BBDO - Bancolombia: An Undervalued Enticing Income Stock

2023-12-04 23:00:14 ET

Summary

- Bancolombia faces headwinds in loans and deposits due to Colombia's economic slowdown, high inflation, and regulatory uncertainties.

- The bank's loan portfolio extends across Colombia, Panama, Guatemala, and El Salvador, providing crucial geographical and revenue diversification.

- CIB shows resilience with recovery trends, strong liquidity, and a positive net income margin.

- Despite consumer loan issues and regulatory challenges, Bancolombia's recovery, robust ROE, and attractive valuation make it an appealing investment, boasting a dividend yield exceeding 10%.

- Short-term challenges persist, but the Company's cautious 2024 GDP growth forecast aligns with expected improvements in the Colombian macroeconomic landscape.

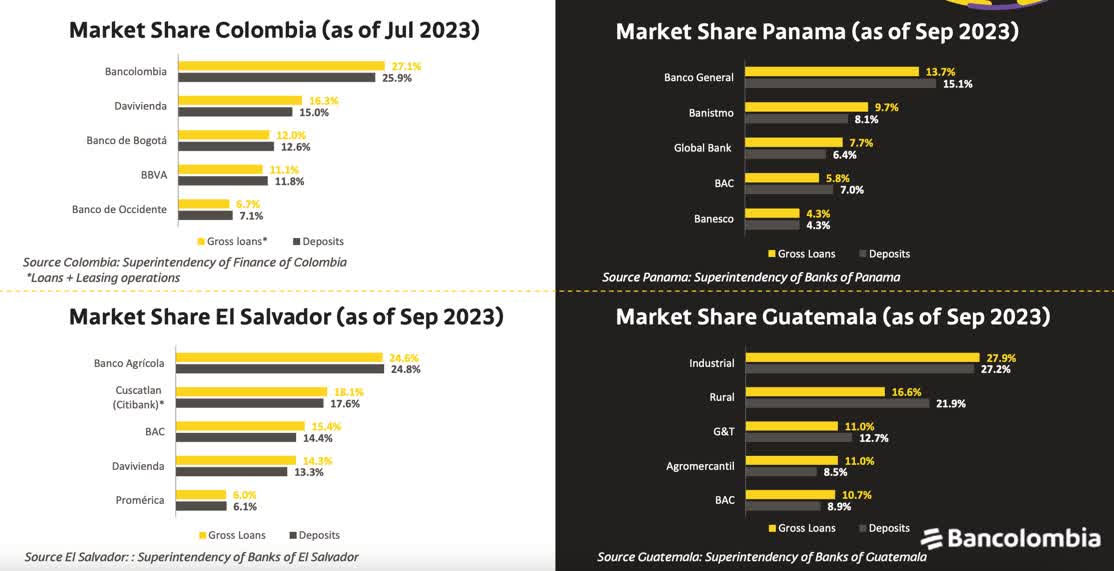

Bancolombia S.A. ( CIB ), Colombia's largest bank in terms of loans and deposits, has faced headwinds amid a progressive economic slowdown in its operating regions, particularly in its home market. The bank commands market shares of 27.1% in loans and 25.7% in deposits on an unconsolidated basis, underscoring its significant influence in the Colombian financial landscape.

With a robust business model that extends its reach internationally across various segments, including investment banking and insurance, Bancolombia boasts geographical and revenue diversification. The bank's loan portfolio is distributed across Colombia (67%), Banditismo (Panama, 13%), GAH (Guatemala, 7%), and Banagrícola (El Salvador, 6%).

{kind=link}

Despite challenges in Colombia's banking sector, characterized by regulatory variations influenced by economic and political factors, Bancolombia has shown resilience. The Colombian banking landscape prioritizes traditional services, aligning with the region's economic diversity and necessitating a more straightforward approach.

The bank has modestly expanded its client segments in Colombia, with corporate clients growing at a Compound Annual Growth Rate ((CAGR)) of 1.3%, SMEs at 2.5%, and retail at 1.4%. However, the sector grapples with regulatory inconsistencies that pose additional risks and complexities, deterring foreign market entry.

