CIB - Bancolombia: Well Managed Solidly Profitable And Historically Undervalued

2023-07-31 12:36:56 ET

Summary

- Bancolombia is an exceptionally well managed bank with a share of more than 25% of deposits and loans in Colombia.

- Colombian equities are historically undervalued, with a price to cyclically adjusted earnings ratio (CAPE) of less than 7x.

- Bancolombia's stock is trading at just 5x earnings, half of its historical average of 10x.

Leading Colombian bank Bancolombia ( CIB ) has performed relatively strongly to start the year, with a total return of more than 16% in USD. That's been entirely the result of the strengthening in the Colombian peso this year of about 22%, though, while shares traded in Colombian pesos have declined in price.

Longer-term share price performance in USD has been poor for more than a decade as the dollar has significantly strengthened. Total return has been essentially zero since 2012.

Longer-term performance for Colombian equities in aggregate have been even worse, leaving valuations historically attractive.

According to the Emerging Markets Investor , the price to cyclically adjusted earnings ratio ((CAPE)) for Colombia was less than 7x as of June 2023. The United States, a poor comparison in isolation, had a ratio of 31x. While the attractiveness of U.S. equities is a different conversation, Colombia is quite cheap compared to its own historical average of 14x. It is also quite cheap to other countries in Latin America, many of which have very different narratives at the moment.

The thesis on Bancolombia is actually quite simple: it is an excellently run bank with a fantastic market position in Colombia, it trades at historically attractive prices, and will benefit as political fears continue to subside.

After covering the company itself and its position in the Colombian banking system, some time is spent below reviewing the political situation in Colombia and why others have perhaps been hesitant to invest in Colombia. Finally, some forward earnings estimates and valuation models are considered.

In short, Bancolombia has a long history of excellent and conservative management, has a leading position in the banking system of a growing economy, political concerns that have persisted for over a year seem overblown, and the bank trades at just 5x earnings.

Bancolombia and the Colombian Banking System

Bancolombia currently has total assets of about $75 billion and shareholders' equity of $8 billion. That puts its balance sheet very roughly on par with Memphis based First Horizon ( FHN ), as a frame of reference for readers in the United States.

About 70% of the bank's profits come from Colombia, with the remaining 30% from ownership in leading banks in Panama, El Salvador, and Guatemala. The Colombian bank is a leader in its market with a very large 27% share of loans and 26% share of deposits in the country. The Colombian banking system has actually historically been extremely competitive , but in the beginning of the 1990s state owned banks were privatized during a period of reforms aimed at financial liberalization. Then, in 1998 the emerging markets financial crisis came to Colombia and about half of the financial institutions in the country ultimately failed or merged with stronger entities. Early that year, the modern Bancolombia was formed by Banco Industrial Colombiano's acquisition of Banco de Colombia. At that time, the bank controlled roughly 12% of the loans and deposits in the country. Incremental consolidation has taken place in the years since then. Today, the four largest banking groups control close to 80% of the financial system. It's an arrangement that is remarkably stable and ensures the Colombian government is unlikely to need to bail out the financial system, but it is not without criticism. For their part, the banks have given the country an extremely stable banking system and pay taxes at rates exceeding other business sectors. They also earn attractive profits. Return on tangible equity over the last decade has averaged about 18% for Bancolombia excluding the pandemic affected year of 2020.

In recent years, Bancolombia has heavily invested in digital channels and has become a market leader in digital banking. Nequi, a digital banking platform developed in-house, now has about 15 million users and deposits of $400 million. The bank has also heavily invested in digital tools for its core banking customers, retail, SME, and corporate customers. These digital investments should help continue to entrench it as the market leader in Colombia.

Without going into extensive detail on the bank's Central American operations, it does have about 30% of its overall business there. Banistmo, the second largest bank in Panama, was bought from HSBC in 2013 for a little more than $2 billion. Banco Agricola, the largest bank in El Salvador with about a quarter of the loans and deposits in the country, was acquired in 2007 for about $900 million . Finally, the fourth largest bank in Guatemala was purchased in a series of transactions between 2012 and 2020 that totaled about $600 million.

Recent Events in Colombia

When discussing Bancolombia with other investors (and Colombian stocks more broadly), two bear themes tend to emerge. The first is the political situation in the country and whether there will be a permanent swing leftward in the country's politics. The second is that Colombia's exports are heavily weighted towards energy and efforts to transition to cleaner energy production could create a big hole in the country's current account balance and weaken the currency substantially.

The first concern was heightened by the election one year ago of Gustavo Petro to President. Prior to that, the country had elected conservative Presidents for twenty-four years - six consecutive terms. The country's liberal party, which had often won the Presidency prior to that point was and is more a center-left party as well, making Petro the country's first President truly of the left. He had previously been mayor of the capital city of Bogota and a Senator, but the extent to which his election would transform Colombia and its markets was a big unknown to investors.

