BOH - Bank of Hawaii: Banking On (One Of) The Most Isolated Places On Earth

Summary

- A reader from Honolulu asked me to take a look at his local bank, the Bank of Hawaii. Being the island's second-largest bank and largest locally-owned, it could be interesting.

- Bank Of Hawaii was founded over 120 years ago and is a regionally owned commercial finance company, and it's the widest-known business of its kind in Hawaii.

- I show you why despite some appeal here, this company is relatively expensive for the upside it offers - and why you may be better off looking for growth elsewhere.

Dear readers/followers,

Bank of Hawaii ( BOH ) is a company that I've looked at a few times over the past 5-or-so years, and even came close to buying when the bank crashed a few years back. Those that invested have seen some pretty amazing RoR - I unfortunately wasn't one of the people who invested at the time.

But, a reader contacted me - and he lives in Honolulu - and he asked me to take a deeper look because he wanted to know if there was any sort of solid case to be made for short- or long-term ownership of this company.

So, let's see what we have here.

Bank of Hawaii - What does the bank do?

Like most banks, BoH offers a selection of financial services to the residents, in this case, the residents of Hawaii. The island is an impressive area to be in, and while I haven't been there (yet) myself, I've heard enough to confirm that it's somewhere I might be interested in visiting. Plenty of things to see.

{kind=link}

The area is home to a more diverse industry than you might expect. I myself, when I started delving into Hawaii, expected a tourist-heavy (excessively so) economy with all the cyclicality that entails. This is not the case. The largest sector in terms of Hawaii's GDP is trade, transportation, and utilities as well as government and defense, with gov/defense at 21%. Leisure and hospitality and real estate/rentals come to 10% and 18% respectively. It's a diverse economy, where 7% of GDP is in finance, insurance, and information.

Hawaii is also home to a very strong real estate market, both in terms of condos as well as single-family homes. While part of the USA, the state has its own "culture" in terms of banking. A strong, low-cost long-duration deposit base that has been growing every single year - even during COVID-19.

BOH IR (BOH IR)

Among these Hawaiian banking peers, BoH stands out as the bank with the lowest loan/deposit ratio, which makes it one of the strongest and most liquid banks in the state. As of 2Q22, the company's LTD ratio was at 62%, compared to the weighted average US peer of 77% (63% for Hawaii).

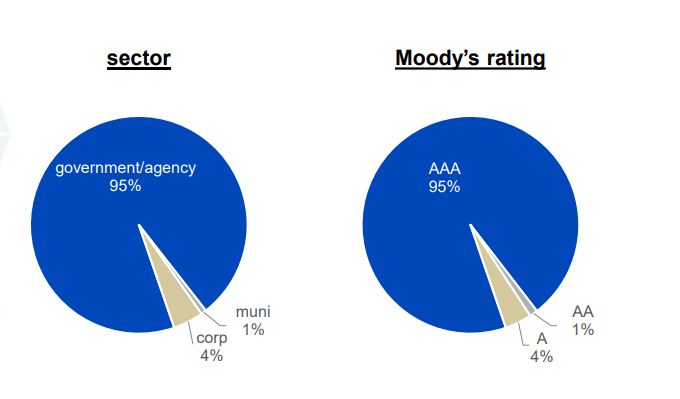

This excess liquidity is then reinvested into higher-quality, low-risk investment portfolios, most of them with AAA-rating, in terms of credit, and 95%+ of them in government/agency.

{kind=link}

Risk is not something BOH likes - not in exposures, mortgages or anything else. The company's loan portfolio is extremely well-balanced. 35% resi mortgages, 16% home equity, 27% CRE, and 10% C&I (Commercial & Industrial). The company is more overweight conservative home loans, and currently carries a total loan/lease of almost $13B, around $7.8B of which is in the consumer sector. Over 92% of the company's business is "only" in Hawaii.

