FBK - Bank of Hawaii: Time For A Downgrade After A Fantastic Move Higher

2024-01-20 09:35:01 ET

Summary

- Bank of Hawaii stock has outperformed the broader market, up 38.5% compared to the S&P 500's 19.5%.

- Deposits at the bank have grown, but the increase in uninsured deposit exposure poses a risk.

- The bank's overall loan portfolio has grown, but revenue and profitability have declined, and the stock is overpriced compared to peers.

Centuries of investment wisdom, combined with my own personal experiences, have led me to realize that some of the greatest investment opportunities occur during periods of tremendous uncertainty. When it seems as though the world is falling apart, that is when stocks are discounted the most. It was the banking crisis that occurred early last year, for instance, that led me to wade into that sector in a way that I hadn't before. One of the companies that I ended up assigning a ‘buy’ rating to in late March of that year was Bank of Hawaii ( BOH ).

At that time, based on the fundamental health of the enterprise, I concluded that shares had been unjustifiably punished. In response, I ended up rating the bank a ‘buy’ to reflect my view that the stock would likely outperform the broader market for the foreseeable future. Since then, shares have done precisely that. As of this writing, the stock is up 38.5% in sense the aforementioned article that I wrote about it. By a comparison, the S&P 500 is up only 19.5%. Fast-forward to today, however, and my mindset on the matter is changing. Although the deposits at the institution have finally reversed course and are growing once again, the stock has gotten a bit pricey. Add on top of this high amounts of uninsured deposit exposure, and I do believe it is time for a downgrade to something more realistic like a ‘hold’.

The picture is mixed but mostly positive

Back when I wrote about Bank of Hawaii in March of 2023, we only had financial data for the company extending through the 2022 fiscal year . Having said that, we also had some other data provided by management in response to all the turmoil that enveloped the banking sector at that time. Some of that data extended through most of the first quarter. Today, our data now extends through the third quarter of 2023 . And in some respects, the picture has gotten better, while in other respects it has gotten worse.

