BDORY - Banco Bradesco: Rising Default Rates And Drop In Net Profit Should Worry Investors

2023-10-18 07:58:13 ET

Summary

- Banco Bradesco is well-positioned to benefit from Brazil's improving economic stability and growth prospects in the banking sector.

- However, its results have been below expectations compared to competitors, especially in terms of services and technological management.

- The bank's recent disappointing quarterly performance, low net profit, and increased provisions for loan losses raise concerns about its ability to remain competitive.

Investment thesis

Brazil's economic stability has been gradually improving, along with growth prospects in the banking sector. Banco Bradesco S.A. ( BBD ), or simply Bradesco, as one of the country's main banks, is well-positioned to benefit from this growth. Furthermore, its solid customer base and wide range of financial services make it resilient to economic fluctuations.

However, in my view, when compared to competitors, especially Itaú Unibanco ( ITUB ), Banco do Brasil S.A. ( OTCPK:BDORY ), and even Banco Santander (Brasil) S.A. ( BSBR ), its results have been far below expectations. This can be seen in services and, for example, in technological management, where digital channels have not been adopted by the public as much as expected, whether due to a lack of interactivity or other reasons.

Therefore, I believe the most pertinent decision at the present moment is to hold your stake in the company. And, in the face of a pessimistic scenario and uncertainties, selling may become a relevant option in the coming periods, since past results have been steadily worse quarter after quarter since 2021. It's important to closely follow economic trends and Bradesco's actions, as well as competition in the financial sector, to make a final decision regarding investment.

A bit about Banco Bradesco

Banco Bradesco is one of the largest financial institutions in the country, founded in 1943 in the city of Marília, in the countryside of São Paulo, under the name Banco Brasileiro de Descontos. The bank offers services and products that include credit operations and deposit intake, credit card issuance, consortium, insurance, leasing, collection and payment processing, supplementary pension plans, asset management, and intermediation and brokerage of securities.

The bank also offers digital banking services, such as mobile apps and internet banking, to facilitate customer access to their services. Banco Bradesco has around 3,000 branches throughout the country and also offers international banking services in several countries around the world.

A snapshot of Bradesco's latest news

The news about the failure in Bradesco's app is a reflection of the increasing technological vulnerabilities that financial institutions are currently facing, which could have been caused by a variety of factors, such as a technical issue in the app, a cyberattack, or an overload on the bank's servers.

{kind=link}

In this case, the failure of an essential tool like Pix is especially problematic, given the importance of this instant payment system in Brazil. Customers rely on the bank to ensure uninterrupted access to their funds and to carry out transactions securely and effectively. When the financial institution experiences disruptions, it can cause serious inconveniences for users and even unexpected financial losses.

This news highlights the bank's urgent need to invest more in infrastructure and technology to ensure the stability of its digital services. Additionally, it's crucial that they have solid contingency plans to deal with failure situations and frequent maintenance, so as to minimize the impact on customers, as it was found by users in this event that the system was down for hours. With digital platforms being crucial, mistakes like this are costly, not only money-wise, but in terms of reliability from investors and customers.

{kind=link}

The statement from Bradesco's CEO , Octavio de Lazari: "We extended more credit than we should have," and that the delinquency rate would remain high in the first half of 2023, indicated that the bank was expected to continue facing difficulties, even with expectations of improvement seen in presentations of the bank's results. Moreover, the need to set aside a considerable amount of resources to cover loans to the retailer Americanas S.A., which sought bankruptcy protection due to accounting inconsistencies resulting from fraud, has been and is an immense concern and headache.

In my opinion, the news about Banco Bradesco's stock hitting the lowest level in nearly two years after a disappointing quarterly performance was an extremely worrying sign for investors and highlights the challenges the bank is facing. The 75% drop in net profit for the fourth quarter, along with the significant increase in provisions for loan losses, is a considerable setback. This reflects the challenging economic environment, as well as the questionable credit-granting decisions that were made during the pandemic and are now weighing in substantial losses for the company.

