BOH - Bank Of Hawaii: Outlook Of Earnings Recovery Appears Priced-In

Summary

- Anticipated improvement in passenger arrivals and unemployment rate bodes well for loan growth.

- Margin expansion will be limited by the suboptimal asset and liability positioning.

- The December 2023 target price suggests a small downside from the current market price. Further, BOH is offering a low dividend yield.

Earnings of Bank of Hawaii Corporation ( BOH ) will likely recover this year after most probably dipping in 2022. Hawaii's economy will drive loan growth, which will, in turn, play a key role in earnings growth. Further, slight margin expansion will support the bottom line. Overall, I'm expecting the Bank of Hawaii to report earnings of $5.31 per share for 2022, down 15%, and $5.72 per share for 2023, up 8% year-over-year. The December 2023 target price is below the current market price. Based on the total expected return, I'm maintaining a hold rating on the Bank of Hawaii Corporation.

Hawaii’s Satisfactory Economic Condition Will Likely Sustain Loan Growth

Bank of Hawaii's loan growth continued to remain strong during the quarter that ended September 2022. The portfolio grew by 8.9% during the first nine months of 2022, or 11.8% annualized, which is the highest growth since 2016. In my opinion, the Bank of Hawaii can have a further few strong quarters before the growth rate subsides to a more normal level. Hawaii's economy is currently very strong, which will likely keep loan growth elevated in the near term.

