BOH - Bank of Hawaii: Worth Buying In The Crisis?

2023-03-29 14:34:01 ET

Summary

- Bank of Hawaii is a bank I've written about once in the last few months, highlighting some of its operational advantages and why one could invest here.

- It's one of the more significant banks in Hawaii, and is a good investment at the right price, provided fundamentals don't change too much.

- In this article, we'll review recent events and see whether the bank, after its 4Q, the banking crisis, and other headwinds, is still a good bank.

Dear readers/followers,

In this article, I'll be providing an update on The Bank of Hawaii ( BOH ), post-bank crisis. I wrote about this company a few months back, and reported on this company's advantages and positives - and there are some to consider. Right off the bat, I can tell you that the Bank of Hawaii is currently in a position of being significantly undervalued - so if the fundamentals hold up, that's something to consider.

We haven't seen the company at this price for over 2 years - so let's update for FY22 and 4Q and see if the bank can hold up in today's environment.

Bank of Hawaii - Updating post-crisis

Bank of Hawaii remains in a relatively unique position due to its geographical exposure - or rather, the lack of it. The bank has a very exceptional deposit base. Alternatives are either lower quality or few, so customers in Hawaii are unlikely to shift things around significantly, even in this sort of environment. The company has significant liquidity to tap, and the company's operating market means that there are some high-quality assets backing BOH up.

How good is BOH?

The company is rated Aa3 by Moody's for long-term deposits. This is the highest in Hawaii, and one of the highest in all of the United States.

It's also been named "Hawaii's best bank" for 12 years consecutively while also being simultaneously ranked in the top 3 among the most trusted companies in the banking industry by Newsweek.

The bank has one of the best histories in the US - 125 years of it, developing a superb deposit base and building relationships across the islands. As with all island territories, this is a unique marketplace.

You probably won't see BOH growing fast. The Island doesn't really support massive growth - it's an established and mature market, meaning aside from market share growth and GDP-like growth, things are going to be steady here. Deposit growth since 2012 after the GFR, is at 5.9% CAGR, and balances remain very steady.

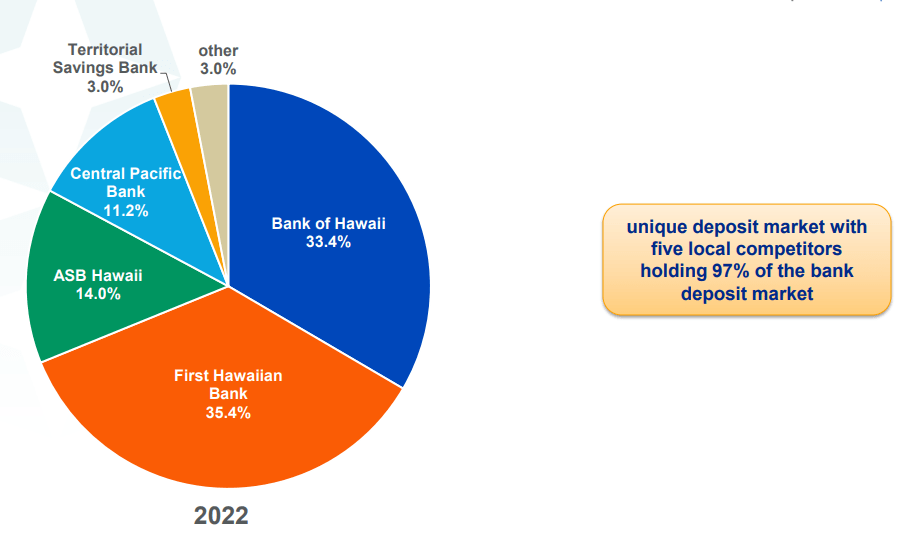

Remember, this is a very unique deposit market. It looks like this:

{kind=link}

As you can see, there's really only one major competitor to this one - and it's only marginally larger in terms of market share compared to BOH.

As you go through the company's 10-Ks and filings, you notice the sheer differences between this bank and other US mainland banks involved in the recent financial instability.

Over 98% of the company's depositors are fully FDIC-insured. 48% of the company's balances are FDIC insured, and the average consumer balance is $18,000, with commercial at $134,000. Unlike SVB or other banks involved in this instability which had the majority of their money in large piles belonging to a few customers, BOH's deposits belong to hundreds of thousands of consumers across the islands, each insured and "safe" overall.

