SBNYP - Banking Crisis: A Primer For Immediate Action

2023-03-20 06:30:39 ET

Summary

- The vast majority of investors do not know or understand how serious the current banking crisis could become.

- The BTFP program implemented by the US Treasury and Fed is insufficient to address the nature and magnitude of the problems facing the US banking system.

- There are no easy solutions that will maintain the status quo. Virtually any long-term solution that is implemented is likely to have revolutionary effects on the US financial system.

You urgently need to understand what is currently going on in the US banking system. In this article, I am going to provide you with some basic facts and analysis that will help you to evaluate the situation yourself and make some important decisions about your investment portfolio.

The ongoing US banking sector crisis has already brought down Silvergate ( SI ), Signature Bank ( SBNY ) and Silicon Valley Bank ( SIVB ), while other banks such as First Republic ( FRC ), Pacific Western ( PACW ), Western Alliance ( WAL ) and Zions ( ZION ) are rumored to be on the brink.

This is not just an isolated problem that affects a small number of banks. As you will learn in this article, the issued faced by the aforementioned banks are systemic in nature, and could potentially threaten the entire banking system in the short-term and particularly in the longer-term.

In this article, my objective will by to elucidate the underlying causes of the current turmoil in the US banking sector, evaluate the extent of the problem and briefly outline some potential scenarios for the US economy and financial system.

Key Facts About the Vulnerabilities of the US Banking System

1. Total equity capital (common + preferred) in US banking sector: 2.14 Trillion.

2. Unrealized losses (mark-to-market) of US banks from duration mismatch: Roughly $1.7 trillion according to one academic study , and roughly $2.0 Trillion according to another academic study .

3. In accordance with points #1 and #2 above, if US banks were forced realize their losses associated with maturity mismatch -- not considering any credit losses - somewhere between 93% and 79% of total equity capital would be completely wiped out. On aggregate, total common equity capital in the US banking system would be negative.

4. In the USA, only bank deposits under $250,000 are guaranteed against loss by the government. Deposits above $250,000 are subject to losses, in the event of a bank failure. For this reason, uninsured depositors, that control very large sums, are particularly prone to "run". In the internet age, large depositors can and do withdraw their funds from banks, in less than one minute, at the press of a button.

5. According to S&P Global , roughly 46% of all US deposits are uninsured, representing $7.89 trillion. This is the proportion and the number of deposits in the US that are particularly prone to "run".

6. The problem of bank runs by large clients with uninsured deposits is not just a problem limited to small and medium sized banks. The following is a partial list of banks with over $200 billion in assets where uninsured deposits comprise over 50% of total deposits:

- Bank of New York Mellon ( BK ) 92%

- State Street Bank ( STT ) 91%

- First Republic Bank ( FRC ) 67%

- JPMorgan Chase ( JPM ) 52%

- U.S. Bank ( USB ) 51%

How Vulnerable Is the US Banking System to Runs by Uninsured Depositors?

