ITUB - Banco Itaú Chile: Quality Bank But Not Good Enough

2023-09-25 07:58:09 ET

Summary

- Banco Itaú Chile is one of the largest Chilean banks with operations in Chile and Colombia. Its largest shareholder is the Brazilian banking conglomerate Itaú Unibanco.

- Banco Itaú Chile had a strong last quarter, pays generous dividends, and owns a high-quality loan portfolio.

- Banco Itaú Chile is the cheapest among its competitors measured by price to book. Its parent company is valued at a P/B multiple of 1.43, while Banco Itaú Chile is at 0.49.

- However, lagging digital transformation, an inefficient Colombian segment, and insufficient capital adequacy are enough to give Banco Itaú Chile a hold rating.

Thesis

Banco Itaú Chile (ITCL) is one of the largest Chilean banks with operations in Chile and Colombia. ITCL is a result of a merger in 2025 between Banco Itaú Chile and CorpBanca. Its largest shareholder is the Brazilian banking conglomerate Itaú Unibanco (ITUB), which owns 66.7% of its shares.

ITCL had a strong last quarter, pays generous dividends, and owns a high-quality loan portfolio. However, lagging digital transformation, an inefficient Colombian segment, and insufficient capital adequacy are enough to give ITCL a hold rating.

Company Overview

ITCL has seven segments, which are as follows: Leasing, factoring, and other financial services for business customers are provided by large, corporate, and real estate companies. Traditional and private banking, which offers checking accounts, consumer loans, credit cards, and mortgage loans, is provided by lower-income retail banking, like Banco Condell's operations, and includes consumer loans, credit cards, and mortgage loans.

