STT - Bank of New York Mellon: Higher Average Interest Rates Will Lead To Gains (Rating Upgrade)

2024-01-18 15:46:08 ET

Summary

- Bank of New York Mellon's recent earnings report shows strong financial performance with a 9.9% YoY increase in revenue.

- Anticipation of interest rate cuts in 2024 could still lead to higher average interest rates versus the past, benefiting BNY Mellon.

- BNY Mellon is a strong choice for dividend growth investors with a current yield slightly above 3% and 13 years of consecutive raises.

Thesis

About three months ago I published an article on Bank of New York Mellon (BK) titled "Underperformance, But Nice Dividend" where I went into details about the mixed outlook of the company. Earnings were reported last on January 12th so I am to provide an updated outlook through the course of 2024. As a result of the earnings report, I am updating my rating to a Buy as I believe BNY Mellon has the potential to provide superior total returns when combining price appreciation and continued dividend growth.

The price has moved up nicely over the last few months. Despite that, I think with the new revenue projections, we may see increased upside throughout the year. In addition, I believe this is supported by the healthy level of cash flow to continue increasing their dividend along the way. So let's dig into some quick analysis to reinforce my rating change.

Bank of New York Mellon Overview

The Bank of New York Mellon is a versatile financial services company with a broad spectrum of business segments. Its primary focus includes asset servicing, wealth management, and investment management services. BNY Mellon plays a pivotal role in safeguarding and overseeing financial assets for institutions, corporations, and individual investors.

The services provided by BNY Mellon encompass custody, fund administration, and securities lending. Furthermore, it engages in active investment management through its dedicated arm. The institution's comprehensive suite of financial services extends its support to clients worldwide, contributing to the establishment of its well-known brand.

BNY Mellon Q4 Earnings

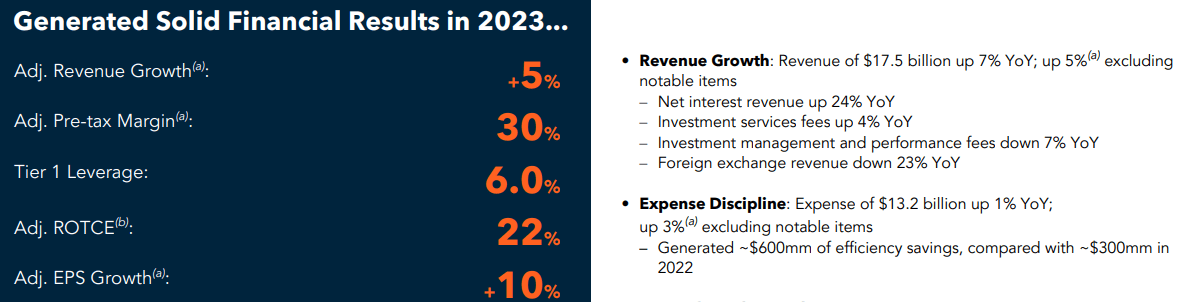

BNY Mellon reported impressive earnings on January 12th, showcasing strong financial performance in the fourth quarter. The Non-GAAP EPS of $1.28 exceeded expectations by $0.16. A significant factor contributing to the strong financials is the impressive 9.9% year-over-year increase in revenue. Total revenue reached about $4.3 billion for the quarter. This growth reinforces BNY Mellon's diversified revenue streams and effective business operations. The breakdown of total revenue reveals a 10% overall increase, driven by various key factors. This is why I am upgrading my rating to a Buy.

{kind=link}

BNY Mellon reported net interest revenue of $1,101 million, marking a 4% year-over-year (YoY) increase. The quarter-over-quarter growth was 8%, primarily driven by a higher balance sheet size and mix. In the Securities Services segment, total revenue reached $2,179 million, remaining flat YoY. Investment services fees saw a 1% YoY increase, with Asset Servicing remaining flat and Issuer Services up 5%, driven by new business and heightened client activity.

The Market and Wealth Services segment reported total revenue of $1,499 million, showing a 7% YoY increase. Investment services fees grew by 6% YoY, with Pershing up 1%, Treasury Services up 5%, and Clearance and Collateral Management up 16%. Foreign exchange revenue increased by 5%, and net interest revenue saw a 10% YoY growth. Non-interest expenses rose by 7% YoY, attributed to higher investments and inflation, partially offset by efficiency savings.