{kind=link}

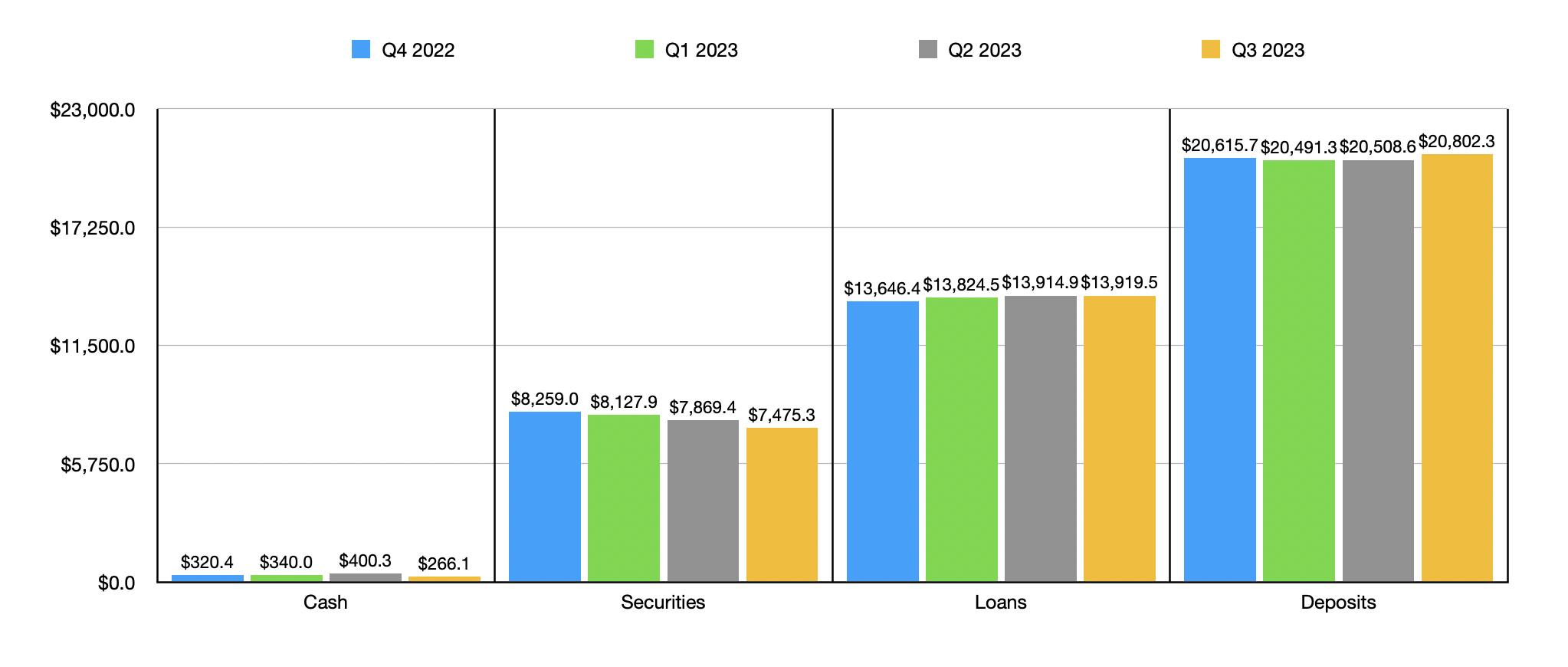

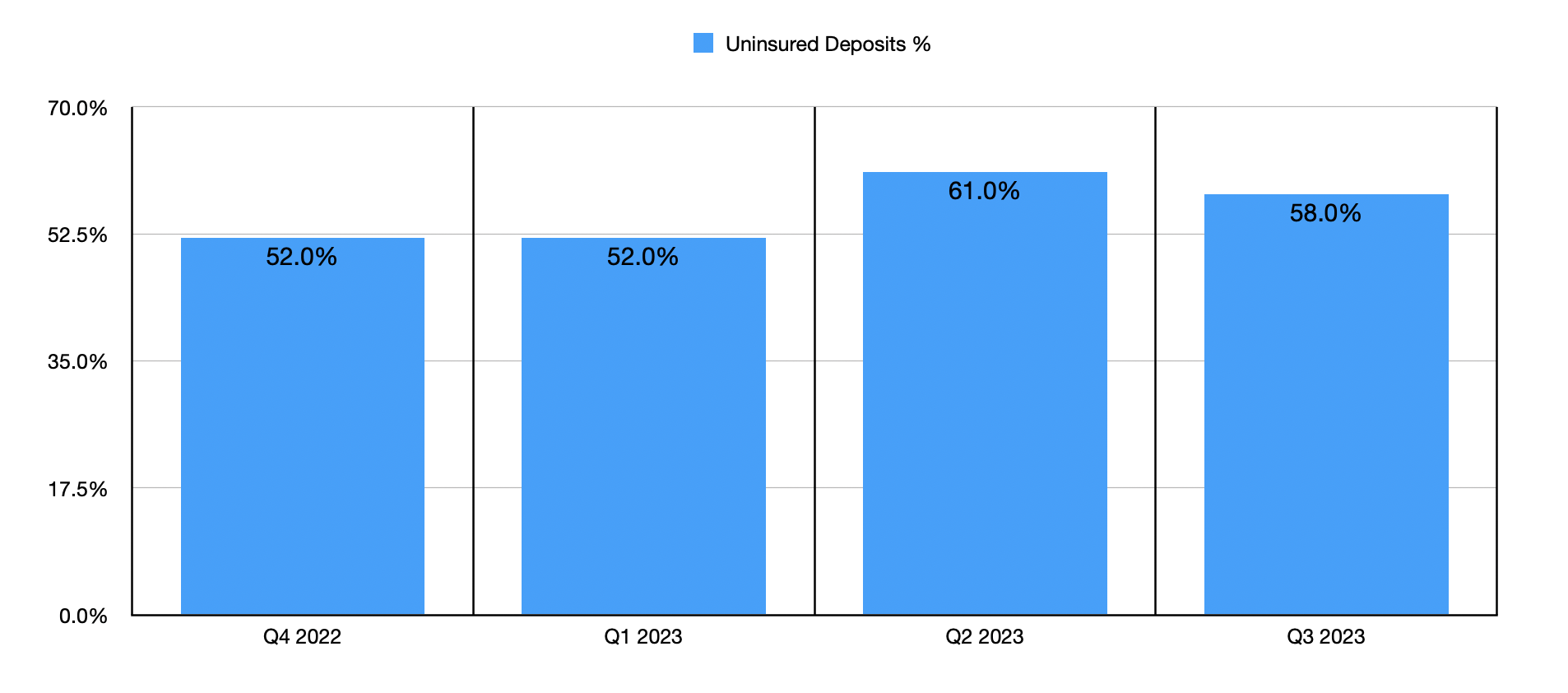

As an example of the picture improving, we need only look at the value of deposits at the institution. At the end of 2022, Bank of Hawaii had $20.62 billion worth of deposits. However, by the end of the first quarter, deposits had dipped by $124.4 million to $20.49 billion. Compared to many other institutions at that time, this was not that bad of a decline. What made the picture problematic, however, is that a large chunk of its deposits were classified as uninsured. That number came out to 52% at the end of the first quarter. Since then, the value of deposits have resumed growth and, as of the end of the third quarter of last year, totaled $20.82 billion. However, the downside to this is that uninsured deposit exposure has since grown to about 58%. That does make the bank carry more risk than I would normally like.

