EUFN - Banking Crisis Dramatically Increases The Odds For 'Hard Landing' Recession

2023-03-21 04:20:00 ET

Summary

- Major bank failures are occurring in the US and Europe.

- Bank failures are common in major recessions, and all fractional reserve banks are at risk.

- This banking crisis could be worse than the Great Recession.

- High inflation puts the Fed between a rock and a hard place.

- Investors can seek safety as well as significant profits during this challenging time.

When I went out on a major limb in the summer of 2021 with my Seeking Alpha article titled " 5 Reasons The Next Stock Bear Market And Recession Could Be The Worst Since The 1930s ", the stock market was hitting new all-time highs and investors didn’t have a care in the world, except for trying to figure out which of the most speculative “investments” they could buy that would enable them get rich quickly. As a result, the bear market that started in early 2022 was an unpleasant shock for most investors.

But after the S&P 500 rallied 20% from mid-October to early February, there was a flurry of “experts” who said not to worry: a new bull market had officially begun and there would be “no landing” for the economy (i.e., no economic slowdown) or, at worst, a “soft landing” (i.e., mild economic slowdown). Regardless, by no means would there be a “hard landing” (i.e., economic recession), since the all-knowing seer of the future - the stock market - had spoken.

This was occurring despite virtually all proven leading economic indicators pointing toward a recession, as I discussed in recent Seeking Alpha articles here , here and here .

Now, Everything Is Different

Things sure have changed in the past few weeks!

We have just witnessed the second- and third-largest bank failures in US history with the sudden collapse of Silicon Valley Bank ( SIVB ) ($209 billion in assets) and Signature Bank ( SBNY ) ($110 billion in assets).

Do most investors remember what the largest bank failure in US history was? It was Washington Mutual ($307 billion in assets). When was that? In September 2008, during the middle of the Great Recession, the worst recession since the Great Depression of the 1930s.

Now one of Switzerland’s largest and most famous banks, Credit Suisse ( CS ), has failed.

What are the implications of these sudden major bank failures for investors? Are these “one-offs”, or are there broader investment implications?

Bank Failures Are Common In Major Recessions

History shows that major recessions are typically accompanied by major banking crises. The first major financial crisis and recession in US history was the Panic of 1819. I wasn’t there, but historians say the number of US banks fell by over 20% in three years as a result of that crisis. Other significant financial panics followed in 1837, 1873, and 1907.

Bank runs were a key cause of the unprecedented disaster that was the Great Depression of the 1930s. Anywhere from 30% to 50% of US financial institutions collapsed during that time, despite the Fed being the banking industry’s “lender of last resort” since 1913. This led to a massive decline in the money supply and significant price deflation, as explained by economist Murray N. Rothbard in his highly acclaimed history of the period, called “America’s Great Depression”.

In addition to Washington Mutual, the Great Recession of 2008-2009 saw the failures of Bear Stearns, Lehman Brothers, Merrill Lynch, Fannie Mae, Freddie Mac, and many other major financial institutions. The fact is, financial institution failures are a feature, not a bug, of major recessions.

All Fractional Reserve Banks Are At Risk

Many bank customers do not know that they cannot all access their money at the same time. This is because modern commercial banks keep only a small fraction of customer deposits on hand for redemption. Most of the rest has been lent out and will not be repaid for many months or years in the future. This is called fractional reserve banking.

As a result, unlike any other business, banks can become instantly bankrupt when enough depositors demand their hard-earned money back at the same time, which is called a bank run.

And it is now much easier and faster to have a bank run than in the past. Depositors no longer have to line up at a physical bank and wait for their cash to be slowly counted out for them. Instead, they can immediately withdraw their money with an app on their phones and transfer it to another bank or put it in a money market fund or buy an ETF that invests in Treasury bills.

This Banking Crisis Could Be Worse Than The Great Recession

The rise in interest rates over the past year, which is even more rapid and severe than the rise in rates before the Great Recession, has put a severe strain on financial institutions. With very safe 3-Month Treasury bills yielding 4.5%, bank deposits yielding 0% or 0.5% are much less attractive. So bank customers are pulling out their money to invest in higher-yielding assets.

Banks then have to sell bonds and other assets to pay off depositors. Unfortunately, due to the rise in rates, banks are sitting on hundreds of billions of unrealized losses on their bond and loan portfolios.