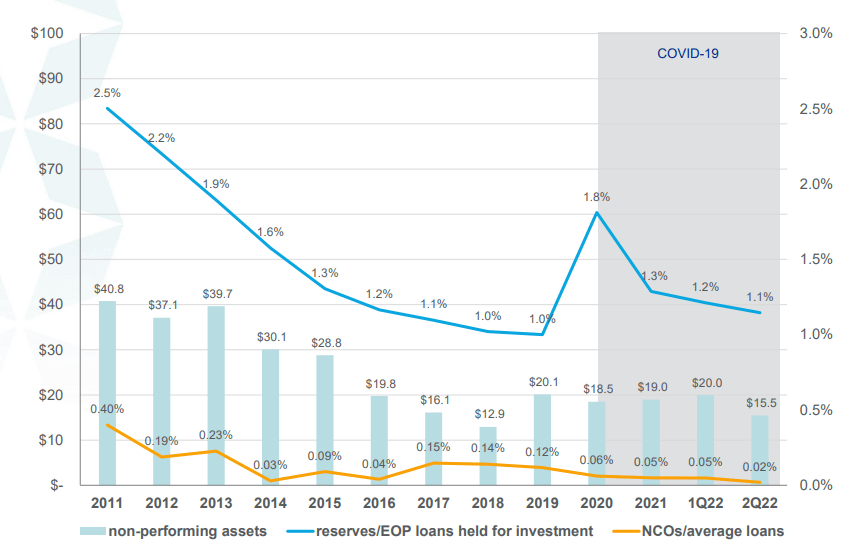

The bank has one of the lowest non-performing assets and NCOs on average loans that I've seen from a U.S. bank, down to 0.02% in NCOs/av.loans.

{kind=link}

The company doesn't have the most solid and stable history - it had years of underperformance back in conjunction with the dot-com crisis, and it left behind holdings in the international markets, Bank of Queensland specifically, back in 2001, as part of its strategic goals to focus only on its core markets, namely Hawaii, Samoa, and Guam. The company has been on a long journey to divest non-core assets for the past 20 years and more and shows a very strong, current state.

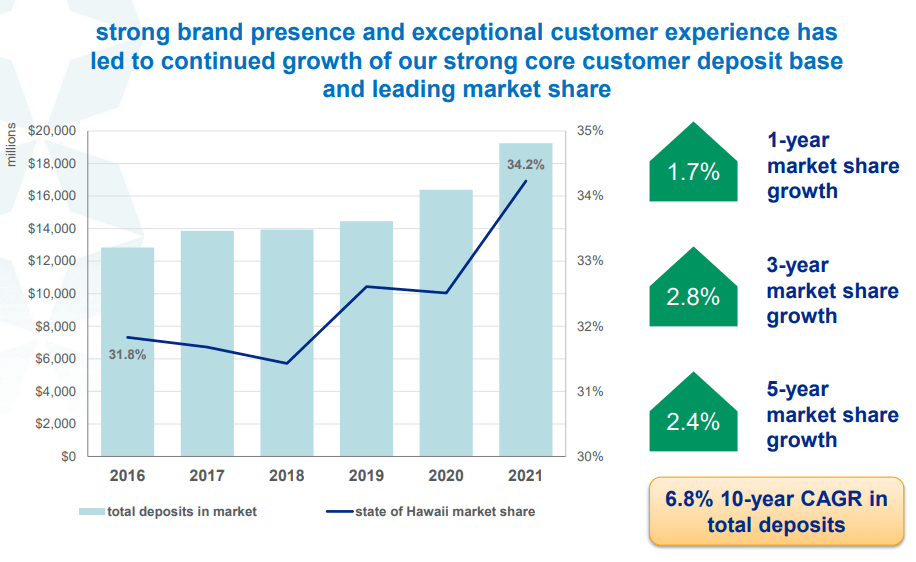

The company is without a doubt the primary bank of most people in Hawaii, with a full quarter of the population having its primary relationship with the bank. It has been growing its market share of loans from around 29% in 2016, to over 33% in 2Q22, which comes to a 4% 5-year CAGR growth, and 8.6% 10-year CAGR growth - without really losing steam in terms of non-performing loans. This is a solid track record.

The same is true for Deposit market share growth.

