OZKAP - Bank OZK: The Preferred Offers A Safe 6.45% Yield

Summary

- $27.7 billion-asset Bank OZK is a perennially top-performing bank, but I was always skeptical of its large construction loan portfolio spread across the U.S. from New York to San Francisco.

- The bank’s 4.625% non-cumulative fixed rate perpetual preferred shares turned up near the top of one of my recent screens of bank preferred issues.

- OZK is an unusual bank, but also undeniably a long-term top performer with impressive loan growth, stable core deposits, a low efficiency ratio and excellent risk management.

- Among bank preferred shares, OZKAP at $17.93 and a 6.45% yield and a 28.3% discount to par at the market’s close on February 17, 2023, provides an excellent trade-off between risk and value for potential capital gains combined with current income.

$27.7 billion-asset Bank OZK (formerly “Bank of the Ozarks”) ( OZK ) of Little Rock, Arkansas is a perennially top-performing bank, but I was always skeptical of its large portfolio concentration of construction, land and development loans spread across the U.S. from New York to San Francisco.

I’ve overcome my prejudice, however, as the bank’s 4.625% non-cumulative fixed rate perpetual preferred shares ( OZKAP ) turned up near the top of one of my recent screens of bank preferred issues. It’s funny how a safe 6.45% yield can change your mind.

The Bank in Brief

Established in 1903, OZK is a regional bank with over 240 offices in eight states including Arkansas, Georgia, Florida, North Carolina, Texas, New York, California and Mississippi. The bank has a $5.6 billion market cap with 2022 year-end assets of $27.7 billion, loans of $20.8 billion, deposits of $21.5 billion and equity of $4.4 billion. OZK is a modern full-service bank with products covering all the traditional retail banking services and loan types. The bank reported $547.5 million or $4.54 per diluted share in 2022 compared to $579.0 million or $4.47 per diluted share in 2021. The unusual year-over-year decrease in net income accompanied by an increase in EPS resulted from stock buybacks which resulted in a 6.9% decline in weighted average diluted shares outstanding. Wall Street analysts are looking for a strong rebound over the next two years with consensus EPS estimates of $5.82 for 2023 and $5.91 for 2024.

OZK’s regulatory capital ratios as of 4Q 2022 were 14.97%, 12.55%, 11.54%, and 15.90% for total risk-based capital, tier 1 risk-based capital, common equity tier 1 risk-based capital, and tier 1 leverage, respectively, drifting down from 17.95%, 15.31%, 14.07%, and 16.17% for the same ratios as of 4Q 2021, but still meeting the definition of a well-capitalized bank.

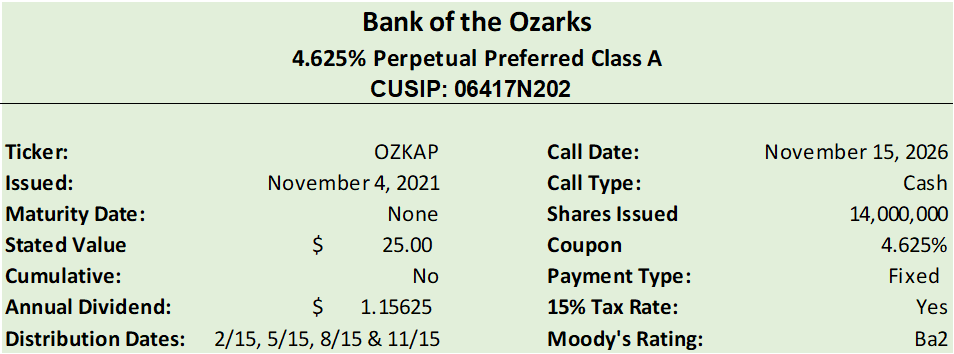

OZKAP: 4.625% Perpetual Noncumulative Preferred Class A

OZK has only one series of preferred stock, OZKAP, the 4.625% perpetual preferred. It’s comparatively new with 14,000,000 shares issued on November 4, 2021 raising approximately $339.0 million in net proceeds. Here’s some relevant information about the shares:

{kind=link}

There’s decent retail-level liquidity in OZKAP with an average daily trading volume over the 10 days ended February 17, 2023 of 25,783 shares per E*Trade.