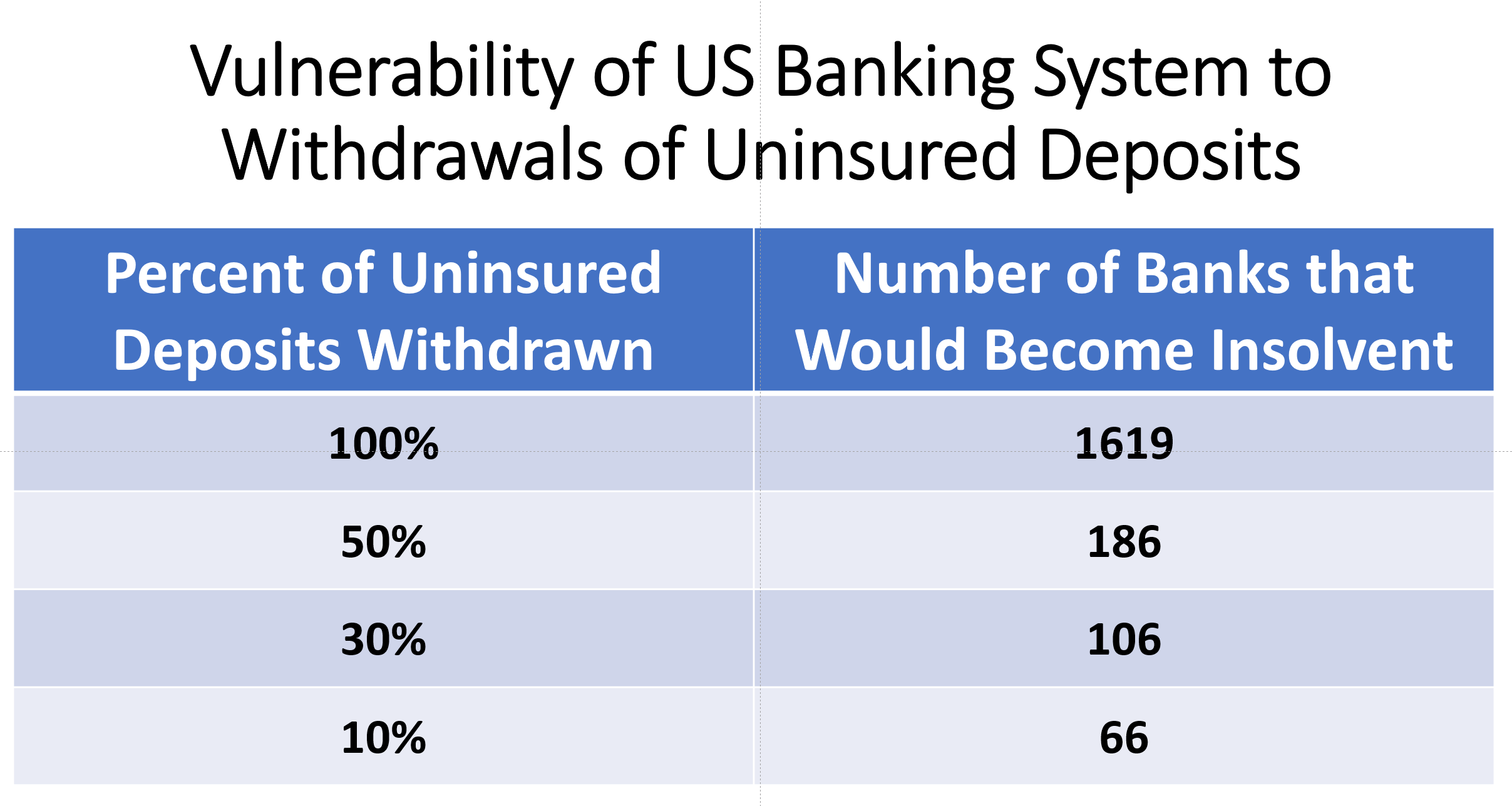

An academic paper recently estimated how many banks would become technically insolvent in the event of bank runs by clients that withdrew their uninsured deposits. Here are the results of only four of the scenarios that were analyzed.

Number of US Banks Vulnerable (Erica Jiang and Investor Acumen)

{kind=link}

For reference purposes, the percentage of uninsured deposits withdrawn at Silicon Valley Bank (SIVB) was roughly 30%. According to the above study, roughly 106 US banks would become insolvent if 30% of their uninsured deposits were withdrawn.

Threat to the Capitalization of US Banks

As stated earlier, on aggregate, between 79% and 93% of US total equity capital has been wiped out, on a mark-to-market basis, due to maturity mismatch. Aggregate common equity is negative.

Looking at banks individually, the problem is clearly systemic. Roughly 50% of US banks would have negative equity if their portfolios were marked-to-market. About 5% of US banks would have negative equity of over 10% of total assets if their portfolios were marked-to-market. Over 95% of US banks would be forced to raise equity capital in order to meet minimum regulatory requirements.

Threat to Lending: Credit Crunch?

If over 95% of US banks are technically insolvent on a mark-to-market basis, this clearly implies that 95% of US banks would need to immediately suspend all new lending activities. Furthermore, the vast majority of these undercapitalized banks would need to deleverage by reducing the amount of credit on their balance sheet. Vast numbers of existing borrowers would have their loans called and/or would be denied roll-overs of existing credits.

Such a scenario would imply a massive and sudden deleveraging of the US financial system, with devastating effects on the real economy.

Left unresolved, the problem described above would have a devastating impact on the US economy, comparable in extent to the Great Depression.

What Are Authorities Doing To Prevent Another Great Depression?

The US Treasury and Federal Reserve have created a program called "Bank Term Funding Program" ((BTFP)) which is designed to deal with the afore-mentioned problems. In particular, this program offers loans of up to one year in length to eligible depositary institutions for amounts that equal 100% of the par value of eligible assets such as U.S. Treasuries, U.S. agency securities, and U.S. agency mortgage-backed securities.