President Petro's first year in office has not gone as he had intended. His approval rating has fallen from 56% to 33%. The President achieved early success with the passage of tax reform last fall that attempted to close large pandemic related deficits largely with increases in corporate taxes, particularly through additional taxes on resource extraction companies and a surcharge on financial institutions. The deficit for 2023 should fall to a little more than 4% of GDP compared to 5.5% in 2022. However, most other aspects of Petro's legislative agenda have not been enacted. These include a proposal to increase access to the pension system and increase the government's role in pension management, labor and health reforms, as well as changes to campaign finance and political parties.

Frustrated by a lack of progress on many legislative priorities (particularly health reform), Petro dismissed most of his cabinet in April. That included Finance Minister Jose Antonio Ocampo, an economics PhD who had previously taught at Columbia University and who is seen as generally friendly to markets. The peso temporarily came under pressure as a result.

However, not long after the cabinet reshuffle, multiple political scandals have emerged. The details of these scandals, involving the nanny of the President's Chief of Staff and accusations of corruption in campaign finance, are less important than the fact that they have been a blow to the President's popularity. With legislative priorities already stalled, the odds have looked increasingly slim that any radical change in the country will be enacted and the Colombian peso has rallied sharply as a result.

There are still three years left in President Petro's term and Congressional elections will take place shortly before the 2026 Presidential election will. That is obviously a long way off and much can happen in the interim. But, the chances of an environment dramatically hostile to business seems to be significantly reduced.

One additional long-term concern for investors is the ability of Ecopetrol ( EC ), the majority state owned oil company, and other oil companies operating in Colombia to continue exporting fossil fuels in enough quantities to preserve a manageable current account deficit in the country - that or the country will be forced to find substitute exports or risk large devaluations in the Colombian peso. Oil is currently about a third of exports and fossil fuels make up even more when refined products and coal are taken into account. Concern has existed due to proposed plans by Ecopetrol to suspend exploring for new oil and rapidly transition to investing in other energy sources. President Petro has said that he will not approve new licenses for oil exploration. That does not mean that oil companies in Colombia will be unable to replace their reserves, but it does mean that they will have to do so by means of existing licenses. I do not consider myself an expert on the oil industry in Colombia, but thus far Ecopetrol has been able to continue replacing reserves - at a ratio of 117% in 2022 - and today has a reserve life of 8-9 years.

Some of the market's concerns regarding Colombia have been extremely valid and warranted. But, at the same time, policy uncertainty has not been lower since the 2022 election cycle kicked off. With the legislature unwilling to pass much more significant legislation as proposed and low approval ratings, it seems unlikely that transformative legislation will be enacted over the next three years. And while the role of oil in Colombia's exports is a vulnerability, it does not appear to be an acute one. The current account balance deficit is set to decline in both 2023 and 2024 from its unsustainable level in 2022 of about 6% of GDP and while restrictions on new oil licenses will ultimately hamper production in the long-term, new exploration within existing licenses should allow for sufficient reserve replacement in the short-term.

Bancolombia Recent Financial Results and Forecast

Turning back to the business itself, Bancolombia's recent financial results have been robust and it is important to point out that compared to its own history, Bancolombia has been modestly over-earning. In part, this is because last year and this year have seen above average net interest margins due to high interest rates. Last year also included a cost of risk result that was well below the bank's history. ROE in 2022 was very close to 20% and my forecast for 2023 is for this to come in somewhat lower at 17% compared to a longer term average ROE of a little bit less than 15%.

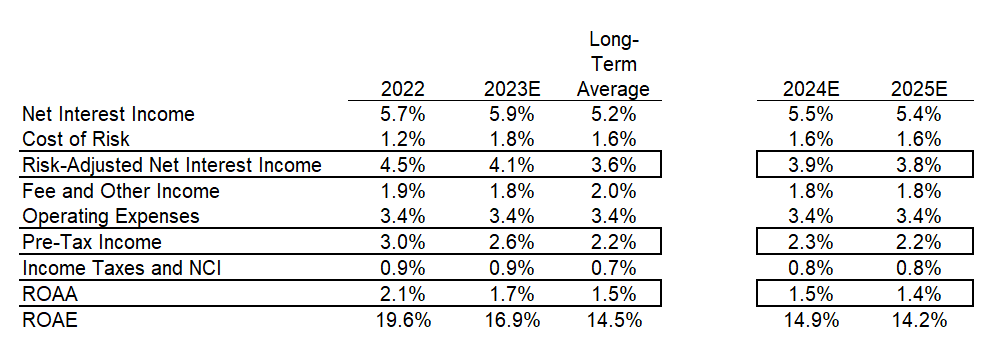

The chart below shows Bancolombia's financial results as a percentage of average assets for 2022, a 2023 forecast, and my estimate of Bancolombia's long-term average. The long-term average is derived from going back to 2015, with results heavily affected by the pandemic removed. My forecast for 2024 and 2025 assumes that the normalization in profitability that looks like its beginning in 2023 will continue over the next two years, with slightly above-trend net interest results and slightly below-trend fee income.