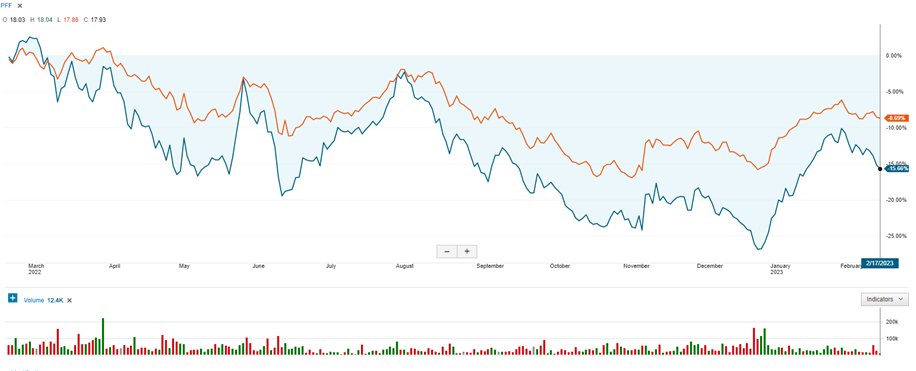

There are two clear attractions to OZKAP, which closed at $17.93 on February 17, 2023; 1) a hefty 28.3% discount to the $25.00 liquidation preference - and its fairly recent offering price - plus 2) a 6.45% yield at that price. The discount to stated value is interesting; OZKAP can be called at par on or after November 15, 2026. The chart below illustrates the unit’s precipitous decline over the past year compared to the iShares Preferred and Income Securities ETF ( PFF ).

{kind=link}

Both securities are essentially fixed-rate; a large part of the decline in their prices resulted from the Fed’s tightening cycle, but, although the ETF is not a pure-play preferred vehicle, OZKAP suffered a decline of roughly 19.9% compared to the ETF’s 9.7%. Also notice that although there have been peaks and valleys, the trend for OZKAP has been downward for the past year. In the next section we’re going to see whether OZKAP’s price and yield are merited by any underlying issues in the bank’s financial performance.

Financial Performance in 2022: Subtle Inflection Point?

For those with historical perspective, think of OZK as a more sophisticated version of an old-fashioned savings and loan circa 1985; primarily real estate loans funded by deposits and minimal noninterest income. As a result 2022 brought about some subtle changes in OZK’s performance.

By design, OZK depends more than any regional bank of similar size on net interest income for profitability. In 2022 net interest income provided 90.2% of OZK’s revenue.

