BDORY - Banco do Brasil: Despite The Risks Still A Solid High-Yield Stock

2023-05-18 12:49:18 ET

Summary

- Shares of Banco do Brasil are up more than 45% over this year alone.

- The latest quarterly results reinforced the strong profitability position of the Brazilian bank, reporting net income growth of 29% YoY.

- The diversification of Banco do Brasil's credit portfolio has been critical to its excellent profitability numbers and its ability to continue paying good dividends.

- Although shares of BDORY trade at 3.62 times its forward P/E ratio, I see limited upside due to risks related to bank governance.

Banco do Brasil ( BDORY ) has stood out in the past few years because of its solid balance sheet, high-profit margin, and high-efficiency ratio compared to its major domestic peers.

The strong profitability of the Brazilian bank - reinforced recently in the latest Q1 results - has made the stock yield excellent dividends to its shareholders, and my bullish thesis is around this.

Despite the governance risks due to half of the bank's shares being owned by the state, I see good reasons for the bank to continue to report solid results, mainly because of its diversified credit portfolio and its exposure to Brazilian agribusiness.

Banco do Brasil's Strong Profitability

As it has shown for at least the last two years, Banco do Brasil has strengthened its strong profitability position every quarter. In its latest Q1 2023 earnings, the bank reported an adjusted net income of U$1.72 billion, representing an increase of 29% compared to last year.

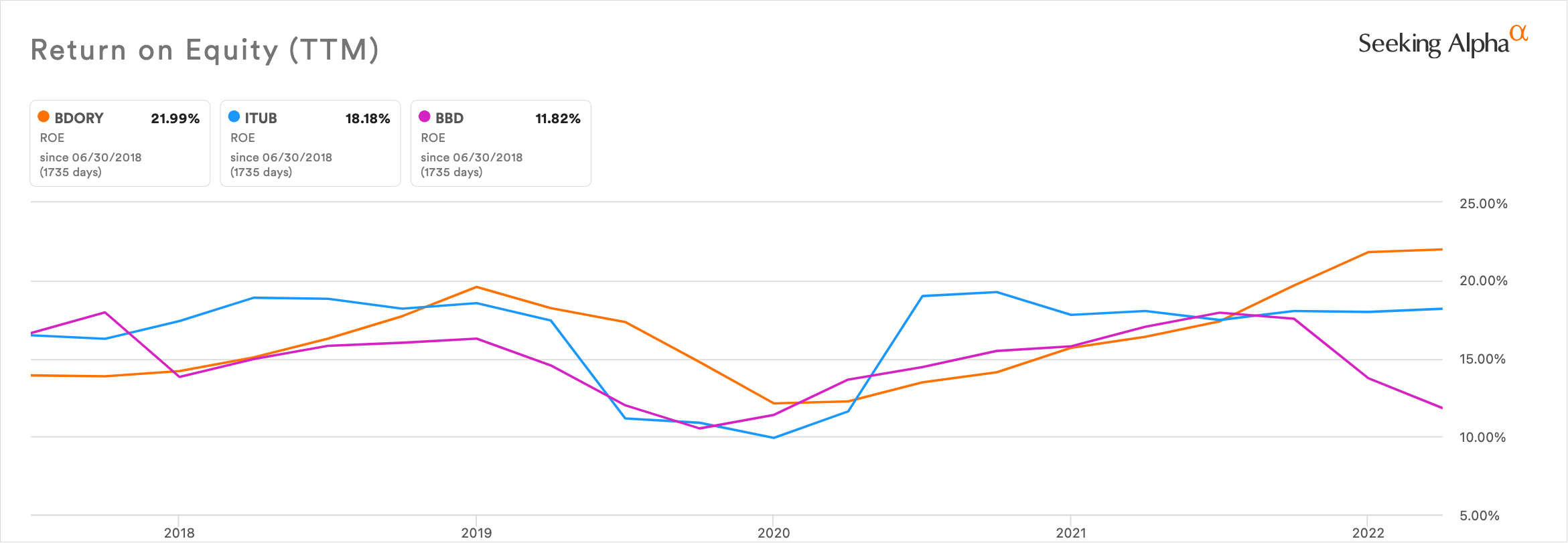

This result gives the bank a current return-on-equity (ROE) of 21%, which has been progressively increasing since 2020 and remains at a robust average of 16.3%. Even during periods of severe economic turbulence in the Brazilian market, such as the 2016 recession and the COVID-19 crisis in 2020, Banco do Brasil has remained profitable with good ROEs of 8.1% and 10.6%, respectively.

