BDORY - Banco do Brasil: Alpha-Generation May Ebb Away

2023-05-09 13:11:21 ET

Summary

- BDORY has been a solid source of alpha over the last 12 months, even as some key metrics have hit 5- and 10-decade highs.

- We don’t believe this is sustainable and expect 2023 to be more challenging.

- The technicals also support a cautious stance.

So Far So Good

Banco do Brasil (BDORY) is a high-pedigree diversified bank (see image below for a list of services) that has been around for over 200 years now. Whilst the core business comes from Brazil, it also engages in international operations (it's been doing this since 1941) in over 119 countries across the world.

{kind=link}

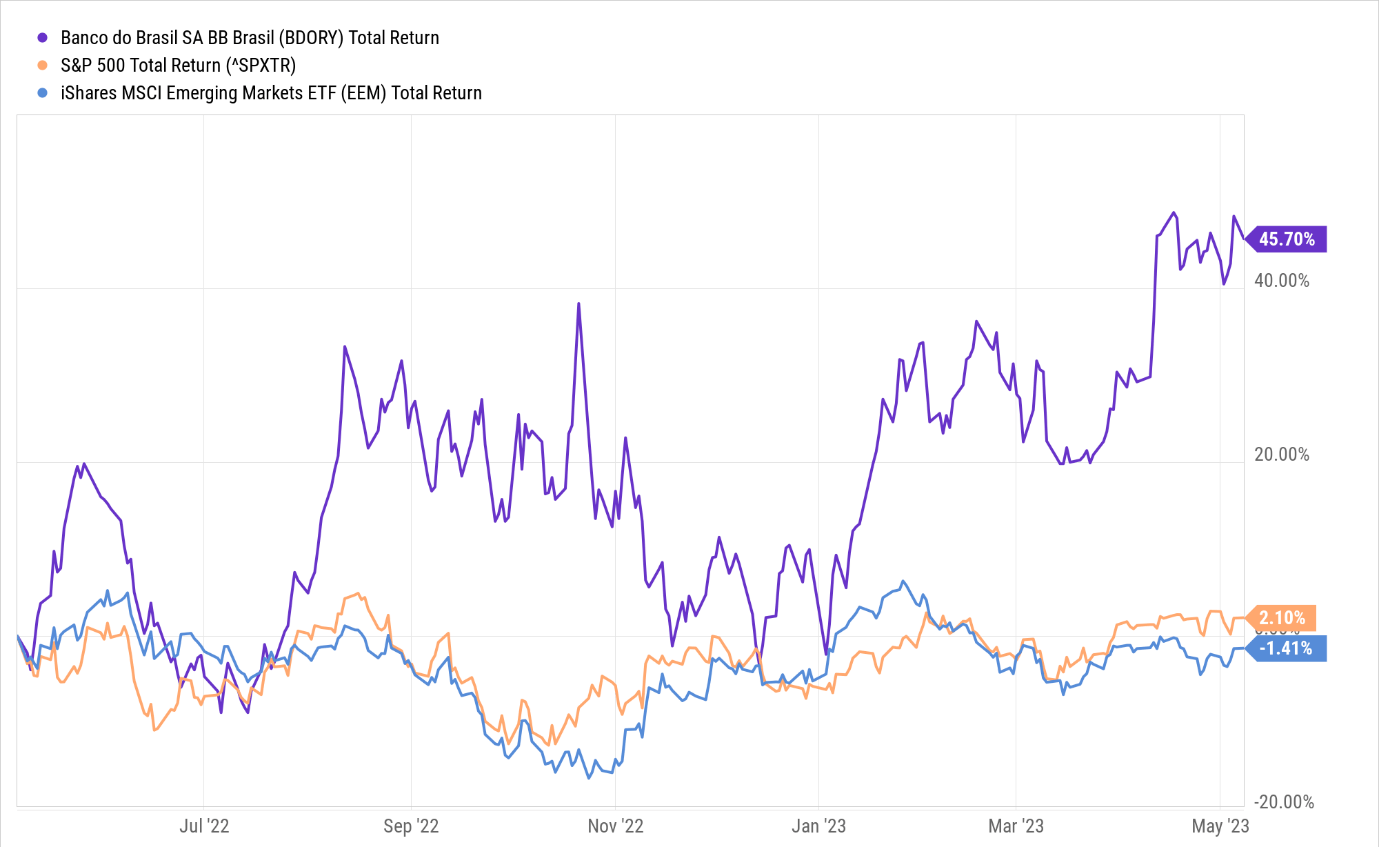

Over the past 12 months, BDORY's stock has been a rewarding play for investors, delivering returns of 45%; as a result, it has not just trounced US stocks which have only seen low single-digit returns, but as well, a flagship emerging market basket (the ETF-EEM), which has only eroded wealth during the same period.

