PGC - Bank Of N.T. Butterfield: A Resilient Bank That Is Being Overlooked

2023-07-02 04:59:00 ET

Summary

- Bank of N.T. Butterfield & Son, a financial institution serving high and ultra-high-net-worth individuals in Bermuda, the Cayman Islands, and the Channel Islands, is currently being overlooked by the market in valuation terms.

- The bank has a solid financial position with a sound risk management approach, a loyal customer base, and limited competition due to high barriers to entry in its markets.

- Despite the positive macro environment for banks and NTB's strong position, the market is currently undervaluing the bank.

- We suggest that this presents an investment opportunity, with a potential return of between 18% and 22%.

Editor's note: Seeking Alpha is proud to welcome Chimerix Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

The business & NTB history

The Bank of N.T. Butterfield & Son Limited (NTB) offers services for high and ultra-high-net-worth individuals and provides residential mortgage lending, automobile financing, consumer financing, and credit cards. We believe that this bank presents the opportunity to take a position in a historically branded institution for a cheap valuation.

The market seems to not properly value the true competitive advantage of NTB, which lies with its name and client relationships more than any other traditional bank (big or small). The bank operates in four major markets: Bermuda (44% of revenues), Cayman Islands (32%), Channel Islands (19%), and other countries (5%); the company was born in Bermuda in the far 1858, and it has gained a big market share in this country, by having 58% of total banking assets of Bermuda. The customer base is loyal to the bank because of its long history and high-quality services in this niche market and as a consequence, it has very solid and non-volatile sources of funding (mainly deposits of wealthy clients).

But the strongest point in favor of the bank is the limited number of competitors and the huge barriers to entry in the countries in which it has the largest portion of revenue. It's not a competition-free market, but there is a very low possibility of seeing structural changes in the market environment due to the entry of competitors in this niche. The long-time brand also gives NTB an advantage when dealing with clients that focus little on cost savings and more on a true relationship with their wealth manager. This is why the case of this bank is so structurally different compared to the failures that we have seen across the year.

Financial position and results: profitability and risk management are the keywords

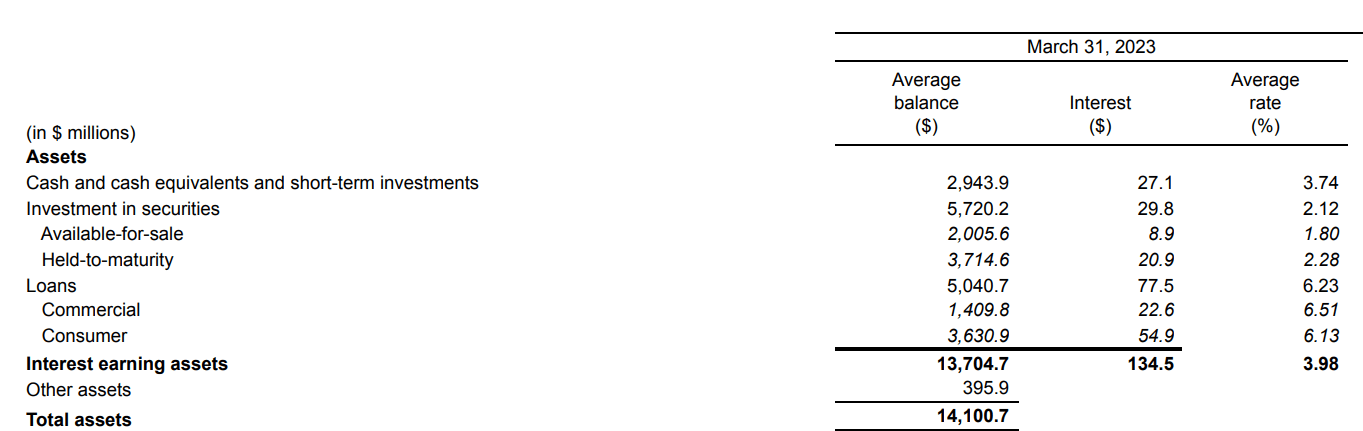

One of the very first things that investors now look at when dealing with banks is how wide the assets/liabilities mismatch is. As a year of rate hikes went on, many institutions found themselves with HTM securities yielding <1% and maturing 5 years from now, while having a deposit base that demanded much more generous yields. This caused the bank runs that we saw starting from SVB collapse.