To get an idea of how significant these ROE results from Banco do Brasil really are, just take a look at this metric across its major domestic private bank peers.

Comparing Banco do Brasil's ROE with the second and the third largest banks private banks, Itaú Unibanco Holding S.A. ( ITUB ) and Bradesco S.A. ( BBD ), the average over the last five years is quite similar even though Banco do Brasil's ROE is currently superior.

Itaú has historically has been more profitable than Banco do Brasil, mainly due to its focus on retail and corporate banking. Itaú's current ROE is 18.1%, averaging 16.7% since 2009. Bradesco, which operates similar to Itau, has its ROE standing at 11.9%, well below its major peers. But when looking at ROE historically, the average since 2009 is 16%.

{kind=link}

An Extremely Efficient State-Owned Bank

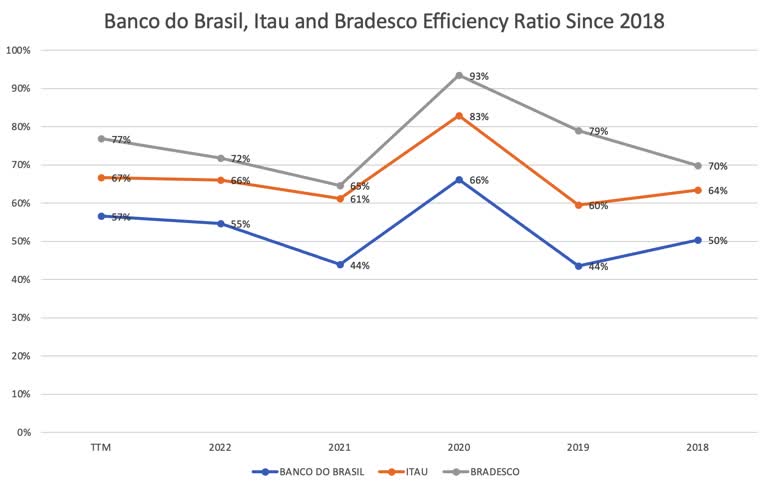

Another metric that caught my attention about Banco do Brasil is its low-efficiency ratio, which suggests that the bank is utilizing its resources effectively and has a better ability to generate profits.

In theory, state-owned banks are supposed to be less efficient than private banks, such as its main peers Itaú and Bradesco, due to bureaucracy, political interference, and sometimes lack of competition. However, Banco do Brasil has defied this expectation by exhibiting higher efficiency than its local peers.

By analyzing Banco do Brasil's efficiency ratio , which is 52.3% in the last twelve months. This efficiency metric is popular among bank stocks, indicating that for every $100 in revenue, the bank had $52.30 in expenses (in the last twelve months).

In comparison, Banco do Brasil's private peers, Itau and Bradesco, have 66.7% and 76.8% efficiency ratios, respectively. This trend has remained consistent for at least the last five years.

Compiled by Author using data from Seeking Alpha

{kind=link}

Banco do Brasil's Attractive Dividend Yield

The high ROE and efficiency metrics demonstrated by Banco do Brasil implies that the bank has efficiently used its equity to generate profits. With large profits, the company has the potential to distribute large portions of earnings as dividends, which ultimately reflects in the robust dividend yield that the bank has been showing for at least the past two years.

In 2022, for example, Banco do Brasil reported an annual dividend yield of 13.31%, representing more than 100% growth compared to 2021. Currently, the average yield stands at around 11%.

{kind=link}

This year, Banco do Brasil has released adjusted profit guidance of between R$33 billion and R$37 billion (US$6.69 billion and US$7.5 billion) for 2023.

Historically, the bank has had an average payout of 38% over the last ten years, currently at 34%. Based on this, according to my calculations, Banco do Brasil will distribute approximately U$2.66 billion in dividends in 2023, resulting in a projected dividend yield of almost 12%. The analyst consensus for 2024 suggests an even higher yield of 12.75%.

Within my bullish thesis regarding the bank's ability to continue with an attractive dividend yield, there are three primary reasons why Banco do Brasil's dividend yield should remain high.

- The first concerns its future earnings. For this year, Banco do Brasil has released adjusted earnings guidance of between R$33 billion and R$37 billion ($6.69 billion and $7.5 billion) for 2023.

- The second is related to its dividend payout ratio. Historically, the bank has had an average payout of 38% over the last ten years, currently at 34%. Based on this, according to my calculations, Banco do Brasil will distribute approximately $2.66 billion in dividends in 2023, resulting in a projected dividend yield of almost 12%. The analyst consensus for 2024 suggests an even higher yield of 12.75%.