{kind=link}

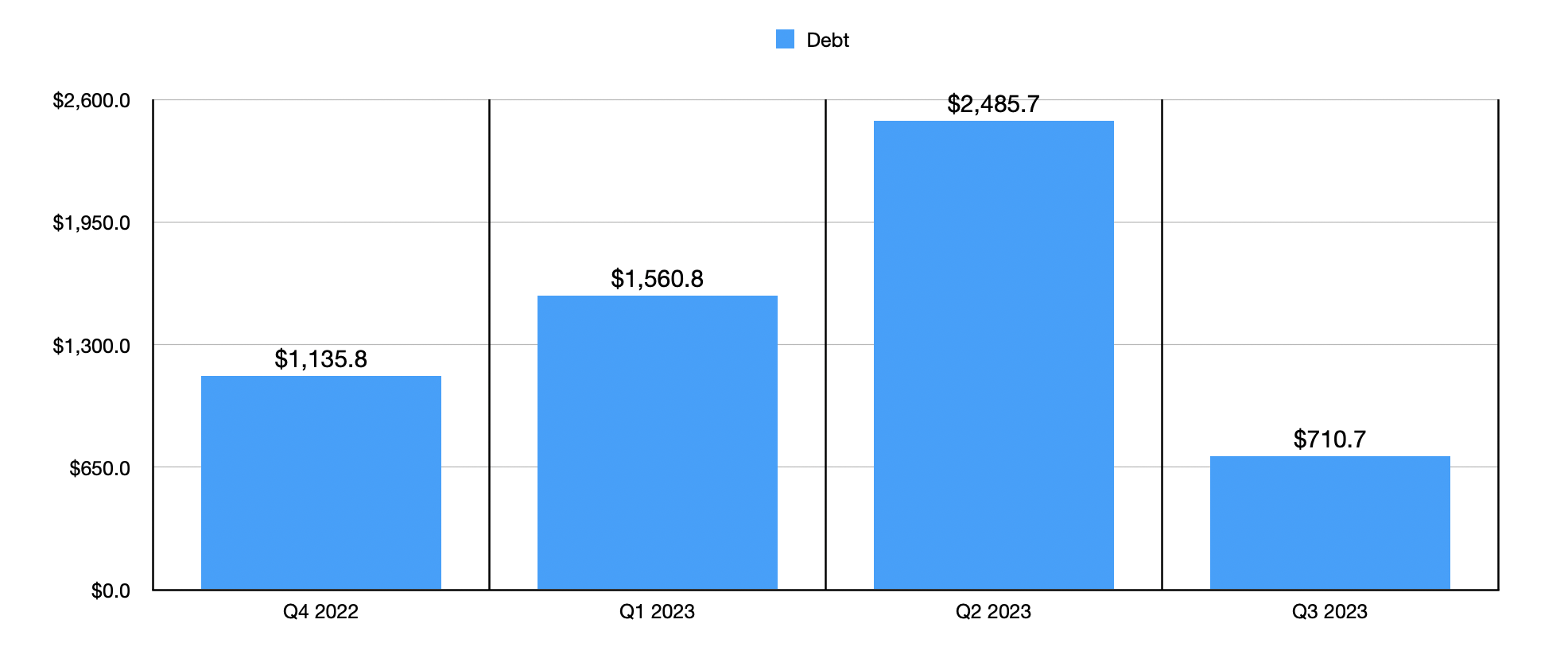

Another positive that we should rejoice in is a growth in the overall loan portfolio of the institution. Despite high interest rates, management has been successful in doling out capital. At the end of 2022, the bank had $13.65 billion worth of loans. This number has grown every quarter since then, eventually hitting $13.92 billion by the end of the third quarter. Debt over the same window of time has also improved. After spiking from $1.14 billion in 2022 to $2.49 billion at the end of the second quarter of last year, the level of debt on the company's books plunged to only $710.7 million by the end of the third quarter.

{kind=link}

On the downside, however, we do have some other data that is discouraging. The value of securities on the company's books, for instance, continue to drop. This was likely in response to management paying down debt. Total securities at the end of 2022 were $8.26 billion. And every quarter since then, that number has declined. As of the end of the most recent quarter, it came in at $7.48 billion. Cash has followed a similar trajectory. After peaking at $400.3 million in the second quarter of last year, it has dropped to $266.1 million. That's down from the $320.4 million reported at the end of the 2022 fiscal year.

