BSBR - Banco Santander (Brasil) Stock: Lackluster Performance Not Warranting A Buy

2023-06-22 09:36:08 ET

Summary

- Santander Brasil's latest results show weak performance and lower confidence in dividends returning to previous levels.

- The bank faces challenges in efficiency, legal security risks, increased provisions for doubtful debts, and competition from digital banks and fintechs.

- Santander Brasil's valuation is considered unattractive compared to its main peers, with better options available in the Brazilian banking industry.

Banco Santander (Brasil) ( BSBR ) is Brazil's third largest private bank today, behind only Itaú ( ITUB ) and Bradesco ( BBD ). The bank stands out for its activities focused on retail and wholesale operations, covering a broad portfolio of products and services with sufficient structure in all regions of Brazil.

I initiated a long position in Santander Brasil a few years ago, considering its leading position among Brazilian national banks and good dividend distribution capacity.

However, the macroeconomic scenario's significant impact on Santander Brasil's revenue generation in the last five quarters has caused the bank's stock to decline over 45% in the previous three years, trailing behind its main domestic peers.

The latest quarterly results showing a weak performance against other central national banks have reiterated lower confidence in dividends returning to levels similar to last year or even the pre-pandemic period.

For this and other reasons, including a valuation that needs to be more attractive, I continue with a neutral stance on the bank despite not getting rid of my long positions in Santander Brasil.

Santander Brasil's latest results

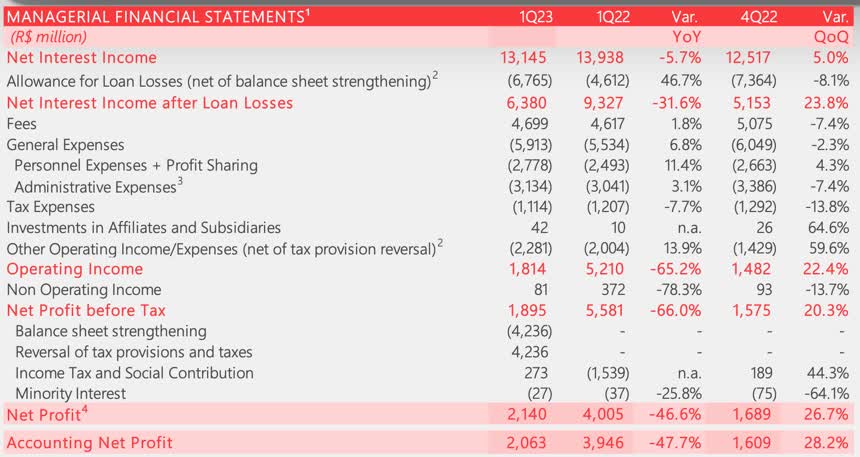

Santander Brasil just came out of a tough quarter. The Brazilian bank reported a significant drop in its net profit of about 47% to R$2.14 billion in the first quarter of this year compared to Q122. However, the figure exceeded the Refinitiv consensus forecast of R$1.83 billion.

Santander Brasil's Investor Relations

{kind=link}

The Brazilian bank has been impacted for the fifth consecutive quarter by credit selectivity and a negative sensitivity to Brazil's interest rate, which has remained at 13.75% since October last year.

This year's most recent results comprising the first quarter showed a gross financial margin totalling R$ 13.1 billion, which implied a 5.7% drop compared to the same period in 2022. The indicator's performance could have improved due to lower results with the market margin due to the pressure of the increase in interest rates in the period.

The quarter's revenues from banking services and fees totalled R$ 4.7 billion, advancing only 1.8% year-on-year. The slight improvement in the result was due to higher payments from credit and current account operations. Revenues from credit cards totalled R$1.3 billion, advancing 1.7% compared with the same quarter last year. This slight increase also benefited from greater transnationality in the period, boosted by the recurrent use of services.

General expenses rose 6.8% to R$5.9 billion. Personnel expenses also grew 11.4% year-on-year, impacted by the collective bargaining agreement on the salary base that the company had at the end of last year - the result of the liquidation of credit.

