BDORY - Banco do Brasil Q3 Earnings: Not Brilliant But Yet Solid

2023-11-20 18:33:00 ET

Summary

- Banco do Brasil's Q3 earnings, while not stellar, reflect solid performance with a 21.3% ROE, outperforming domestic peers.

- Mild concerns have surfaced due to the rise in delinquency rates and a decline in net profit growth for the quarter.

- The credit portfolio expanded, driven by individual, companies, and agricultural segments, showing strong year-over-year growth.

- Valuation multiples remain attractive, with a heavily discounted P/E of 3.7x for 2024E and a P/B below 1.

- Despite a likely growth slowdown in 2024, Banco do Brasil's focus on credit expansion and favorable interest rate trends in Brazil means a positive outlook.

In my previous article on Banco do Brasil ( BDORY ), I took an extremely optimistic stance on the Brazilian state-owned bank. This was grounded in its impressive sustainability metrics, as highlighted by its above-average Return on Equity ((ROE)) for a non-private bank. Furthermore, the bank currently maintains a discounted valuation, and there is the potential for substantial dividends to be distributed both this year and next.

In the third quarter, Banco do Brasil demonstrated a solid performance again, reporting a robust Return on Equity result consistently exceeding 20%, outperforming other domestic private competitors. However, notable concerns have arisen, particularly regarding the trajectory of default levels, warranting close monitoring, especially in the short term. Additionally, net profit holding steady in the quarter interrupted the growth trend.

Banco do Brasil's quarter faced negative impacts due to the necessity of making additional provisions for problematic credits associated with the retailer Americanas , resulting in a R$507 million increase in provision expenses for doubtful debts.

If not for the impact caused by the retailer, we believe that Banco do Brasil would have had the potential to achieve the highest profit among large banks, directly competing with Itaú for the top spot in this quarter.

Looking ahead, Banco do Brasil maintains its focus on expanding its credit portfolio, especially in the agribusiness segment, identified as the primary avenue for growth. With the prospect of a reduction in interest rates in Brazil (Selic) benefiting the bank in the short term, management anticipates growth in loans surpassing the securities portfolio over the next 6 to 18 months. This strategic move will likely allow net interest income to align with the loan portfolio by 2024, potentially resulting in profit growth.

Considering these factors, I maintain a positive outlook. However, recognizing the potential for a less enthusiastic quarter than the previous one and anticipating a growth deceleration in 2024, I am retaining a "buy" recommendation rather than the previous "strong buy" stance.

Banco do Brasil Q3 Earnings

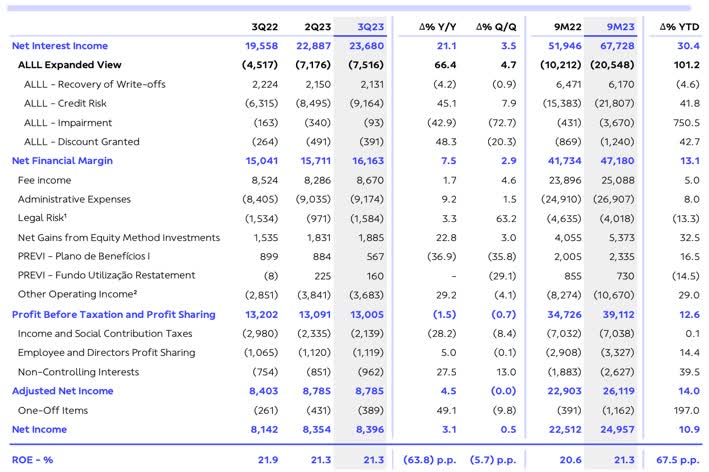

In the third quarter of 2023, Banco do Brasil recorded a profit of R$8.8 billion, interrupting the sequence of quarterly growth but still reflecting a 3.1% year-over-year increase. Nevertheless, the result remains solid, with a high Return on Equity of 21.3%, placing Banco do Brasil on a similar level to its peers, such as Itaú Unibanco ( ITUB ), and considerably ahead of Santander Brasil ( BSBR ) and Bradesco ( BBD ) in terms of profitability.

{kind=link}

However, the quarter was negatively affected by the need to make additional provisions for problem credits related to Americanas, increasing to R$507 million in bad debt provision expenses. Were it not for the impact caused by the retailer, Banco do Brasil could have had the potential to post the highest profit among the major banks, competing directly with Itaú for the title this quarter.