{kind=link}

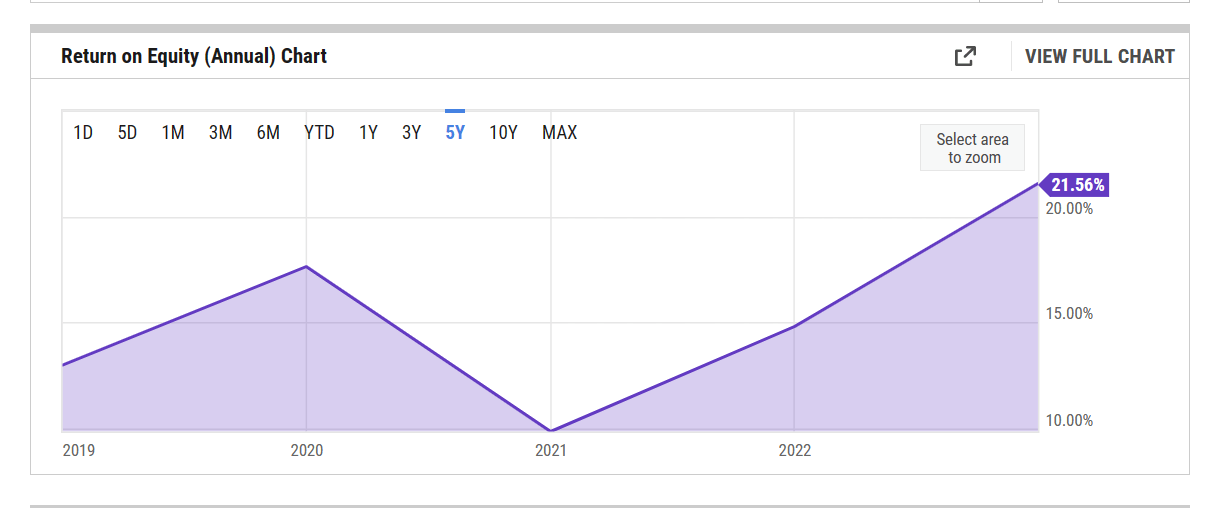

There is good reason for BDORY's strong performance; there are different gauges to measure quality execution and one of them is the Return on Equity (ROE) metric. Note that BDORY's ROE of 21.5%, at the end of FY22, was the highest it's been in five years. For context, the average ROE for Seeking Alpha's coverage of 66 diversified banking stocks is only around 12% .

