BDORY - Banco Do Brasil Q2 Earnings: Setting New Heights Amid Brazilian Notable Banks (Rating Upgrade)

2023-08-12 02:30:55 ET

Summary

- Banco do Brasil is demonstrated strong performance in the second quarter of 2023 with impressive net profit, robust expansion in its loan portfolio, and an above-average Return on Equity (ROE).

- Despite concerns about potential state intervention risks due to its governance structure, the bank's efficient operations led to a significant increase in stock price by over 60% year-to-date.

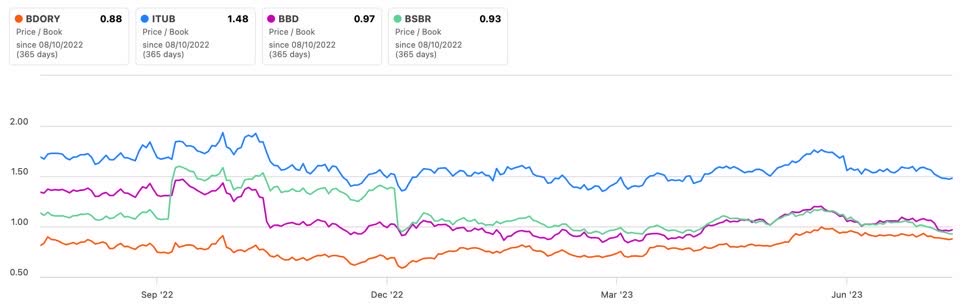

- Banco do Brasil stands out with a discounted valuation compared to its peers, reflected in its forward non-GAAP P/E ratio of 3.8x and price-to-book ratio of 0.88x.

- With a positive outlook for the third quarter, driven by an expected gradual improvement in Brazilian default rates, I am upgrading my previous "buy" position to a confident "strong buy."

Banco do Brasil ( OTCPK:BDORY ) presents compelling reasons for its shareholders to maintain confidence in their investment in Brazil's largest state-owned bank. In my previous article , I underscored my bullish stance on Banco do Brasil, primarily due to its impressive sustainability metrics, exemplified by its above-average Return on Equity ((ROE)) for a non-private bank.

The recently disclosed second-quarter results further underscore the bank's adept execution of its strategic plans, auguring well for an anticipated dividend yield that could exceed 10% for the year. These results effectively alleviate any concerns that Brazil's prevailing challenges, such as elevated delinquency rates and credit scarcity, might have significantly impacted the bank's second-quarter performance.

Although Banco do Brasil's governance structure entails notable state-related risks, the bank's valuation remains remarkably attractive. Furthermore, while these risks are presently distant, they have yet to materialize. As a result, my outlook on Banco do Brasil remains bullish, and I am buying more shares. Consequently, I am upgrading my stance from "buy" to "strong buy."

Q2 Financial Results Analysis

Banco do Brasil has unveiled its earnings for the second quarter of 2023, reaffirming its strength in the Brazilian financial landscape. The results strategically position Brazil's largest state-owned bank as a formidable player amidst the country's premier private banks.

Notably, the bank has reported an impressive net profit of R$8.354 billion, outperforming its counterparts in the Brazilian financial sector. Additionally, Banco do Brasil has showcased remarkable growth, solidifying its position with the most robust expansion in its loan portfolio. This accomplishment underscores the bank's resilience and pivotal role in shaping the Brazilian economy.

| Loan Portfolio (R$ bi) |

| Loan Portfolio Growth (YoY) |

| Gross Margins (R$ bi) |

| Delinquency Rate |

| Expanded ALL (R$ bi) |

| Coverage Ratio |

| ROE |

| CET1 |

| Basel |

| Banco do Brasil |

| 1045 |

| 13.6% |

| 17.0 |

| 2.7% |

| -2.9 |

| 201% |

| 20.8% |

| 12.2% |

| 14.1% |

| Itaú Unibanco |

| 1152 |

| 6.2% |

| 25.9 |

| 3% |

| -9.6 |

| 212% |

| 20.9% |

| 13.7% |

| 15.1% |

| Bradesco |

| 868.7 |

| 1.6% |

| 16.5 |

| 6.5% |

| -10.3 |

| 164% |

| 11.4% |

| 12.4% |

| 12.9% |

| Santander Brasil |

| 499.5 |

| 6.6% |

| 13.5 |

| 3.3% |

| -5.9 |

| 214% |

| 11.2% |

| 11.7% |

| 13.5% |

In the second quarter, Banco do Brasil achieved an impressive Return on Equity ((ROE)) of 21.3%, which marks an increase from the previous year's 20.8%. This positions Banco do Brasil among the world's most profitable banks, alongside its private domestic peer Itaú Unibanco ( ITUB ), which reported a ROE of 20.9%. In comparison, giant American banks renowned for their efficiency, such as JPMorgan ( JPM ) and Morgan Stanley ( MS ), achieved comparable ROE figures of 16% and 10%, respectively.

Banco do Brasil and Itaú have established a remarkable global presence underpinned by their stellar ROE. In Banco do Brasil's case, the significance of this achievement is threefold: the attained ROE level is exceptionally high, it surpasses domestic peers, and it upholds consistency with prior management strategies.