Bancolombia's performance since mid-2022 has been impacted by the economic slowdown, notably in Colombia, where high-interest rates and inflation have weakened credit origination, compressed net interest income, led to impaired loans, and kept operating costs elevated.

Despite these challenges, Bancolombia has steadily recovered throughout the year, leveraging its substantial and diversified balance sheet. The bank has maintained adequate efficiency, sustaining an attractive Return on Equity ((ROE)), and exhibited a positive trend in net income margin.

Looking ahead, the outlook for dividends in 2024 may be less optimistic; however, Bancolombia remains an enticing income stock. The bank's valuation level supports an optimistic stance when trading below its book value. The recovery trajectory and resilience displayed by Bancolombia position it as a noteworthy player in the ever-evolving Latin American banking landscape.

Colombia Faces Economic Challenges Amidst High Inflation and Sluggish Growth

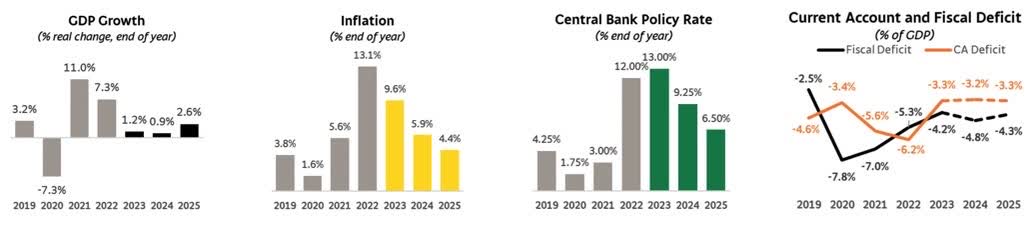

Colombia is grappling with economic headwinds as it battles persistently high inflation and interest rates in the double digits, fueling concerns about the nation's economic trajectory.

The Colombian economy has encountered a pronounced slowdown, eking out a modest expansion of just 0.3% in the second quarter of 2023. Troubles in critical sectors such as retail, construction, and manufacturing have persisted, casting a shadow over the country's economic prospects for the latter part of the year. Bancolombia, a major financial player, has set a cautious GDP growth forecast of 1.2% for 2023, with a conservative estimate of 0.9% for 2024, citing weakened demand and tightening financial conditions as key influencers.

: DANE, Banco de la República, Ministerio de Hacienda. Forecasts by Grupo Bancolombia.

{kind=link}

Challenges persist despite a downtrend in inflation, which currently stands at 11% as of September. The inflationary pressure is attributed to soaring oil prices and fluctuations in regulated goods within the Latin American nation.

A watchful eye is being kept on additional factors contributing to inflation, including the potential impact of El Niño-induced climate conditions on food and energy prices, possible spikes in oil and diesel costs, and the looming decision on a higher-than-expected minimum wage for 2024. Consequently, the Central Bank has opted to maintain its policy rate stability at 13.25%, leaving room for potential gradual rate cuts before the end of the year.

Despite the economic challenges, there is a glimmer of fiscal improvement. Lower-than-expected government spending and tax and oil revenues stability have contributed to a positive fiscal outlook. The government has committed to adhering to the Fiscal Rule, a goal that seems attainable for 2023-2024. However, potential fiscal uncertainties in the medium term loom, including the possibility of increased social spending and resource allocation for implementing approved reform agendas.

The current account balance has contracted, driven by a 10% year-on-year decline in exports and a substantial 25% reduction in imports. Fitch Ratings anticipates the operating environment for Colombian banks to remain stable, aligning with a 'bb' factor score.

Bancolombia's Financial Landscape: Navigating Challenges Amid Economic Strain

In the face of a challenging economic environment in Colombia, Bancolombia's financial health has been under scrutiny, revealing a nuanced picture of profitability, loan portfolio quality, liquidity, and operational efficiency.