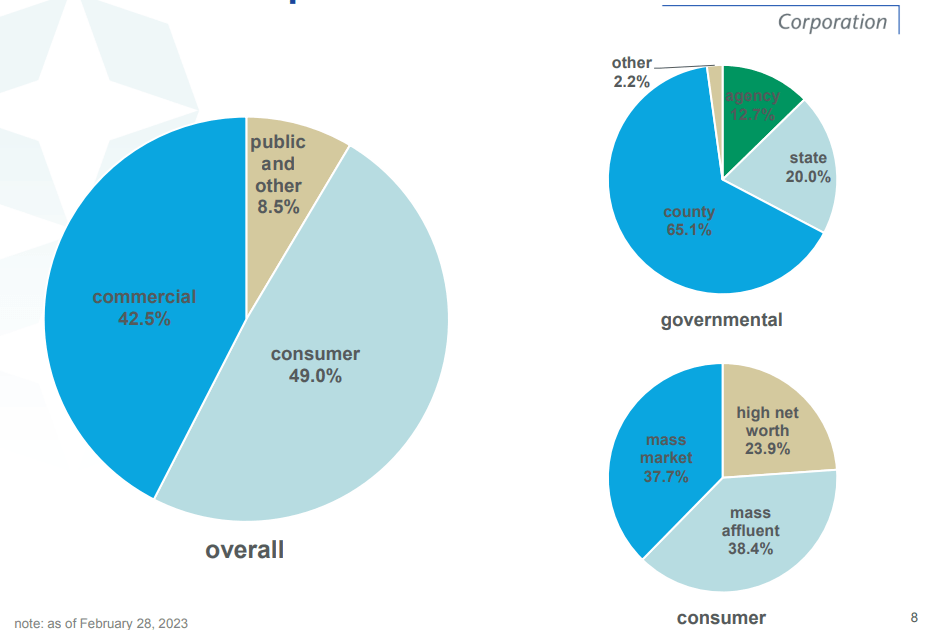

Take a look at the depositor mix.

{kind=link}

This diversification also reaches beyond the mix, but also to where these commercial customers work. Much in real estate, finance, healthcare, accommodations, title companies, retail, but no one segment over 17%, and only 2 over 10%.

Bank of Hawaii is one of the most diversified banks I've encountered when reviewing the US banking sector.

What's more, very low amounts of the company's business are interest-bearing in terms of demand. With 40% savings, and 31.2% non-interest-bearing demand, BOH appears more insulated from movements and volatilities compared to other banks.

Most of its deposit base is well over 20 years in terms of the age of the account/deposit, and in the public sector, deposits and accounts are 91% at 20-year account age or higher. The company also has a borrowing capacity of over $10B and pledged assets, making it extremely safe in my view. All of these facts bear reiteration when looking at the fallout from the banking crisis.

Why?

Because the Bank of Hawaii, like many other US banks, fell significantly over the past few weeks. In one month, the bank is down almost 32%.

That's a massive drop given that the company isn't actually that affected by this.

Now, it's true. BOH isn't the fastest growing, not the most profitable bank in the US. But its yield at this time is 5.5% and currently trades at a price of $51/share. Most of the company's upside is in the value/valuation that we get for our money - and more on that in a bit.

The company reported its 4Q in January, and results were in line with high-level expectations for the bank - not massive, outsized growth, but growth. Loans were up 2.4%, but almost 11.3% YoY in both commercial and personal businesses, while deposits were up 1.3% YoY. The company didn't see any massive expense increase with excellent overall credit quality at a high level, and RoCE at 21.3%. The instability we've seen in the rest of the sector hasn't really spread massively to the islands of Hawaii. Employment continues to rise and outperforms the market on a national average - it was higher than the national for the 29th consecutive month. And visitors continue coming to the islands as well.

We are heading into a more volatile environment for Hawaii as well - no doubt about that, and asset values in Hawaii may be tested by the higher rates we've since moved into. Seeing the bank's 1Q23 will be interesting because it will give us a preliminary look at the first part of the year.

The only real worries that I see, or would be looking at, would be the loan growth rate and deposit growth rate going forward in the next few quarters as the rate effects and macro effects start hammering home. This would impact the bank's overall growth rate.

However, all of these worries are small next to what I believe matters for this bank.

Namely, that Bank of Hawaii is currently seeing lower returns and margins than it historically has, but they're still high. It has better capital safety ratios than peers, and at a 5.5% yield, the stock is at a level that we typically don't see with this bank.

The valuation for the Bank of Hawaii

BOH is a bank with a market cap of around $2B, making it one of the smaller US banks I look at. However, it's one of two major players on the islands of Hawaii. The main challenge with this bank is its expected EPS growth rate, which based on current macro trends is actually negative, expected to decline 3-5% for the next few years.

Why invest in a bank that isn't expected to grow earnings, you might ask?

Well, the banking crisis has caused the bank to drop significantly. In my last article, I made a case for why the bank is a clear "HOLD". The company's performance since that article has obviously been stellar - no questions there, even if the market has not reflected this performance in the share price.