{kind=link}

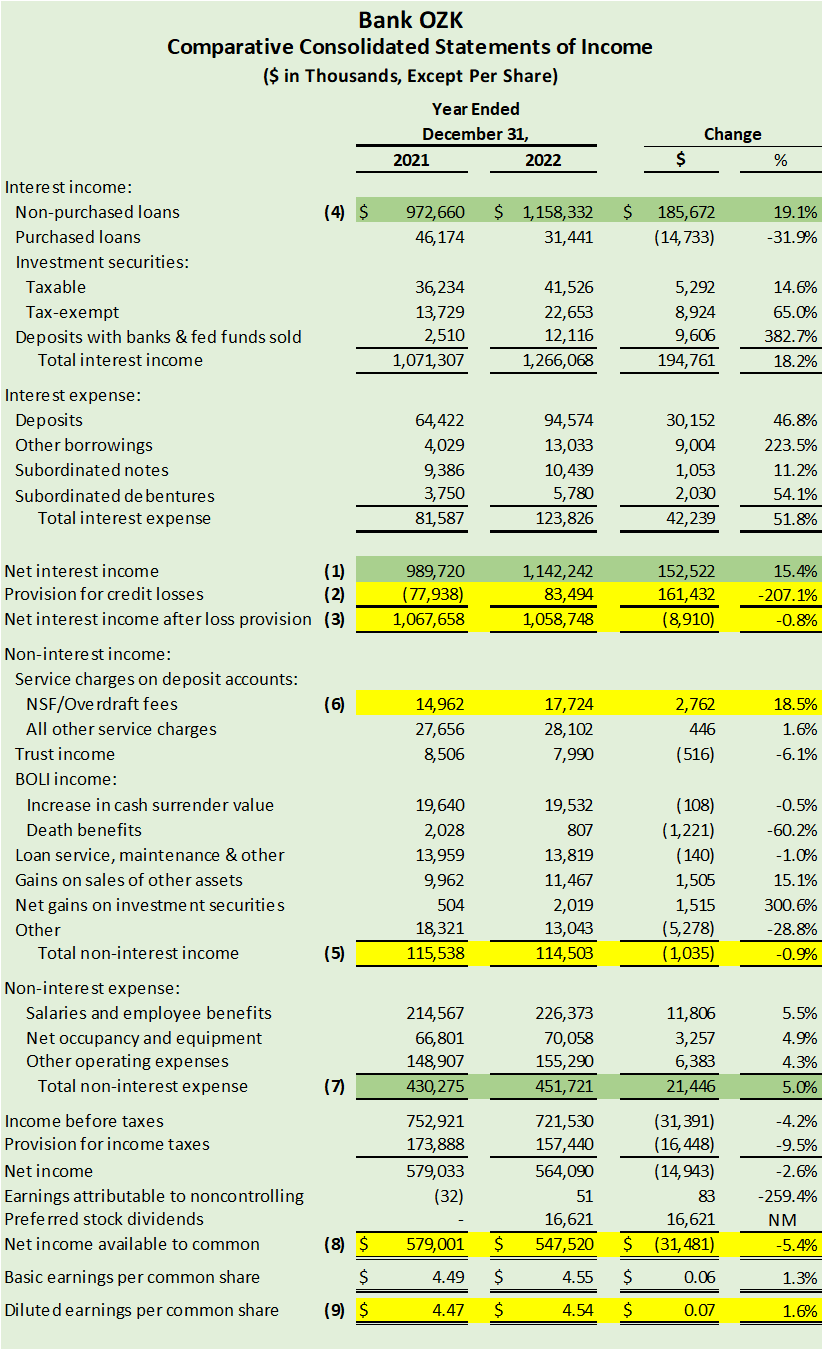

NOTE : For the following discussion, please refer to the 2021 – 2022 comparative income statements below. I’ve both numbered my comments and marked them in yellow for negative and green for positive.

Bank OZK Fourth Quarter and Full Year 2022 Press Release, Herding Value Analysis

{kind=link}

Net interest income before the provision for loan losses (1) - marked in green - increased 15.4% from $989.7 million in 2021 to $1.1 billion in 2022. In 2021, through the sometimes baffling operation of FASB CECL loan loss provisions , there was actually a (2) negative provision for loan losses of $77.9 million compared to a provision of $83.5 million in 2022 – marked in yellow, so (3) net interest income after the provision for loan losses actually declined very slightly in 2022. Surprisingly, management reversed course on the loan loss provision in a single quarter; as late as 4Q 2021 there was a negative $8.0 million loan loss provision followed by a 1Q 2022 $4.2 million loan loss provision. Management explained the abrupt change in direction in the Fourth Quarter and Full Year 2022 Press Release as “based on a number of key estimates, assumptions and economic forecasts and including certain qualitative adjustments to capture items not fully reflected in the modeled results.”

OZK’s lending focus has been construction loans for years, 39.9% of total loans as of 4Q 2022 were construction, and in a rising rate environment the rates on these generally floating rate LIBOR loans adjust rapidly upward. The net interest margin benefits from this loan concentration. From 2021 to 2022, the average yield on OZK’s interest-bearing liabilities rose 91 bps from 4.43% to 5.34%, while the average rate on interest-bearing liabilities rose only 28 bps from 0.47% to 0.75%. As a result, the FTE-adjusted net interest margin increased 73 bps from 4.09% to 4.82% year-over-year. Looking forward, CEO Gleason had this comment on the net interest margin for 2023 during the Fourth Quarter and Full Year 2022 Conference Call :

I would tell you that our prevailing thought is, is that we will see some compression in NIM and core spread in the coming quarters, but that that’s going to be more than offset by growth in average earning assets.

The main contributor to the higher net interest margin and increased net interest income was a very large (4) $185.6 million or 19.1% increase in interest income from loans - marked in green. Amounts increased in every loan category between 2021 and 2022, but, interestingly, construction loans increased by the smallest amount, suggesting risk management in action. Nonfarm, nonresidential loans were the leader in volume terms, increasing $882.4 million or 23.3%. Multifamily residential loans were second, increasing by about $568.5 million or an astonishing 60.8%. The yield on the non-purchased loan portfolio increased a stunning 155 bps from 5.83% for 4Q 2021 to 7.38% 4Q 2022. It has been more than a decade since I’ve seen a 7%-plus yield on a $20.0 billion real estate loan portfolio.