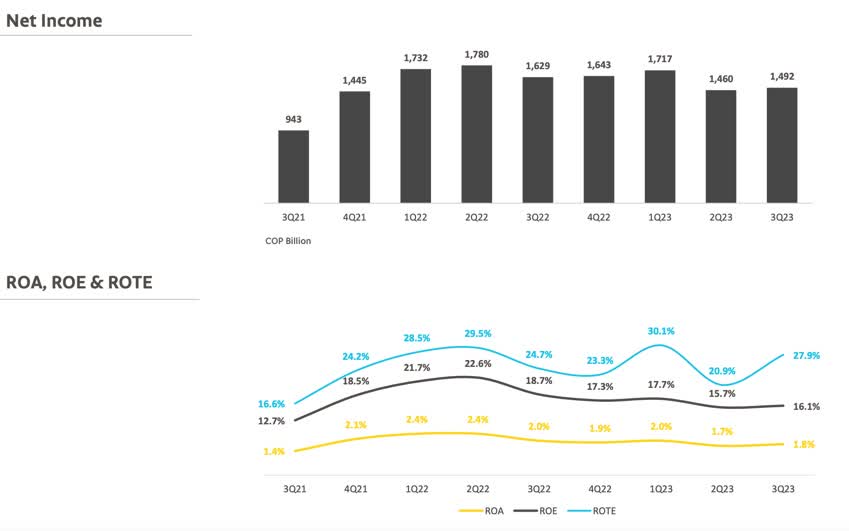

Profitability Challenges: Over the past three years, Bancolombia's profitability indicators have faced headwinds influenced by Colombia's economic struggles with high-interest rates and inflation. Key metrics such as Return on Assets (ROA) and Return on Equity ((ROE)) have steadily declined since the second quarter of 2022, mirroring a drop in net income. In its latest quarter, Bancolombia revised its ROE guidance from 16% to 15%, anticipating a more challenging scenario for the fourth quarter.

{kind=link}

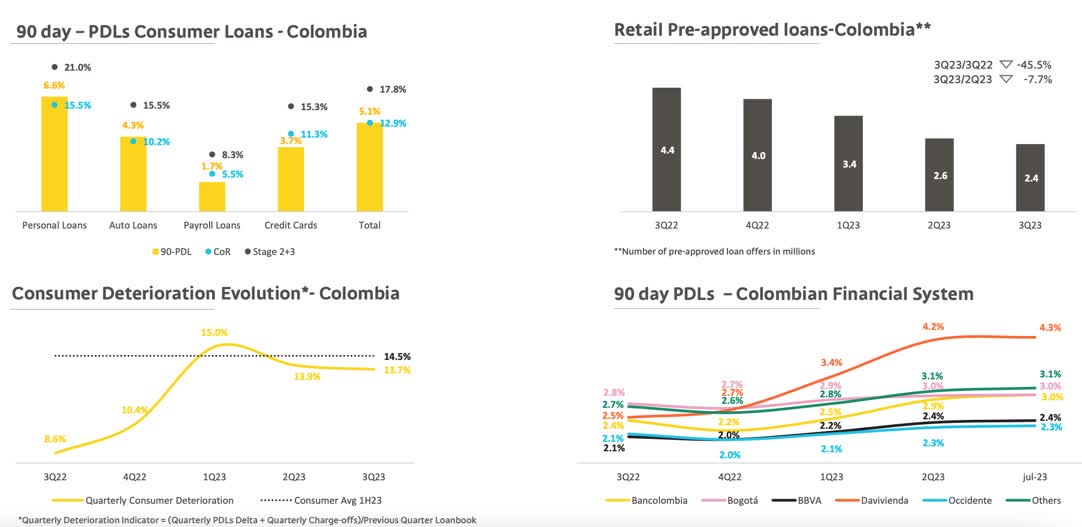

Loan Portfolio Quality: Bancolombia's loan portfolio reflects challenges, notably with consumer loans experiencing a 13.7% increase in deterioration over the past year. Although slightly below the industry average, the uptick in 90-day Past Due Loans (PDLs) to 3.2% signals a rise in significantly delinquent loans. This trend, while maintaining a somewhat tolerable level in the face of a credit environment impacted by high-interest rates in Colombia, poses noteworthy challenges.

{kind=link}

The Colombian bank experienced a significant reduction of nearly 45% in the volume of preapproved loans extended to individuals on a year-over-year basis, with a 7% decrease observed quarter-over-quarter. As a result, the trend in the formation of past-due loans in consumer loans in Colombia persists, aligning with the trajectory witnessed in the first half of the year. Notably, the evolution is below the established average for the initial six months, although progressing slower than anticipated by Bancolombia's management.