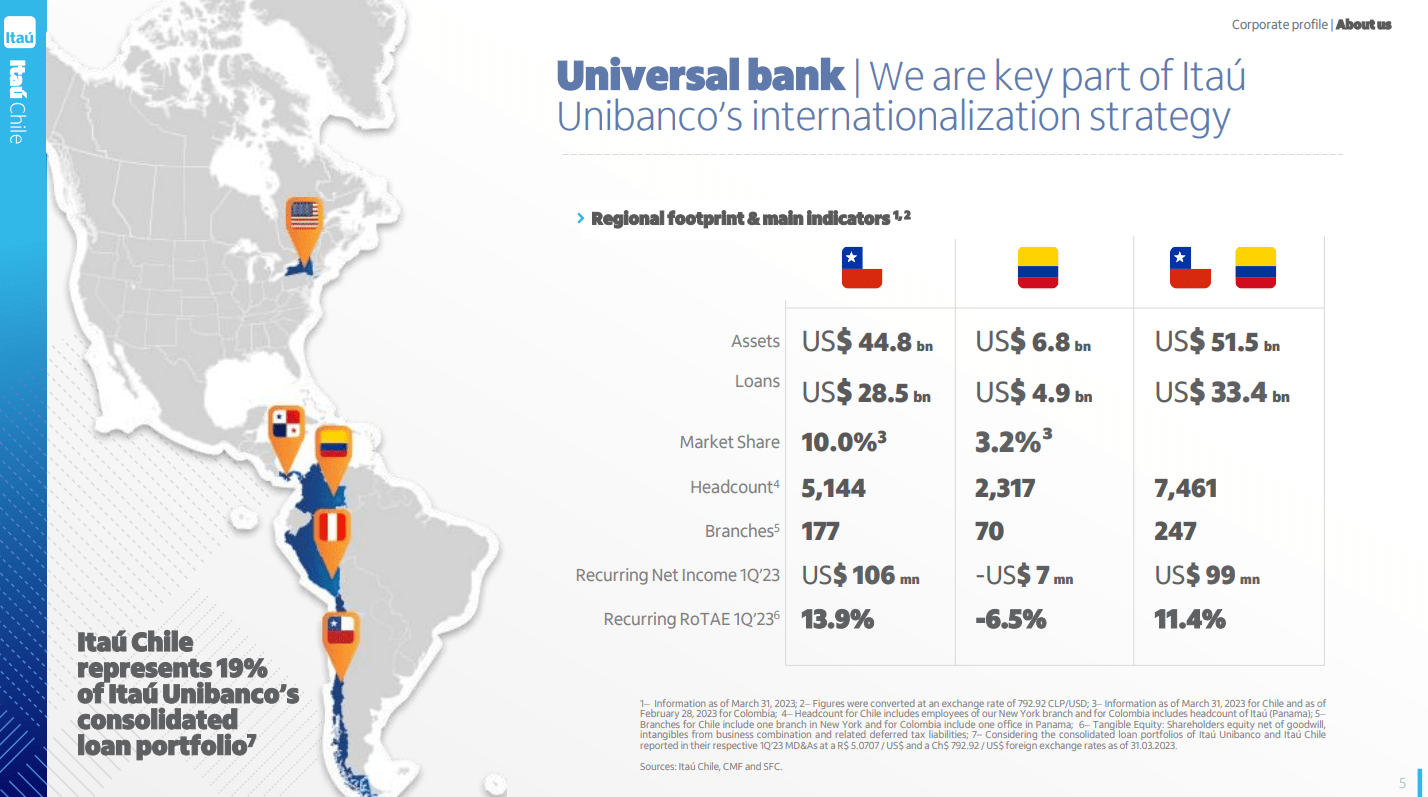

ITCL has branches in Colombia and Chile. The image below from the last corporate presentation shows its operations.

{kind=link}

Chilean assets represent 87% of the total, while the loans are 85%. Itaú Chile's market share is 10%, with an adequate RoTE of 13.9%. The Colombian segment has been a drag with (6.5)% RoTE while holding a 3.2% market share.

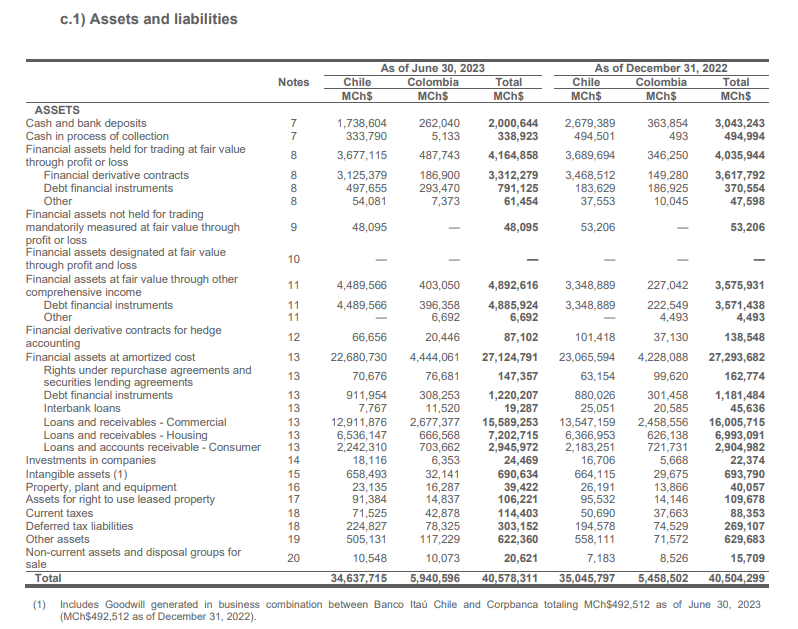

Let's go into more detail and compare Chilean and Colombian operations. Colombian assets are 14% of the total. However, revenue is 14.7% and is a mere 2.8%. The two tables below from the Q2 2023 financial report show the company's geographic asset distribution and income statement by country.

{kind=link}

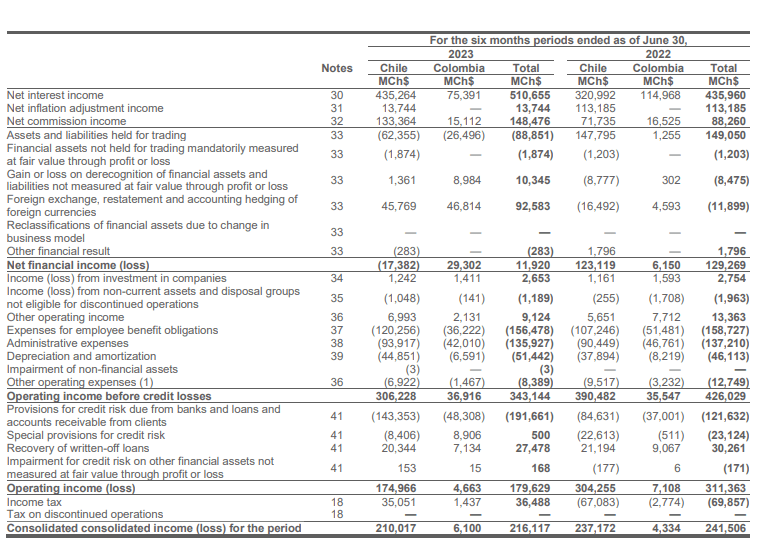

The Colombian segment has more significant exposure to commercial loans and a higher cash-to-assets ratio than the Chilean segment. However, the loans as a whole have stalled. Colombian commercial loans have soared by 8.5% and mortgages 6.3%, respectively.

{kind=link}

The income structure is very similar between both segments. The net commission income to interest income ratio is 18% for Chile and 20% for Colombia. Colombia segment has significantly higher provisions for credit risk as a percentage of revenue, thus affecting the segments' bottom line.