What does this program accomplish? As mentioned before, US banks hold assets that, on a mark-to-market basis, are worth less than their stated book value (acquisition cost). In the event of bank run of sufficient magnitude, banks would have to sell those assets at a loss (realized loss), impairing their equity. As indicated earlier, depending on the extent of the bank run, due to the impairment of their equity values, massive numbers of US banks would be forced to shut down. However, under the BTFP program, US banks with losses on the eligible securities named above would not be forced to sell those particular assets at a loss. Banks with these eligible classes of securities can obtain loans from the BTFP program at 100% of the par value of the securities, thereby raising liquidity (to meet deposit withdrawals) without having to sell said assets and sustain realized losses and concomitant equity impairment.

Is the BTFP Solution Sufficient to Solve the Current Problem? Short-Term? Long-Term?

The answer to this question is not straightforward. If the question is limited to whether BTFP solves the problem of the vulnerability of US bank capital against bank runs, the answer is a clear "no". This is for two reasons:

1. BTFP does not provide any protection to uninsured deposits. Uninsured deposits are legally as vulnerable today as they were before BTFP. Therefore, the US banking system remains highly vulnerable to "runs" by large clients which may choose to withdraw deposits from US banks. The deposits if these large clients, representing 46% of all deposits in the US banking system, are all subject to losses and/or asset freezes in the event of bank failures.

2. The BTFP program only covers limited "eligible" assets such as U.S. Treasuries, U.S. agency securities, and U.S. agency mortgage-backed securities. Assets such as corporate bonds, non-agency mortgage loans, business loans, real-estate loans and all other assets are absolutely not covered by the BTFP program. Therefore, for those banks that do not hold a significant portion of their assets in the types of securities that are eligible under the BTFP program - and this represents a significant majority of US banks - the BTFP program will be of little help to them. In the event of a run by large clients with uninsured (or even insured) deposits, these banks would be forced to conduct fire sales of their (BTFP-ineligible) assets at a substantial loss. And as indicated in the prior sections, the sale of a substantial proportion of assets at a loss would force hundreds, if not thousands, of US banks to shut down.

But the above analysis begs the question: In light of the announced BTFP program, plus the possibility of further programs, will large clients with uninsured deposits continue their "run" on US banks?

Unfortunately, this is not a question that can be answered by reference to factual data. This is a question that can only be answered via a subjective analysis of the psychology of depositors.

One thing is clear: From an individual perspective, clients with uninsured deposits have very little incentive to "wait this out" and place their cash at risk of seizure and potential haircuts. For most depositors, there is essentially zero cost to move their deposits to banks that they perceive as safer or -- safer still -- into money market funds or directly into risk-free securities (e.g T-Bills). Given that there is essentially zero cost to secure 100% of the value of their deposits, it is not individually rational for large clients to maintain deposits at a bank that has even a 1% chance of being shut down.

Indeed, the incentive structure right now vastly encourages large depositors to withdraw their deposits. It is a classic problem of "prisoner's dilemma" and "collective action."

Furthermore, history shows that once a bank runs get started, they tend to spread and accelerate hyperbolically.

A Disaster is Unlikely in the Short-Term

Due the potentially disastrous consequences of inaction, US authorities will simply not allow further bank runs that would threaten the US banking system. If current measures are insufficient to stem the panic, US authorities will step in and offer drastic solutions to prevent further shut-downs of US banks.

While the exact solutions to be eventually implemented by US authorities are unclear, it is virtually certain that solutions will, in fact, be implemented. This could include extension of the BTFP to cover all assets, or the announcement of a blanket guarantee of all deposits, regardless of size.

These sorts of drastic solutions alluded to above would stem the immediate crisis, in the short-term. However, the longer-term outlook for the US banking system - and indeed, banking systems around the world -- is far more uncertain.

Longer-Term Issues

While a blanket guarantee of all deposits might halt bank runs in the short-term, unless the guarantee is extended permanently, the problem will continue to plague the US banking system, with potentially very deleterious consequences for the US economy in the short, medium and longer terms.

A permanent extension of guarantees to all deposits would require legislation. Providing blanket guarantees to all deposits would amount to a multi-trillion-dollar subsidy to US banks. Furthermore, such a regime would create all sorts of moral hazard problems. As a result, such legislation would be very unpopular and, in my view, it is quite doubtful that such legislation could be successfully achieved in the US - at least not under current political and economic conditions.

With this fact in mind, the US banking system faces the long-term prospect of large clients permanently removing their deposits from the banking system and investing their funds in money market instruments that are exclusively invested in US-government-guaranteed securities (e.g. T-Bills) and/or directly into US-government-guaranteed securities.

