BDORY - Banco do Brasil: Solid Results Boost Optimism Among Investors Offering ~9% Yield

2023-10-27 08:30:00 ET

Summary

- Banco do Brasil is a strong and reliable financial institution with a significant presence in the Brazilian market.

- The bank's consistent financial performance and efficient risk management set it apart from its competitors.

- The positive economic environment in Brazil and the bank's commitment to innovation and digital transformation contribute to its potential for growth.

Investment Thesis

Investors looking to acquire a stake in a perennial sector with high potential for steady growth over the coming years should not overlook Banco do Brasil S.A. ( BDORY ). This financial institution, with a long history and a significant presence in the Brazilian market, stands as a cornerstone of the country's banking sector, thanks to its extensive network of branches and diverse financial services.

Especially in recent years, the bank has shown consistency, financial solidity, and efficient risk management. Its revenue-generating ability, high Dividend Yield with excellent control of its Payout, and resilience in managing default rates make the bank more appealing compared to peers like Itaú Unibanco ( ITUB ), Banco Bradesco S.A. ( BBD ), and Banco Santander (Brasil) S.A. ( BSBR ).

The expected positive economic environment in Brazil, started by the ongoing cut in the basic interest rate and a gradual economic recovery, can also favor Banco do Brasil. Contrary to the other Brazilian banks, which benefit from high interest rates, Banco do Brasil has some protection to the downside, due to the bank being the main player in charge of the country's agribusiness loan portfolio, Brazil's most important sector, which would benefit from a low-rate environment.

It's also worth noting that, despite the recent decrease in the central bank rates (the Selic), yields on Brazilian bonds have increased, but I believe it's just a matter of time before they start following the Selic rate.

Also, the ongoing pursuit of innovation and commitment to digital transformation also contributes to my current buy stance, because the adaptation to new technological trends will strengthen its competitive position in the market.

A Little Bit About Banco do Brasil

Banco do Brasil S.A. was established in 1808 at the request of Prince D. João, recently arrived from Portugal on Brazilian soil. As the first banking institution to operate in the country, BB was founded when only three issuer banks were active globally - in England, France, and Sweden.

Today, the bank offers a variety of products and services to individuals and corporations, also catering to the public sector. Banco do Brasil's operational segments include banking, investments, asset management, insurance, pensions, savings bonds, consortiums, and payment methods.

Beyond its brand, the Banco do Brasil conglomerate consists of subsidiary companies, affiliates, joint ventures, managed entities, sponsored entities, and foundations. BB Seguros and BB Tecnologia e Serviços are among the controlled companies. Brasilprev, Brasilcap, Cielo, Alelo, Elo, and Cateno are examples of affiliates and joint ventures. BB Previdência, Previ, and Fundação BB fall under managed, sponsored, and foundation categories.

According to the financial institution's 2021 annual report, Banco do Brasil has a presence in 96.8% of Brazilian municipalities, with 56,082 service points that include its own, shared, and correspondent networks.

Additionally, the company has an international network comprised of 21 branches located in 13 countries. In addition to its own structure, 668 banks act as correspondents in 94 countries, catering to the needs of clients residing abroad and other international demands.

Valuation

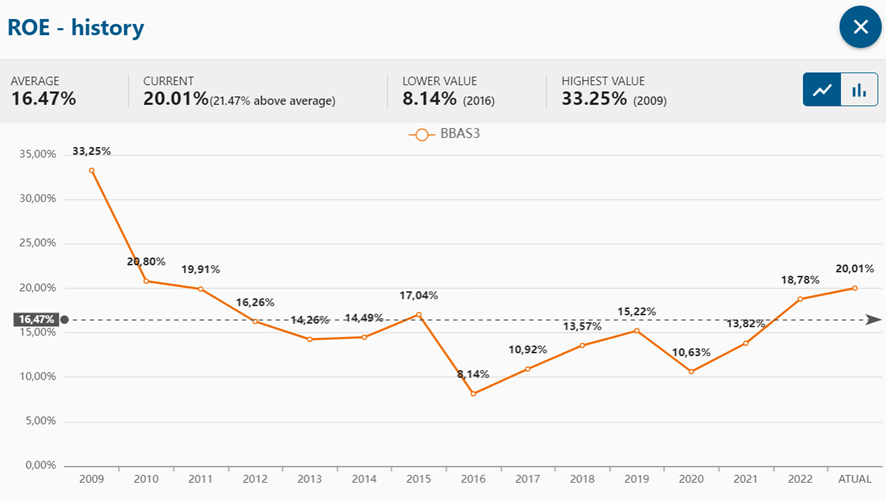

The bank has been demonstrating effective management work, significantly increasing its margins. Its ROE has exceeded its historical average of 16.47%, reaching 21.3% in recent results, a figure not seen for over 13 years.

Undoubtedly, this shows how the bank's reinvestments and technological transformations have yielded good long-term returns, even amidst crises. Currently, the bank boasts the highest ROE among its peers this quarter.