{kind=link}

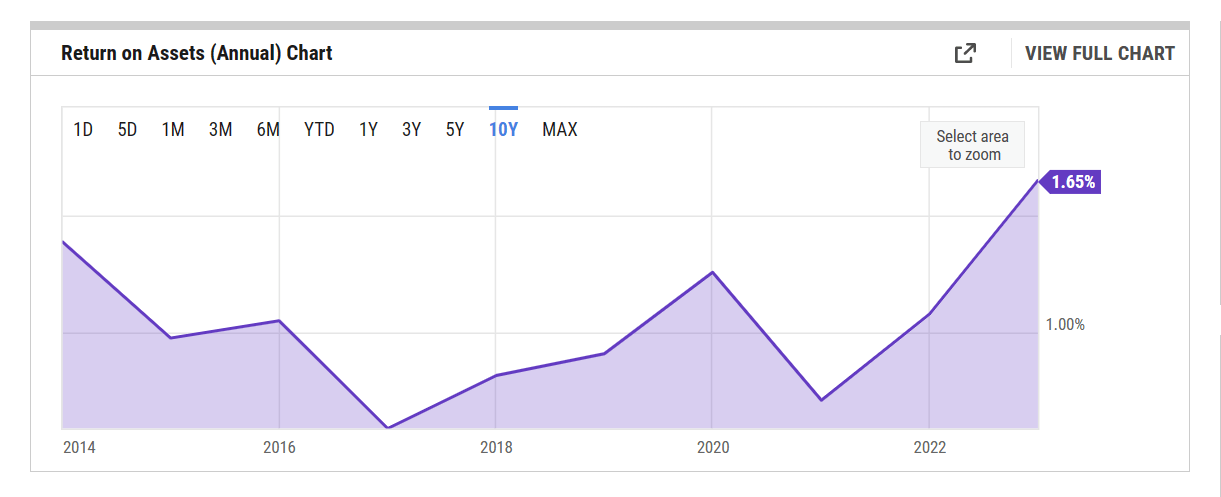

Some would say that the ROE metric doesn't give a good sense of the risk taken, as certain banks can always lever up and generate excess returns on a low equity base. To negate the leverage flaws of the ROE metric, we've switched our attention to the Return on Assets (ROA) metric which gives you some semblance of the quality of assets that BDORY operates. Well, as far as the ROA is concerned, you'd be interested to note the performance was even better than the ROE as last year's figure of 1.65% was the best in over 10 years. To highlight how sturdy this is, also do consider that the average for the peer-set was just 0.95% .

{kind=link}

BDORY may be in a good way, but looking ahead, we don't believe it would be realistic to expect BDORY to keep up these high standards; rather investors are advised to be a tad cautious. Here are a few reasons why we are less gung-ho about BDORY's prospects.

Curb The Enthusiasm

The bank's core business, as represented by net interest income ((NII)) growth has been chugging along very nicely in recent periods. Last year this grew by 24%, and in Q4 alone, growth came in at an impressive rate of 45% (10% sequential increase). While there are other factors at play, much of this has been on account of a hefty policy rate, which has filtered through to better repricing of BDORY's loan portfolio. Favorable treasury results have played a role as well. Coming back to policy rates, note that the Selic rate has been consistently high at the 13.75% mark for six straight meetings, but it now looks increasingly likely that we could be on the cusp of a pivot soon enough and this will no doubt weigh on BDORY's NII trajectory.

