BAND - Bandwidth: Struggling With Limited Liquidity

2023-09-12 21:20:43 ET

Summary

- Bandwidth's stock has dropped over 40% while rival Twilio's stock has risen over 30%, indicating a divergence in fortunes between the two CPaaS companies.

- Bandwidth is losing active customers and has weak net revenue retention rates, indicating a struggle to execute its growth strategy.

- The company has strained liquidity and may need to raise capital soon, making it a risky investment option.

- Bandwidth is cheap at <1x forward revenue, but its fundamental risks make it cheap for a reason.

Even though there has been tremendous market volatility over the past few months, most tech stocks remain sharply up for the year in defiance of high interest rates. But while a rising tide has lifted most boats this year, investors have to be incredibly careful going forward to only select the highest-quality stocks to remain in their portfolios - especially as Fed interest rate policy doesn't look like it'll turn more dovish any time soon.

Bandwidth ( BAND ) has been one major exception to the tech rally this year, dropping more than 40% while larger rival Twilio ( TWLO ) has jumped by more than 30%. This reflects a divergence of fortunes between the two publicly traded CPaaS (communications platform as a service) companies, and in my view that disparity is here to stay.

I cut my rating on Bandwidth to bearish several months ago. The Q2 earnings season has been mildly kind to Bandwidth, but I continue to see trouble ahead and am retaining my negative view on the stock. Especially in light of Bandwidth's recent results, several big red flags for the company have popped up:

- Bandwidth continues to shed active customers. Amid weak revenue performance, we should be mindful that Bandwidth is actually losing customers, indicating that it may be losing market share.

- Net revenue retention rates continue to be weak. Barely now over 100%, Bandwidth is failing to execute the "land and expand" strategy that makes CPaaS an attractive business and allows the company to scale its bottom line.

- Strained liquidity. Bandwidth barely has over $100 million in cash remaining and is in a net debt position after considering its convertible debt note. The company is also burning free cash flow, so it may have to raise capital soon in a tough environment.

Yes, Bandwidth is admittedly cheap. At current share prices near $13, Bandwidth trades at a market cap of just $339.5 million. After netting off the $122.5 million of cash and $417.6 million of convertible debt on Bandwidth's most recent balance sheet, the company's resulting enterprise value is $634.6 million.

Meanwhile, for the next fiscal year FY24, Wall Street analysts are expecting Bandwidth to generate $672.1 million in revenue, representing 14% y/y growth. If we also assume 14% y/y growth on the company's adjusted EBITDA target of $45 million this year (holding an 8% margin), adjusted EBITDA would be $51.3 million.

This would put Bandwidth's valuation multiples at:

- 0.9x EV/FY24 revenue

- 12.4x EV/FY24 adjusted EBITDA

In my view, however, Bandwidth is a value trap that's best avoided as the company continues to struggle in recovering top-line fundamentals and achieving meaningful margins. We have to note that at Bandwidth's ~55% gross margin profile (substantially lower than most other software companies), its long-term ability to scale its bottom line is more limited - especially when growth has slowed to the single digits at Bandwidth's current small scale.

Steer clear here and invest elsewhere.