The case of NTB, however, is very different. The bank was somewhat known in these past years for its resilience and risk-averse book, with the majority of securities (HTM and AFS) being US agency-issued (more than 95%). But the most important point is to also look at deposit changes. As of December 2022, NTB saw an increase in non-interest-bearing deposits of around $200 million (roughly 8%), offset by a decrease in interest-bearing by around $550 million, leaving a very moderate reduction of less than 3% on the table. During the banking chaos of the first quarter of 2023, deposits continued to move very little, decreasing only by 4%.

NTB - Balance Sheet (SEC Filings)

{kind=link}

Also, the bank was focused on increasing the average yield of its assets, which now sits close to 4% which is more than 2.5 times the average yield it pays on liabilities, leaving a great interest income for shareholders.

We believe that this mix of high-quality assets along with limited leverage is the best receipt for avoiding a bank run or any other kind of stress on their financial position. In fact, if we just look at their securities' portfolio, we can argue that it would be very easy for them to access to a Bank Term Funding Program ('BTFP') loan. This facility allows banks under stress to post securities as collateral and receive relatively-cheap funding from the FED. This means that NTB could easily borrow from the FED and have very easy access due to 95% of their securities being AAA-rated.

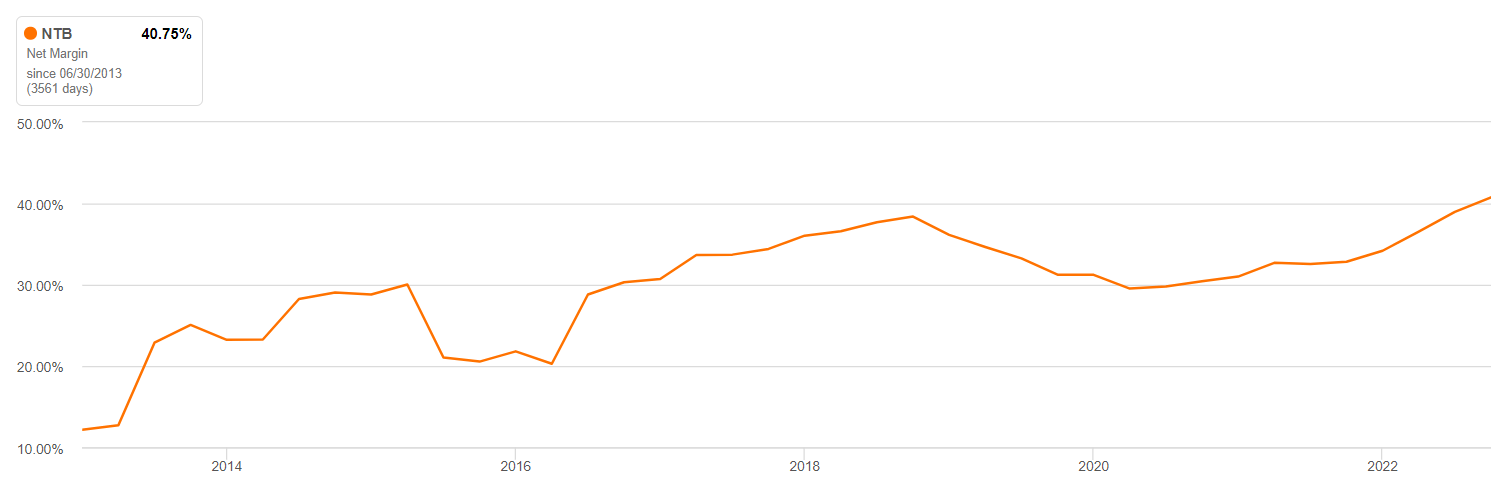

The other resilience part of the story is told by the income statement, where more than 30% of the revenue is from non-interest income. Indeed, NTB is bringing home more than $90 million per year in specific, tailored solutions like "Trust business", and "Foreign exchange revenue". All this left the bank with a net increase of around 32% in net income YoY between 2022 and 2021, an outstanding result given the little changes in the deposit base and improved cost structure. The EPS at the end of Q1 2023 is $1.24 per share on a fully diluted basis, which means close to $5 per year, or 20% earnings yield(!), which can be found in the latest earnings release . Such great amounts of diversified income allow NTB to have more flexibility in their balance sheet structure. If many fees are collected from non-interest-bearing activities (i.e., are independent of lending), the banks will be more resilient in periods of stress on interest rates. Indeed, large changes in lending volume will have a more limited impact, as the income from such activities will continue to flow.