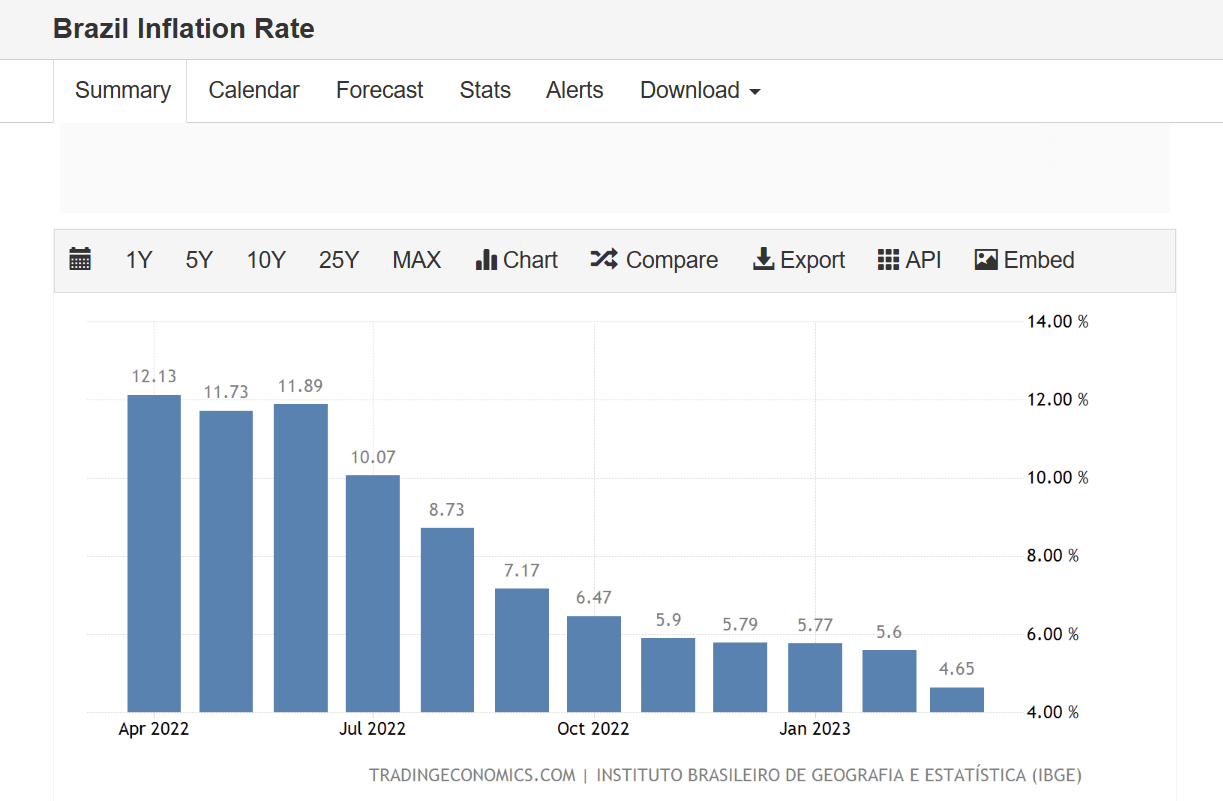

The Brazilian central bank will understandably have been pleased to note that inflation had been sliding sequentially for nine straight months, and recently it also dropped below the 5% mark, the first time in 26 months!

{kind=link}

While these trends have been encouraging, they haven't yet pushed ahead with rate cuts as there were some fears that the government would continue to hamper the fiscal position with excess populist spending, which would only likely kickstart inflationary trends yet again. However, one is enthused to note that under a new fiscal framework, growth in future government spending will only be limited to 70% projected revenue growth in that year. Put another way, spending will likely lag revenue growth.

On the cost front, one also ought to commend BDORY for maintaining one of the lowest cost-to-income ratios around; it came in a just 29.4% last year (to get a sense of how impressive this is, do consider that globally the cost-to-income average is around 55% , and for Latam banks alone it is close to 60% ). Looking ahead, it is not going to be sustainable to keep the cost to income at sub-30% levels, as OPEX growth in FY23 will likely be a lot higher as management doubles down on investments in digitization and IT initiatives. All in all, admin expenses which grew at only 5.5% in FY22 will likely grow at a higher threshold of 7-11% in FY23.

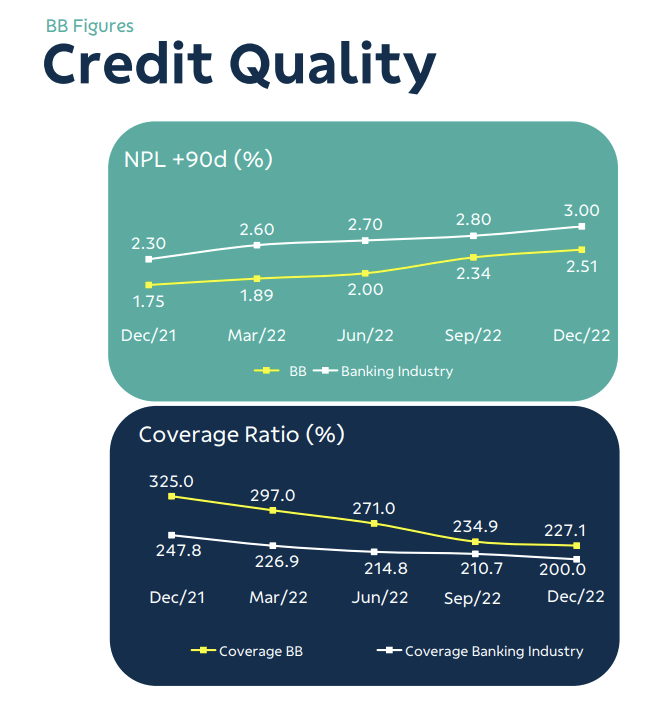

The heightened interest rate regime in Brazil is also unlikely to do anything to alter the deteriorating asset quality position of BDORY. Already over the last few quarters, we've seen the gap between BDORY's asset quality (the positive variance in the NPL ratio was around 70bps at the end of H1, now it is less than 50bps) and the industry narrow. Some may even question if BDORY is taking ample precautions to provide for its bad assets. BDORY has exposure to the Brazilian retailer- Americanas, which had recently filed for bankruptcy but the bank only provided for 50% of the exposure. Recent reports suggest that BDORY, alongside other creditors, could take an 80% haircut on their claims; one way or another, expect this to reflect unfavorably on the bank's forward earnings.