{kind=link}

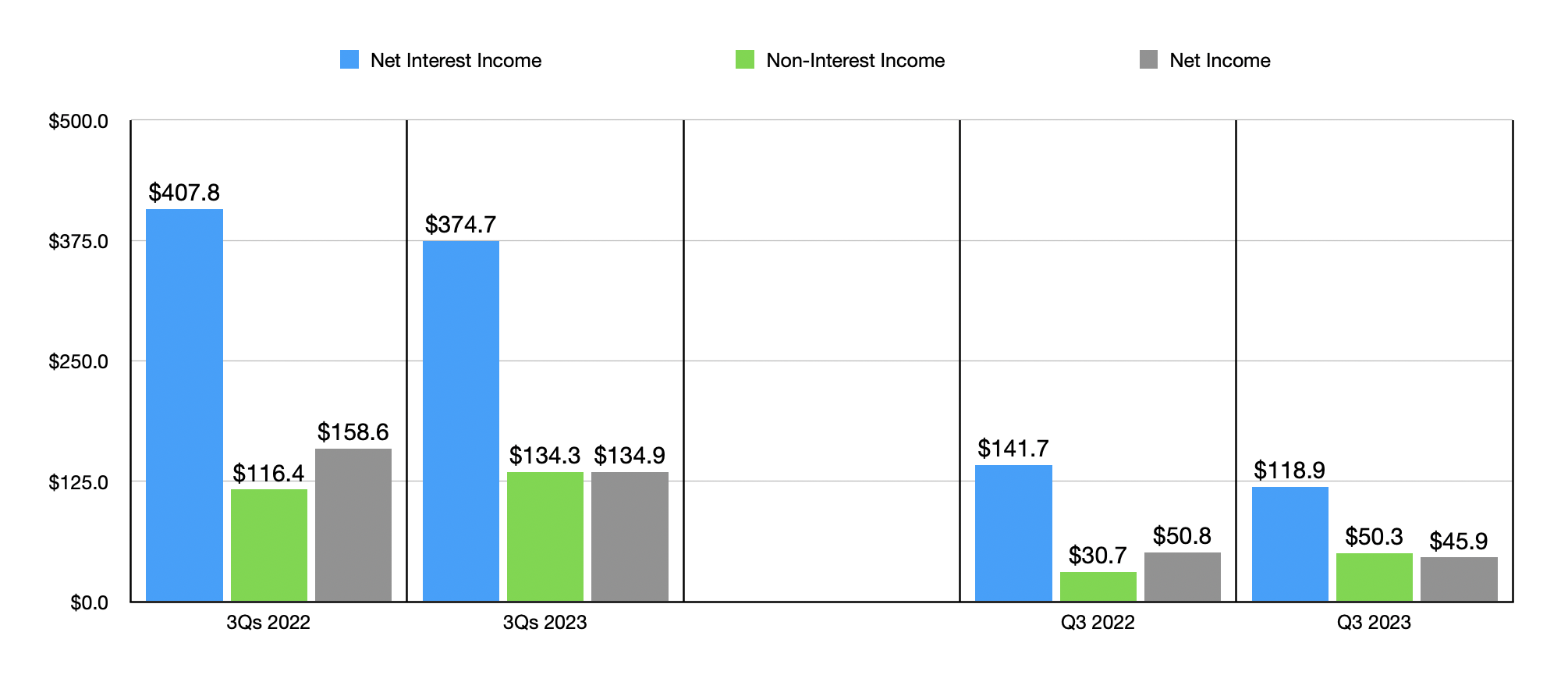

Another area of weakness that has emerged as of late has been when it comes to revenue and profitability. As you can see in the chart above, net interest income and net profits for the institution both declined year over year for the first nine months of 2023 in their entirety and even when focused on the third quarter on its own. In addition to the reduction in securities hurting the company, the firm also suffered from a drop in its net interest margin from 2.60% to 2.13%. This was caused in part by a growth in deposits, as well as the necessity of the company paying out more in order to keep funds in the bank.