Highlights from the latest earnings release

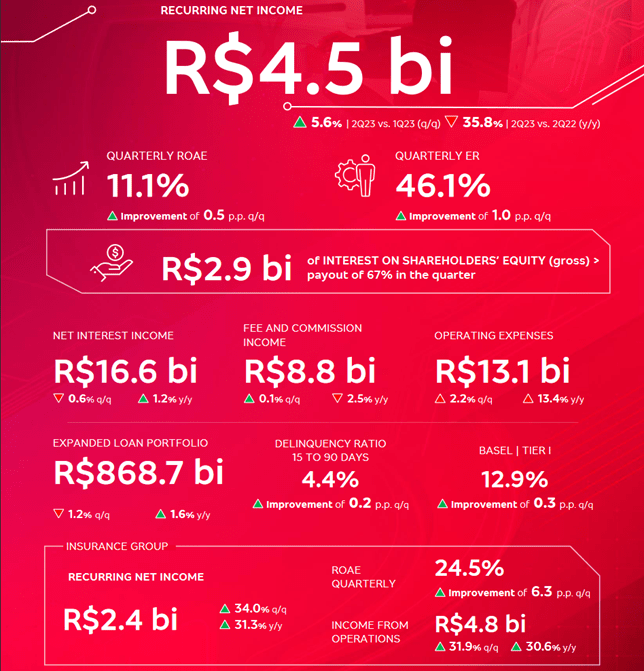

One of the most significant negative highlights I observed in the latest earnings release is certainly the drastic reduction in net profit by 35.8%, compared to the same period of the previous year from 7 billion. This is even more alarming when we see that, from these 4.5 billion, more than 2.4 billion comes from the revenue of the insurance group, more than half of the total profit. This shows that the insurance model has been successful, however, this alone is certainly not enough to cover the operational costs that increased to 13.4% per year and other bank expenses. The Basel ratio at 12.9% remained stable and is still within the healthy spectrum between 11% and 50% stipulated in the country by the Central Bank, which is positive.

The prominence of the insurance model overshadowing other outcomes clearly highlights the deficits in the bank's other sectors tied to the actual banking model (branches, applications, and online services). This includes aspects such as fees, credit offerings, and the sales of additional products and services. Such facts, as well as the reduction in revenue and costs, are emphasized when analyzing the ROAE, denoted by the bank, which increased by 0.5 p.p. to 11.1% compared to the last quarter. However, the same period in 2022 was at 18.1%, a significant difference of 7.0 p.p. Once again, we see significant variations in a short timeframe.

In my opinion, customers are likely less engaged with contracts and services. This disengagement becomes evident when we see a 4.4% rise in delinquencies between 15 and 90 days, up from 3.6% in 2Q2022, and an astonishing 94.2% in Loan Loss Provisions. These figures suggest that Bradesco's customers are struggling to meet their financial obligations and repay their debts, or they might be unhappy with the bank's offerings and how it operates and manages its services.

{kind=link}

Even though Banco Bradesco is still one of the largest and most influential banks in Brazil, these facts will undoubtedly have a massive and ongoing impact on short- and medium-term results if they do not receive special attention, better flexibility, adaptation to the current economic scenario, and the needs of their customers, as well as a slowdown and better filters in credit approvals.