There is a positive trend regarding the efficiency ratio, a key metric indicating the relationship between expenses and revenues. The ratio improved, declining to 28% during the quarter. This decline indicates that while expenses have risen, revenue growth has outpaced these expenditures, contributing to heightened efficiency.

The discussion then turns to credit quality, specifically portfolio defaults. Banco do Brasil has effectively maintained a default rate below the national financial system average, showcasing adept credit management. Despite a rise in delinquencies to 2.73%, it's important to note that this rate remains below the average of the National Financial System ((SFN)) sector, which concluded at 3.6%. While this 2.73% represents the highest delinquency in 12 months, the prevailing trend suggests a continued decline in SFN delinquencies.

Banco do Brasil's credit portfolio is distinguished by its safety, primarily composed of agricultural and consigned credits with lower risk profiles. The quarter concluded with a substantial portfolio size of one trillion reais, reflecting an impressive growth rate of 13.6%. This portfolio diversification is a positive attribute for investors, contributing to a safer outlook relative to industry norms.

Moving to the coverage ratio, which gauges the bank's provisioning ability for defaults, Banco do Brasil has consistently maintained a robust ratio of provisions to defaults. This underscores the bank's conservative risk management stance. While a modest decline in this ratio is observable, it still surpasses the financial system average.

Furthermore, Banco do Brasil's leverage, represented by the Basel ratio, remains at 14.1%, closely aligned with the industry average. This suggests a potential adjustment in the pace of future loan portfolio growth.

Banco do Brasil has announced a dividend payment of 14 cents per share alongside 65% of Interest on Equity (IOE). Notably, the bank's history of increasing payouts at 53% above the 10-year average opens the possibility of an additional dividend payment.

BDORY's payout; net profit (green bars) and dividends (blue bars). (Status Invest)

{kind=link}

In conclusion, Banco do Brasil's Q2 2023 results demonstrate a positive trajectory consistent with prior management approaches. Despite certain areas warranting attention, such as the decline in leverage, the overall narrative reflects the bank's steadfast journey toward enhanced profitability and efficiency.

Valuations

Banco do Brasil trades at a significantly more discounted valuation than its peers. It boasts a forward non-GAAP P/E ratio of 3.8x, notably lower than its domestic counterparts: Itaú Unibanco, Bradesco ( BBD ), and Santander Brasil ( BSBR ), trading at 7.9x, 8.9x, and 9.6x, respectively.

When we turn our attention to the price-to-book ratio (P/B), a widely used metric in financial institutions due to its incorporation of factors like provisions for loan losses, Banco do Brasil's valuation becomes even more compelling. With a price-to-book ratio of 0.88x, it demonstrates a substantial discount compared to its peers. This discrepancy is particularly pronounced when considering the most efficient player in the field, Itaú Unibanco, which trades at a price-to-book ratio of 1.48x.

{kind=link}

Considering Banco do Brasil's high-quality metrics, the significantly lower valuation can be attributed to substantial risks arising from its status as a bank, with half of its shares owned by the Brazilian state. This is particularly relevant when considering Brazil's significant political risk.

Brazilian legislation delineates governance guidelines for public and mixed-economy companies, encompassing specific criteria for selecting directors, CEOs, and board members. As the previous year drew to a close, conversations arose concerning the prospective easing of these regulations.

This movement was propelled by the new direction of the Brazilian political and economic leadership, which leaned towards a more interventionist stance. If these modifications are implemented, their potential impact could extend to state-owned enterprises, including Banco do Brasil. This consideration is particularly relevant given the new leadership trajectory exemplified by the oil-giant Petrobras ( PBR ) case. Notably, Petrobras appointed a former politician as the company's new CEO earlier this year.

However, Banco do Brasil boasts the highest corporate governance listing on the Brazilian stock exchange. This category mandates companies to issue shares with voting rights exclusively, irrespective of the shareholder's position. Furthermore, Banco do Brasil's board includes an equal number of independent members and two representatives from minority shareholders.

A positive development is that since the appointment of Tarciana Paula Gomes Medeiros as the CEO of Banco do Brasil earlier this year, concerns regarding potential state intervention risks under the new management have not materialized. Investors' risk perception has been diminishing over the past two quarters. Consequently, confidence in Banco do Brasil's stocks has grown by over 60% by the beginning of August this year.

The bottom line

Banco do Brasil has unveiled robust Q2 results despite minor blemishes, effectively allaying any concern among shareholders arising from a more stringent credit landscape and elevated delinquency rates prevailing in Brazil.

The bank continues to uphold exceptional efficiency, outshining its domestic peers. The outlook for maintaining a double-digit dividend yield and retaining a stock price valuation at a noteworthy discount remains promising, despite political risks that have yet to manifest.

I am maintaining a positive outlook on the company's performance in the third quarter, anticipating a gradual improvement in delinquency rates in Brazil. Consequently, I am upgrading my previous recommendation from "buy" to "strong buy." Nonetheless, I am maintaining close monitoring of Banco do Brasil due to its status as a state-owned bank in Brazil.

For further details see:

Banco Do Brasil Q2 Earnings: Setting New Heights Amid Brazilian Notable Banks (Rating Upgrade)