The credit portfolio reached R$946 billion in the quarter, showing a 2.6% increase quarter-over-quarter and a 9.8% increase year-over-year. This indicates a slowdown compared to the previous quarter but with expansion well above the other incumbents. The Individuals portfolio grew by 0.7% quarter-over-quarter (QoQ), Companies by 1.5% QoQ, and agro by 6.0% QoQ. Compared to the previous year, the Individuals portfolio grew by 7.8% annually, the Companies portfolio by 6.0% annually, and the agricultural portfolio by 17% annually.

{kind=link}

In 3Q23, Net Interest Income reached R$23.7 billion, up 3.5% quarter-over-quarter and 21.1% annually. Notably, a 5.0% quarterly growth in financial income was driven by an increased credit portfolio and securities. On the negative side, financial expenses grew by 6.5% QoQ due to the 8.5% QoQ increase in commercial funding.

{kind=link}

The Margin with Customers grew by 2.3% QoQ and 8.4% annually, driven by the expansion of the loan portfolio, an increase in the spread from 8.9% in 2Q23 to 9.0% this quarter, and a greater number of working days. The Margin with the Market grew 11.8% QoQ and 397.0% annually. The annual solid growth results from a higher average Selic rate, benefiting the remuneration of free securities and Banco Patagonia's net interest income.

Service revenues reached R$8.7 billion in 3Q23, representing an increase of 4.6% QoQ and only 1.7% annually. In the quarter, growth was positively driven by the insurance, pension, and capitalization lines raising 10.6% QoQ, fund administration up 5.7% QoQ, and consortiums up 8.6% QoQ. On the other hand, some segments negatively impacted the services line in the quarter, such as credit operations and guarantees, declining 3.3% QoQ; collections declining 7.9% QoQ; and subsidiaries/controlled companies -11.5% QoQ).

Up to September 2023, accumulated profit reached R$26.1 billion, in line with the middle of the guidance range of R$33 billion to R$37 billion of total profit in 2023. It expects to end the year with a profit of close to R$35 billion, of which R$9 billion is forecast for the last quarter.

Bad debt provision expenses totaled R$7.5 billion, raising 4.7% QoQ and 66.4% annually, negatively impacted by the additional provisioning of Americanas' toxic credits, resulting in R$507.4 million on PDD expenses for the period. In 2Q23, the same event had already affected credit risk by R$338.8 million.

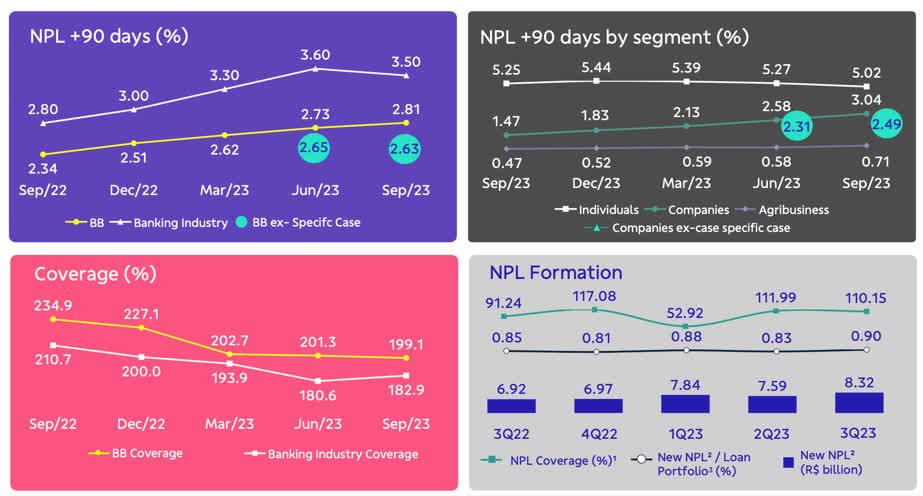

The delinquency rate above 90 days (NPL 90+) increased by 0.08 percentage points QoQ, reaching 2.81%, impacted mainly by the toxic credits of Americanas, which also worsened the indicator in 2Q23. Excluding the effect of the retailer, the NPL 90+ would have improved QoQ from 2.65% in 2Q23 to 2.63% in 3Q23. The bank pointed out that the balance of operations with the retailer is already 100% reflected in the delinquency indicator above 90 days, and all the necessary provisions have been made.

{kind=link}

In the quarter, the Banco do Brasil coverage ratio came in at 199.1% (-2.2pp QoQ), while the industry index increased by 2.3pp in the same period to 182%. In the annual comparison, the bank's coverage was consumed by 35.8pp.