However, the 204% coverage in 90-day Past Due Loans (PDLs) for Bancolombia indicates a robust provision for potential credit losses, reflecting a prudent risk management strategy.

The bank's reduced coverage ratios for past-due loans suggest a potential risk perception and provisioning strategy shift. Despite management assurances that consumer loan deterioration is peaking, guidance for the last quarter indicates a cautious outlook.

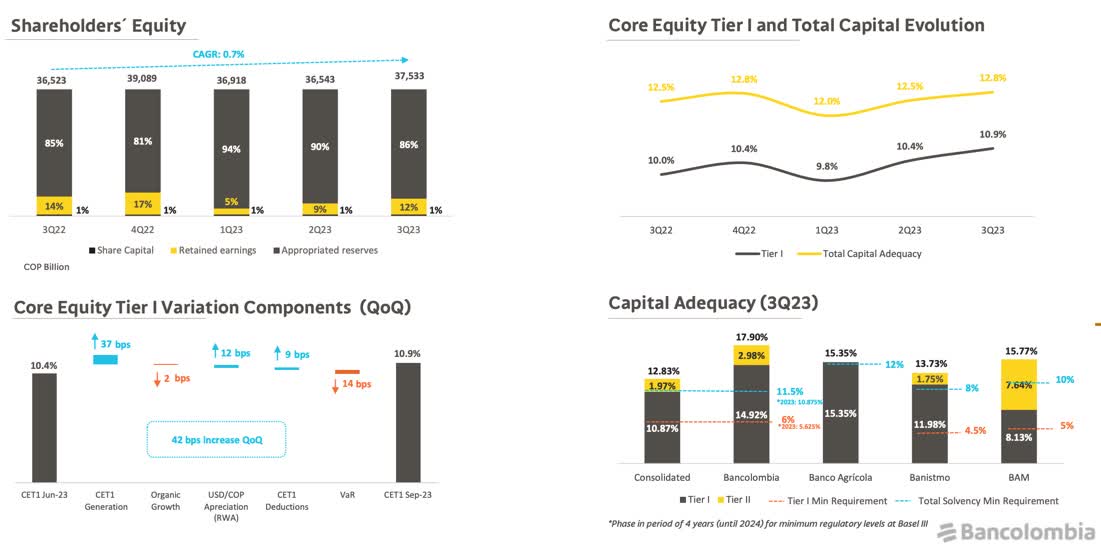

Liquidity Resilience: Bancolombia's resilience stands out in terms of liquidity, supported by a diverse mix of time deposits, savings accounts, and checking accounts. While liquidity posed concerns in early 2023, total capital adequacy improved annually, with the rising Core Equity Tier I (CET1) and Total Capital ratios. These positive trends indicate effective risk management, regulatory compliance, and financial stability.

{kind=link}

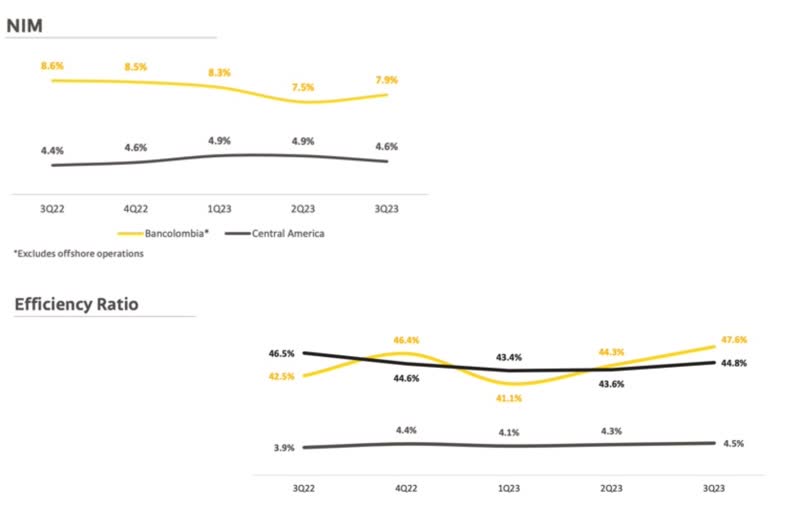

Operational Efficiency and Management Effectiveness: Operational efficiency is a mixed bag for Bancolombia. The efficiency ratio has seen a progressive increase, signaling a decline in efficiency. Operational expenses (Opex) rose significantly in Q3 2023, growing 19.7% YoY, prompting a red flag. Management emphasizes ongoing cost control initiatives to enhance efficiency, aiming for an efficiency ratio of around 46% by year-end.

