NTB - Bank of N.T. Butterfield & Son: Great Bank At A Steep Discount

2023-06-22 10:25:39 ET

Summary

- N.T. Butterfield, a Caribbean island banking company, fell sharply thanks to the broader industry's troubles.

- N.T. Butterfield has substantial losses on its investment securities, but investors have blown the risk far out of proportion.

- Actual operating profits are hitting record highs, and there has been no issue with the bank's deposit base.

- Shares should move sharply higher once worries clear up. In the meantime, there's a large dividend and a buyback program in effect.

The bull and bear cases for Caribbean banking franchise The Bank of N.T. Butterfield (NTB) are both quite simple.

The bear case is that N.T. Butterfield has a high level of losses on its balance sheet from owning long-duration bonds that are currently underwater. If N.T. Butterfield were forced to liquidate its portfolio today and cease operations, the bank would be worth significantly less than its current trading price.

The bull case is that no one will force N.T. Butterfield to liquidate today, it can hold its bonds to maturity and come out fine, and that at this price, you own a dominant franchise at less than 6x earnings, a 6.4% dividend yield, and a long history of above-average management, profitability, and credit risk management.

The crux of the matter comes down to whether you think banks will be forced into selling their treasury and agency bonds and other long duration assets at big losses today rather than holding to maturity (or at least until rates go back down).

I am of the view that N.T. Butterfield is not prone to a bank run, the recent hubbub is much ado about nothing and shares are a deep value at the present price.

An Island Bank

N.T. Butterfield is a bank with a unique business model. It exists to serve a few specific island jurisdictions, namely Bermuda, the Cayman Islands, and the Channel Islands. In other words, this is a bank that serves the residents of a few small wealthy island jurisdictions often known for their large offshore banking operations.

Butterfield is the largest bank in both Bermuda and the Caymans and has more than 50% market share in Bermuda specifically.

This gets to a big part of why I'm confident here. As there are only a few Bermudan domestic banks at all and Butterfield is far and away the biggest, it is hard to foment a run against. For one, where exactly would people park their money if not Butterfield? To that point, there are only four licensed banks in the entirety of Bermuda. And the Bermudan government is incentivized to make sure their dominant bank remains in good standing.

That's doubly true since Butterfield has done nothing wrong. Its investment portfolio is more than 95% AAA-rated bonds, primarily U.S. treasuries and agency bonds. And its lending portfolio has the vast majority in residential mortgages, primarily against houses and condos in Bermuda and the Caymans.

So how did Butterfield end up in a mess relating to held-to-maturity securities now?

As the bank explains it, there is not all that much demand for loans among their customer base, which is primarily wealthy individuals and companies operating in Bermuda and the Caymans. Butterfield is happy to lend these folks money, both for personal uses (autos, credit cards, etc.) along with residential property.

But there are limits to how much housing, in particular, can be built on a small island with extensive zoning/height restrictions. There are natural limits to the size of the housing market in Bermuda. Naturally, Butterfield has been able to pile up deposits a lot faster than it has found loan opportunities. So it put a bunch of its money in U.S. AAA-rated bonds, which are generally supposed to be the safest assets on Earth.

Instead, we've seen a historic drop in bond prices, which has, on paper, wiped out a big chunk of Butterfield's tangible equity. But, being government-backed securities, there isn't any risk of long-term loss here. As long as Butterfield can hold its paper until maturity, they will get all their capital back, and with interest. No one is forcing them to realize losses by selling at current depressed prices.

If this were a bank like SVB or First Republic that had a large skittish deposit base with many alternatives, the fear would make sense. People could just move enough of their capital out of Butterfield to force them to sell securities at current prices, locking in sizable losses.

But that seems unlikely. Butterfield is exceptionally conservative, running a loan-to-deposit ratio of just 39% (something closer to 90% is typical at big banks). Its underwriting is also strict, and the bank has had minimal loan losses in recent years.