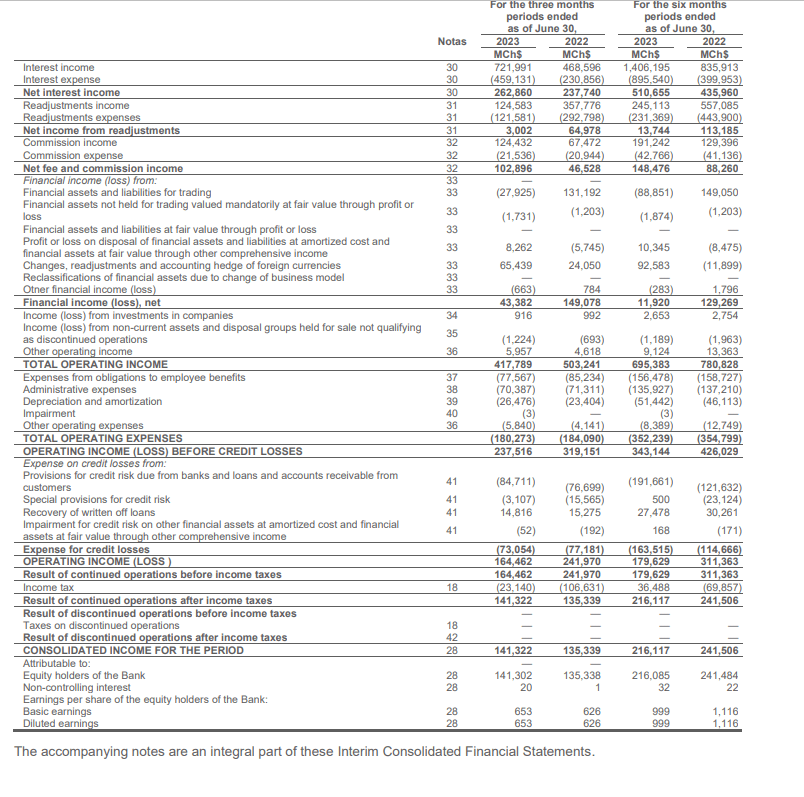

A few things are worth mentioning when considering ITCL's consolidated income statement. First is the net income growth for the last three months. While [[BSAC]] and [[BCH]] have realized declining net earnings, ITCL had a strong quarter. The image below is the ITCL Q2 consolidated income statement.

{kind=link}

ITCL has realized substantial growth in net commission income quarter over quarter at 110%. At the same time, net interest income soared by a respectable 56%. Given such impressive results, the company's bottom line is up by 4.4%. Negligible at first glance, however, much better than BSAC and BCH, who realized declining results.

Company Financials

ITCL's balance sheet is not the exception for Chilean banks. The bank funds its operations with interbank borrowings, client deposits, and bond issuance. The table below represents some metrics I use to measure banks' balance sheet quality. The data is from the Q2 financial report .

| Asset ratios: assets structure |

| Cash/Total Assets |

| 5.7% |

| Loans (total)/Total Assets |

| 59% |

| Consumer loans/Total Assets |

| 7.1% |

| Mortgage Loans /Total Assets |

| 17.0% |

| Commercial Loans/ Total Assets |

| 38% |

| Bonds/Total Assets |

| 20% |

| Liability ratios: capital structure |

| Deposits/ Total Liabilities |

| 47% |

| Interbank borrowings/ Total Liabilities |

| 10% |

| Company bonds/ Total Liabilities |

| 36% |

| Other financial instruments/Total Liabilities |

| 3.4% |

| Equity/ Total Liabilities + Equity |

| 8.8% |

| Solvency ratios: |

| Loans /Deposits |

| 149% |

| Cash/Deposits |

| 11% |

| Borrowings (inc. bonds)/ Total Assets |

| 29% |

ITCL's balance sheet metrics mirror those of BSAC and BCH with a loan-to-deposit ratio higher than 100%, solid cash-to-deposit ratio, and higher borrowing-to-total assets ratio.