Noninterest income (5), just 9.8% of revenue, was essentially flat year-over-year – marked in yellow. In a potentially bad sign for the U.S. economy, NSF/Overdraft fees (6) increased 18.5% over 2021 – also marked in yellow.

OZK management does an exemplary job controlling noninterest expense especially considering that the bank offers a full suite of banking products, some of which – given the low level of noninterest income relative to the bank’s size - are probably not benefitting from scale economies. Noninterest income (7) – marked in green - only increased $21.4 or 5.0% to $451.7 million in 2022 from $430.3 million in 2021.

{kind=link}

Without the bank’s adjustments, I calculated simple efficiency ratios (noninterest expense / NII after the provision + noninterest income) of 36.4% for 2021 and 38.5% for 2022; these are amazingly low for a bank of this size. Management deserves credit for excellent cost control.

The bottom line was a $35.5 million or 5.4% decline in (8) net income available to common stockholders between 2021 and 2022 – marked in yellow. Adding back the $16.6 million in preferred dividends paid in 2022 versus none in 2021 cuts the decline to 2.6%, but my assumption was that the $339.0 million in net proceeds from the November 2021 preferred stock issue would have been invested at around the 6.18% 2022 average yield for non-purchased loans, producing roughly $20.9 million in additional interest income to more than offset the dividends. Obviously, the some of the net proceeds went elsewhere.

The “elsewhere” might have been the stock buyback program. As previously mentioned, EPS (9) increased year-over-year by 1.6% - marked in yellow. During 2022, OZK repurchased 8.4 million shares for about $350.0 million which reduced the weighted average shares outstanding for 2022 by 6.9%. In November 2022, the board approved repurchasing an additional $300.0 million in shares.

Let’s shift our focus and take a look at the bank’s unusual loan portfolio.

Loan Portfolio: 75.5% Real Estate Loans

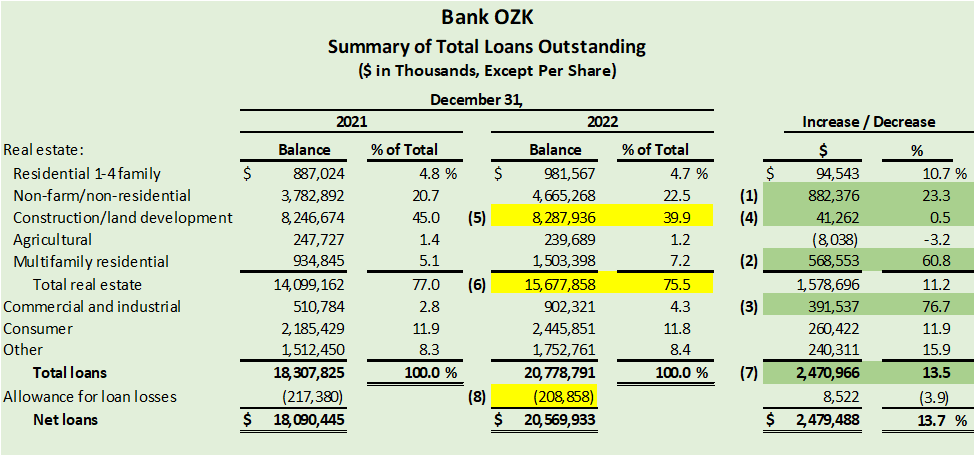

OZK is an unusual bank in terms of its lending focus. Here’s what the bank’s loan portfolio looked like as of December 31, 2021 and 2022.

Bank OZK Fourth Quarter and Full Year 2022 Press Release, Herding Value Analysis

{kind=link}

I found a lot of the volume changes in the loan portfolio interesting if the numerous predictions of a 2023 recession are accurate. CEO Gleason mentioned loan portfolio diversification several times – a recurring theme - during the Fourth Quarter and Full Year 2022 Conference Call:

So, we think we are going to see good diversification and probably better contributions from some of those community bank units in the next year than we saw in the last year, and that was positive. So, we are constructive on the continued trend toward diversification in the portfolio.

Accordingly, the three biggest increases - all marked in green - were all aimed at diversification:

- (1) $882.4 million or 23.3% in nonfarm nonresidential.