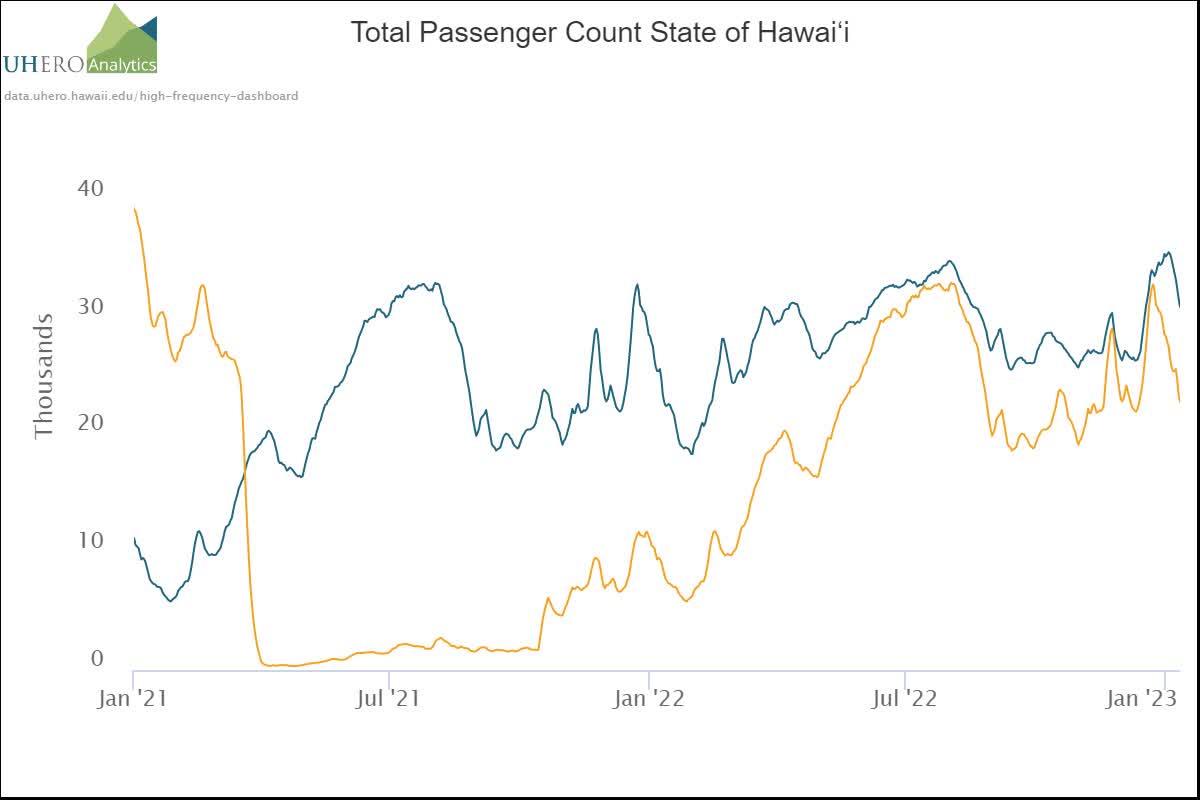

The elevated passenger count shows that the state's tourism industry is doing quite well. The following chart shows how the current passenger count is higher than last year's passenger count. (Note: the blue line is current while the orange line is lagged by one year. The gap between blue and yellow lines shows how much better the current value is relative to a year ago period.) University of Hawaii Economic Research Organization (“UHERO”) expects total passenger arrivals by air to rise by 4.1% in 2023, as mentioned in its December forecast release .

{kind=link}

Further, the state's unemployment rate is currently very low compared to both the national average and the state's history. UHERO expects the unemployment rate to drop even further in 2023 relative to 2022.

Considering these factors, I'm expecting the loan growth to have remained elevated at 2% in the last quarter of 2022, taking full-year loan growth to 11%. For 2023, I'm expecting loan growth to moderate to around 6%. Meanwhile, I'm expecting deposits to grow somewhat in line with loans. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22E |

| FY23E |

| Net interest income |

| 486 |

| 498 |

| 496 |

| 497 |

| 544 |

| 610 |

| Provision for loan losses |

| 13 |

| 16 |

| 118 |

| (51) |

| (4) |

| 20 |

| Non-interest income |

| 169 |

| 183 |

| 184 |

| 171 |

| 153 |

| 149 |

| Non-interest expense |

| 372 |

| 379 |

| 374 |

| 394 |

| 419 |

| 438 |

| Net income - Common Sh. |

| 220 |

| 226 |

| 154 |

| 250 |

| 211 |

| 227 |

| EPS - Diluted ($) |

| 5.23 |

| 5.56 |

| 3.86 |

| 6.25 |

| 5.31 |

| 5.72 |

| Source: SEC Filings, Author's Estimates(In USD million unless otherwise specified) |

In my last report on the Bank of Hawaii, which was published in June 2022, I estimated earnings of $5.33 per share for 2022. My updated earnings estimate is a bit lower because the non-interest income reported for the third quarter missed my previous expectations.

My estimates are based on certain macroeconomic assumptions that may not come to fruition. Therefore, actual earnings can differ materially from my estimates.

The Current Market Price is Above the Year-End Target Price

Bank of Hawaii is offering a dividend yield of 3.5% at the current quarterly dividend rate of $0.70 per share. The earnings and dividend estimates suggest a payout ratio of 49% for 2022, which is in line with the five-year average of 50%. Therefore, I’m not expecting an increase in the dividend level.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value the Bank of Hawaii. The stock has traded at an average P/TB ratio of 2.37x in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| Average |

| TBVPS - Dec 2023 ($) |

| 26.4 |

| 26.4 |

| 26.4 |

| 26.4 |

| 26.4 |

| Target Price ($) |

| 52.1 |

| 57.4 |

| 62.7 |

| 68.0 |

| 73.3 |

| Market Price ($) |

| 80.6 |

| 80.6 |

| 80.6 |

| 80.6 |

| 80.6 |

| Upside/(Downside) |

| (35.3)% |

| (28.8)% |

| (22.2)% |

| (15.7)% |

| (9.1)% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 15.3x in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| Average |

| EPS 2023 ($) |

| 5.72 |

| 5.72 |

| 5.72 |

| 5.72 |

| 5.72 |

| Target Price ($) |

| 76.0 |

| 81.7 |

| 87.4 |

| 93.1 |

| 98.8 |

| Market Price ($) |

| 80.6 |

| 80.6 |

| 80.6 |

| 80.6 |

| 80.6 |

| Upside/(Downside) |

| (5.7)% |

| 1.3% |

| 8.4% |

| 15.5% |

| 22.6% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $75.0 , which implies a 6.9% downside from the current market price. Adding the forward dividend yield gives a total expected return of negative 3.4%. Hence, I’m adopting a hold rating on the Bank of Hawaii Corporation.

For further details see:

Bank Of Hawaii: Outlook Of Earnings Recovery Appears Priced-In