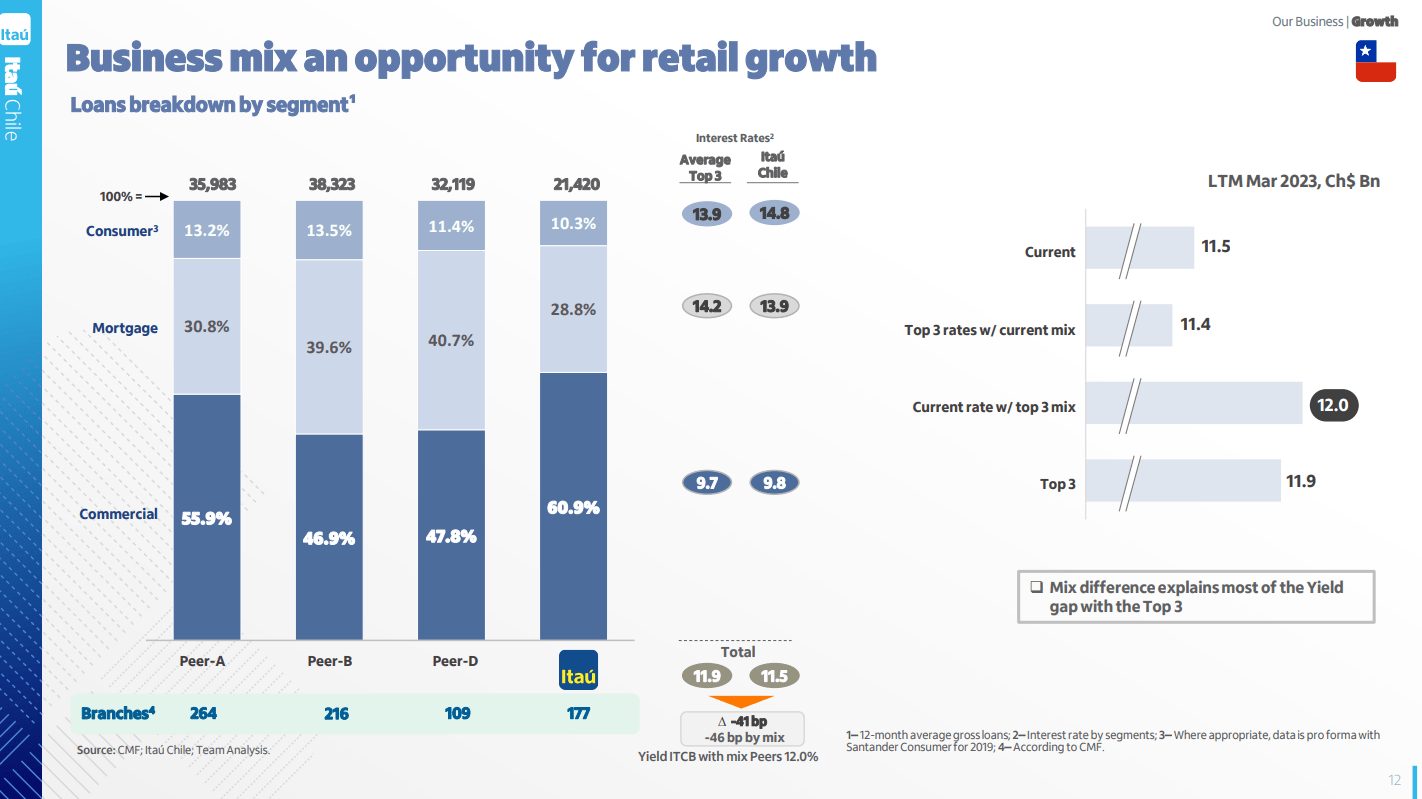

Let’s dig deeper into the details of loan and deposit composition. The chart below represents the bank's loan structure compared to its Chilean peers.

{kind=link}

ITCL, among its competitors, has the highest percentage of its loan portfolio in commercial loans. This is a direct bet on economic growth. Given the declining inflation and the Chilean Central Bank's consistent rate cuts, the businesses will have stimulus to take loans. Lower rates squeeze profit margins, attracting more enterprises to borrow more. Thus, the bank's interest income composition will change. More companies will borrow at lower rates instead of fewer at higher rates. The bank's bottom line might remain the same, but lending to a growing number of enterprises mitigates the bank`s credit risk. On the other hand, the lower rates improve borrowers’ liquidity due to declining expenses to serve debt obligations.

In the previous chapter, I mentioned the Colombian segment and its notably higher provisions as a percentage of its revenue. Non-performing loans ((NPL)) have increased notably in the last quarters, as shown in the graph below.

{kind=link}

Chilean average NPL is 2.0%, and Colombian average NPL is 4.6%. The image above represents Colombian segment performance. NPL is at the bottom left. For one quarter, it moved by more than 20% from 2.43% to 2.95%, though these figures are still much lower than the Colombian average.

