BOH - Bank of Hawaii: Facing Weak Near-Term Earnings

2023-09-15 14:50:23 ET

Summary

- Alongside its peer group, Bank of Hawaii shares have tumbled this year due to the now well-known headwinds facing regional bank stocks.

- While the bank is sitting on large unrealized losses in its securities portfolio, the deposit franchise here has always been a positive feature.

- Overall deposit balances have been broadly stable YTD, though like its peer group higher funding costs are squeezing margins.

- Asset quality is going to become more of an issue for the industry, but Bank of Hawaii has historically been a very solid performer on that score.

- These shares are cheaper than last time out and offer a solid dividend yield, but the near-term outlook is poor.

Sometimes you have to hold your hands up and admit when you are wrong. Bank of Hawaii ( BOH ) is one I got wrong, as higher funding costs, concerns surrounding the extent of unrealized losses on its securities portfolio and general poor industry-wide sentiment have torn into these shares since my last piece back in 2022.

Down around 40% in that time on a total return basis, Bank of Hawaii's decline is a pretty good reflection of the issues it faces. While there was material concern about unrealized losses in its securities portfolio, I believe the main story here is about earnings - and the fact of the matter is that the near-term outlook is now very weak for the bank.

Most of the sector is in the same boat of course, but Bank of Hawaii's specific constitution likely makes for an extra weak loan growth outlook, and that will exacerbate the more generic funding cost issue that is currently squeezing margins. While the stock has become cheaper in terms of valuation, that mirrors to a large extent the decline in earnings and profitability that look likely over the next year or two, and lacking any near-term catalysts it's hard to see much upside to these shares over the next year or so. This led me to a Hold rating.

Deposits Relatively Stable, But Funding Costs Up Sharply

Bank of Hawaii faced some very difficult questions in the early days of the regional banking 'crisis' back in Q1. Unrealized losses on its AFS and HTM securities are ultimately running pretty close to its entire tangible book value, raising uncomfortable questions for the bank should deposits leave en masse.

That was always a bit of a doomsday scenario, though, as Bank of Hawaii's deposit franchise is solid by regional bank standards given it controls around a third of the state's overall total. It's also worth noting that around half of its deposits are through relationships lasting 20-plus years.