{kind=link}

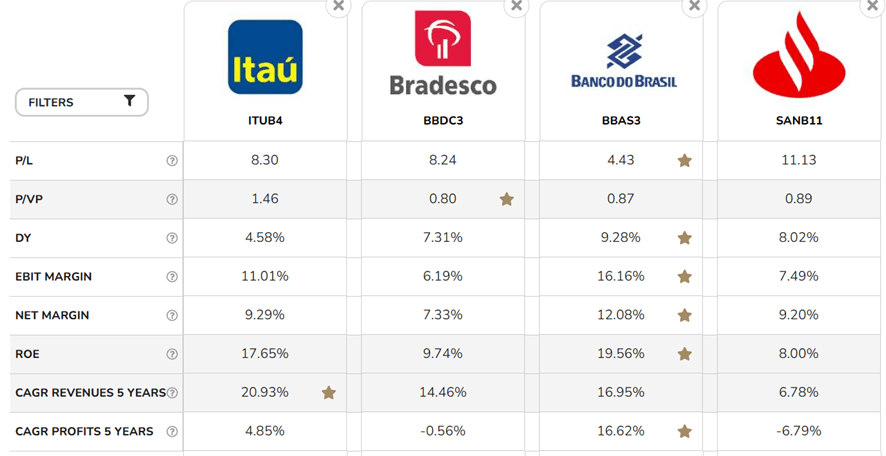

Despite the significant appreciation that Banco do Brasil shares have experienced, it still carries a P/Book of 0.87x, meaning that, theoretically, investors would be buying at a moment cheaper than the bank's shareholder equity.

In my opinion, relatively, you would be paying less for Banco do Brasil now as you would for Santander, with a P/Book of 11.13x, and for Bradesco, with a P/Book of 0.80x. However, it's undeniable that both are underperforming significantly compared to Banco do Brasil.

P/L = P/E; P/VP = P/Book (Investidor10)

{kind=link}

I find it unusual that the P/E ratio remains so low at about 4.43x, almost half when compared to its biggest private-sector competitor, Itaú, which has a P/E of 8.30x and has been achieving results as good as Banco do Brasil, which is state-owned. This could indicate 2 aspects:

- Investors' apprehension about possible government influence;

- Or that there is much expectation for significant volatility anytime soon.

It's worth noting that Banco do Brasil's dividend yield has decreased compared to the 10.4% from last year, but it remains the highest among its peers at 9.28%. It's also interesting that the bank generally doesn't have a high payout ratio (currently 45%) when looking at Bradesco and Santander during certain periods, which, in my view, demonstrates resilience and good resource management, likely due to recent reinvestments in the company itself.

This efficient resource management enabled a huge increase in its EBIT margin and net margin by 16.16% and 12.08% respectively, accompanied by revenue and profit CAGR growing by 16.95% and 16.62%. It's noteworthy how, in this quarter, Banco do Brasil achieved its best historical efficiency ratio of 28.3% when relating its service provision to administrative and operational expenses.

Banco do Brasil vs. Banco Bradesco and Why BB is the Best Option Now

Considering the current global macroeconomic scenario, I see several key points that will continue to influence the assets that make up the IFNC, an index that encompasses companies in the financial sector on the Brazilian stock exchange. Initially, the pace of interest rate adjustments in the United States still depends on economic data, which may suggest further increases if economic activity remains at high levels.

These new adjustments could affect, for example, the BRL/USD exchange rate, as higher interest rates in the United States tend to attract capital, impacting resource allocation in Brazil. This dynamic is related to the difference in interest rates between the USA and Brazil. While the USA is maintaining or raising its rates, Brazil entered an interest rate reduction cycle, dropping its benchmark rate from 13.75% in August this year to 12.75% as I write this article, in contrast to increasing rates in the North American market.

As mentioned in the first section of this analysis, a low-interest rate scenario also benefits Banco do Brasil, as opposed to other banks. This makes Banco do Brasil much more hedged against the ups and downs of the economy, which, in my view, is a terrific trait itself, an even better for a bank.

Domestically, I'm sure the Brazilian Central Bank is closely monitoring U.S. and global economic indicators to guide its next actions. As a result, there is a risk of negative impacts for banks if interest rates in Brazil do not fall or fall without credibility, which could indicate that the Central Bank is cutting rates recklessly, representing an additional risk for the Brazilian economy.

This might explain the current upward movement in the rates of Brazilian bonds since July. But, in my opinion, it's just a matter of time before they get pulled back down.

Additionally, there are positive qualitative indicators regarding inflation in Brazil, as demonstrated by September's IPCA (Brazilian CPI), projecting inflation slightly above the target of 5% for this year. This supports the continuation of adjustments in Brazilian interest rates, even in the face of a challenging global scenario.

It's also important to note the challenges related to balancing public accounts, which pose a hurdle for the current government, with real risks to the monetary adjustment cycle, especially if the set targets are not met. In summary, the risks that can affect the banking sector, focusing on Banco do Brasil and Bradesco, include interest rates higher than those expected by the Central Bank and the market, which can impact the revenues of these institutions. These revenues are affected by the capital lent by banks, used to shield their loan portfolios and for equity operations.