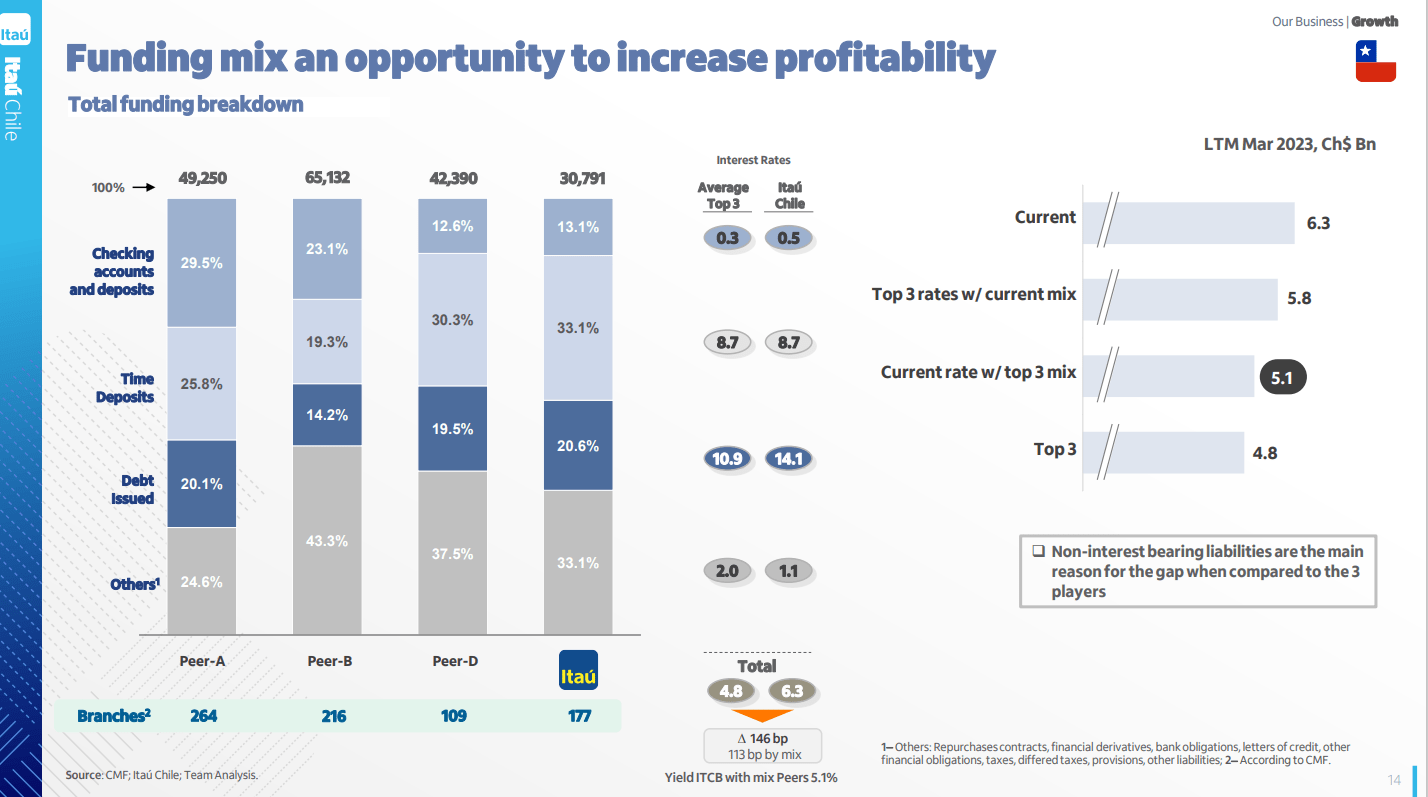

We have the bank's liabilities on the right side of the balance sheet. The image below shows the banks' funding composition compared to its Chilean peers.

{kind=link}

ITCL has the highest percentage of time deposits of total liabilities and second lowest checking accounts and deposits. However, time deposits bear higher interest rates and are not as liquid as checking accounts. A higher percentage of time deposits mitigates banks' liquidity risk and compresses net income margins. It's a fair trade-off, sacrificing profitability for an improved risk profile.