{kind=link}

For the uninitiated, it's also worth noting that BRODY is controlled by the Brazilian government which has a 50% stake in it. I suspect this facet of BRODY could prove to be a tricky hindrance, particularly when you consider that you have new management at the helm of affairs. State-controlled entities often have to put socialistic objectives ahead of profit-making, and this is something even the new Lula government has been keen to reiterate. Given new CEO- Tarciana Medeiros's limited experience at the top level of a bank, she remains vulnerable to political pressure and may be promoted to divert credit to economically sub-standard avenues.

Closing Thoughts

Finally, we'll conclude with some thoughts on the technicals.

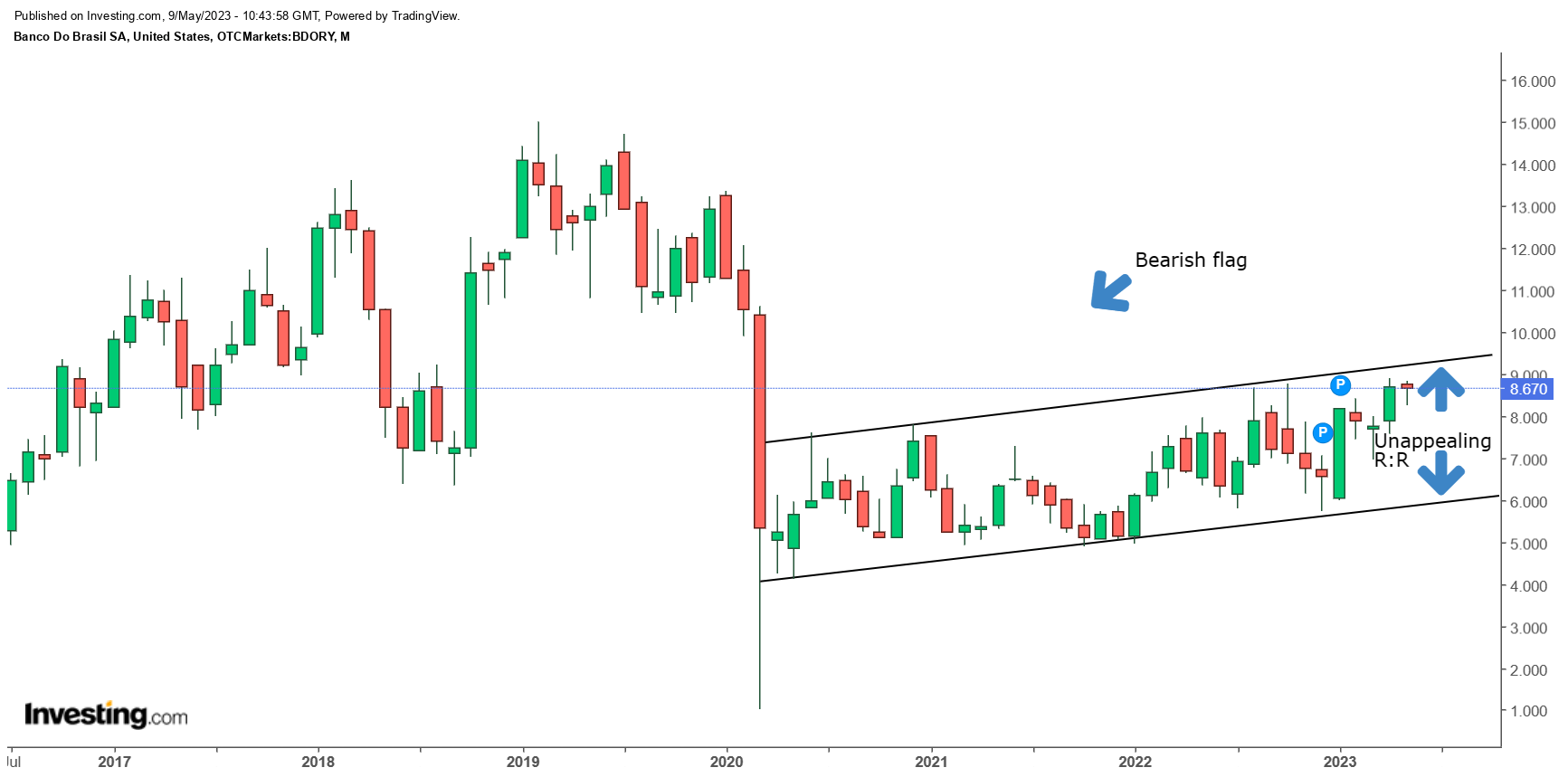

On BDORY's monthly chart, we can see that there was a rapid descent in the price action since early 2020; However, since then, over the last three years, the stock has been chopping around within a slight ascending channel. Taking a step back, and looking at the broader