Why NTB is undervalued and the possible play out of the opportunity

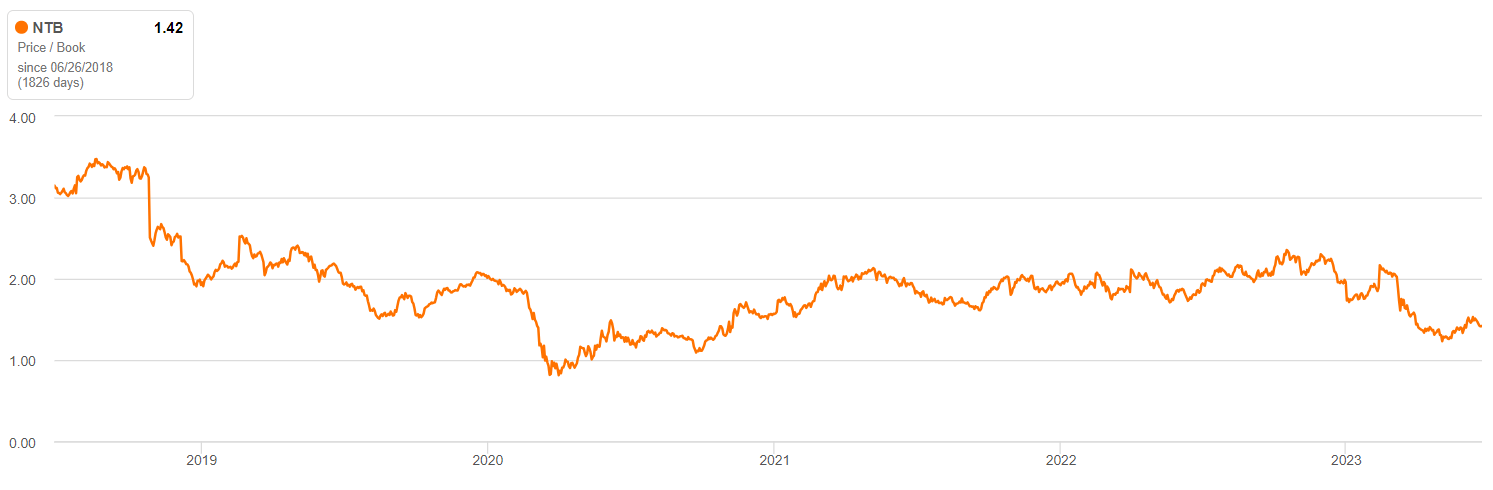

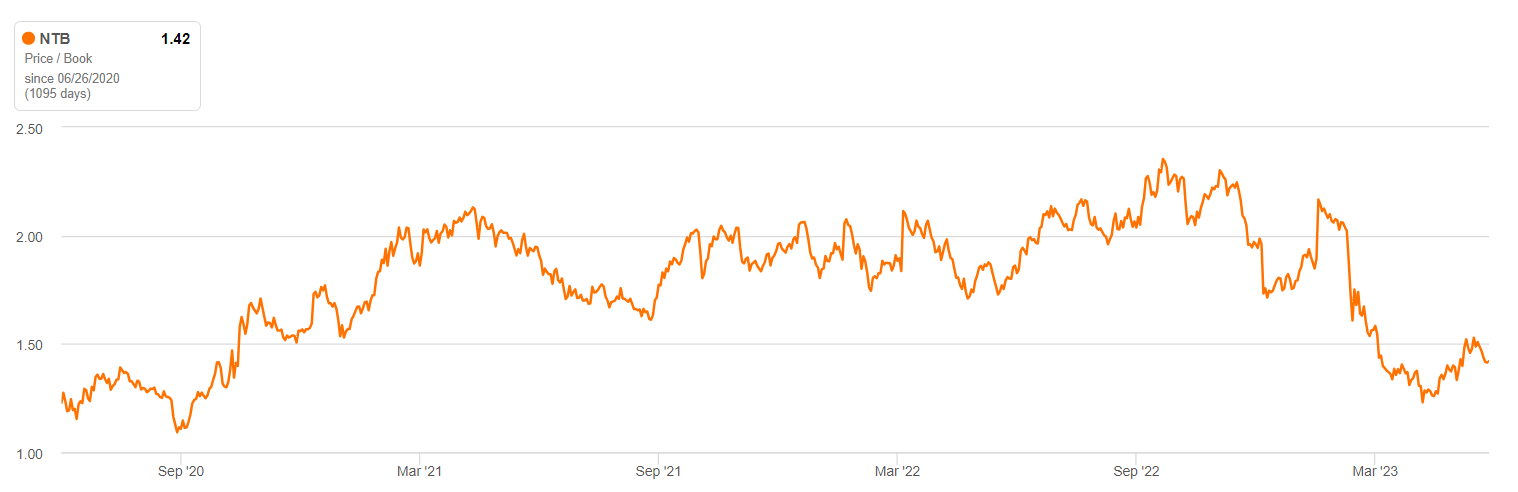

We think that NTB currently sits in a peculiar spot: rising rates are steadily benefiting the bank, as the interest they are earning on the assets is growing much faster than the one they pay on liabilities. But in our opinion, the market decided instead to put a discount on this bank instead of a premium, and that's why the price to tangible book value (P/TBV) is much lower compared to the historical average.

NTB - Historical P/B (Seeking Alpha)

{kind=link}

This shows a very aggressive re-rate that seems unjustified at the moment given: (1) the nature of NTB, being much more focused on stable asset classes and activities, such as wealth management; (2) the pace of development of the net interest income, and net income margins, which improved; and (3) the eventual reduction of interest rates in the foreseeable future. Also, it is good to note that banks are historically known for being assets positively correlated with rising interest rates, so the contraction in multiples should be much more limited.

NTB - Net margin (Seeking Alpha)

{kind=link}

We also believe that the market is not taking into consideration that rates might eventually come lower, and thus NTB earnings position will stabilize, but at higher levels than in the pre-COVID era. And this, along with a sound and resilient balance sheet, will make it one of the best-positioned banks to take advantage of an era of higher rates (and earnings).