Q2 download

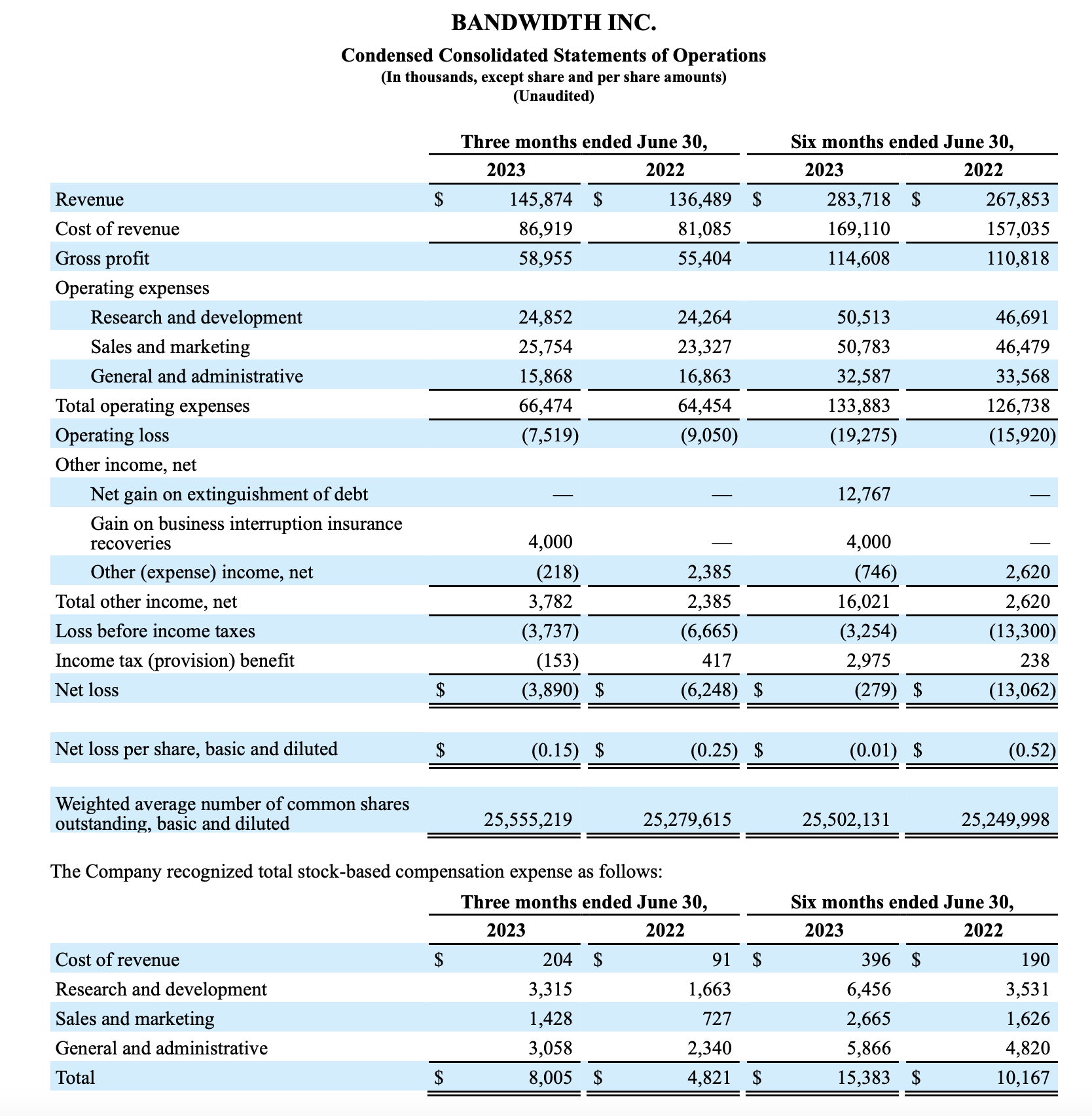

Let's now discuss Bandwidth's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Bandwidth's revenue grew just 7% y/y to $145.9 million, slightly coming ahead of Wall Street's expectations of $140.9 million (+3% y/y). In spite of the earnings beat, however, we do have to wonder if the company has any catalysts to return to double-digit revenue growth next year, which is what consensus is calling for.