- The third is related to changes in its stock price. If a company's stock price decreases, the dividend yield will increase, even if the value of the dividend remains the same. Banco do Brasil's stock has appreciated more than 46% this year alone. Although the company is trading at a forward non-GAAP price-to-earnings ratio of 3.62, well below its major domestic peers Itau and Bradesco, this lower valuation multiple can be explained due to material risks because the bank is half state-governed especially since Brazil is a country with considerable political risk.

Still extending the third point slightly, I want to pinpoint these political risks around Banco do Brasil governance.

Legislation in Brazil establishes governance guidelines for public and mixed-economy companies, including criteria for appointing directors, CEOs, and board members. Since late last year, there have been discussions about relaxing these rules, as the new Brazilian political and economic team elected this year tends toward more interventionist leanings. If it occurs, this should potentially impact public banks such as Banco do Brasil, as the new Brazilian political and economic team elected this year tends toward more interventionist leanings.

However, Banco do Brasil is listed at the highest level of corporate governance on the Brazilian stock exchange. This segment requires companies to issue only common shares with voting rights, regardless of the shareholder. Additionally, Banco do Brasil's board comprises half independent members and two representatives of minority shareholders

While these risks are significant and should not be ignored, Banco do Brasil faces lower governance risks than other state-owned companies in Brazil. For example, Petrobras ( PBR ), Brazil's leading oil company, also controlled by the government, holds a significant percentage of 73% of national oil and gasoline production. In contrast, Banco do Brasil has about 20% of the credit market in Brazil, with a different market share dynamic, reducing the risk of state interference.

Even so, the low valuation multiples of Banco do Brasil is consistent with reality considering these risks. In my view, this should be a deterrent for the shares of Banco do Brasil to remain in such a steep climb as has been repeated over the past year, limiting upside potential for Banco do Brasil shares in 2023. Therefore, there is less chance of the share price increasing and the dividend yield falling.

Participation In the Brazilian Agribusiness Loan Market

An additional reason that firmly supports my thesis that Banco do Brasil will continue to report very expressive profitability and thus continue to pay good dividends is based on its diversified credit portfolio, mainly due to its relevant participation in the Brazilian agribusiness and consigned credit. These two niches are desirable for financial institutions due to their meager delinquency rates.

Today, the bank's credit portfolio comprises about 30% agribusiness, a segment that grew 26% compared to last year and about 4.5% compared to the previous quarter, primarily responsible for the significant profit results in the latest earnings.

Banco do Brasil's Q1'23 Agribusiness Loan Portfolio (Banco do Brasil IR)

{kind=link}

According to the Brazilian Association of Banks ((ABBI)), Banco do Brasil has a market share of 63.1% in the Brazilian agribusiness loan market. It means that the bank provides loans to more than half of all agribusinesses in Brazil, followed by Itaú and Bradesco, which have 19% and 20% of this segment, respectively.

Banco do Brasil's strong presence in the agribusiness market is due to several factors, including its long history of providing financial services to this sector, its deep understanding of the needs of agribusinesses, and its wide range of products and services that are tailored to this sector.

The agribusiness sector represents 14% of the country's gross domestic product ((GDP)), and the whole agricultural chain accounts for 28%. Brazilian agribusiness closed 2022 with record exports of $159.1 billion, a growth of 32% compared to 2021, according to data from the Federal Government. The sector also generated the largest surplus ever recorded in history of Brazil, of $141.8 billion and is expected to register a CAGR of 5.93% during the forecast period until 2027.

Additionally, the agribusiness today is responsible for 47% of everything exported in Brazil. It can be seen that agribusiness in Brazil has been the engine of the economy, even in the difficult times experienced by the COVID-19 pandemic.

Therefore, I see Banco do Brasil's significant participation in this segment as key to maintaining the solid results of the loan portfolio, offsetting eventual slowdowns in individual and company loans.

Conclusion

I remain long on Banco do Brasil due to its current and future potential to distribute good dividends.

I believe that the bank should continue to report significant profits over the next few years, mainly by diversifying its loan portfolio to low-risk loans such as consigned loans and especially Brazilian agribusiness, where I see a huge future potential for Banco do Brasil considering its market share penetration in this segment.

However, although the bank's shares are traded at 3.62 times its forward price-to-earnings, I believe that its shares appreciation of more than 46% over this year leaves BDORY reasonably priced, considering the risks on account of half of the bank's corporate governance being owned by the state.

For further details see:

Banco do Brasil: Despite The Risks, Still A Solid High-Yield Stock