{kind=link}

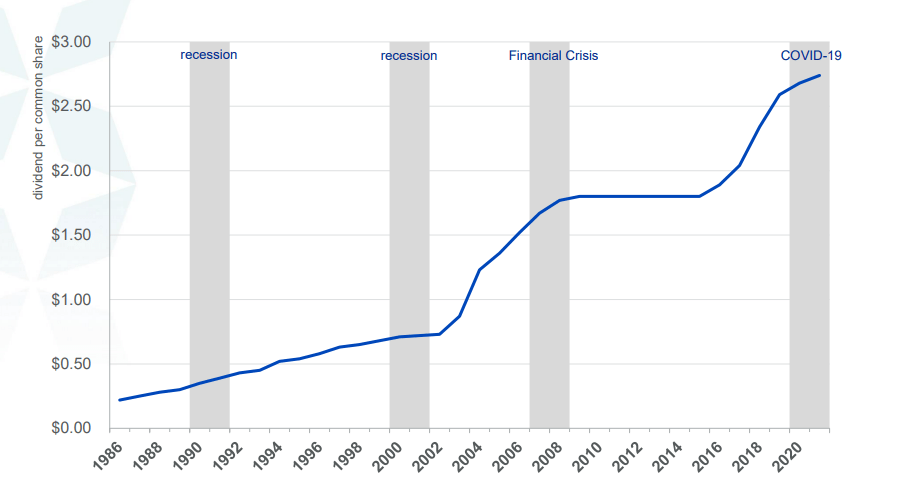

Overall impressive numbers, without a doubt, and the bank has delivered excellent overall rates of return, by looking at ROCE numbers. Even COVID-19 only slightly moved things down. Furthermore, the company yields a full 3.5% here, and that record is completely unbroken for many, many years.

{kind=link}

The Bank doesn't have a full credit rating from S&P, though Moody's gives the company's long-term issuer outlook an A2. Also, DBRS Morningstar has confirmed "A" for the bank. Moody's latest outlook for the bank is negative, but this is due to Macro from COVID-19 and what this has done to the bank's overall geography, rather than something "specific" about the bank itself.

The company's latest results echo the overall positive trend of this bank, and financial institutions in general as things currently stand. Net interest income trends, and all of the things that have been bad for finance companies in the recent past, have instead been positive as things have been moving towards higher interest rates and the like.

3Q22 is the latest set of results we have - and there is nothing that stands out here in comparison to what I'm showing you above, or what could be expected from a bank in this particular environment. The company saw loan growth at 2.9% sequentially, and a significant 12.7% increase YoY. This is balanced across both consumer and commercial categories, with over 99% sourced in Hawaii.

Deposits were down less than 0.8%, but non-interest-bearing demand deposits stayed at around 35%, and the company's LTD ratio improved to a full 64% at this time, which starts reaching some European/Scandinavian banks in terms of how stable things are.

The bank's overall split in terms of consumer and commercial will likely allow for some outperformance here. There is a lot of granularity to these deposits, with half of the company's combined sitting in account sizes of less than $0.5M each.

Unemployment in Hawaii is down to 3.5%, which means that for the first time since COVID-19 began, the state is back to the national average, and the visitor markets to the island remain strong, both from Japan and also from the US visitations.

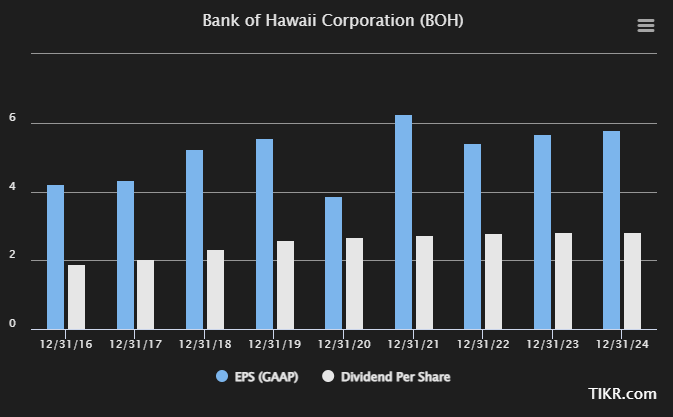

There aren't really a lot of questions or company-specific risks to consider here. The bank's results show relative overall stability and recovery from the COVID-19 pandemic, which saw the company's earnings go "low" back in the 2020 fiscal. The current trend, after the bounce-back, is for a slow growth in earnings back toward the $6/share GAAP level, and for the dividend to increase there as well.

{kind=link}

Yes, the bank missed expectations slightly. And yes, BOH is preparing, like any bank for increased delinquencies, NPL's and overall non-performing assets and holdings - but at the same time, the company is making more money per loan, and its fundamental qualities are improving. 3Q22 didn't result in a positive reaction by the market, but it's in line with what I see in the rest of the finance sector.