Valuation

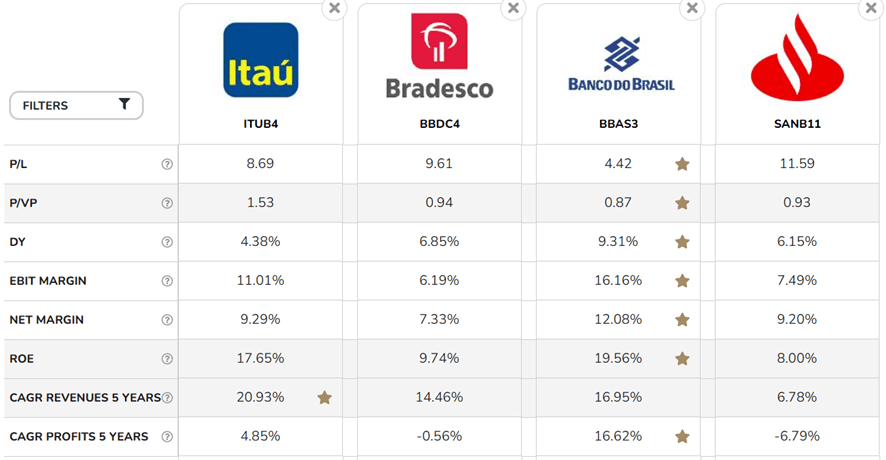

I could compare Bradesco with other more modern banks, but I chose the major traditional banks operating in Brazil, Itaú, Banco do Brasil, and Santander Brasil, which are direct competitors of Banco Bradesco.

P/L = P/E; P/VP = P/Book (Investidor10)

{kind=link}

That said, when we look at Bradesco's P/E of 9.61, even though it's not the highest, we have, on the other hand, Banco do Brasil's P/E of 4.42, less than half, which, despite being a state-owned bank, has had huge market optimism due to its excellent management, extremely competent governance, and very good compliance.

As a Brazilian myself, I recognize the general skepticism surrounding state-owned enterprises in our country. However, in the current scenario, where we have a private bank like Bradesco underperforming and a state-owned entity like Banco do Brasil achieving impressive results despite inherent governmental challenges, the assumption that Bradesco will bounce back shortly seems riskier. It's less likely that Banco do Brasil would abruptly lose its current stability and positive performance.

If we take a moment to analyze and ask ourselves: "But what about the P/Book lower than Itaú's and close to Santander's?", yep, but the Book Value is just a basis, and there are many variables involved that lead to values that come from many years prior to the present. For instance, all the startup capital from businesses related to the bank, including loans made, cash flow, and potential angel investors, are influenced by the fact that the accounting does not precisely reassess these and other older assets regularly, which results in inaccurate determination of the P/Book ratio.

Santander, which, in theory, would also be cheap, is also having terrible results, just like Banco Bradesco.

Banco Bradesco still has a good Dividend Yield of 6.85%, even with a payout above 128%, much higher even when compared to Itaú, for example, which currently has a 50% payout. For those interested in dividends, Bradesco is still a relevant choice, however, given recent results, it may not be the wisest option for the bank to continue distributing such large dividends instead of focusing on short- and medium-term financial control.

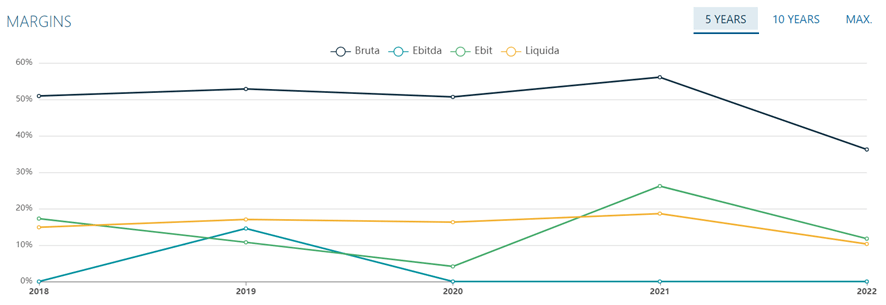

Bruta = Gross; Líquida = Net (StatusInvest)

{kind=link}

Bradesco's EBIT margin and net margin of 6.19% and 7.33% in the current quarter, the lowest compared to its peers, show how its profitability and operational and product efficiency have been declining since 2021. This is also further emphasized by the ROE of 9.74%, thus, very low returns, only losing to Santander with 8%. The revenue CAGR at 14.46% and the profit CAGR at -0.56% also highlight a reduction in Bradesco's profits and revenues, only trailing Santander, while they soar at Banco do Brasil and Itaú, due to good management of their resources

In my opinion, this strengthens the fact that it is best to hold on to the bank's shares and evaluate its behavior in the face of circumstances, as its biggest competitors have been showing much superior performances.