Lastly, in the Investment and Wealth Management segment, total revenue amounted to $676 million, reflecting an 18% YoY decrease. Investment Management was down 26% YoY, impacted by the reduction in fair value and the prior year divestiture. Wealth Management was down 3% YoY due to changes in product mix. Non-interest expenses decreased by 2% YoY, driven by efficiency savings and the impact of a prior year divestiture. Income before income taxes was $(5) million, or $151 million excluding notable items, showing a 1% YoY increase. AUM reached $2.0 trillion, up 8% YoY, and Wealth Management client assets were $312 billion, up 16% YoY. I believe this trajectory will continue as we are expected to see a higher average interest rate going forward.

Catalyst: Higher Average Rates

It is anticipated that rates will be cut over the course of 2024. However, it seems that the consensus is that the Fed is in no rush to do so. Recent statements from a Fed official hint at a potential adjustment in interest rate policy for the year 2024, suggesting the likelihood of rate cuts if inflation remains stable. I think this is likely because of confidence in the economic activity and labor markets, coupled with a gradual decline in inflation towards the Fed's target of 2%.

In the event of interest rate cuts throughout 2024, there is a possibility of average interest rates still being higher than in the past. It's possible that long gone are the days of almost 0% rates. This shift could be advantageous for financial institutions, particularly those with diverse financial services. This is where BNY Mellon would come in and is set to benefit. Such a change may positively impact the net interest margins for banks, contributing to enhanced profitability as we have already seen with this recent earnings report.

Comparison

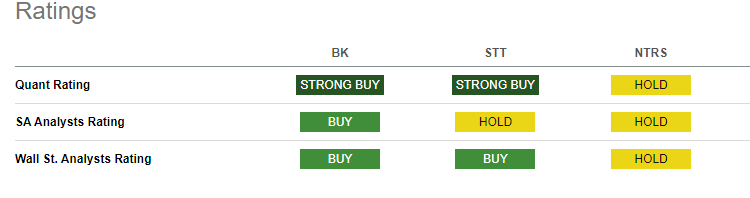

Taking a quick look at some of the peers, we see that BK is one of the more attractive choices. I will use State Street ( STT ) and Northern Trust Corporation ( NTRS ) in these comparisons as they more closely match the business overview than some of the listed peers. Taking a quick look at total return, we can see that BNY Mellon outperforms. This remains true over a ten-year time frame, as seen below, as well as shorter five year time frame.

It seems that BK also has better ratings from Seeking Alpha's Quant, SA Analysts, and Wall St. This is due to BK having better growth, profitability, and valuation metrics compared to STT and NTRS. This comes as no surprise as BK has the highest revenue growth YoY. The revenue growth YoY is as follows:

- Bank of New York Mellon: 6.40%

- State Street: -0.18%

- Northern Trust: -2.68%

{kind=link}

BNY Mellon has the smallest yield of the three but the highest dividend growth over the last 3 year period as well as the lowest payout ratio. I think this makes BK the best choice for dividend growth investors looking to have a growing stream of reliable income.

BK Stock Dividend

As of the latest declared dividend of $0.42/share, the current dividend yield sits a bit over 3%. With the increased levels of cash flow, BNY should have no issues raising their dividend and continuing their 13-year streak. Historically, they have announced increases in Q3 of the fiscal year so I would be expecting a raise announcement sometime around September or October this year.

The dividend growth story has been stellar here and with so much room to grow, I expect continued performance here. Over the last 5 years, the dividend has grown 50%. This represents a dividend CAGR of approximately 8.72% over the same time period. Zooming out on a 10-year period, the dividend has grown at a CAGR of 10.5%. If this wasn't already convincing enough, take into account their great payout ratio of only 31%.

The safety metrics of the dividend are as reassuring as they can be. There is almost no risk of a dividend cut here. For reference, the dividend coverage ratio sits at 3x compared to the sector median of 2.62x. Even if the price were to remain suppressed, BK still makes a great holding in a dividend growth portfolio as it has the growth metrics and safety points there to be an attractive holding for income over time.