- (2) $568.6 million or 60.8% in multifamily.

- (3) $391.5 million or 76.7% in commercial and industrial.

Construction/land development is marked in BOTH (4) green and (5) yellow. On one hand, loan growth in this category - the riskiest – essentially stopped in 2022. However, originations by the Real Estate Specialties Group (“RESG”) which focuses primarily on acquisition, development and construction lending hit a record $13.8 billion for the year. The apparent contradiction results from the delayed funding of these loans; funding will occur in increments over one to three years as project sponsors acquire land, develop infrastructure and finally build and sell their projects.

CEO Gleason spoke about the loan growth in 2023 – the first sentence, the RESG funding cycle and again mentioned loan portfolio diversification during the Fourth Quarter and Full Year 2022 Conference Call:

I think it’s going to be diversified again. Obviously, with the high level of RESG originations, the record level of originations in 2022, a lot of those loans will start funding up in 2023 and finish funding up in 2024. So, RESG’s funded balances will undoubtedly grow and should grow in a decent manner because of the big originations last year. But at the same time, we are getting good traction as shown in the little waterfalls there on growth in the portfolio.

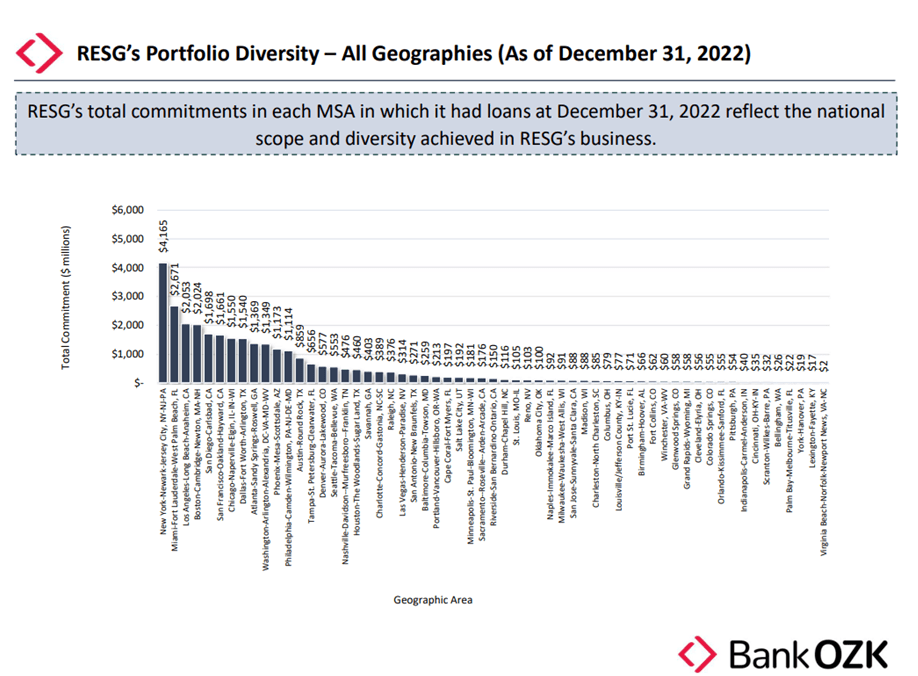

The following chart shows the incredible geographic dispersion of OZK RESG loans.

{kind=link}

Generally rising rates and the funding of construction loans originated in 2022 at floating rates are likely to drive higher loan yields in 2023.

Despite ongoing diversification efforts, OZK remains very much a real estate lender. Real estate loans (6) comprised 75.5% of total loans in 2022 – marked in yellow, down a bit from 77.0% in 2021. Considering that there was no balance growth in construction/land development loans, the largest category, the $2.5 billion or 13.5% increase in the total loan portfolio (7) for 2022 was notable. The volume increases required to achieve that growth, however, might be a concern, but OZK has an impressive record of managing credit quality.

{kind=link}

As a result, the decrease in the allowance for loan losses (8) – marked in yellow, is less of a concern than it would be for other banks.

Loan growth has begun to put pressure on funding with a loan to deposit ratio of 96.6% at year-end 2022 compared to 90.6% at year-end 2021. The bank’s borrowings decreased between 2021 and 2022, implying that immediate funding of loans will have to come from the bank’s $1.0 billion in cash and $3.5 billion in securities held for sale which combined totaled or 16.4% of assets at year-end 2022.