The positive side was Santander's credit portfolio which showed a growth of 9.9% in comparison, closing the period with a value of half a trillion reais. Large companies and individuals grew by 18.8% and 8.4%, respectively.

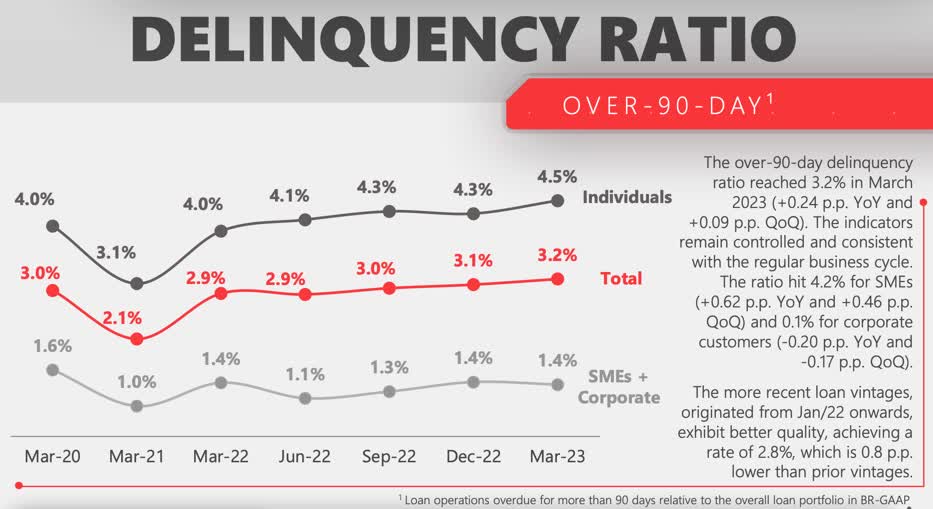

As for asset quality, the 90-day delinquency ratio was 3.2%, registering a temporary increase of 0.1 p.p. compared to the previous quarter, showing some stability. This shows that the NPL appears to be under control.

Santander Brasil's Investor Relations

{kind=link}

The Basel ratio recorded in the fourth quarter was 13.8%, down from the 13.9% reported during the last quarter and 2.8 percentage points above the minimum regulatory value required by the Central Bank.

Santander Brasil grew its active customer base by 3% YoY and tied customers with six or more products by 3% YoY to 8.6 million customers. The bank has also been intensifying its digital efforts as in the most recent quarter, transactions in digital channels advanced 4%, totalling 97% of the bank's total transactions.

Finally, the bank currently has an NPS (Net Promoter Score) of individual clients at 53 points, well below fintech such as Nubank ( NU ), which has an incredible 87 points. As a cost-cutting policy, the bank reduced its customer service branches to 1,687 in the last quarter, closing 100 units compared to the previous year.

Not expecting a dividend increase

The buy thesis on Santander Brasil, based on its capacity to distribute rich dividends, continues, in my opinion, to be the main one regarding the Brazilian bank. Santander Brasil has an average payout of 58% of its profits over the last ten years and usually pays dividends four to five times yearly.