Assessing a fair value and price for NTB

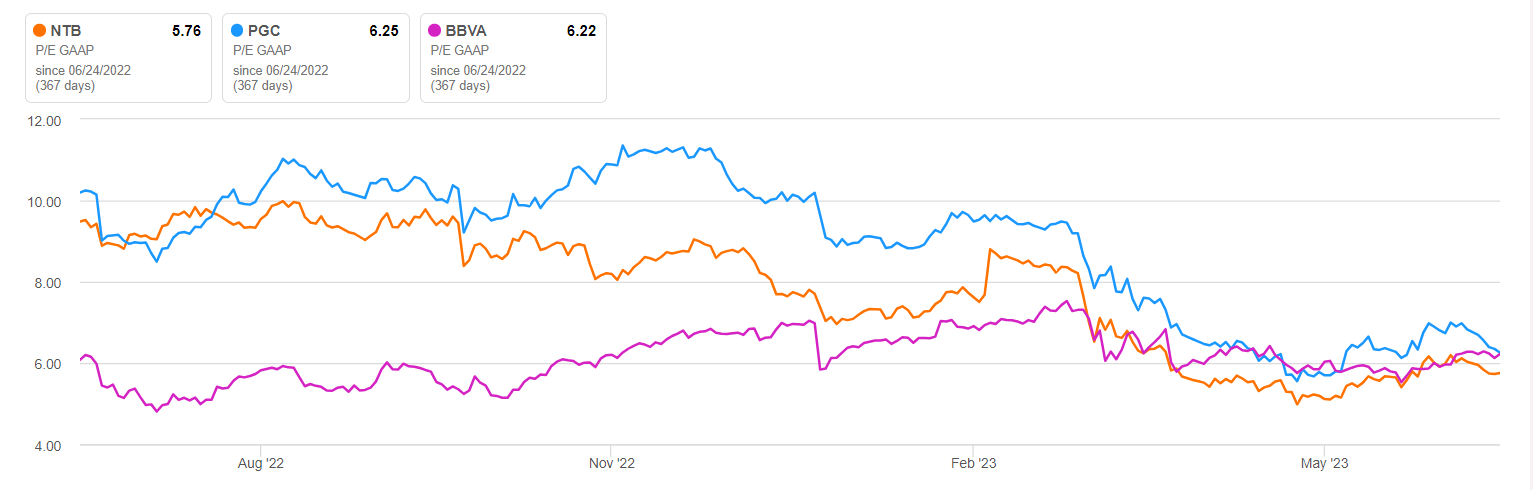

Evaluating a financial company is never easy. A bank is usually valued using P/E and P/TBV multiples, which compared to peers and the overall macro environment will yield a decent spectrum of value. The case with NTB is that, however, its business model is quite peculiar and the comparables are difficult to find if not non-existent. So we have decided to use a mix of both historical levels of its multiples and some similar banks that may be compared with some margin of error.

NTB - Comps P/E (Seeking Alpha)

{kind=link}

This comparison with some comparables (Peapack-Gladstone Financial (PGC) and Banco Bilbao Vizcaya (BBVA)) is making the point that NTB's P/E is actually the lower of the group, sitting at 5.7 compared to 6.2 of the other two. Using expected EPS for 2023 in the $5 figure, this would represent a fair price of $32, or an 18% upside scenario. We also compare this outcome with the forward P/E ratio, which assuming an EPS of $5 for the FY 2023 would get us a ratio of 5.4. This is even lower than the historical one because the market is not appreciating the marginal gains from the rising rates' environment.

NTB - Historical P/B (Seeking Alpha)

{kind=link}

If instead we go and compare the current P/B to the historical one, we will notice even a better outcome. This shows a 1.4 P/B ratio compared to an average in the last years of around 1.9, and if we re-rate the current tangible value per share ($17.3) at the average ratio, we get a fair price of $33. This would mean a 22% return.

To recap, this is what the two upside scenarios look like using different valuation methods:

| Valuation Method |

| Inputs |

| Outcome |

| Relative (to peers) P/E |

| 6.2 and EPS of $5 |

| $32 - 18% upside |

| Historical P/B |

| 1.9 and book value of $17.3 |

| $33 - 22% upside |

What could go wrong?

As with any investment thesis, it is also important to speak the other side, which in this case would be the bearish one. What could go wrong at NTB? Well, a couple of things, from very unlikely ones to more probable drawbacks. Here are listed for importance (and impactfulness). (1) NTB might have its reputation impacted, either because of incompetence or scandals (see the Credit Suisse (CS) case) and this might negatively affect its most valuable asset: its moat . This would make the stock much less attractive as NTB would lose its ability to gain from non-conventional services (i.e., trusts management, etc.). Its competitive advantage would then be limited, and competition in that niche market might arise. (2) NTB might start to lose deposits and may thus need to increase the interest rates paid to customers to keep them. (3) Regulation might impact the company's position given its operations are set in peculiar countries (Caymans, Bahamas, etc.).

Conclusion

We think The Bank of N.T. Butterfield is a sound and solid institution that has been serving a niche market for centuries. Right now, the market is overselling this successful name by confusing its position with that of many other banks, which are in far worse shape, and this creates an opportunity. The proposed valuation method points out an undervaluation between 18% and 22%.

For further details see:

Bank Of N.T. Butterfield: A Resilient Bank That Is Being Overlooked