CIB - Bancolombia: Is It Really The Right Time To Invest In LatAm Banks?

2023-10-14 07:32:45 ET

Summary

- Bancolombia faces risks from rising interest rates and the growing popularity of e-commerce/fintech in Latin America.

- The stock has been volatile, with periods of extreme growth and massive drops.

- The bank's expansion into different geographies has helped mitigate risks, but investors should watch for resource allocation.

Introduction

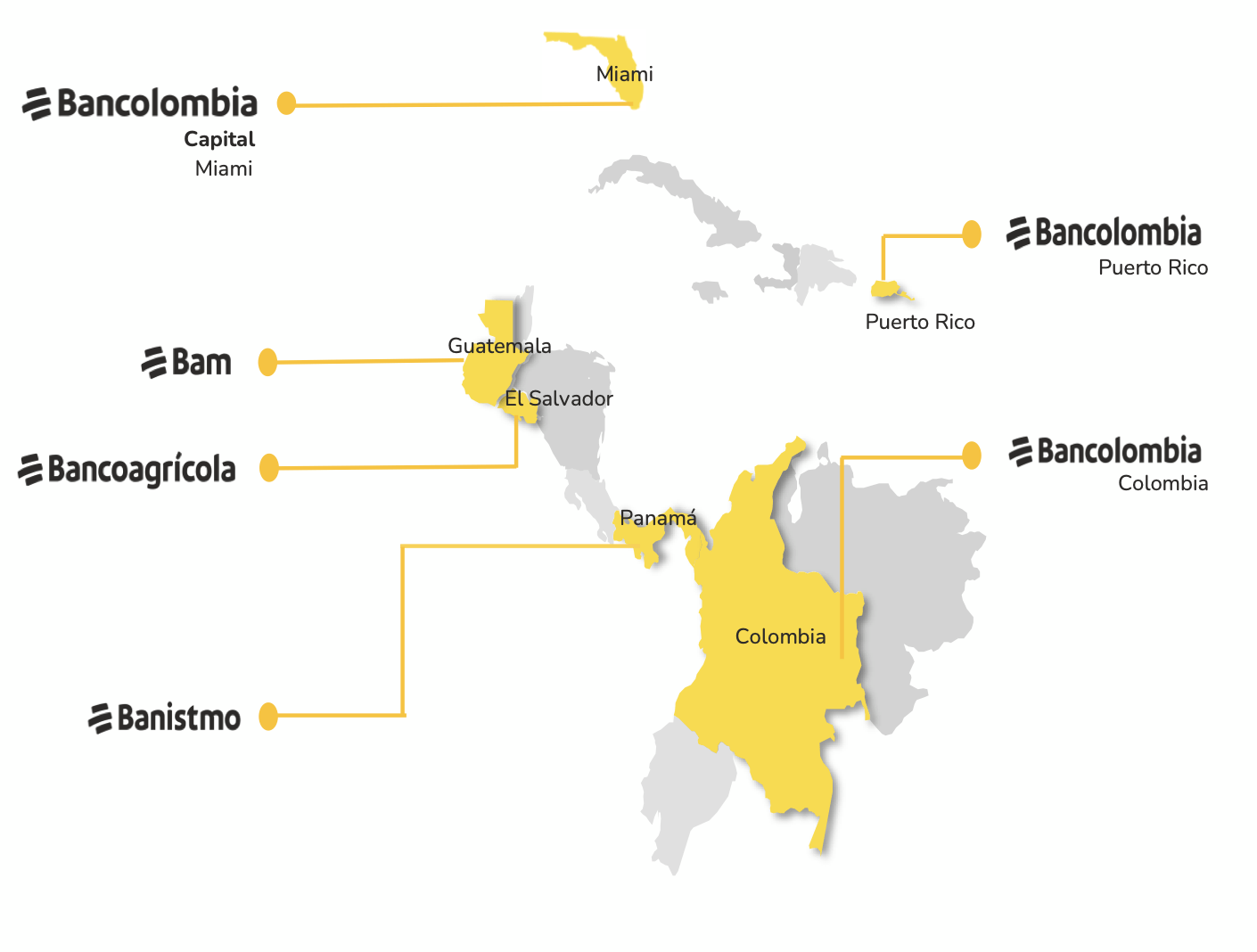

In today's article, we'll explore the Latin American banking company, Bancolombia (CIB) which is a financial institution serving a wide range of LA regions, including Colombia, Panama, El Salvador, Puerto Rico, the Cayman Islands, Peru, and Guatemala. The bank provides various financial products and services, from banking to insurance and trust services.

Bancolombia is in a unique position, it faces threats from the rising interest rate environment, the growing popularity of fintech in Latin America, and an expected economic slowdown. But working in Bancolombia's favor are the strong demographic trends in the region, whereby the population is expanding much faster than in the West which will support new account growth and strong local market positioning.

For investors, the stock has been incredibly volatile going through periods of extreme growth and massive drops. After peaking in 2013 at $70 a share investors' returns have languished as the stock has slowly trailed down to the price where it currently trades, $25.

Investors who are deep in the red, of which there are surely many, are likely wondering what the best course of action moving forward is. Is it time to pull the rip cord and sell, or is it rather the time to back up the truck and double down?

Within this article, we'll explore that and much more.

Banking in Latin America

{kind=link}

For investors new to the name, it's important to understand that banks in the US versus Latin America operate under a very different framework.

For example, the United States is marked by well-established institutions, a robust regulatory framework, and a diverse range of financial services from investment banking to asset management and insurance.