{kind=link}

A closer look at Net Interest Margin ((NIM)) reveals a decline from 8.6% to 7.9% YoY, indicating a reduction in the spread between interest income and expenses. However, a positive trend emerged in Q3 2023, with NIM improving by 0.4% despite ongoing growth in interest expenses.

Valuation and Dividends

Despite encountering substantial macroeconomic challenges throughout the year, Bancolombia appears to be trading at highly attractive valuation multiples, presenting a potential opportunity for investors.

The bank's price-to-book value stands at 0.83x, a notable 25% below the sector average. This discrepancy suggests that the market is undervaluing Bancolombia, possibly due to concerns about its assets, earnings prospects, or future performance. This apprehension is likely rooted in the more pessimistic outlook for the Colombian economy and its inflationary environment.

Comparing Bancolombia to its domestic peers, Grupo Aval ( AVAL ) reveals intriguing dynamics. Despite trading at similar multiples, Bancolombia showcases more robust growth potential. In a year-over-year comparison, while Grupo Aval experienced a 14% decline, Bancolombia demonstrated resilience.

{kind=link}

Examining the excellence and perception of services among domestic banks, as of November 2023, Banco de Bogotá (which belongs to Grupo Aval) is at the forefront of the reputation ranking within the Colombian banking sector, boasting a 5.7 out of 10. Following closely behind are Bancolombia and Banco de Occidente (which also belongs to Grupo Aval), with scores of 5.5 and 5.3, respectively. Despite occupying the top position in the ranking, the analysis suggests that the reputation of the evaluated banking entities is still perceived as "fragile, weak, and average."

Extending the comparison to other banks in Latin America, particularly Brazil's giants Itaú Unibanco ( ITUB ) and Bradesco ( BBD ), reveals intriguing trends. Despite sharing a similar ROE, the Brazilian banks command more robust multiples, underscoring the resilience of the Brazilian economy. Notably, Itaú stands out with more favorable valuation metrics.

Regarding dividends, Bancolombia's dividend yield, exceeding 10% this year, is expected to moderate for 2024 due to less optimistic growth projections. Projections indicate a yield of 10.9% for 2023, but with a forecasted 6% EPS decrease in 2024, the annual dividend per share is estimated at $2.50, yielding 8.8%. An 8% Return on Investment ((ROI)) implies an implied value of $31.23 per share. This suggests that investing in Bancolombia could be a strategic move, considering its potential as a robust income stock for 2024.

Bancolombia's filings, Seeking Alpha, compiled by the author

The Bottom Line

The negative performance of Bancolombia's shares since mid-2022 can be attributed to a trend following the deterioration of the Colombian economy, high inflation, and rate hikes by the Colombian central bank. Both small businesses and individuals have restricted their access to credit, impacting the bank's profit generation.

Several factors contribute to this scenario, the most significant being the rise in provisions for the consumer portfolio. Additionally, Bancolombia and other Colombian banks face challenges in expanding their assets. Another sizable risk is the uptick in 90-day Past Due Loans (PDLs), posing noteworthy challenges despite Bancolombia's initiatives to reduce nearly half of the preapproved loans extended to individuals year-over-year.

Nevertheless, Bancolombia has demonstrated a mild recovery trend this year, suggesting that there may still be a peak in customer loan deterioration between Q3 and Q4. The prognosis for 2024 appears more positive, anticipating improvements in the Colombian macroeconomic landscape as gradual interest rate cuts are likely to be considered before year-end.

From a personal perspective, investing in Bancolombia shares seems appealing, especially considering their current trading value at a book value below 1x. This is supported by the fact that the bank's liquidity concerns seem to be in the past. It maintains a robust Return on Equity ((ROE)), higher than that of other larger domestic and Latin American banks, and it may continue delivering enticing dividends for the following year.

For further details see:

Bancolombia: An Undervalued Enticing Income Stock