NCBDF - Bandai Namco Holdings: A Well-Run Content Company Expanding Its Global Footprint

2023-08-07 06:35:36 ET

Summary

- Bandai Namco Holdings continues to focus on growth in overseas markets, which is crucial for its long-term prospects.

- The company's strong library of character content and expansion into global markets are driving its overseas sales growth.

- Despite some challenges in the post-pandemic environment, Bandai Namco is expected to sustainably generate free cash flow and maintain stable profitability.

Investment thesis

BANDAI NAMCO Holdings Inc. ( OTCPK:NCBDY ) continues to execute growth in overseas markets, which will be key for the company's longer-term prospects. Current valuations appear cheap for a quality franchise business with a stable earnings outlook and free cash flow generation. We rate the shares as a buy.

Quick primer

Bandai Namco Holdings is a Japanese content company with intellectual property such as 'Mobile Suit Gundam', 'DRAGON BALL', 'ONE PIECE', and 'Id@lmaster'. This IP is used for toys, figurines, game software, anime/film, music, and amusement facilities. Legacy game software titles published include 'Tekken', 'Soulcalibur', 'Ace Combat', 'Taiko no Tatsujin' and 'Dark Souls'. Digital game content on smartphones via Apple ( AAPL ) made up 11% of total FY3/2023 sales ( page 34 ).