It's unfortunate that the firm bought so many bonds at what ultimately proved to be unattractive prices. But it shouldn't make any difference to day-to-day operations, as the bank can keep generating huge profits today while its investment book moves toward maturity, causing unrealized losses to shrink.

With NTB stock trading at a less than 6x P/E today, it will earn back roughly 17% of its market cap every year going forward. The bank was already well-capitalized with its ratios far in excess of regulatory requirements. And, to the extent that investors are nervous about NTB's investment securities, it can simply let cash from its operating profits pile up for the next couple of years to defray any worries about the state of its security portfolio.

NTB has been one of the most profitable banks in my coverage universe, often running a return on equity "ROE" above 20% since its 2016 NYSE IPO:

Banks that can earn an ROE above 20% should generally be worth at least 2x if not 2.5x book value in normal conditions. This bank is an absolute profit machine with its niche in wealthy island finance. And actual operating results are getting better and better as we've moved into 2023, as the above chart shows.

Fantastic Earnings Trajectory

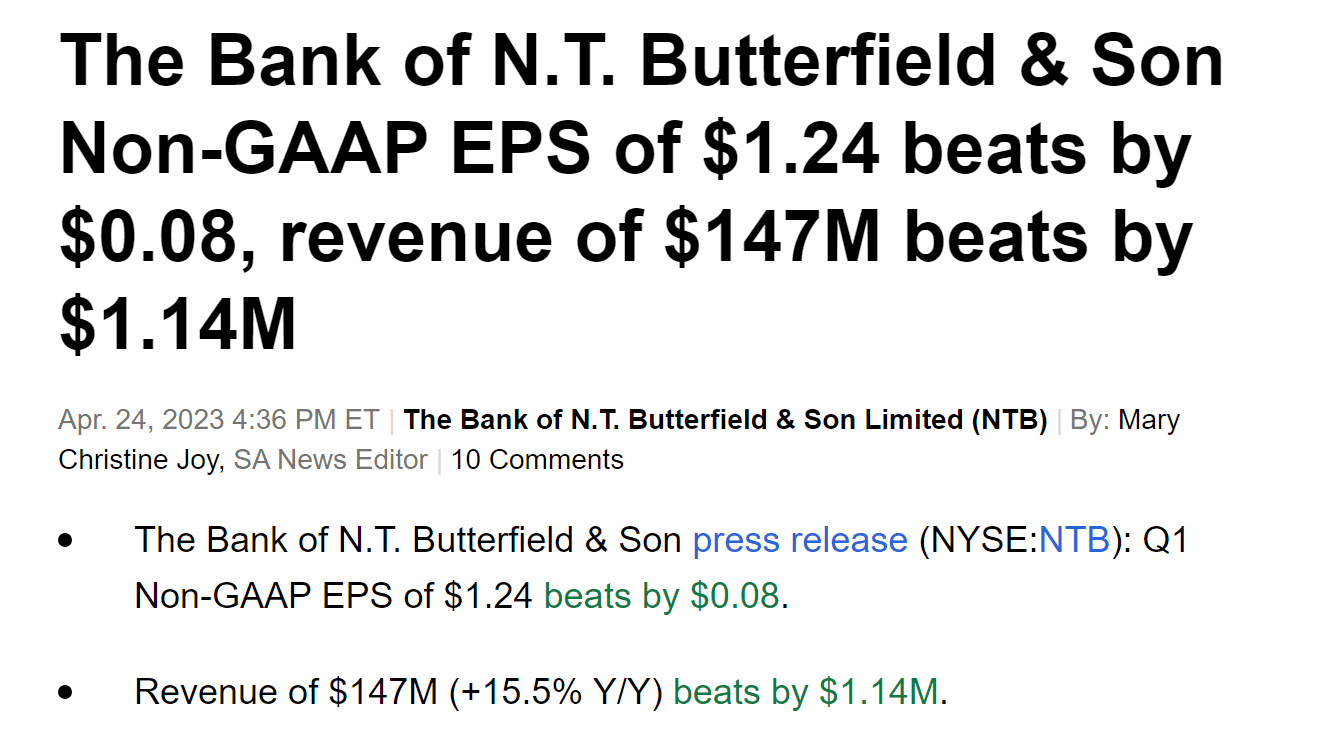

Indeed, the bank's ongoing operations are firing on all cylinders. Shares leapt to new 52-week highs in February following a massive Q4 report. Earnings of $1.27 topped expectations by 13 cents, and revenues of $149 million (+17% y/y) were far ahead of expectations at $143 million.