This would represent a revolutionary change in the US financial system with potentially drastic long-term consequences. Credit to the private sector would be drastically reduced and the maturity of loans would be drastically reduced. Fixed-rate loans, including fixed-rate home mortgages, would largely disappear. Certainly, fixed-rate loans to businesses would largely disappear. The volume of credit to the private sector, more generally, would be drastically reduced.

It is widely believed that small and medium-sized US banks could be particularly impacted by a failure to provide some sort of deposit guarantee system that covers large deposits. The economic consequences of a run on small and medium sized banks in the US would be devastating. Small/medium banks account for 50% of US commercial and industrial lending, 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending.

However, as has been alluded to earlier, even large US banks would be deeply impacted by a shift in the preferences of large depositors toward money market funds and or direct holdings of risk-free securities.

Failure to adequately resolve the problem of uninsured deposits, could lead to a significant disintermediation of the US financial system. Indeed, in the context of modern technology, it is somewhat difficult to imagine that things will not evolve in this direction, sooner or later.

The result of disintermediation would be a contraction in overall credit to the private sector, higher interest rates to the private sector and a drastic reduction in maturities. Private investment and private long-term investment would be severely reduced. This would obviously have devastating effects on long-term US economic growth.

Indeed, the problems described above are so massive that it would be somewhat "easy" to conclude that the US government will have to do "anything" to address these threats. However, as I have mentioned, addressing these problems fully would be extremely difficult politically. Furthermore, any political solution would likely involve revolutionary changes in the US regulatory system and the degree of involvement of the US government in the banking business.

Indeed, providing a blanket guarantee of all US deposits would amount to a quasi-nationalization of the US banking system.

Why would a blanket guarantee of all deposits amount to a quasi-nationalization of the US banking system? Because if the US government is going to guarantee all deposits, the US government would necessarily have to become far more active in regulating and supervising the activities of all US banks. Government regulators would essentially determine what sorts of loans US banks could and could not make. Inevitably, in such a regime, risky loans to the US private sector would be drastically curtailed. Worse still, such a system would become a breeding-ground for official corruption. Furthermore, such a system would inevitably become dominated by politically-motivated mandates (pro-environmental, pro-LGBTQ+, anti-oil, and etc.)

Conclusion

As alluded to earlier, I do not have a definitive answer to the question of whether the currently implemented BTFP program (and the prospect of more programs in the future), will be sufficient to halt the current bank run on US banks.

Clients with uninsured deposits seemed quite happy for many decades to warehouse their funds in US banks -- up until three weeks ago. Therefore, it certainly seems plausible that these depositors could once again become content to perpetuate their current cash practices, at least for a time.

However, it is also quite possible that a "genie has left the bottle". By this I do not mean that massive numbers of US banks will be shut down in the short-term. I think this is highly unlikely. What I mean by this is that, in the short, medium and longer runs, large clients with funds that are not fully covered by deposit insurance may very well choose to alter their cash management practices. This would be a somewhat logical evolution. Indeed, it seems almost inevitable.

For clients with funds that cannot be insured by banks, managing all or a greater portion of their available cash in risk-free money market funds or directly managing their own portfolios of risk-free assets makes a great deal of sense. Indeed, many large corporations such as Apple ( AAPL ) already manage their own cash.

From a cost-benefit perspective, it makes very little sense for large clients to stick with the current cash management regime, unless their deposits are fully guaranteed. However, as I pointed out in this article, a regime that fully guarantees all deposits, even if it were politically feasible, would be fraught with enormous risks and costs for the US economy.

Investors need to think hard about how the US financial system is going to evolve in the short-term and in the long-term. And they need to take action more or less immediately. Events are moving at lightning speed and investors do not have the luxury of contemplating passively for weeks or months. Markets are going to be discounting various scenarios very quickly - both short-term scenarios and longer-term scenarios.

The US banking system is built on a business model that was devised more than 100 years ago before the age of computers, the age of the internet and even before the age of the automobile. Due to technological and societal developments, the US and global financial system is going to evolve in new directions. These changes, which are inevitably going to occur - at a faster or slower pace -- will have profound effects on the entire US economy in the short, medium and longer-terms. These changes will also inevitably have enormous effects on your personal equity and bond portfolios. Indeed, the impacts on portfolios could be very revolutionary. We are certainly preparing for financial evolution -- of various types and of various speeds and under various scenarios -- at Successful Portfolio Strategy. We are currently extremely focused on the evolution of the financial system that will be triggered by recent events.

One thing is virtually certain: The evolution of the financial system, from this point forward, is going to be bringing about major risks and enormous opportunities for investors that are able to understand what is happening that are able to use this knowledge to anticipate future trends and events.

For further details see:

Banking Crisis: A Primer For Immediate Action