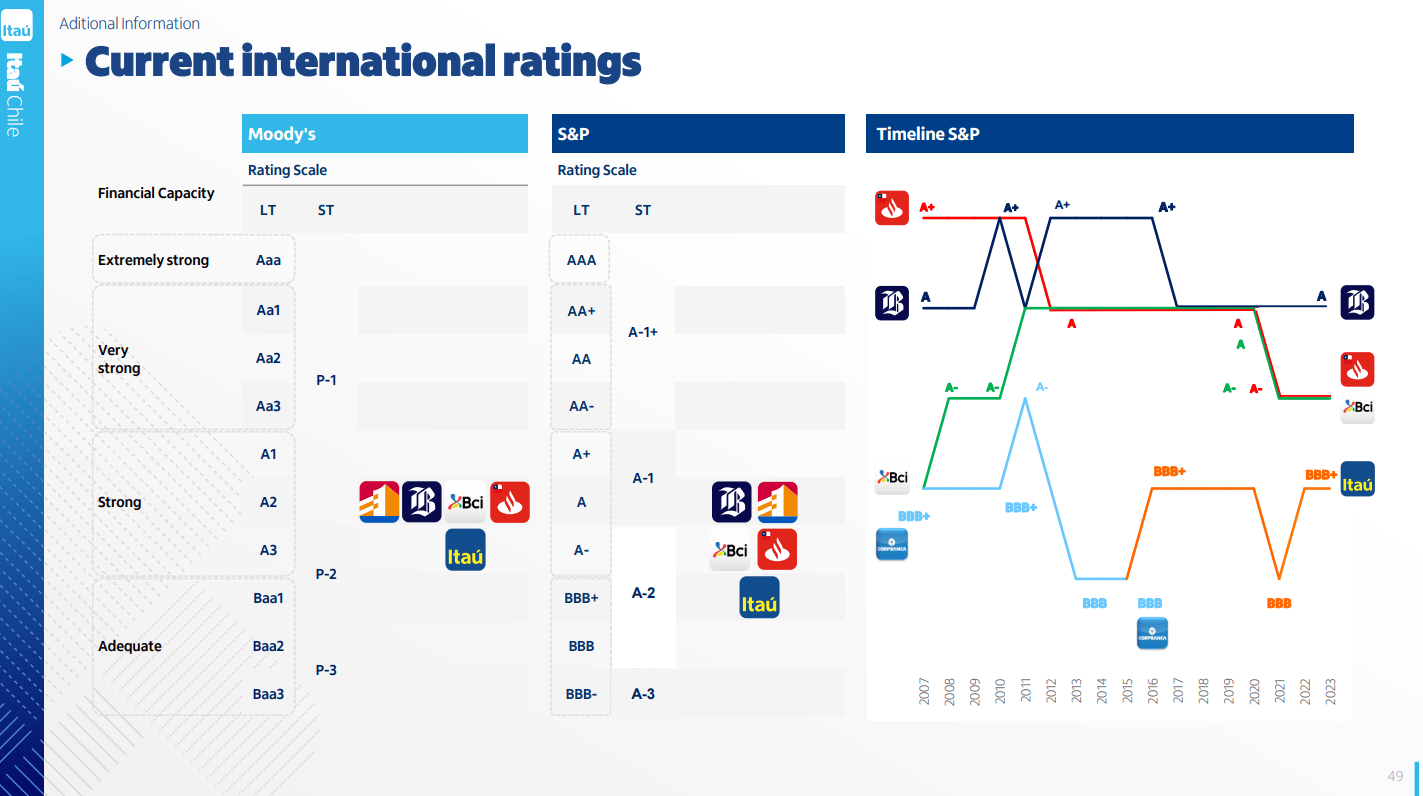

As I mentioned, ITCL funds its operation with the issuance of bonds. The image below shows the banks' credit ratings compared with other Chilean banks.

{kind=link}

ITCL lags behind its competitors despite its bonds being categorized as investment grade. The top performers are BCH and BSAC. On the other hand, Itaú's rating soared last quarter while BCH and BSAC dropped.

Last but not least, we have to check ITCL Basel III metrics. The table below shows banks' solvency and liquidity. The data is taken from the last company financial report .

| Capital (in millions of Chilean peso): |

| Regulatory Capital |

| 4,091,738 |

| Tier 1 capital |

| 2,960,738 |

| Common equity tier 1 ((CET1)) |

| 2,826,565 |

| Risk-Weighted Assets |

| 26,807,237 |

| Basel III Ratios: |

| Regulatory capital ratio (Capital adequacy ratio) |

| 15.2% |

| Tier 1 ratio |

| 11.0% |

| CET1 ratio |

| 9.4% |

| LCR |

| 234 % |

| NSFR |

| 112 % |

ITCL risk metrics are average but below BSAC and BCH. Most disappointing is the CET1 ratio, which is below 10%. BCH, for reference, is 12.7%, and BSAC is 10.5%. Lower CET1 drags all capital metrics down. However, ITCL liquidity numbers are more than adequate.

Despite the last quarter's strong performance, ITCL's profitability is average. The table below compares ITCL, BCH, and BSAC profitability metrics TTM.

| ITCL |

| BCH |

| BSAC |

| ROE |

| 12.33% |

| 25.6% |

| 13.7% |

| RoTE |

| 20.4% |

| 26.1% |

| 13.8% |

| RoCET 1 |

| 21.0% |

| 22.4% |

| 16.9% |

| ROA |

| 1.3% |

| 2.2% |

| 0.75% |

Banco De Chile is the top performer, while ITCL is second and BSAC third. The discrepancy in improving earnings and lagging return on capital is due to an insufficient Colombian segment. It holds 14% of banks' consolidated assets and equity but contributes only to 2.8% of net earnings.