{kind=link}

{kind=link}

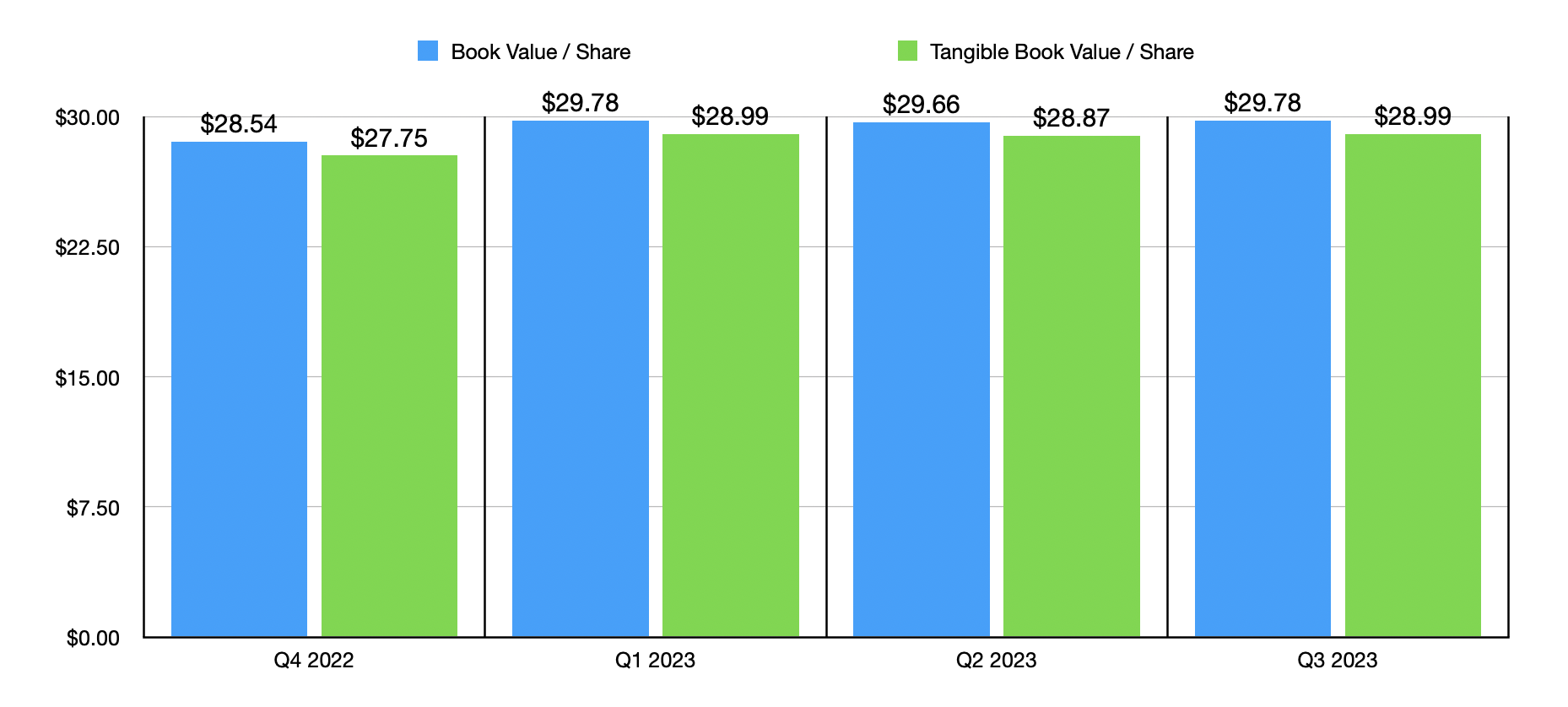

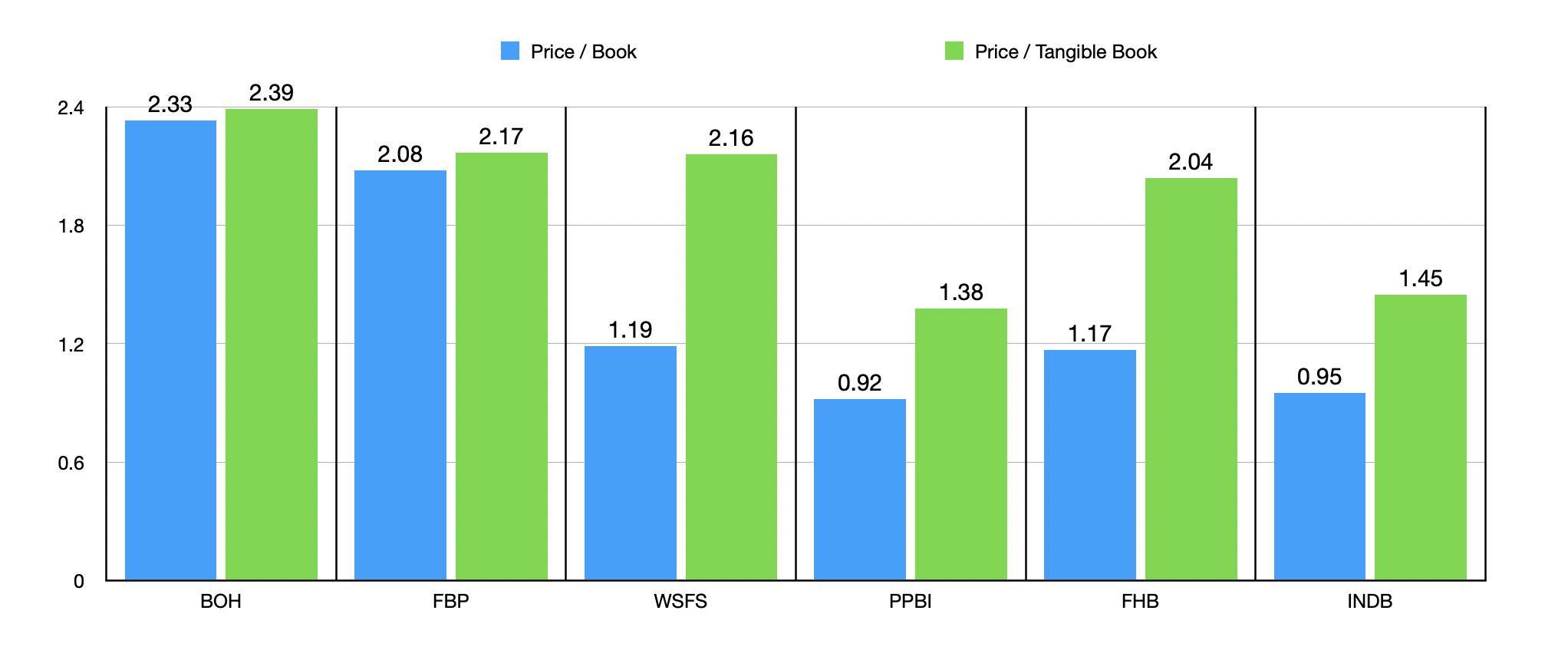

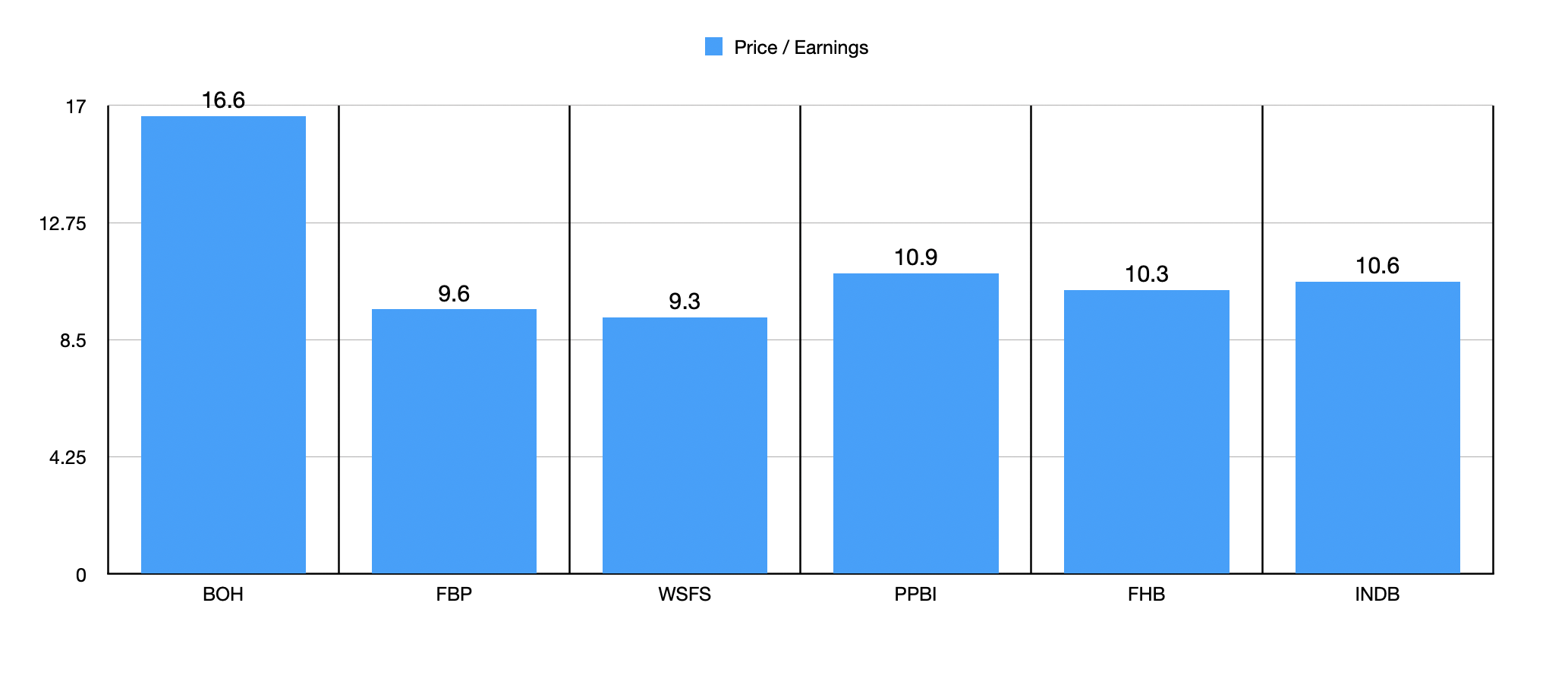

Despite the negatives, I am happy to see that the book value and tangible book value, both on a per share basis, for the company managed to continue growing quarter after quarter. The increases were not much, amounting often to just a few cents per share on a sequential basis. But the general trend is positive, and it indicates accumulated value on behalf of shareholders. Unfortunately, investors are having to pay quite a bit for that value. At present, the company is trading at 2.33 times its book value and 2.39 times its tangible book value. In the chart above, I compared the firm to five similar companies using the price to book and price to tangible book values. What I found was that, in both instances, it had become the most expensive of the six enterprises. Then, in the table below, I decided to look at the picture through the lens of the price to earnings approach. If analysts are correct about earnings for the fourth quarter of the 2023 fiscal year, then net profits should be around $167.1 million for the year in its entirety. That translates to a price to earnings multiple of 16.6. As the chart below illustrates, this is well above what other players are trading for at this time.