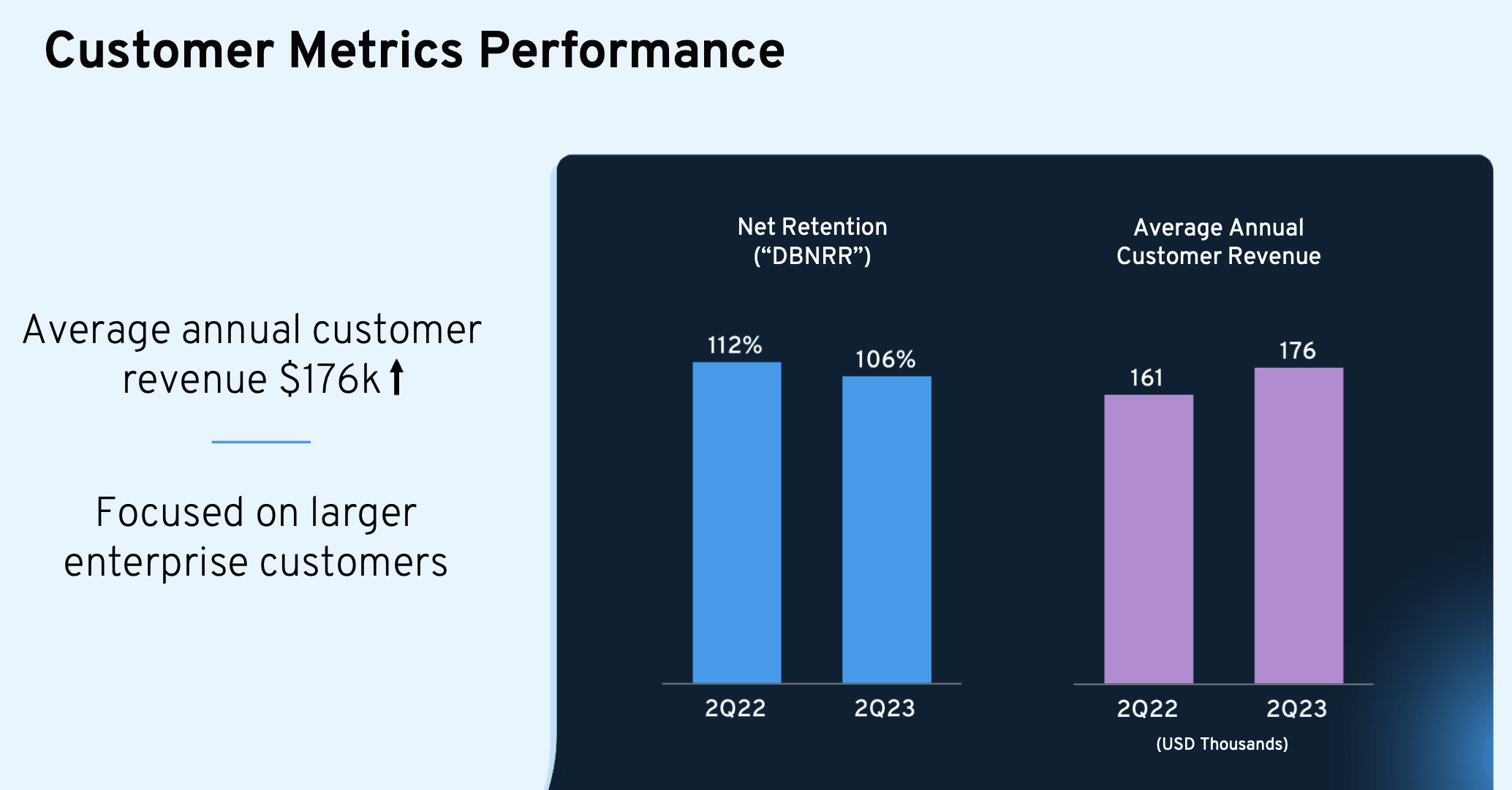

One of the core issues here is a reduction in dollar-based net retention rates, which is a measure of how much customers are expanding their billings on Bandwidth in the following year. This metric has fallen to 106% (down from 112% in the year-ago quarter); despite the company's growing focus on enterprise customers and higher average annual revenue, customer spending trends are still down.