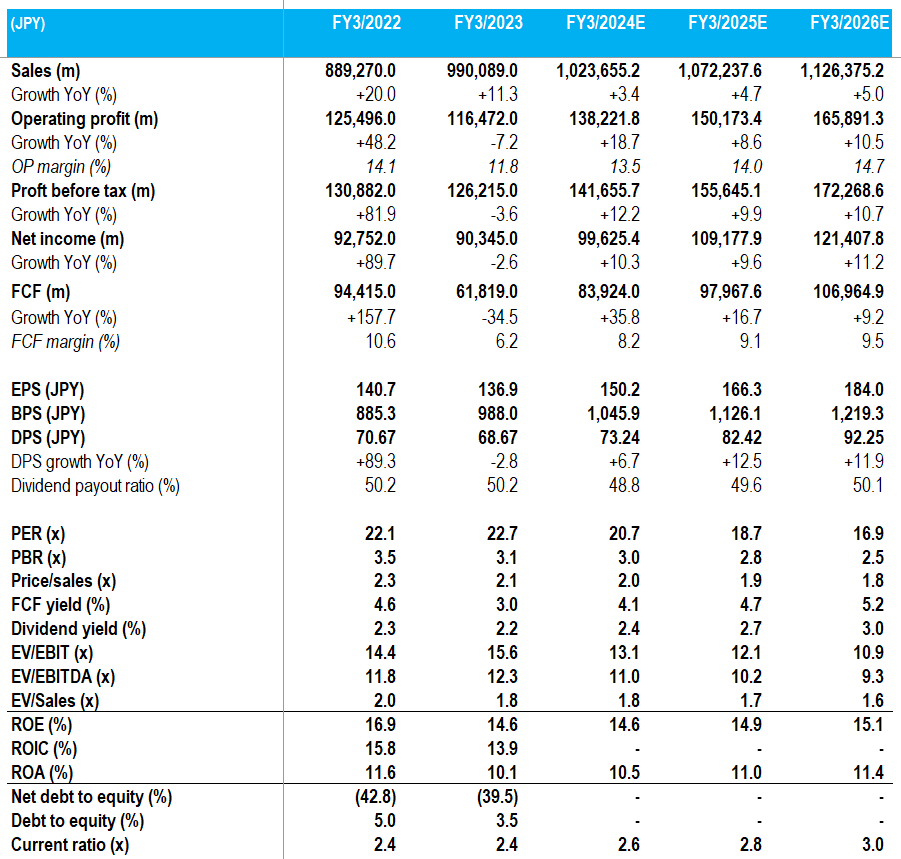

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

{kind=link}

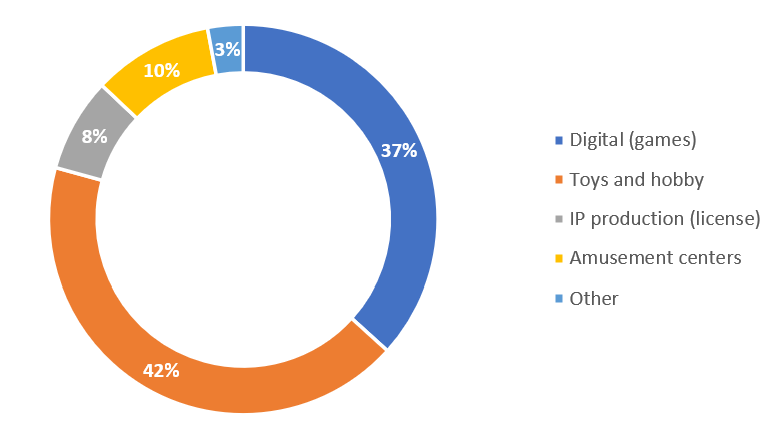

Sales by segment FY3/2023

{kind=link}

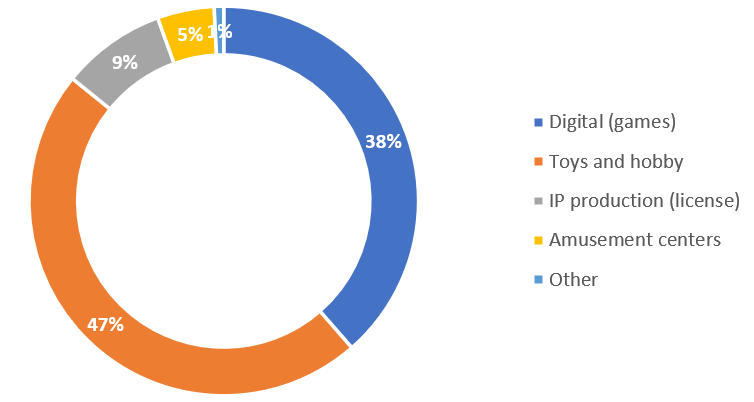

Operating profit by segment FY3/2023

{kind=link}

Segmental profit margin FY3/2023

{kind=link}

Area of discussion

Like many Japanese content companies, Bandai Namco navigated the post-pandemic environment with some difficulty as 'stay-at-home' consumption for digital content normalized. Consequently, FY3/2023 results saw sales growth slow from a high hurdle in FY3/2022 to 11.3% YoY. Operating profits fell by 7.2% YoY as the company saw less successful title releases and write-downs of capitalized game development costs.

For FY3/2024 the company is guiding flat sales growth YoY (only +1.0% YoY), and mild operating growth at 7.3% YoY ( page 3 ). Consensus estimates (please see the Key financial table above) show a stronger growth profile at 18.7% operating profit growth YoY - we want to assess whether this is realistic.

Overseas markets are the key growth driver

Bandai Namco's competitive strengths are its library of character content, and it is making progress in expanding its popularity worldwide. In FY3/2023, overseas sales made up 28.5% of total sales ( page 9 ), an increase from 22.3% in FY3/2022. The company has a target to reach 35% of total sales by FY3/2026, and a longer term projection at 50%.

The importance of overseas growth comes from the impact of the domestic ultra-aging society, which is pushing down the addressable market at home. In Tokyo, the over-65 age group made up 22.7% of the city's population ( page 14 ) in 2015 versus 11.5% of those aged 0 to 14. This demographic trend is expected to continue, forcing the company to seek and acquire new and younger customers elsewhere with the aim of generating high lifetime value.

Whilst Bandai Namco's digital content has traditionally not had the major global following as some of its peers (such as Nintendo ( OTCPK:NTDOY )), the company is making strides in winning foreign fans with 'Naruto' content, as well as new game software titles designed for a global audience such as the award-winning ' Elden Ring ' - the development of an expansion pack was announced in February 2023 to positive feedback, although a release date is yet to be unveiled (we estimate early 2024). With a growing track record of titles with a global reach (such as the 'Dark Souls' franchise, and the 'Tekken' fighting game), we believe the company can continue to effectively gain market share overseas.

The domestic market cannot be ignored, and the company continues to effectively recycle its key franchises such as 'Gundam' and 'DRAGON BALL'. The company remains relatively weak in catering to the female audience (an area served well by the likes of the Sanrio Company ( OTCPK:SNROF )), and this area remains work-in-progress. However, we believe there will be positive developments in licensing revenues as customers return to concerts and fan event activities, and foot traffic continues to recover at the amusement centers pushing up same-store sales YoY.

The company will announce Q1 FY3/2024 results on August 8th, 2023.

Valuation

With a solid slate of product releases and the continued depreciation of the yen, we believe current consensus forecasts look more than realistic. Whilst a major part of annual earnings is derived from the Christmas season, we believe FY3/2024 should start off on a positive note with high-margin repeat sales of back catalog software. On consensus forecasts the shares are trading on PER 20.7x (at a significant discount to the 5-year average of 28.0x), a free cash flow yield of 4.1%, and a dividend yield of 2.4% (based on a 50% payout ratio).

We believe these valuations denote a discount on the following grounds. The current PER multiple looks too cheap versus the 5-year average, despite stable secular themes in electronic entertainment demand. The company appears able to sustainably generate free cash flow, with stable profitability and low capex requirements. Increasing overseas market share should result in high earnings visibility for the company. We see Bandai Namco as a quality franchise business, with solid overseas organic growth opportunities.

Risks

In the short term, content companies run the risk of delayed releases of software titles which can push back earnings recognition. Although such events result in negative market sentiment, it is usually only short-term and an opportunity to buy.

Overseas expansion is progressing but perhaps not at the pace demanded by investors. The company could be penalized for this, or management could take greater risks and invest more heavily in business expansion which may not yield results.

Conclusion

We believe Bandai Namco remains positively positioned to grow, aligned with growth in the electronic entertainment industry. Its contents are gaining market share overseas, which will be key in the longer term. We believe current valuations reflect a discounted quality franchise business, and rate the shares as a buy.

For further details see:

Bandai Namco Holdings: A Well-Run Content Company Expanding Its Global Footprint