Seeking Alpha BOH (Seeking Alpha)

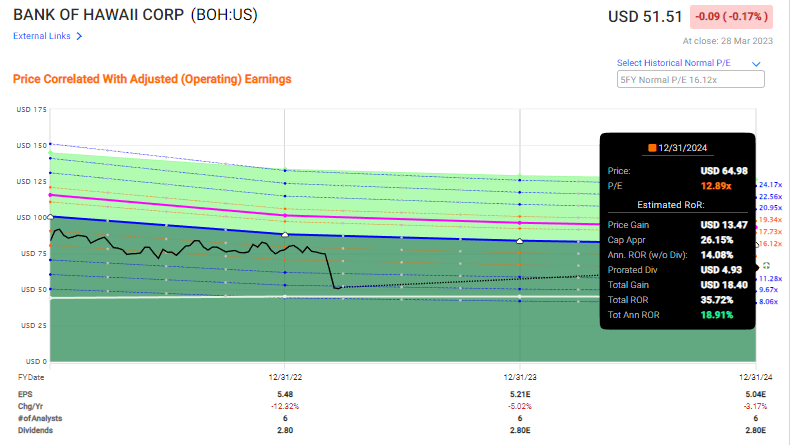

At a price of almost $50/share, I believe this bank has an upside even without growth and even trading well below its overall average. The bank average is at around 15-16x P/E, which we shouldn't allow for when it declines. So I'll put it at 12-13x P/E - which still gives us a significant, near 20% annual upside for the company.

Bank of Hawaii Upside (F.A.S.T graphs)

{kind=link}

The company doesn't have the same sort of conservative safeties and credit ratings we find in larger banks - but as mentioned before, the deposit safeties here appear to be stellar - so I wouldn't worry about the lack of an S&P Global CR.

The S&P Global analysts, 6 of them, still haven't changed their tune on the company despite cutting the average target from $77 to $68/share - that's from a range of $55 low and $83 high, by the way. But still, those analysts are giving the company no more than a "HOLD", with only one analyst at a "BUY", despite the current price being over 33% below their average PT. But I think they're wrong, and I'm going to change my rating on BOH from a "HOLD" to a "BUY".

The company is a "BUY" for one reason - its value/price, relative to what it offers, is well below where it should be. Even in the case of sub-par performance, this bank should, based on its operating geography and its safety, come out on top - and shareholders seem likely to as well in my view.

Shareholders will be compensated at the very least with a 5.5% dividend, which is high enough to interest me. At this time, I give this company the same sort of positive rating as I do some high-performing Canadian banks like Toronto-Dominion ( TD ) and Scotiabank ( BNS ).

It's the same upside as with some Swedish banks. Eventually, well-performing banks will normalize - and the fundamentals as well as the valuations confirm the upside here. Relative to its yield, the company is at multi-year lows. The RSI indicators, which are more on the TA side of things, are also flashing green with the 14-day RSI in the 85th percentile. Every single valuation multiple from Price to earnings, to FCF, to CF, to revenue, to Graham, are either at average or above all, below the company's own historicals. While the company is experiencing some faster asset growth than revenue growth, and we're seeing some insider selling (which are small worries), none of these worries should dictate or impact what positives we're seeing. Moreover, the insider sales were at the 2022 highs, and there have not been many sales since things dropped down.

Because on the plus side, we have excellent scores in every multiple related valuation, we have close to 10-year highs in yield and so forth, and the company is a market leader. The company's RoCE and RoE numbers may be down compared to where they were in 2015-2018, but they're still very much positive relative to their cost of capital.

There are some risks to BOH. Primarily, I would say they are related to the relatively limited growth potential in the long term for the bank. You do get safety in exchange for that, but at times, this bank has underperformed the market average simply as a product of its limited growth. For instance, a long-term shareholder has currently only a 20-year annual RoR of just around 5.5%. This highlights the importance of not buying this bank too expensively - if you do, even the long-term returns you may gather likely won't beat the market.

Overall, I don't see enough of a downside to stick to my conservative hold rating here, and I'm bumping it to a buy for reasons related to its valuation and quality, in spite of the potential downside in the near term.

Here is my new and updated thesis for the Bank of Hawaii.

Thesis

- Bank of Hawaii is a market-leading bank in a very attractive geography. It has solid historicals, fundamentals, and a good moat given where it is located. Its near-term targets while not massively positive, show overall stability.

- I believe Bank of Hawaii is a "BUY" with an upside of over 10% annually, a safe 5%+ yield, and a company that you can potentially hold onto for years.

- I remain at a price target of $72/share and rate it a "BUY" at this time.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now a "BUY" based on valuation.

For further details see:

Bank of Hawaii: Worth Buying In The Crisis?