Bancolombia Actual and Forecasted results as a percentage of average assets. (Company Financials and Author Forecast)

{kind=link}

Along with the normalized returns, though, both assets and shareholders equity should continue growing at a good rate with about half of profits currently being paid out as dividends and the rest available for reinvestment, implying that assets and equity should be growing at a 7%-8% rate over the next few years.

Factoring for all of the above, then, should mean that earnings are down slightly over the next couple of years, but generally flattish as lower returns are offset by continued compounding in underlying equity and assets.

The chart below assumes an average exchange rate of 4,300 Colombian Pesos per USD this year and 4,200 in 2024 and 2025 compared to the current exchange rate of 3,940 and a YTD average rate of about 4,500.

These estimates are my own and it should be noted that consensus estimates are lower. Seeking Alpha's aggregation of analyst estimates currently has the next three years at $5.82, $5.71, and $5.63, however, I think much of the gap can be explained by the fact that the peso has appreciated sharply in the last two months and forecasts are lagging that appreciation.

Bancolombia Historical and Forecasted Earnings per ADR in USD (Author)

Valuation

Over the last ten years, Bancolombia has traded at a P/E ratio of roughly 10x and a similar valuation does not seem unreasonable today. Given that the bank is on-track to pay out about 50% of net income as dividends (at 10x earnings that would mean a 5% dividend yield) and retaining the other 50% of net income should produce 7%-8% growth annually in assets and the loan book (assuming 14%-15% sustainable return on equity), a valuation of 10x earnings should imply long-term returns of 12%-13%. That is an attractive return, but not terribly out of line with what an investor might expect in an emerging market bank.

Today's valuation is actually about 5x earnings, implying a dividend yield of about 10% and long-term returns of 17%-18% assuming no multiple expansion to more attractive levels. That seems extremely generous - even for a Colombian bank - especially one with such attractive historical economics and with an excellent position in both its Colombian and Central American markets. Using 10x current year earnings would produce fair value of about $61.

Valuing on historical price to book value gives similar results. The long-term average is close to 1.5x book value. Again, that makes sense for a bank with mid-teens returns on equity that can retain half its earnings and maintain its returns. Taking actual first quarter book value per share and using the current exchange rate gives book value today at just shy of $39 per share. That might be slightly generous given the Panama and El Salvador businesses deal in dollars, but it puts the current price to book value back below 80% compared to the reported value of above 90% using the exchange rate at the end of March. Fair value using historical ratios of price to book value would be about $58.

Given that earnings will likely be flattish over the next couple of years, investors may want to be somewhat conservative and base current valuation on 2025 estimates. But, even doing so and discounting to today at a 12% discount rate still values Bancolombia at close to $50.

Conclusion

With much of the policy uncertainty in Colombia clearing up and historically attractive valuations across the entire Colombian stock market, investors may well be rewarded by deciding to have some exposure in some way to the country, even a small amount.

As previously mentioned, the CAPE ratio for Colombia is now less than 7x - cheaper than just about every global stock market except for Turkey. And although the currency market this year has indicated a renewed optimism for Colombia, the stock market has not - with gains experienced thus far by U.S. investors being nothing more than the effect of currency movements. Local currency investors in Colombia have had a negative year so far in aggregate. To some extent that may be because of Colombia's small capital markets base, but perhaps also because some compelling narratives are at play amongst countries that may normally be competing with Colombia for investment dollars. Mexico, for example, has garnered significant attention as a beneficiary of near shoring by American companies. Argentina has also been attracting significant capital flows in anticipation of a better political climate after the elections this year in October. Peru has also shown much greater stability this year after a Presidential impeachment late last year.

This is not to say that a better performance for Colombian equities is guaranteed along any particular timetable, but it does seem that even though economic growth in Colombia is set to moderate over the next couple of years and earnings should be more or less flat for Bancolombia over that timeframe, that probabilities strongly skew towards Colombia outperforming many emerging markets (including those in Latin America) over the next decade. So long as that's the case, it is very hard to see Bancolombia not participating in that outperformance.

For further details see:

Bancolombia: Well Managed, Solidly Profitable And Historically Undervalued