3 per share, this position has materialized, with the shares declining by 15% since the end of July. Considering Bradesco's dividend potential for the year, I view the current share price of $3 as reasonably priced. Consequently, I am upgrading my sell thesis to neutral for Bradesco.

For further details see:

Banco Bradesco: Q3 Earnings, The Bottom Is In (Rating Upgrade)