In Bradesco's case, the challenge related to this revenue stream is tied to the fact that the bank does not hedge its credit portfolio, which mainly consists of pre-set rates with an average duration of 18 months. This makes the bank sensitive to changes in the economic cycle and interest rates. Bradesco serves clients with lower incomes and smaller companies.

On the other hand, Banco do Brasil has a more diversified credit portfolio in terms of rates and is less sensitive to economic cycles due to the use of active hedging. Its average revenues per quarter in this area exceed BRL 1 billion in profits. The bank primarily serves the agricultural sector and public employees.

Bradesco operates with a riskier credit portfolio, concentrated on lower-income clients, both individuals and businesses, making it more sensitive to economic cycles. During periods of monetary tightening, defaults increase, impacting this revenue source. However, the riskier client profile also allows the bank to achieve higher profits since it demands higher interest rates.

In Banco do Brasil's case, the profile is more conservative, focusing on public employees and INSS (Brazilian Social Security Service) beneficiaries in the individual segment, and on businesses linked to agribusiness in the corporate segment. These credit lines have a lower risk compared to Bradesco, but the risk premium is more closely tied to political interference than to clients' credit ratings.

In summary, I truly believe Banco do Brasil appears more attractive than Bradesco, based on fundamental metrics. I can also extend this opinion to the other Brazilian banks as well, as stated previously in this article. Bradesco will need to make structural adjustments to regain its historical profitability, evidenced by an average ROE of 18%. During the third quarter of the 2023 earnings season, it will be important to monitor the evolution of default rates, credit coverage, and margins with clients and the market.

Furthermore, in the context of the banking sector as a whole, it's crucial to follow developments related to the end of interest on equity payments (JCP: Juros Sobre Capital Próprio) and the limit on revolving credit card loans, as these factors can directly affect the earnings of Brazilian banks.

The Main Risks

In my mind, the biggest risks are certainly the political ones, as Banco do Brasil is a state-owned enterprise and is heavily subject to changes arising from political decisions that may come into force.

Investor Relations

Due to Banco do Brasil's close ties with the Brazilian government, it's possible that the bank's pursuits may not always be best suited for minority shareholders. Changes in legislation or regulation of the financial sector, as well as alterations and increases in taxation, would directly impact the bank's profits and business model.

The current president and his party have repeatedly expressed their discontent and repudiation towards the private sector and agribusiness, which primarily make up the largest part of Banco do Brasil's credit portfolio. I believe, without a doubt, that the current government's motivation to reduce incentives for financing the private and agribusiness sectors could have significant impacts on the bank's portfolio, leading to substantial declines in the short and medium term.

The emergence of competitors, especially fintechs, as well as increased aggressiveness in the offerings of current competitors, can affect the bank's results. However, I don't see this risk as more concentrated in the long term, especially if the bank emphasizes diversifying the portfolio in technology areas, mitigating risks of system failures and hacks in its applications, as well as greater interactivity with its customers.

Despite its state-owned nature and still being very old-fashioned internally, Banco do Brasil isn't too far behind its competitors in terms of technology. However, it falls short in many aspects. For instance, its talent-seeking procedure is still performed through public exams, which limits the search for top-quality professionals that could be broader when conducted online.

Banco do Brasil recently formed a partnership with the Mila company to integrate artificial intelligence into its platforms and services. Until the end of last year, the bank lacked innovations in the mobile app, such as fingerprint and facial recognition, which have now been integrated into the bank's data management .

As a customer of the bank myself, I mainly use the Android app and have noticed other issues. For example, the investment platform isn't integrated into the main app, unlike banks like Bradesco and Inter.

The lack of accessibility and the outdated layouts make it complicated for elderly users and put off younger customers who prefer a more "gamified" experience. Delays in the transaction history for purchases and bill payments have been reported by myself and others, with complaints written on the Play Store page.

Now, what concludes my viewpoint that Banco do Brasil's technological area is still quite lagging is that, in recent months, according to the Central Bank, Nubank surpassed Banco do Brasil's position, becoming the 4th largest bank in the country in terms of customers.

Final Words

Banco do Brasil stands out as a promising choice for investors, backed by its solid financial performance and commitment to sustainable development. The leadership of the bank's first female president, Tarciana Medeiros, brings a new inclusive and diversified perspective, strengthening the institution's reputation in the face of strong ideological ideals that are more present than ever in our society.

The emphasis on supporting small- and medium-sized rural producers, as well as the robust performance of the credit portfolio, are positive aspects. However, investors need to be aware of the political risks associated with the bank's state-owned nature, as well as possible regulatory changes in the financial sector.

Despite this, I currently find it the best company in the Brazilian banking sector to buy, showing significant growth potential, indicated by favorable metrics such as P/Book and P/E. With a history of successful reinvestments and technological transformations, Banco do Brasil maintains a prominent position in the market, offering solid returns to investors looking to add it to their portfolio.

For further details see:

Banco do Brasil: Solid Results Boost Optimism Among Investors, Offering ~9% Yield