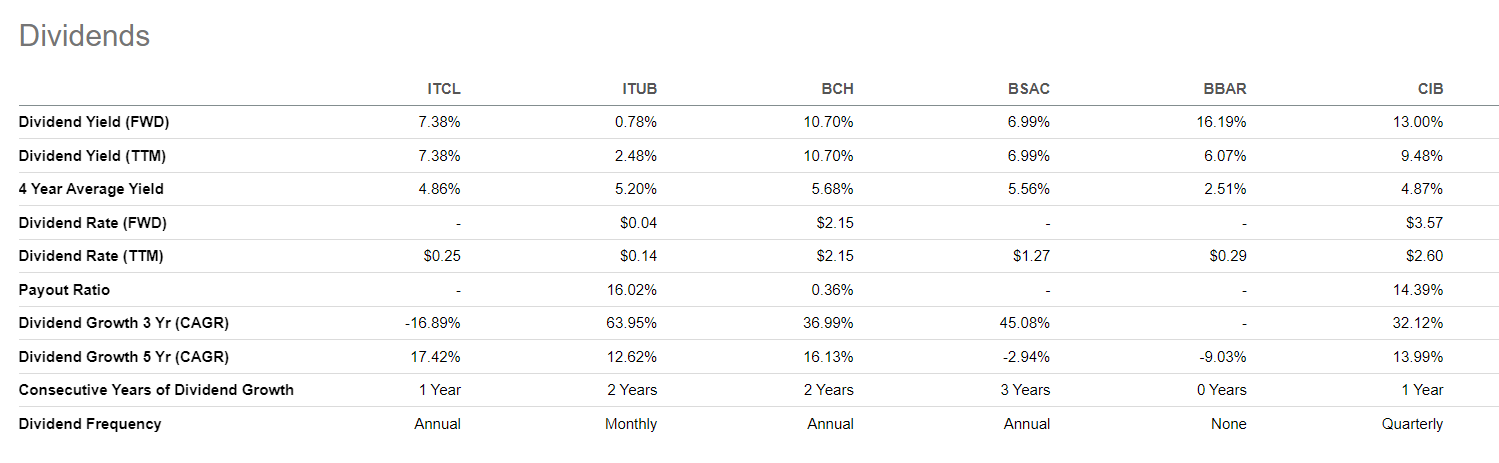

ITCL pays generous dividends, but lower than its competitors, except its [aren’t company ITUB.

{kind=link}

Company Valuation

To calculate ITCL value with the Dividend Discount Model, I have to measure the price of the company's equity and levered beta.

To obtain those numbers, I use the following steps and assumptions:

- Risk-free rate equals the 5Y average of USA long-term Government bond Rate, 2.2%.

- Growth rate, g, equals the 5Y average of the USA long-term Government bond Rate, 2.2%.

- Weighted equity risk premium is 6.52 %. Thus, ITCL revenues originate from Colombia and Chile. I have to calculate the combined equity risk premium based on a percentage of income the country generates.

ITCL weighted equity risk premium

- ITCL's dividend pre-share of $ 0.25

- ITCL unlevered Beta 0.83

- ITCL Debt/Equity ratio 466%

- Chile's effective tax rate 27 %

-

- Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E).

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for the leveraged beta. The formula I use is:

Cost of Equity = Risk-Free Rate + (Levered Beta * Equity Risk Premium).

3. Calculate the Terminal Value of dividends considering the Cost of Equity and Expected dividend growth:

Terminal Value = Dividend per share * (1 + expected dividend growth) / (Cost of Equity – Expected Dividend Growth)

4. Calculate the Present Value of Terminal Value assuming a constant discount rate for ten years.

For ITCL, I get the following results:

Intrinsic value per share = $ 2.39

Current Market price = $ 3.36 on Sept 22, 2023

To estimate BCH`s relative value, I choose the following South American banks:

- Banco de Chile ( BCH )

- Itaú Unibanco Brazil ( ITUB )

- Banco Santander-Chile ( BSAC )

- Banco BBVA Argentina ( BBAR )

- Bancolombia ( CIB )