70.5% Core Deposits

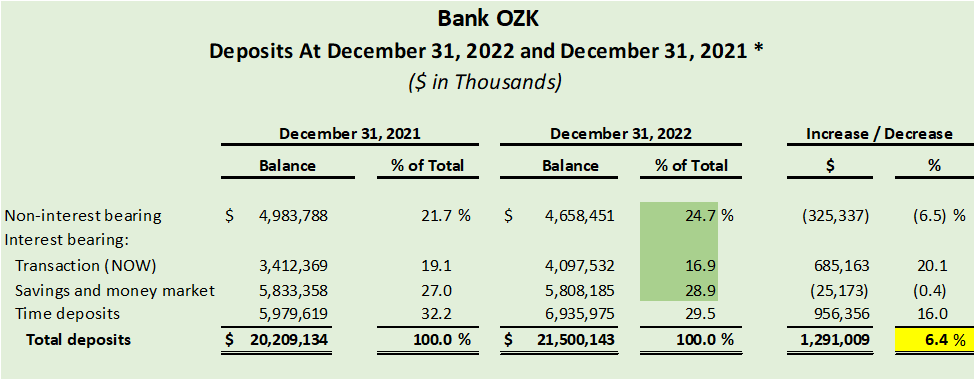

Without relying on new borrowings, deposit growth might restrain the bank’s ability to grow its loan portfolio. While total loans increased $2.5 billion or 13.7% in 2022, deposits only increased $1.3 billion or 6.4%. The bank’s branches averaged a very efficient $89.6 million per branch at year-end 2022. The table below presents summary data regarding the bank’s deposits.

Bank OZK Fourth Quarter and Full Year 2022 Press Release, Herding Value Analysis

{kind=link}

Noninterest-bearing deposits comprised 24.7% of total deposits as of 4Q 2022, up slightly from 21.7% as of 4Q 2021. Core deposits – marked in green; essentially various types of checking, money market and savings accounts, accounted for 70.5% of deposits, providing the bank with funding stability in a rising rate environment. Bank executives from almost any point in the past 40 years would have been envious of OZK’s 0.62% average cost of deposits in 2022, even if significantly higher than the extremely low 0.39% reported for in 2021.

Although OZK only has meaningful deposit market share in Arkansas where it ranks third, management has not been focused on acquisitions to increase asset size, operations, or deposit market share since completing 15 deals from 2010 to 2017.

Conclusion: Buy for Income and Capital Gains

Bank OZK is an unusual bank. I would characterize it as a hybrid; the real estate lending operation of big circa 1985 savings and loan spliced together with the core deposit base of a modern commercial bank, but without significant noninterest income. To make its operations even stranger, the bank emphasizes risky construction lending across the U.S., a difficult undertaking for banks 10 times its size, but succeeds year after year, and somehow all this is accomplished with an efficiency ratio below 40%. This is not only an unusual bank, it is a very special bank.

Although I remain skeptical, it is hard to argue with success:

{kind=link}

As for the preferred stock, I am not worried about its safety, net income in 2022 covered the preferred dividend about 35 times. Another way to look at this is a preferred payout ratio of about 3%. Net income would have to fall from $547.5 million in 2022 to about $17.0 million before the preferred dividends were not covered. After my review of the bank, I would discount any possibility of the preferred not being paid, even in a replay of the Great Financial Crisis of 2008.

The remaining minor issue I have with OZKAP is its low coupon. Before the preferred trades at par, eliminating the current 28.3% discount, we would need to see either a) a Wall Street re-rating of OZK, b) a higher credit rating for the preferred and/or bank or c) a drop in rates to make the 4.625% at par yield competitive. The current discount to par is 28.3%.

Currently, the majority of Wall Street analysts consider OKZ a “Hold” while Seeking Alpha authors are split between “Buy” and “Hold.” With the bottom line a little soft in 2022, most analysts are unlikely to change their ratings anytime soon.

{kind=link}

For income investors, among bank preferred shares, OZKAP at $17.93 and a 6.45% yield and a 28.3% discount to par at the market’s close on February 17, 2023, provides an excellent trade-off between risk and value for potential capital gains combined with current income.

For further details see:

Bank OZK: The Preferred Offers A Safe 6.45% Yield