canvass, it looks like we have a bearish flag pattern . Even if you want to dispute the flag thesis and suggest that this is just routine base-building, we don't think this is the right time to enter the stock as its almost inching the upper boundary of its 3-year range; the preferable entry point would be somewhere closer to the lower boundary (around the $6 levels) where the risk-reward looks more appealing.

{kind=link}

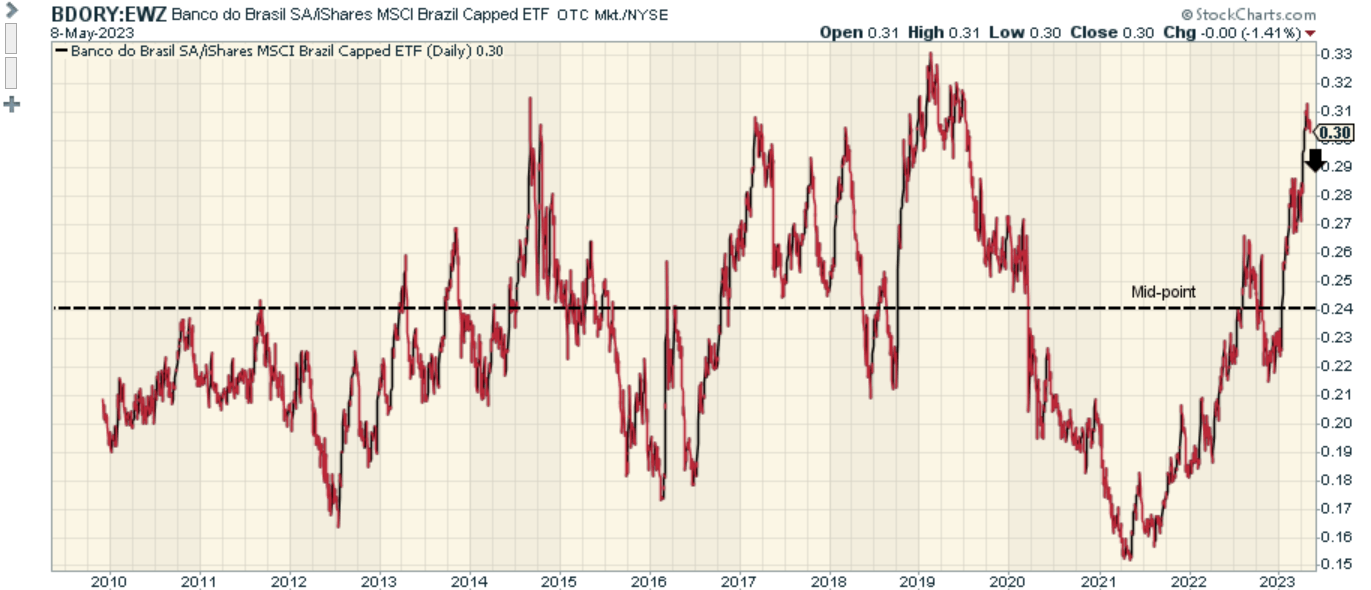

The chart below juxtaposes the strength of BDORY's stock against its peers from the popular iShares MSCI Brazil Capped ETF ( EWZ ). We can see that this ratio tends to move in cycles, and whilst BDORY may have worked as an interesting mean-reversion pick in 2021, that certainly isn't the case now. Rather the current relative strength ratio is 25% away from the mid-point of the range, and not far from hitting all-time highs which is certainly not ideal for those contemplating a long position in BDORY.

{kind=link}

For further details see:

Banco do Brasil: Alpha-Generation May Ebb Away