BSBR - Banco Santander (Brasil): Recovery Mode But Overvaluation Persists

2023-10-06 06:48:16 ET

Summary

- Santander Brasil's recent focus on loan defaults and credit availability has influenced the broader Brazilian banking sector.

- While the bank has shown some improvements in its financial results, challenges remain, and its higher valuation compared to peers raises caution among investors.

- Regulatory changes and an uncertain economic environment make some hesitant about buying Santander Brasil shares despite a recent drop in stock price.

Over the past few quarters, the investment thesis for Banco Santander Brasil ( BSBR ) has predominantly centered around concerns related to loan defaults and credit availability, which have significantly influenced the broader Brazilian banking sector. Specifically, regarding Santander Brasil, it's worth noting that loan arrears have continued to rise, although at a decelerated pace, throughout the second quarter of 2023.

However, major Brazilian banking institutions, including Santander Brasil, have exercised caution regarding lending and adjusted their projections for portfolio growth this year.

In my previous article concerning Santander Brasil, I emphasized that the earnings for the first quarter revealed a weaker performance than other central national banks. This has further eroded confidence in the possibility of dividends returning to levels seen last year or even before the pandemic.

Itaú Unibanco ( ITUB ) and Banco do Brasil ( BDORY ) have outperformed their peers, thanks to their strong profitability, despite facing slower portfolio growth and narrower financial margins. On the other hand, Bradesco ( BBD ) and Santander Brasil have shown a slight improvement in their return on equity ((ROE)) indicators. However, they still fall short of the profitability levels observed a year ago. This suggests that a short-term recovery may be unlikely.

Furthermore, when we compare Santander Brasil to its domestic counterparts, the bank is trading at a premium that, in my opinion, is not justified given its current challenges.

Has Delinquency Reached Its Peak?

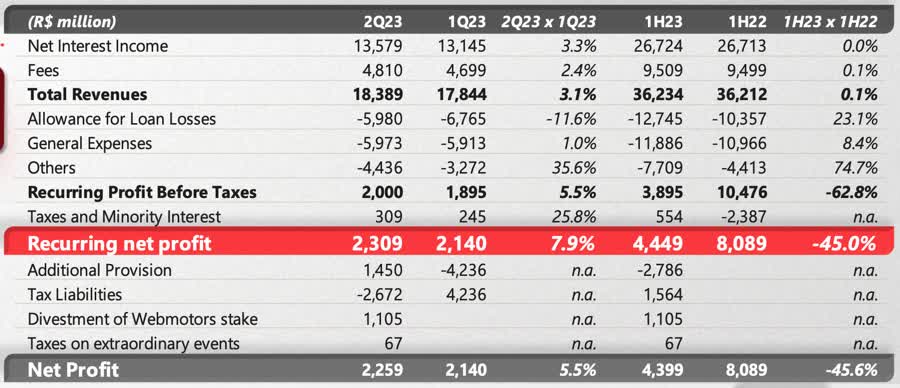

Santander reported a recurring net income of R$2.309 billion in the second quarter, 45% lower than in 2022. The ROE (Return on Equity) of 11.24% represented a decrease of 961 basis points compared to the same period last year.

The bank's gross financial margin, reflecting earnings from interest-bearing operations, amounted to R$13.579 billion, showing a 6.3% increase over the past year.

{kind=link}

Santander Brasil's executives expressed confidence regarding the delinquency of the bank's credit portfolio. During the earnings call on the second-quarter results, Mario Leão, the bank's CEO, stated:

"We're comfortable saying that the peak of default generation has passed."

The bank did report a marginal increase in the portfolio of non-performing loans over 90 days old, rising from 3.2% in March to 3.3% by the end of June. This increase was anticipated, but investors were keen to know if defaults had peaked. While the macroeconomic scenario could impact this, there is hope for improvement based on factors such as a reduction in interest rates, decreasing household indebtedness, and debt renegotiation programs.

Santander Brasil's IR

Santander Brasil emphasized its focus on loans with guarantees, including payroll loans, real estate financing, and rural credit. The bank aims to grow in areas where it has accepted declines without taking excessive risks.

Santander Brasil aims to maximize profitability within its customer base, particularly in the high-income and corporate segments. The bank intends to shift its portfolio profile to be less exposed to low-income and unbanked customers.

During the most recent earnings call, company executives expressed their desire to return the bank's ROE to levels seen in the past, between 15% and 20%. However, they acknowledged that achieving this target will take several quarters.

While Santander Brasil has made positive progress in some metrics, there is still a considerable journey ahead. Overall, despite some pressure from higher provisions and assistance from favorable income tax, the combination of a healthy balance sheet and improved net interest income signals positive prospects for better results in the future.

Historical Payout and Dividends

Banco Santander Brasil, which is controlled by the Spanish Banco Santander S.A. ( SAN ), is committed to returning dividends to its controlling shareholder. Consequently, the bank has historically maintained a payout ratio ranging from around 40% to 50%, and this trend is expected to continue into the second half of 2023.

Payout (orange line), net profit (green line), and dividends (blue line). (Status Invest)

{kind=link}

However, it is reasonable to anticipate a more modest dividend yield due to lower profits. Therefore, expecting a dividend yield between 3.6% and 4% for 2023 might be a prudent estimate. Although risk perception is improving, and Santander Brasil may move towards higher future profits, it remains relatively high, particularly considering interest rates and potential downside spread risks. These factors should encourage caution in the bank's approach.

Looking ahead to 2024, the improved profit and profitability trend may lead Santander Brazil to consider increasing its payout to compensate for lost time. The consensus is bullish, estimating growth rates of 7.5% for 2024 and 8.2% for 2025.