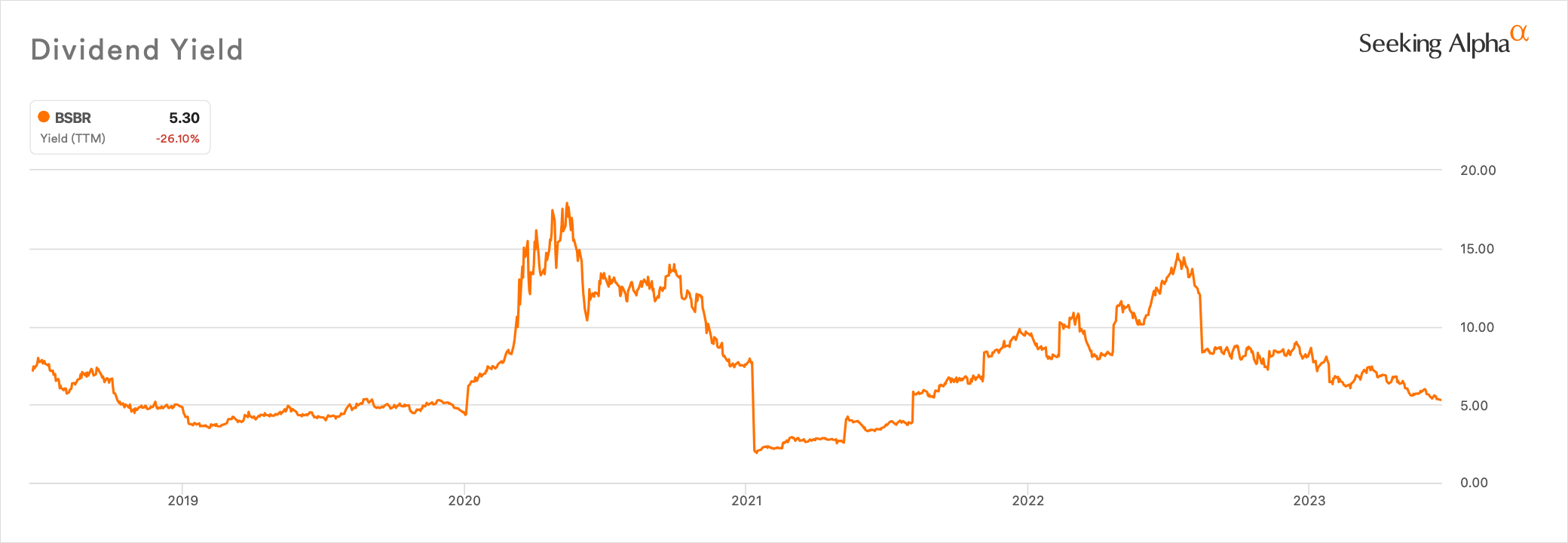

For 2023, the bank has a yield of 5.3%, remaining at an average of 6.57% throughout the first quarter of this year. This yield, however, is well below last year's average, when Santander Brasil distributed a 9.68% dividend yield to its shareholders, or the incredible 11.43% in 2020 at the height of the pandemic - which then dropped to below 2% in 2021.

{kind=link}

With net income almost halving in the first quarter of this year, the bank has significantly reduced the projection for a robust dividend this year. As shown below, Santander Brasil's share price has been following the decline in net income, but in recent months in a less correlated way. When the share price rises, the percentage represented by the value of the dividend concerning the price is lower. Therefore the dividend yield tends to decrease.

Critical concerns in the investment thesis

Some points evidenced in Santander Brasil's latest results denote attention due to the bank's management execution and the macroeconomic scenario. Thus, I predict some factors should continue to pressure Santander Brasil's shares in the medium term.

- Efficiency ratio: Until the pre-pandemic period in 2018, Santander had an efficiency of 35% in a period of more robust revenues in a more favourable macro scenario for credit in Brazil. Now back to 40%, expectations for revenue expansion in Brazil do not appear to be very positive in the country, considering the high-interest rate and higher risk of default. On a year-on-year comparison, the last quarter showed a 4.8% increase in the efficiency ratio, evidencing a significant deterioration in a short period.

Santander Brasil's Investors Relation

- Tax reversals and legal security risks: Santander Brasil is involved in a legal security risk issue in Brazil according to the material fact released on June 12 regarding the taxation of the PIS/CONFIS tax - a federal tax such as the sale of products, rendering of services, and import of goods, among others. The plenary of the Supreme Court has formed a majority to allow the incidence of PIS and Cofins on financial revenues of financial institutions as interest and charge a retroactive period referring from 1998 to 2014. Santander Brasil could come out as one of the big losers of this story, and it could impact R$4.5 billion before taxes, of which R$2.2 billion refers directly to Santander Brasil about the collection of the PIS. In comparison, the remaining R$2.3 billion relates to the affiliated companies that belong to Santander Brasil. So far, the risk prognosis classifies as a possible loss, not necessarily probable. But anyway, there was a more specific positive outcome of R$4.5 billion with the reversal of tax provisions, accounted in "other operating income". Santander allocated this reversal to provisions, resulting in a total amount of R$6.8 billion in the bank's most recent quarter, below the formation of new NPLs, theoretically indicating a negative impact.