{kind=link}

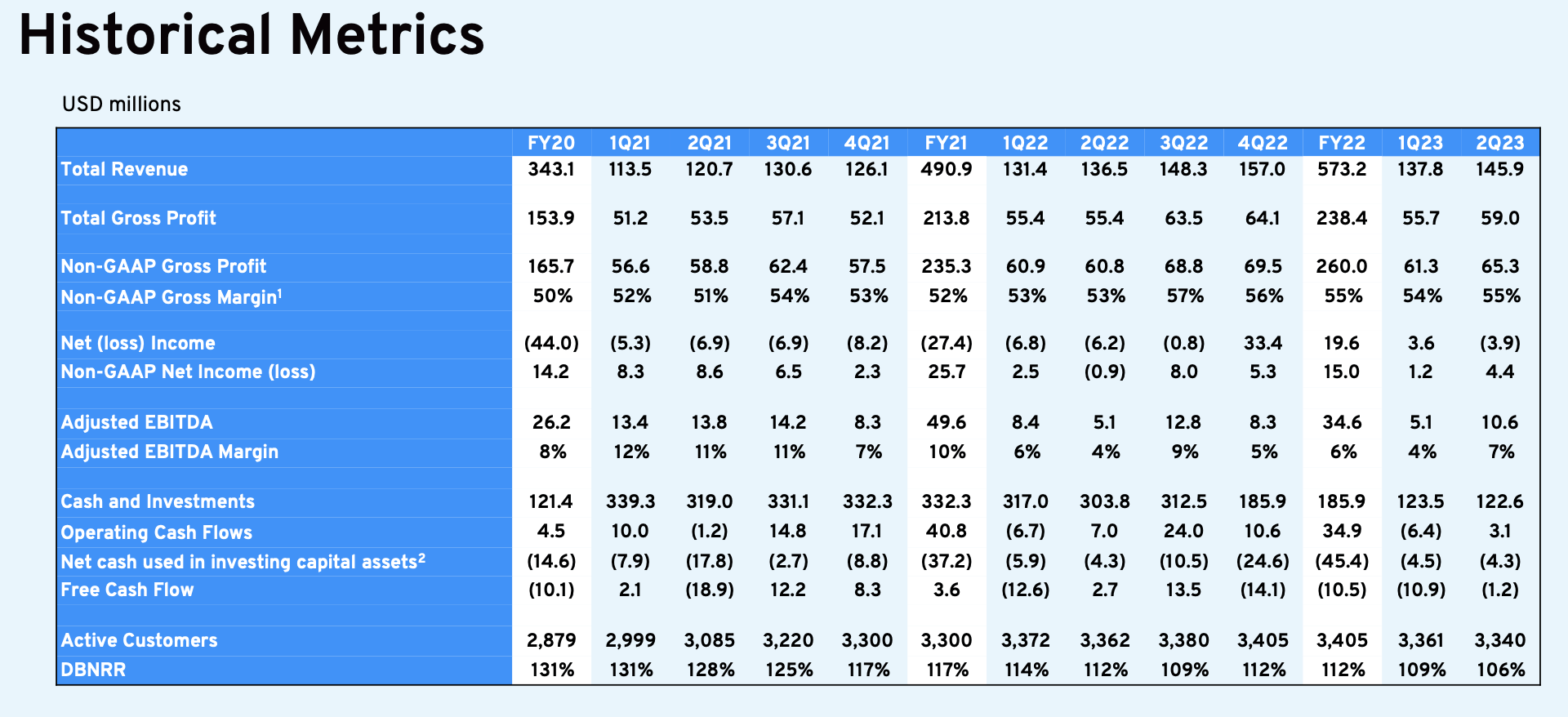

Worse yet: the absolute number of customers that Bandwidth has continues to decline. Total customers in Q2 fell to 3,340, or a loss of 21 customers versus Q1. The slide started in Q1 when Bandwidth first shed 44 customers.

{kind=link}

Software companies rely on momentum to drive sales, especially as IT leaders look to other companies' examples to decide what infrastructure to procure, and a loss of active customers is a clear signal of loss of momentum.

The company continues to cite macro headwinds as a core driver for this slowdown. Per CEO David Morken's remarks on the Q2 earnings call :

Just as we had projected at the start of this year, the macroeconomic environment remains uncertain. We've observed continuing cautious behavior from our customers who are shrewdly evaluating the environment and making investment decisions where it makes most sense and for the greatest returns. We are likewise operating our business through the same environment by scrutinizing product and investment strategies while balancing growth and profitability. We expected this season and thus far it has played out as we projected."

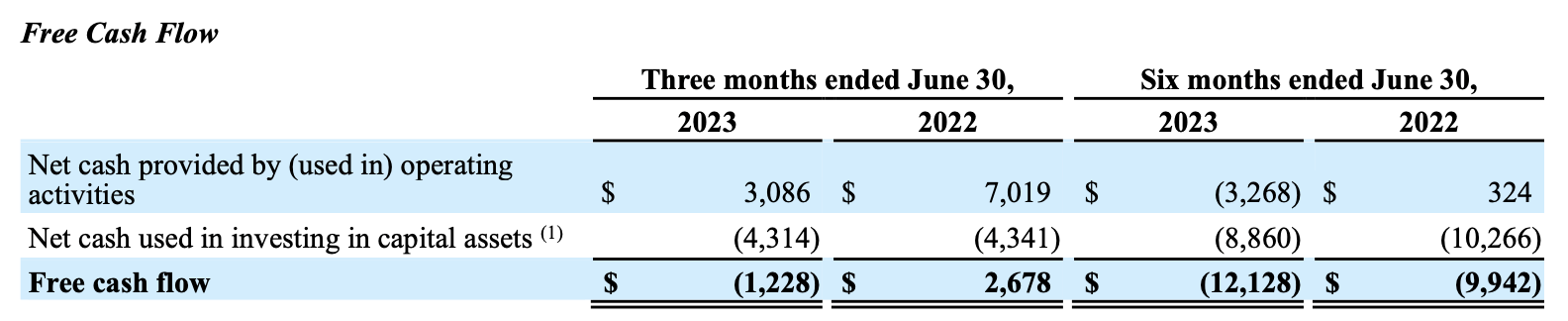

And especially because Bandwidth is a small-cap stock with limited liquidity, we have to be very mindful of the company's cash burn. Year to date, free cash flow has clocked in at -$12.1 million, or a 22% higher burn rate than -$9.9 million in the year-ago period.

{kind=link}

With only $122 million of cash on Bandwidth's most recent balance sheet (or $295 million in net debt ), this is a precarious position for Bandwidth to be in - especially as it only has a line of sight to single-digit growth rates on top of fairly weak gross margins.

Key takeaways

Bandwidth continues to face a bevy of issues, from slow growth and low expansion rates to declining customers and higher cash burn. It's telling that Twilio, despite being at a much larger scale than Bandwidth, grew at a faster 10% y/y pace in the same quarter (gaining market share over Bandwidth, despite facing the same macro conditions). There's a reason the stock trades at such a cheap multiple of revenue: don't fall for the value trap here and invest elsewhere.

For further details see:

Bandwidth: Struggling With Limited Liquidity