{kind=link}

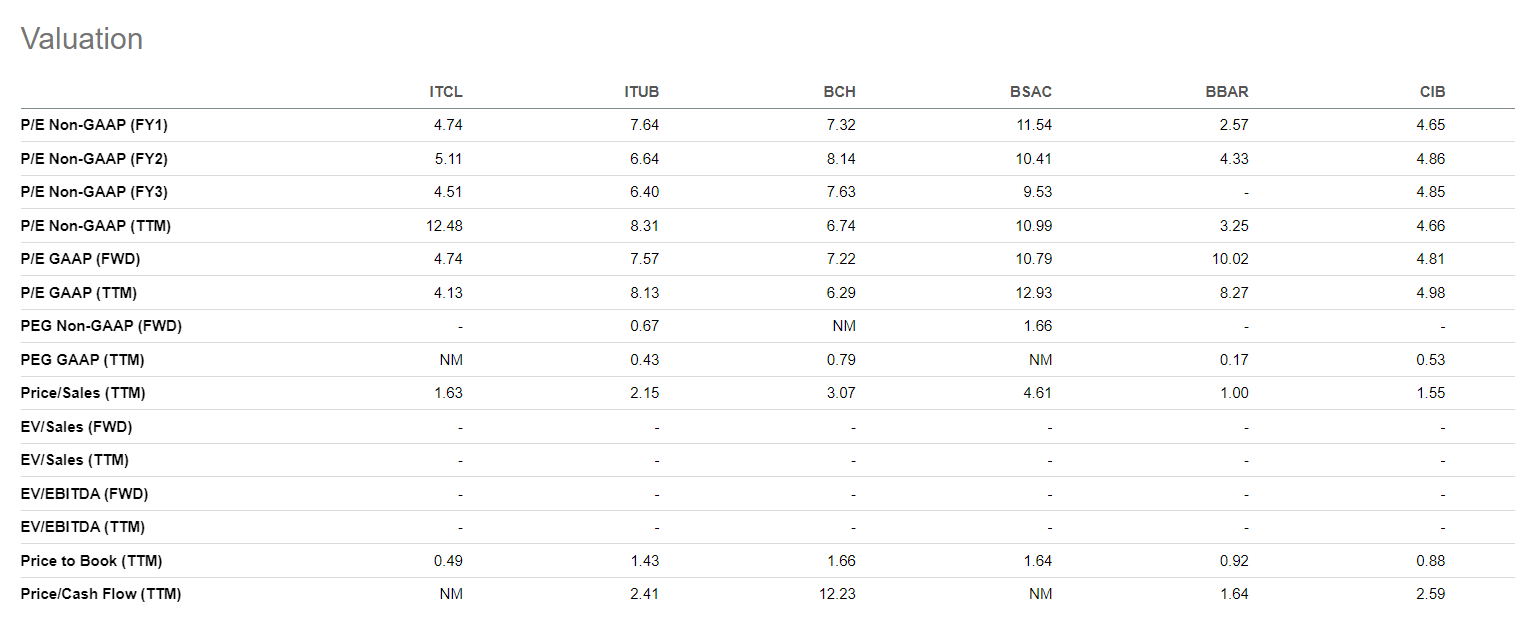

ITCL is the cheapest among the groups measured by price to book. Its parent company, ITUB, is valued at a P/B multiple of 1.43, while ITCL is at 0.49. The largest Colombian bank, Bancolombia, is priced at 0.88 P/B.

Risks

ITCL carries the usual risks: liquidity, credit, operation, and market risk. The bank's balance sheet composition is adequate, given its cash-to-deposit ratio and LCR and NSFR ratios. On the other hand, ITCL's solvency metrics are mediocre compared to BSAC and BCH. Despite being higher than Basel III guidelines, the CET1 ratio below 10% is a red flag for me. Banks' credit risk is well distributed but more dependent on economic growth due to its higher exposure to commercial loans.

Banks' operation risk is worth special mention. Colombian segment performance is more than insufficient. It holds 14% of company assets while generating one digit of net income. I attribute that to banks' operations. ITCL's Colombian segment is too small to compete with leading banks such as Bancolombia. Holding a 3.2% share of the market dominated by a few prominent players puts ITCL in the corner, dependent not only on the Colombian economy and politics but also on fierce competition.

In my humble opinion, divesting its Colombian assets will improve banks' efficiency. Thus, ITCL will focus on the Chilean market, especially digital transformation. Digital banking is the big challenge all traditional banks face, and ITCL significantly underperforms. Its banking app holds 49 th place from 50 among Chile's most popular digital banking apps.

Conclusion

Of all three Chilean banks available for trading on the NYSE, ITCL is last in line measured in balance sheet quality, profitability, and digital transformation. The dividends, with a yield of 7.89% and growing profitability, are not enough to give ITCL a buy rating.

On the other hand, I like ITCL's higher exposure to commercial loans and its last solid quarter, unlike BSAC and BCH's disappointing results. With declining interest rates, enterprises will be tempted to borrow more, creating more credit demand. ITCL is well-positioned to benefit from that. Due to those positives, I will give ITCL a hold rating, expecting to improve its Colombian operations and enhance its capital structure.

For further details see:

Banco Itaú Chile: Quality Bank, But Not Good Enough