- Increase in Provision for Doubtful Debts ((PDD)): Santander increased PDD expenses by 43.88% compared to the first quarter of 2022. The rise in PDD indicates a conservative posture of the bank regarding risk management and protection against possible losses. However, it has also been affecting the bank's profitability as provisions represent a reduction in profit or equity. The 12-month cost of credit has also risen from 3% to 4.7% year-on-year.

- Insider selling: Another alert regarding Santander Brasil is due to the systematic sale of shares by the company's executives over July of last year, as the bank has been reporting a decrease in its net income in the third quarter of 2022. Interestingly, insiders started selling Santander Brasil shares after the bank announced a share buyback plan in August 2022, which would not make sense to sell. The timing of the sales, however, could have been the right one. Santander Brasil shares have risen about 8% since the sales began.

- Digital banks and fintech: Digital banks like Nubank and Inter ( INTR ) have quickly taken a large percentage of Brazil's share and advanced swiftly concerning credit card growth. Nubank, for example, has a Net Promoter Score (NPS) of 87, about 35% above Santander's score.

Additionally, Santander's cost to serve full digital clients reached R$18.7, while Nubank's monthly average cost to serve per active customer at year-end was R$3.80.

Valuations, far from a bargain

I believe Santander Brasil's current valuation is expensive for what the bank has been delivering compared to its main peers.

Considering the projection that the bank should decrease its EPS by the end of the year by 15.5%, still, the consensus is that the bank should reach a forward price-to-earnings ratio of 10.79. Something around 20% above the banking sector in general. It still looks more overvalued when comparing Santander Brasil with its main national private peers such as Itaú and Bradesco. Itaú trades at a forward price-to-earnings of 8.67 and Bradesco at 10.18.

Based on projections for a scenario two and a half years from now, analysts expect Santander to achieve a 44.2% growth in EPS and approximately 20% growth in revenues. These projections indicate a forward P/E ratio of 7.34 and a forward price-to-sales ratio of 2.63, aligning more closely with the current average of the banking sector.

In any case, the bank must conduct a very assertive execution to obtain this multiple and count on a more relevant macroeconomic scenario of interest rate reduction to reverse this trend. The Brazilian Central Bank, in its last meeting , maintained the forecast for 2024 at 10.0% and projected an interest rate of 9.0% for 2025, while the current interest rate in Brazil stands at 13.75%. The projection for the end of the year remains at 12.50% for the introductory interest rate of the Brazilian economy.

The macroeconomic scenario of high-interest rates for the foreseeable future implies that national banks will continue to face a challenging environment of higher defaults. The persistence of high-interest rates puts pressure on these banks to increase efficiency and justify their valuation multiples.

The Bottom Line

Santander Brasil's latest results could have been more robust, showing that there is still a long way for the bank to adjust its operation to reduce the risk of its credit portfolio, which should continue hurting its function for the following quarters. The steep drop in net income and other areas of concern discourage a more optimistic scenario for the distribution of better dividends throughout this year.

Among the leading national banks, I see Santander Brasil's valuation as unattractive for what it has been delivering. The thesis of buying Santander Brasil based on dividends continues to be the most appealing. Still, as the financial results should remain under pressure, I see a less attractive dividend yield further ahead.

Although I still hold a long position in Santander, acquired years ago due to the bank's ability to be one of the primary payers of dividends in the banking sector in Brazil, for now, I am not investing more in Santander as I see better options in the Brazilian banking industry such as Itaú for a more defensive approach and Banco do Brasil ( OTCPK:BDORY ) for better dividends.

For further details see:

Banco Santander (Brasil) Stock: Lackluster Performance, Not Warranting A Buy