The U.S. financial landscape is characterized by large, global banks, providing a stable and sophisticated environment for investors, think of JPMorgan ( JPM ), and BlackRock ( BLK ) as examples. While the US banking industry remains exposed to economic shocks (as we all saw earlier this year) it is much more regulated than many banks in developing markets like Bancolombia.

Additionally, as the world's reserve currency, US-based banks are granted the additional benefit of primarily transacting in the reserve currency. This results in a lower impact of currency fluctuations and increased liquidity for large transactions.

In contrast, Latin American banking is more fragmented, with varying regulatory environments influenced by each country's unique economic and political factors. Banking in Latin America tends to be more focused on traditional services, such as savings and loans, reflecting the need for a simpler approach given the region's economic diversity. Regulatory consistency can also be a challenge, creating additional risks and complexities that make it more difficult for foreign companies to enter.

Another component of banking in Latin America is the underlying economic development story which has seen periods of extreme booms and busts.

In Latin America, most of the economies are reliant on cheap labor to serve tourism, materials, mining, and industrial sectors. These industries are heavily connected to global growth which has historically been a major contributor to the poor share price performance of banks during times of economic weakness.

The Story of Bancolombia

Bancolombia roots begin as one of the oldest, still operating, organizations formed in Latin America as the Banco De Colombia came into existence in 1875. Over the years the bank has grown to expand beyond its borders, both through organic expansion, as well as M&A to gain access to new territories or consolidate market share.

Through M&A they've established a large presence in the developing economies of Guatemala, Panama, and El Salvador. The bank's strategy of organic + inorganic growth in new territories allows them to land, and then rapidly expand through consolidation of the peers in the region.

Supporting their M&A strategy, many Western banks are highly risk averse which led to underinvestment in the region. This underinvestment has created a great landscape for buyers who can move quickly, buyers like Bancolombia.

Another plus to this strategy is that its expansion through different geographies helps Bancolombia mitigate the impacts of investing in developing economies. Since their "eggs" are not all in one basket, negative developments in one country could be offset with growth in another.

That said, spreading so wide runs the risk of spreading your resources too thin so it's something investors should keep their eyes on over time.

Steady Book Value Growth

Their continued geographic expansion has led to a steady increase in book value which now sits at $8.77B, up from $2.5B in 2010.

Interestingly, though book value continues to grow, the share price languishes, so what gives? Well, that would be due to their dividend policy whereby investors are able to cash in on a roughly 10% dividend yield!

Talk about cash flow.

Taking into account the large dividends Bancolombia pays, the performance of their share price has not been nearly as atrocious as previously indicated but still leaves much to be desired as after 10 years, investors would still be in the red, dividends included.

However, it must be said, that with such a large payout, one must be cautious and keep their eyes out for signs of a dividend cut. Something that their financial performance may indicate could happen sooner versus later.

Economic Woes Ahead

Per their latest quarterly earnings, net interest income fell 8% quarter-over-quarter as a result of more expensive funding. In layman's terms, that means they are having to pay out more interest to depositors.

Yes, NII is still up 14% year-over-year, but often in banking, these shifts come rapidly and thus a slowdown could deepen exponentially. Past due loans are also up 3% quarter-over-quarter indicating that the slowdown may be starting to rear its head in large parts of Latin America.

And yes, again, to reiterate, 3% is indeed a low number, but it could rapidly expand if the slowdown persists, which I believe is likely given the rise of long-term interest rates, especially in the US, over the past month.

It does appear the bank has been making some efforts to mitigate this risk. For example, Bancolombia has experienced increased client engagement and deposit growth, but there's been a reduction in loans from the digital Nequi and Bancolombia a la Mano. Per management in the last earnings call, this decline in lending is primarily a strategic decision to ensure the loans align with their risk tolerance, given that these digital banking initiatives target middle to low-income individuals. Asset quality led Bancolombia to slow down originations, refine scoring models, and gather more data to restart lending with different strategies in the second quarter.

They note their focus remains on monetization and profitability while being mindful of what they call a "challenging economic slowdown".

New Threats

The rise of e-commerce and fintech brings a new wave of risks to Bancolombia. These risks encompass the competition from new digital platforms that can attract customers away from traditional banking notably the potential for fintech to disintermediate banks and evolving customer expectations for a better digital experience. To manage these risks, Bancolombia does offer some digitally native services, but it is still exposed to competitors like MercadoLibre ( MELI ) who have large fintech aspirations.

Valuation

On a price-to-book basis, Bancolombia looks very cheap at just .7x book value. This means you are essentially buying a dollar for a mere 70 cents. Banco Santander De Chile, which has had slower book value growth sports a price to book of more than 2x than Bancolombia.

Of these peers, only Woori Financial ( WF ) has a lower price-to-book ratio at 0.3x.

Conclusion

In conclusion, Bancolombia is certainly an interesting investment prospect... On the one hand, they are navigating the challenges of a shifting financial landscape marked by rising interest rates and the rise of fintech along with all the risks those bring. On the other hand, the bank is bolstered by favorable demographic trends in Latin America.

With a growth strategy blending organic expansion and strategic acquisitions, Bancolombia maintains a sturdy position, offering an alluring 10% dividend to yield-hungry investors.

Looking forward, the company will need to manage its balance sheet through the economic uncertainties ahead, as evident from the recent pace dip and mounting interest costs. However, given the extremely low valuation, I feel that there is a large enough margin of safety for investors with a risk-on appetite.

With that, I rate Bancolombia a "Buy".

For further details see:

Bancolombia: Is It Really The Right Time To Invest In LatAm Banks?