Let's look at how this influences the company's valuation and when we should be investing in Bank of Hawaii - if ever.

Bank of Hawaii Valuation

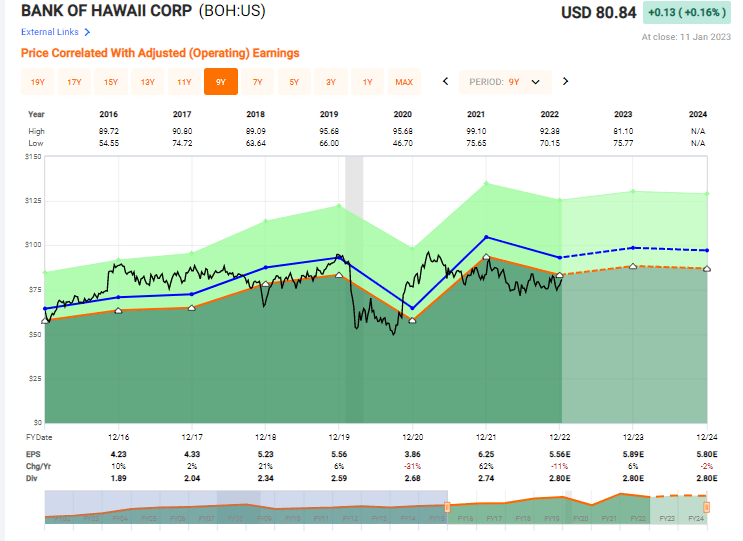

The bank's valuation is generally fairly positive - but it's also high, in terms of what we have in the sector. BoH Is a high-quality bank in the market with what I would consider being an above-average moat. However, it already trades at valuations that reflect this - and I wouldn't t assign the premium 15.5-17x P/E multiple that the market is seeing here.

To me, finance businesses are somewhat more volatile, and deserve some discounting in accordance with this. The market agrees, for since COVID-19, the company hasn't really traded close to its pre-pandemic premium, and currently comes in at 14.5x P/E.

This is still high if we look at peers.

BOH valuation (F.A.S.T graphs)

{kind=link}

Compared to other regionals, the bank is well above an average of 8-11x P/E, despite being only in the middle when it comes to overall market capitalization in its peer group.

6 analysts from S&P Global follow the bank, and they give the company a range starting at $71 and going up to $87 - a very tight range, with an average of $78. That means that the bank is currently 3.3% overvalued, and only 1 analyst considers BoH a "BUY" at this particular time. There is quite a bit implying at this time that the Bank of Hawaii is in fact somewhat overvalued here. This also includes forecasted RoR based on adjusted EPS.

If we disregard the 15x+ P/E premium a 15x P/E normalized RoR until 2024 would be around 7.08% annually, which is below what I would consider an absolute minimum for investing in a company here.

This has to do with the fact that most analysts are forecasting a double-digit compared EPS growth in 2022, which makes sense given how earnings peaked. But it also means a mixed outlook in the next two years, with non-performers compressing things down a bit, and a risk of underperformance very much still in the cards.

For myself, I would say that Bank of Hawaii trading at over $80/share is not a "BUY". What I would be looking for is a sub-$72 share price that would allow conservative outperformance - and even that is going fairly high for the bank. However, BoH has a moat, it's one of the best choices in its geography, so I'm willing to treat it much like a Swedish incumbent at this point.

At a lower valuation, the return potential for BoH is high - over 10%, with a decent yield of close to 4%.

But it's too expensive here.

Here is my current thesis on the Bank of Hawaii.

Thesis

- Bank of Hawaii is a market-leading bank in a very attractive geography. It has solid historicals, fundamentals, and a good moat given where it is located. Its near-term targets while not massively positive, show overall stability.

- At the right price, Bank of Hawaii becomes a "BUY" with an upside of over 10% annually, a safe 4%+ yield, and a company that you can hold onto with a profit for years.

- However, currently, it is too expensive.

- I give BoH a price target of $72/share and rate it a "HOLD" at this time.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I would consider it a "HOLD" based on the company not fulfilling my valuation-related investment criteria.

For further details see:

Bank of Hawaii: Banking On (One Of) The Most Isolated Places On Earth