{kind=link}

It's worth noting that the CEO of Santander Brasil emphasized that he does not foresee a substantial change in how the bank remunerates its shareholders.

Risk #1: The Potential Elimination of Interest on Shareholders' Equity (JCP)

The recent comments by Brazil's Finance Ministry about the possible extinction of interest on shareholders equity (JCP) have been indigestible for the banking sector.

This practice, specific to the Brazilian tax system and corporate finance, revolves around companies paying interest to their shareholders on the equity invested in the company, carrying distinct tax implications in Brazil. Unlike dividends, JCP is accounted for as an "expense" for companies, reducing taxable net income. At Santander, on average, JCPs represented 57.3% of income distributions over the last five years.

Santander Brasil said that there is a need for the government to understand that the financial industry is different from others because banks need to have a high capital base to be solid and make loans.

According to the bank's CEO, a standalone decision to eliminate JCP without a corresponding reduction in income tax and CSLL (Social Contribution on Net Profit) rates would be unfavorable. Such a decision could further burden the financial industry and potentially harm consumers, leading to more expensive credit for Brazilians.

One of the probable ways out for Santander Brasil in this situation would be to pay dividends less frequently and supplement remuneration with buybacks and bonuses.

Risk #2: Credit Card Revolving Payment Legislation

The Brazilian Chamber of Deputies has approved an expedited procedure for the bill that limits the interest rates charged on credit cards. This means that the matter will bypass the House committees and proceed to be voted on in the upcoming plenary sessions.

The individuals most impacted by this decision would be those with the highest credit risk. From the banking perspective, setting limits for this segment could render new operations unviable and reduce existing ones due to the risk-return ratio. Santander Brasil, Bradesco, and Nubank ( NU ) would be among the primary entities affected, primarily because of the larger proportion of revolving credit cards in their operations and greater exposure to higher credit risk segments, which naturally carry the highest interest rates.

Revolving credit is offered when a consumer fails to pay the full credit card bill by the due date. The unpaid balance is then carried over to the next month's bill, along with interest, and added to the amount initially scheduled for that installment.

After a month of revolving credit, financial institutions must provide an alternative credit line with more favorable terms to encourage repayment and prevent over-indebtedness. The installment plan for the revolving credit amount is one of the options generally made available.

This development is unfavorable for banks, particularly those with the highest exposure to revolving credit card products, which often come with the highest interest rates. Currently, the average annual interest rate stands at approximately 440%. Consequently, if the proposed 100% interest rate limit is approved, it could significantly curtail the availability of credit cards in the sector.

The Bottom Line

In conclusion, I maintain a pessimistic outlook for Banco Santander Brasil, expecting it to continue facing challenges and weaker results in 2023. Meanwhile, peers such as Itaú and Banco do Brasil have performed significantly better and offered more attractive pricing.

However, Bradesco remains an outlier in this context. It has been heavily impacted by high recurring provisions stemming from the " Lojas Americanas " effects, referring to one of the major Brazilian retailers that faced bankruptcy in an accounting scandal.

| Loan Portfolio (R$ bi) |

| Loan Portfolio Growth (YoY) |

| Gross Margins (R$ bi) |

| Delinquency Rate |

| Expanded ALL (R$ bi) |

| Coverage Ratio |

| ROE |

| CET1 |

| Basel |

| Santander Brasil |

| 499.5 |

| 6.6% |

| 13.5 |

| 3.3% |

| -5.98 |

| 214% |

| 11.2% |

| 11.7% |

| 13.5% |

| Itaú Unibanco |

| 1152 |

| 6.2% |

| 25.9 |

| 3% |

| -9.6 |

| 212% |

| 20.93% |

| 13.7% |

| 15.1% |

| Banco do Brasil |

| 1032 |

| 16.80% |

| 21.1 |

| 2.62% |

| -5.8 |

| 202% |

| 21% |

| 16.70% |

| Bradesco |

| 868.7 |

| 1.6% |

| 16.5 |

| 6.5% |

| -10.3 |

| 164% |

| 11.4% |

| 12.4% |

| 12.9% |

Significantly, when considering valuation multiples, excluding Banco do Brasil due to its status as a state-owned bank, Santander Brasil is trading at a premium compared to its two primary private competitors. Its forward Price-to-Earnings (P/E) ratio currently stands at 9x, in contrast to Itaú Unibanco's 7.5x and Bradesco's 8x. Moreover, the consensus projection indicates that Santander Brasil's multiple is expected to remain in the range of 6x to 5x from 2024 onwards.

Regarding the Price-to-Book (P/B) ratio, Santander Brasil positions itself above its other private peers. I find few plausible reasons for Santander Brasil to trade at a higher multiple than Itaú. This is especially notable considering investors generally have tremendous confidence in Itaú's assets, particularly its substantial and more sophisticated customer base. It is expected to lead to higher value generation and trade at an ROE almost double that of Santander Brasil and Bradesco.

While I'm inclined to consider a sell rating for Santander Brasil's shares, the recent 20% drop since the end of June leaves less room for a more bearish stance. The trend for Q3 and the second half of 2023 suggests a potential recovery for the Brazilian banking sector, with expectations that the worst defaults may be behind us.

However, I remain neutral about buying Santander Brasil. This skepticism stems from its higher valuation than its peers, lack of a clear competitive advantage, and the lack of significant catalysts for substantial stock appreciation in the short to medium term.

For further details see:

Banco Santander (Brasil): Recovery Mode, But Overvaluation Persists