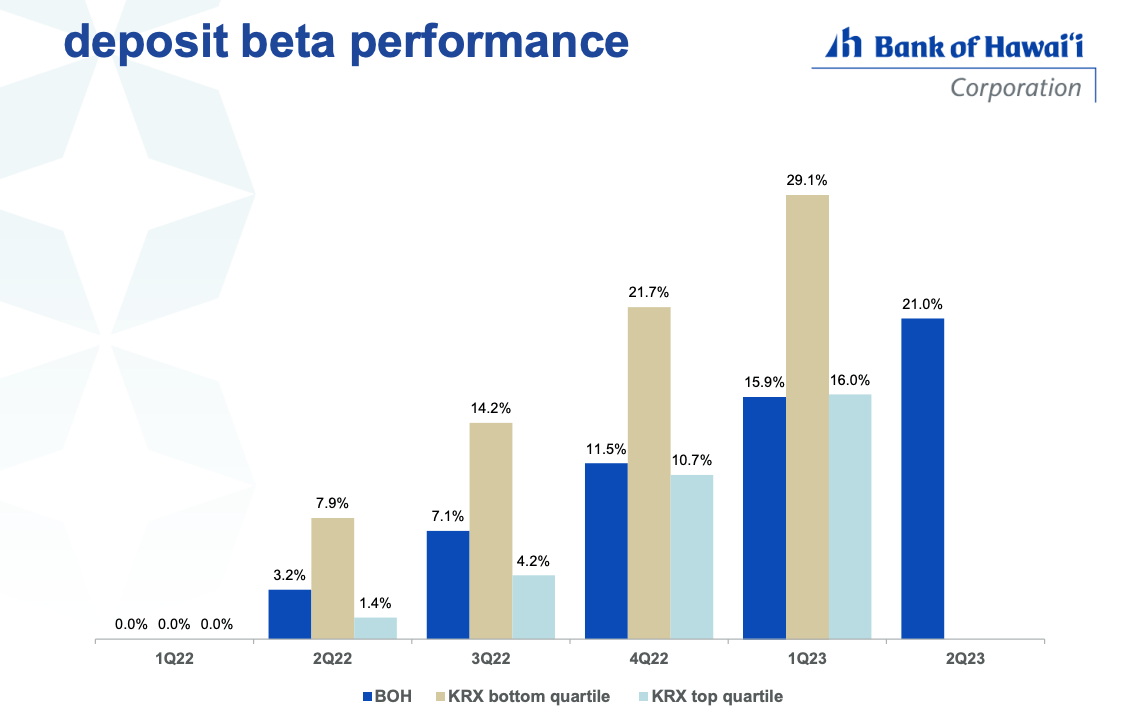

Total deposit balances have remained quite stable, falling just 0.5% YTD in H1 to a little over $20.5B. While deposit beta in the 21-22% area has been better than average, funding cost pressure remains a salient issue. Non-interest bearing deposit balances have declined to around 29% of the total (versus circa 33% at YE 2022), while time balances have increased around 50% YTD. The bank also took on around $1.25B in additional FHLB advances in H1, with that costing it around 4.3%. As a result, net interest margin fell ~38bp to 2.22% in H1 and will continue to contract in Q3 and Q4.

Source: Bank of Hawaii 2Q23 Results Release

{kind=link}

Now, most banks face the twin issue of higher funding costs and weak loan growth, but around half of the loan book here is in residential mortgages and HELOCs. Loan growth is going to be particularly weak I think, and indeed management is basically guiding for flat performance in Q3 onwards:

And what I would anticipate is, likely loan growth to be flat at this point moving forward. It just seems like the consumers slowed down a bit based on rate, seems like commercial clients are sitting on their hands a bit on transactions. Hopefully, we'll see that change as more positive signals come out of the economy, hopefully. But for now, feels reasonably muted, I think.

Peter Ho, CEO Bank of Hawaii, 2Q23 Earnings Call

While average yields may still rise as old loans roll off, higher funding costs and flat loan balances mean the overall outlook for NII and pre-provision income is pretty soft.

Credit Quality Not A Major Concern

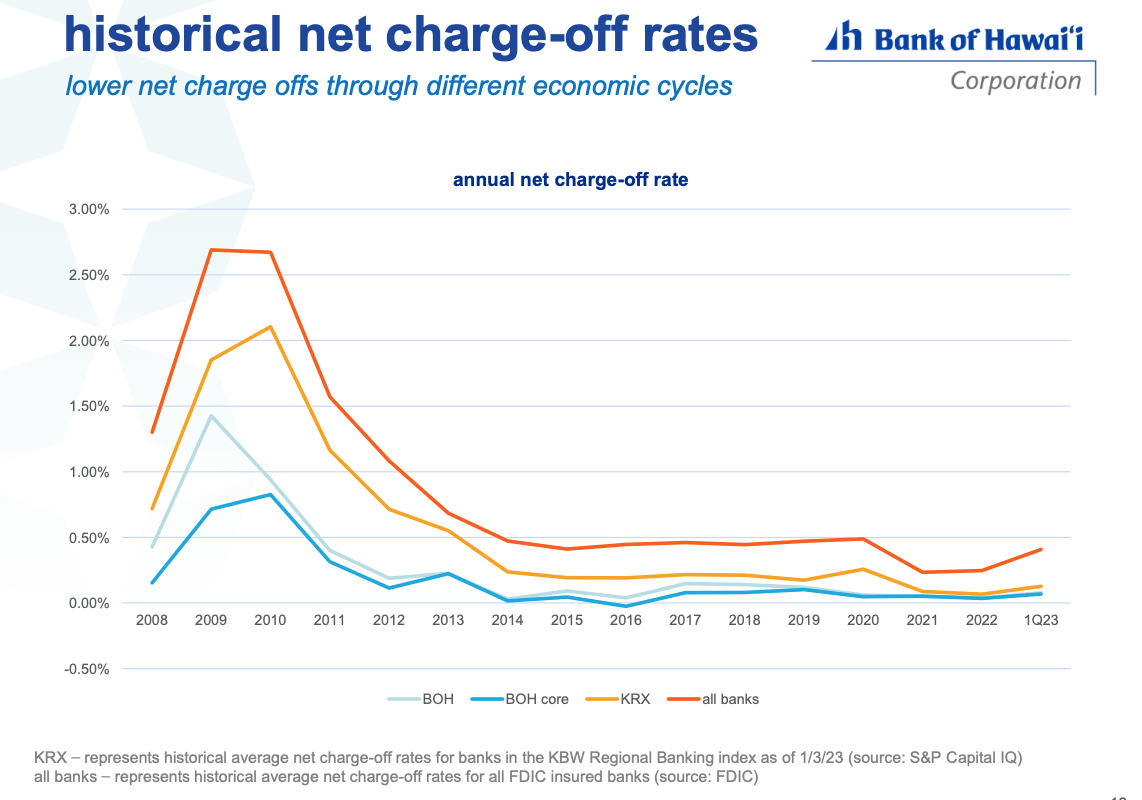

Something I am not too concerned about is asset quality. Higher loan loss provisions are a given (releases were a big earnings contributor across FY21 and FY22), but Bank of Hawaii has historically been a very good performer on credit quality, meaningfully outperforming peers in terms of net charge-offs in the last downturn and every year since.