Total administrative expenses reached R$14.0 billion, up 6.5% QoQ and 8.8% annually. The quarter was marked by growth in Other Administrative Expenses of 15.3% QoQ and 12.4% annually, partially offset by the decrease of 1.4% QoQ reduction in Personnel Expenses (raising 5.2% annually).

Lastly, the core capital improved by 0.28 percentage points to 12.5%, driven mainly by profit growth of 0.53 pp and the new capital regulations, which freed up another 0.60 pp. The Basel Index reached 16.2% (+0.5 percentage points QoQ and -0.5 percentage points annually), and the Tier I capital ratio reached 14.6% (+0.5 percentage points QoQ and -0.1 percentage points annually).

What to Expect for Q4 and 2024

The bank has reiterated its guidance for 2023, projecting recurring net income to fall within the range of R$33 billion to R$37 billion. I anticipate provisions to align with the upper end of the guidance spectrum, ranging between R$23 billion and R$27 billion. I expect this to be offset by financial margin growth on an annual basis, also positioned at the upper end of the range, fluctuating between 22% and 26%.

Looking ahead to 2024, I foresee sustained robust profitability, albeit with a deceleration in profit growth following the substantial increases of 11.4% year-over-year (YoY) in 2023 and 51% YoY in 2022. This is especially notable considering the growth of digital banks like Nu Holdings ( NU ), particularly in segments like consigned credit, where Banco do Brasil holds a significant market share.

My estimate points to a profit of over R$37 billion and a Return on Equity of around 20% in 2024, thanks to the increasing margins in retail credit as interest rates in Brazil continue to decline.

This slowdown is expected to be primarily influenced by slower growth in net interest income, aligning with a lower expansion rate in the loan portfolio. However, my assessment considers that provisions will remain the same compared to 2023, benefiting from lower defaults.

Dividends and Valuation

The valuation multiples at which Banco do Brasil is currently trading remain highly attractive, with just 3.7x price-to-earnings (P/E) for 2024E and 0.83x price-to-book (P/B) for 2023E. This represents a considerable discount compared to the key private domestic peers in the market, including Itaú Unibanco, Bradesco, and Santander Brasil.

{kind=link}

While Banco do Brasil faces a more significant discount due to its state risk, its recent performance has been far superior to most private peers and very similar to that of the most efficient private bank (Itaú). This becomes evident when we compare the operational metrics of the leading Brazilian banks.

| Loan Portfolio (R$ bi) |

| Loan Portfolio Growth (YoY) |

| Delinquency Rate |

| Expanded ALL (R$ bi) |

| Coverage Ratio |

| ROE |

| CET1 |

| Basel |

| Banco do Brasil |

| 1070 |

| 10% |

| 2.8% |

| -7.5 |

| 199% |

| 21.3% |

| 12.4% |

| 16.2% |

| Itaú Unibanco |

| 1163 |

| 4.7% |

| 3% |

| -9.3 |

| 209% |

| 21.1% |

| 14.6% |

| 16.3% |

| Bradesco |

| 877.5 |

| -0.6% |

| 5.6% |

| -9.1 |

| 182.5% |

| 11.4% |

| 13.4% |

| 12.9% |

| Santander Brasil |

| 502.6 |

| 0.7% |

| 3% |

| -5.6 |

| 230% |

| 13.1 % |

| 11.2% |

| 14.3% |

Given my belief that Banco do Brasil is poised to report a net profit at the high end of its annual guidance, potentially close to R$37 billion (approximately $7.2 billion, considering a net profit for 2023 of R$36 billion), and assuming a projected payout of 38%, this would translate to an annual dividend per share of $0.96, yielding over 9%. With a Return on Investment of 8%, I estimate a fair price for Banco do Brasil shares at $12 per share, representing a potential upside of 20%.

The Bottom Line

I believe Banco do Brasil's Q3 earnings left more to be desired than praised. The main negative highlights include the increase in defaults, albeit minimal, and the tepid quarter-on-quarter growth in net income. However, on the positive side, ROE remained robust and surpassed all its domestic peers, showcasing Banco do Brasil's excellent efficiency and mitigating concerns about state interference.

In addition, the valuation remains highly attractive, with a price-to-book value below one and the prospect of a dividend yield above 9%. Therefore, despite indications that net profit growth might slow down in 2024, I maintain a bullish outlook on Banco do Brasil, although I am updating my rating from "strong buy" to "buy."

For further details see:

Banco do Brasil Q3 Earnings: Not Brilliant, But Yet Solid