{kind=link}

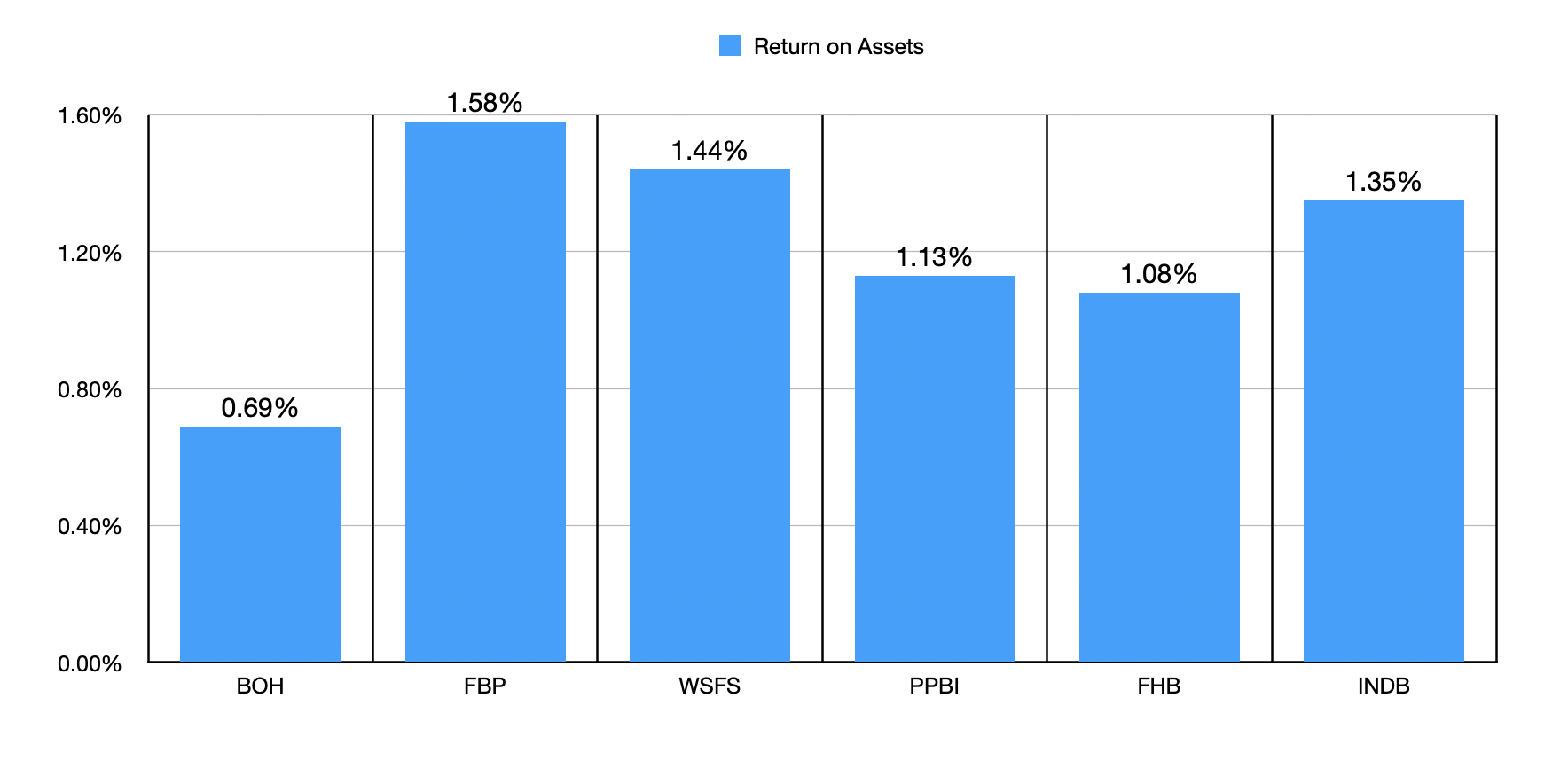

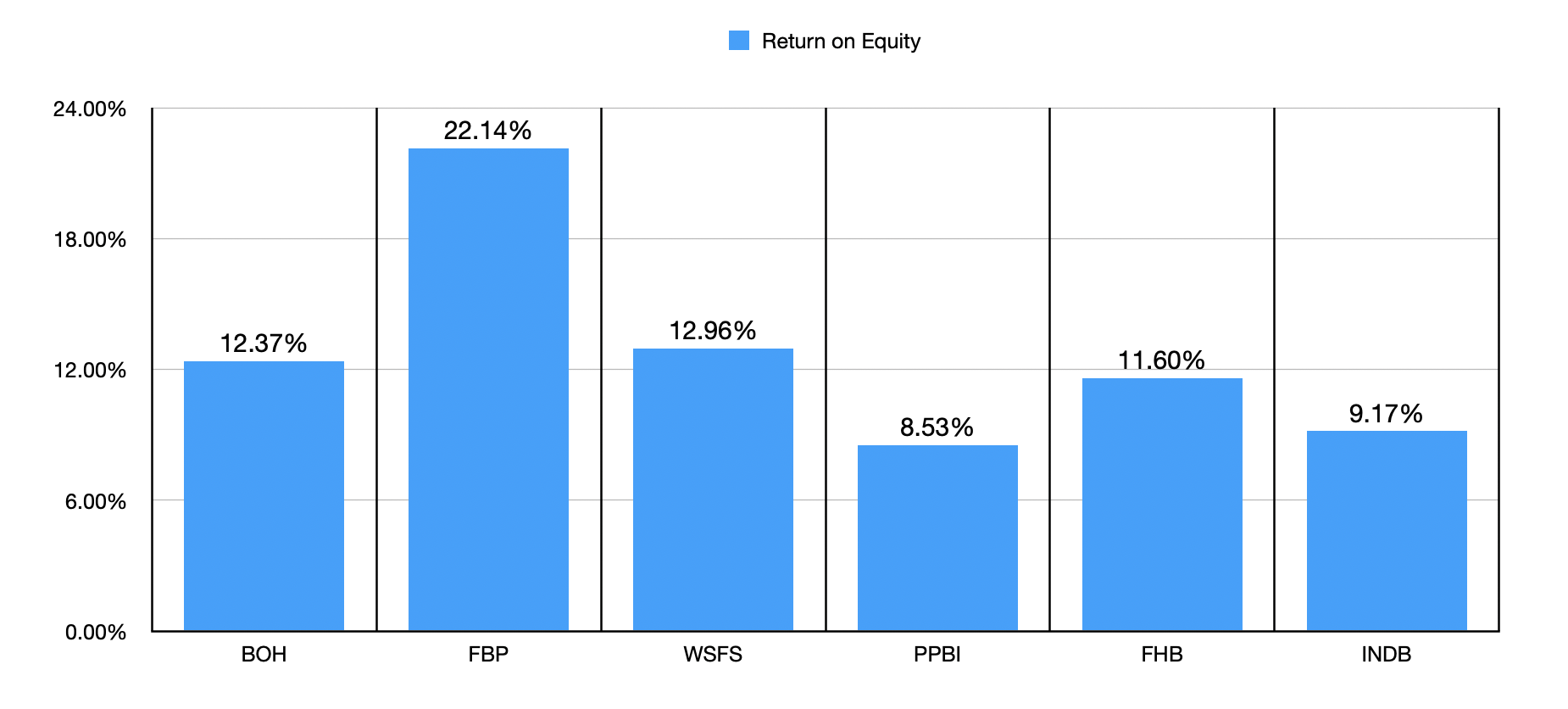

I think an argument could be made that a healthier institution might warrant a premium over its peers. But that doesn't appear to be the case either. In the first chart below, you can see the return on assets for Bank of Hawaii, as well as for the five companies i decided to compare it to. It actually has the lowest reading at only 0.69%. Fortunately, the company is a little more competitive when it comes to the return on equity picture. With a reading of 12.37%, only two of the five companies were higher than it.

{kind=link}

{kind=link}

It is important to note that the picture can change, perhaps even for the better, and the best time for a change to be revealed would be when the firm in question reports financial results. Later this month, on January 22nd, management is expected to announce financial results for the final quarter of the 2023 fiscal year. But if analysts have any say in the matter, the picture will be somewhat disappointing. I say this because they are currently forecasting revenue of $160.4 million. That's down from the $181.9 million reported the same time of the 2022 fiscal year. The company is also forecasted to generate $0.81 per share in profits. That's little better than a 50% cut from the $1.50 per share the business reported for the same quarter of 2022. That would bring net profits down from $59.3 million to $32.2 million.

Takeaway

From all that I can see, Bank of Hawaii is a fine institution, but it's not a great prospect anymore. We have seen some continued weaknesses and shares have gotten quite pricey compared to where they were when I wrote about the business those several months ago. If management comes out with some big surprise for fourth quarter earnings, that picture might ultimately change. But leading up to that point, I don't have enough hope to justify keeping the bank rated a ‘buy’ at this time, so I have decided to downgrade it to a ‘hold’.

For further details see:

Bank of Hawaii: Time For A Downgrade After A Fantastic Move Higher