Data Source: Bank of Hawaii 2Q23 Results Presentation

{kind=link}

In terms of where market concern currently lies, commercial real estate ("CRE") exposure is circa 26% as a portion of total loans - about average among US banks. Excluding owner-occupied non-farm, non-residential, CRE exposure falls to around 23% of total loans, though as a portion of tangible common equity (~2.8x) this is higher than average. Particular areas of concern, like office lending (~2.7% of loans; ~33% of TCE) and construction (~2% of loans; ~20% of TCE), are worth keeping an eye on.

Current asset quality metrics remain very strong, with non-performing assets (~0.08% in Q2) and net charge-offs (0.04%) yet to meaningfully tick up. I'd also note that the current allowance for loan losses (~1% of gross loans) remains above peak charge-off rates in the last financial crisis, and that annual pre-provision income, though currently being squeezed, is also running at around 1.8% of gross loans to absorb potential bad debt.

Shares Are A Better Value But Lacking Near-Term Drivers

Bank of Hawaii stock trades for $50.15 at the time of writing, putting it around 1.75x tangible book value ("TBV"). On a P/E basis, the stock trades for 12x and 13.8x consensus FY23 and FY24 estimates respectively.

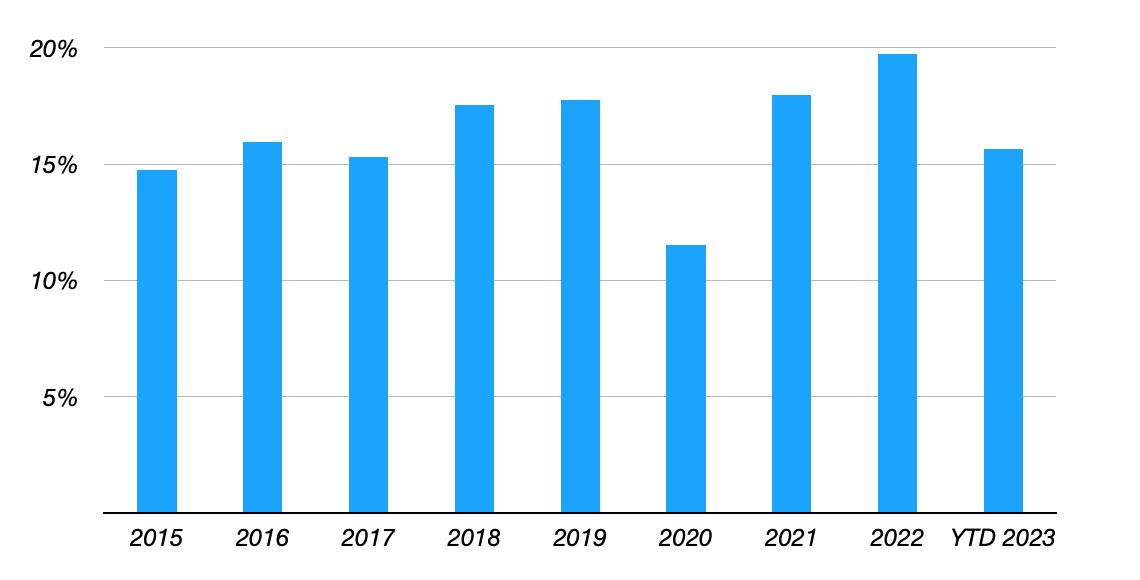

That may not look all that cheap, but note the bank's recent historical average return on tangible equity lands at around 16%. Even diminished FY23/FY24 EPS estimates would be good for an average 14% ROTE if accurate.

Bank of Hawaii: Return on Tangible Common Equity

Data Source: Bank of Hawaii Annual Results Releases

{kind=link}

Relative to its 10-year average P/E and P/TBV ratios, current multiples represent substantial discounts:

While I do think the above makes the stock an okay option for long-term buy-and-hold type accounts, near-term drivers are distinctly lacking. At the end of the day investment returns are driven by three factors: EPS growth, valuation multiple contraction/expansion, and dividend payments to shareholders. On the first, there's a reasonable chance that earnings - both net income and before provisioning - will decline year-on-year in both FY23 and FY24, and that also means that multiple expansion in the near term is a hard sell. That leaves the dividend which, although offering a decent 5.6% yield, is unlikely to grow in the near term given both the poor earnings outlook and management's desire to build capital. With short-term Treasury yields currently in the same ballpark area in terms of yield, investors could probably afford to watch this name from the sidelines for the next year or so. Hold.

For further details see:

Bank of Hawaii: Facing Weak Near-Term Earnings