But what about the regional banking crisis? Did that hit Q1 results? Not at all.

{kind=link}

The company beat on revenues and easily topped EPS expectations once again. The company has now earned $1.27 and $1.24 per share over the past two quarters, respectively. That works out to about $5/share annualized, and is well ahead of the prior analyst expectations for the bank.

Despite the tremendous earnings, shares slumped to 52-week lows during the recent banking industry scare as everyone became fixated on mark-to-market losses:

For the year, NTB stock started with a 25% rally largely due to its excellent Q4 results, then lost 40% of its value due to the United States' regional bank concerns, and has recently moved up a bit, but still remains well down from where it was prior to the recent jitters.

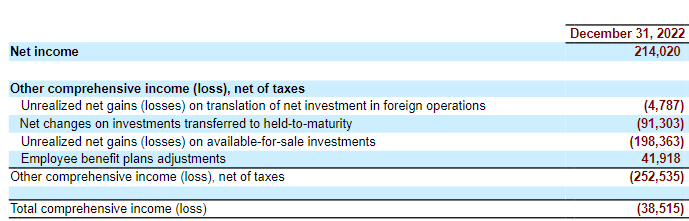

But should we be worried about those unrealized losses? It appears, in total, that the bank is about $400 million underwater on its securities portfolio, counting losses from unfavorable interest rate movements in both 2021 and 2022. On the other hand, the bank earns more than $200 million a year in the course of doing business. Note this full-year 2022 adjusted income disclosure, for example:

{kind=link}

Even taking nearly $300 million in losses on HTM and available-for-sale investments last year, the bank had a mere comprehensive loss of $39 million. Needless to say, these do not seem like particularly awful figures for a bank with a $1.4 billion market cap and more than $800 million in equity.

Banks that own securities always have swings in the mark-to-market value of those bonds. As bond prices tend to be volatile, this is natural and part of doing business. The volatility has been higher than usual given the unusually rapid rate of interest rate increases we've seen, but this still doesn't seem like an existential event for most of the industry, N.T. Butterfield included. If they barely lost money outright in the worst year for the bond market since the 1980s, it seems like things will work out fine in the end.

NTB Stock Verdict

If N.T. Butterfield continues to operate normally, as I expect, this is a $40 per share or greater stock with a tremendous and unique banking franchise, and also one that offers a greater than 6% dividend yield today.

If bank runs spread to the point that dominant banks on small Caribbean islands start running into trouble, NTB stock would be greatly impacted. However, there's little to no indication that this would happen. In fact, in its Q1 earnings release, N.T. Butterfield noted that average deposits were up to $12.8 billion for Q1, rising sequentially from $12.5 billion for Q4 of last year.

I'm highly skeptical that the problems of SVB and First Republic are representative of a much broader industry-wide concern. That's doubly true for a firm like N.T. Butterfield, which is not even a U.S.-based bank. While there is always the possibility that money will rapidly exit banks in small Caribbean island jurisdictions, I don't see it as a serious concern at this juncture.

As such, N.T. Butterfield can wait out the current downturn and let its bond portfolio recover. It will be aided by its strong balance sheet and record operating profits. In the meantime, shareholders get a strong dividend yield, and management is also repurchasing stock at the moment. All this adds up to a favorable outlook for N.T. Butterfield going forward.

For further details see:

Bank of N.T. Butterfield & Son: Great Bank At A Steep Discount