Risks

Several risks can impact Bradesco's stability and financial performance. First, accuracy in underwriting insurance policies is crucial, as the bank is heavily involved in the insurance business. If pricing models are inaccurate, claims could exceed issued premiums, potentially resulting in significant losses.

Economic recessions pose an inherent risk to the banking sector, affecting asset quality, borrowers' repayment ability, and consequently, Bradesco's results. Particularly, the growing competition from fintechs and the aggressiveness of established competitors can put pressure on the bank's profit margins and market share.

Reputational risk is also a concern, as any involvement in scandals or unethical practices can undermine customers' and investors' confidence in the institution, as was seen in the news of the bank's app and its services being down for several hours during one day.

The CET1 (Common Equity Tier 1) ratio can also be negatively impacted by an increase in provisions or actuarial liabilities, as well as by the reduction in the fair value of assets related to Pension Plans and Health Benefits for Employees and former employees managed by Sponsored Entities.

{kind=link}

Bradesco's rise to prominence as one of the largest banks globally, not just in Brazil, is no accident. There's potential for its management to mitigate any negative impacts on its financial performance by diversifying its operations. For instance, the bank has recently shown an interest in expanding its presence in significant international markets, including Mexico . Additionally, it's focusing on improving the creditworthiness assessment of its clients, extending credit and loans to a broad spectrum of customers, from low-income individuals to large corporations.

Should these strategies prove successful, there could be a positive uptick in the bank's share prices. This potential rise might represent a missed opportunity for investors who fail to capitalize on this phase.

Another risk to consider, tied to the upcoming results of the third quarter of 2023, is Bradesco's recent mention of its growing involvement in the agribusiness sector, increasing its market share through its digital platform. Agribusiness plays a crucial role in Brazil's economy, involving significant capital movements and boasting an exceptionally low and distinct default rate, making it an attractive sector for any banking institution in the country.

I suppose if acquisitions and the expansion of international operations and agribusiness credit show substantial returns, as well as if net income continues to grow (despite the significant drop compared to last year) and loan loss provisions do not increase, we might see EBIT and other margins stabilizing.

Such a scenario would favor Bradesco and enable what many Brazilian investors are currently speculating — a rise in bonus shares to 20% this year, up from the 10% maintained since 2020. This would showcase the bank's resilience in its strategic choices and its commitment to thorough preparation, effectively diversifying its risks and investments while embracing digital trends. Consequently, this could boost market confidence, reduce the spread of negative news on social media, and ultimately lead to an increase in its stock price.

Final words

The current situation at Banco Bradesco raises significant concerns for investors. Recent disappointing quarterly performances, marked by a drastic reduction in net profit in the second quarter and a substantial increase in provisions for loan losses, represent a serious setback. These inferior results compared to its main competitors, such as Itaú and Banco do Brasil, raise grave concerns about Bradesco's ability to remain competitive in the market.

The risks mentioned, such as accuracy in underwriting insurance policies, economic slowdown, competition, reputational risk, and the Basel Index, also add a layer of uncertainty for investors. Additionally, the customers' lack of adherence to the bank's digital channels is troubling and indicates a need for significant improvements in digital strategy.

Although Bradesco is a robust financial institution with a global presence, the current financial indicators and challenges faced lead me to consider a more cautious approach. Maintaining the company's current shares might be a sensible decision at this time, while closely monitoring the bank's performance and its ability to adapt to changes in the economic landscape and customer preferences.

For further details see:

Banco Bradesco: Rising Default Rates And Drop In Net Profit Should Worry Investors