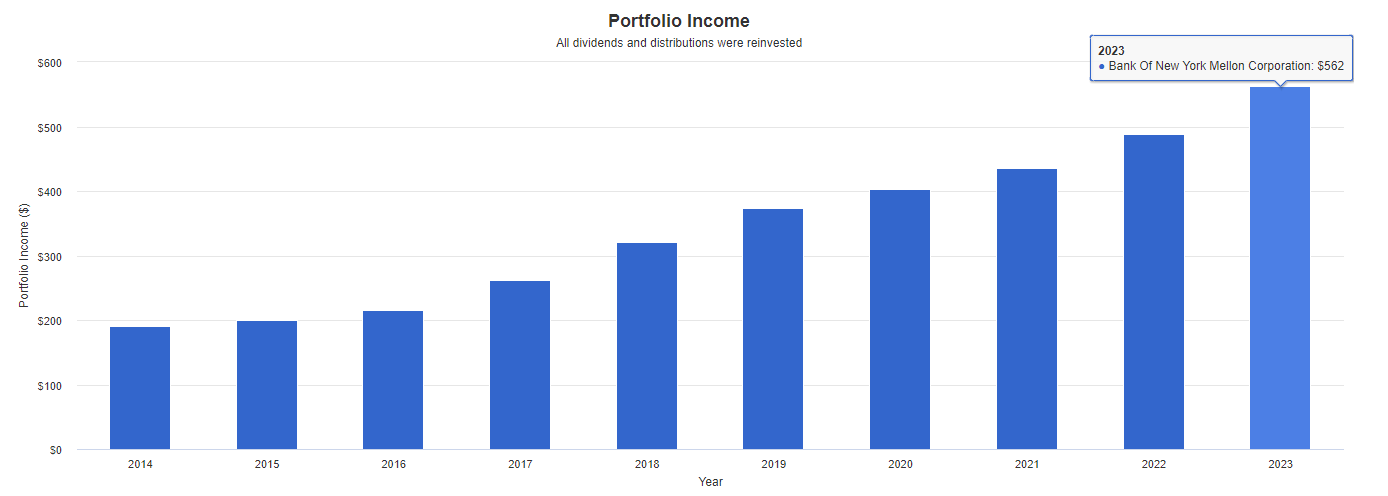

Using Portfolio Visualizer's back-test, we can see that an initial investment of $10,000 a decade ago would have grown to over $18,000 while also increasing your income by 4x. This is with only dividends reinvested and without additional capital deployed

{kind=link}

Risk

While the current outlook for BNY Mellon appears positive, it is essential to acknowledge potential risks associated with the anticipated interest rate cuts in 2024. The catalyst for these cuts is contingent on stable inflation. However, any deviation from this expectation could pose a risk to the interest rate environment.

In the event of interest rate cuts, there is still a possibility that average interest rates could be higher than in the past. While this shift could be advantageous for BNY Mellon, it simultaneously introduces a level of uncertainty. Changes in interest rates, even if they result in a higher average rate, can bring about challenges in managing balance sheet size and mix. Overall, BK's ability to adapt to these changes will be crucial for sustained positive performance.

In addition, in my previous article, I talked about how BNY Mellon has experienced a series of changes in leadership. I think this still holds true and still may pose a risk as we are heading into a new economic environment with new leadership.

Thomas Gibbons took the reins as CEO in 2020, leading the company until 2022 when he stepped down from both his role and the company's board. He was succeeded by Robin Vince in March 2022. Prior to Gibbons and Vince, Gerald Hassell played a pivotal role, serving as president from 2007 to 2012 and later as chairman and CEO from 2011. Lastly, Karen Peetz made history as the bank's first female president, serving from 2013 to 2016. These leaders may have each left their mark on BNY Mellon but unfortunately this turnover makes the company look a bit disorganized in my opinion.

Takeaway

In summary, the updated outlook for BNY Mellon reflects positive momentum, prompting a revised Buy rating after the recent earnings report. The company's fourth-quarter performance was strong and is represented by a 9.9% year-over-year increase in revenue.

The anticipation of interest rate cuts in 2024 doesn't disrupt the potential catalyst for higher average interest rates, presenting opportunities for BNY Mellon. Despite the positive trajectory, we should still be mindful of associated risks.

BNY Mellon's comparative strength against peers, coupled with its dividend growth story, enhances its attractiveness. With a current yield slightly above 3% and a robust history of dividend growth, the company remains a compelling choice for income-focused investors.

For further details see:

Bank of New York Mellon: Higher Average Interest Rates Will Lead To Gains (Rating Upgrade)