As a result, the KBW Bank Index has already fallen 47% since its early 2022 high, which is over half the 85% decline from early 2007 to early 2009, as shown below. That’s why we believe history will likely refer to this period as the “Greater Recession”.

{kind=link}

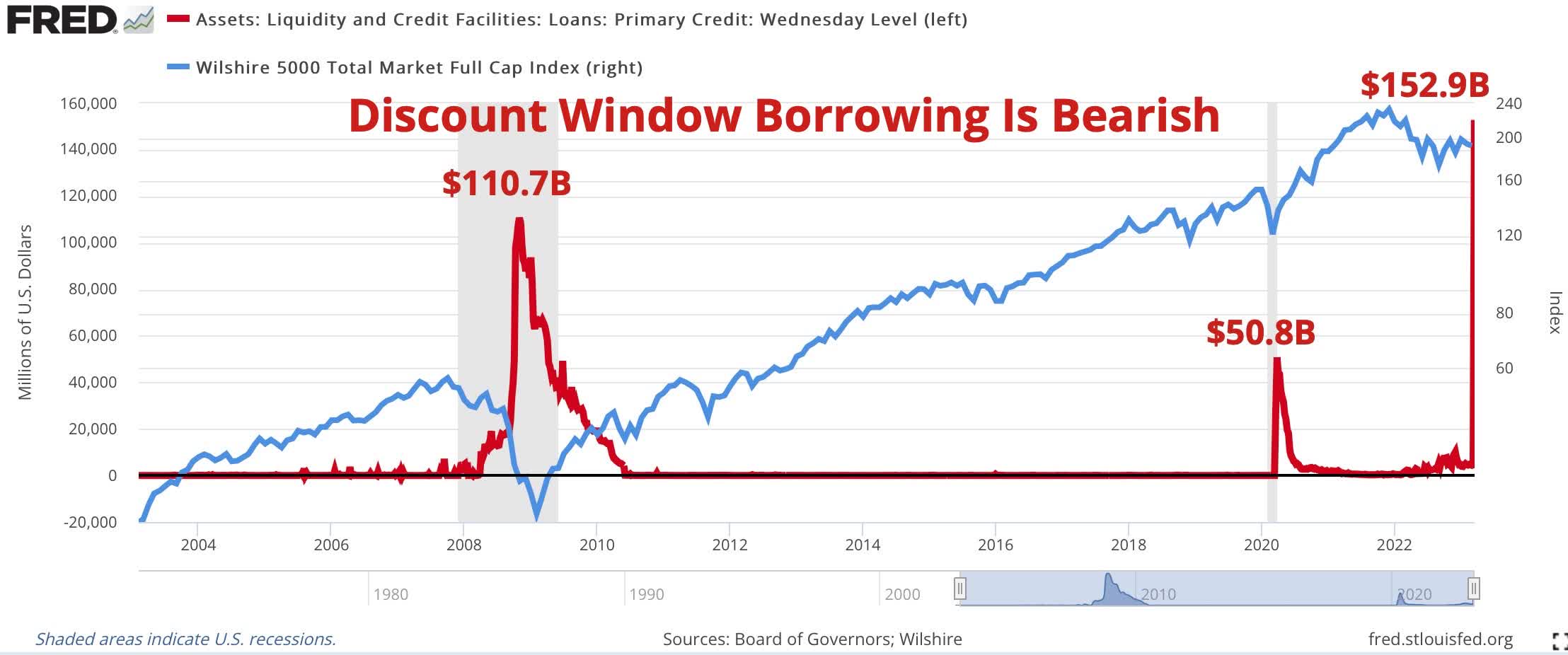

To try to pay off depositors, banks are now rushing to borrow money from the Fed’s “Discount Window” at the highest levels in history. As shown in the following chart, Discount Window borrowing (red line) is nearly 40% higher than during the depths of the Great Recession and three times more than during the Covid panic of 2020. Note that stocks usually fall significantly during periods of banking stress like this, as we saw in 2008 and 2020 with the broad Wilshire 5000 stock index (blue line).

{kind=link}

And this is all happening before banks suffer credit losses and the obvious signs of recession are occurring. Imagine what will happen when unemployment rises from current levels that are near 50-year lows.

Inflation Puts The Fed Between A Rock And a Hard Place

Inflation is still near 40-year highs and well above the Fed’s 2% goal. The Fed has been aggressively raising rates over the past year to try to bring inflation down before market interest rates rise to 10%+, as they did in the early 1980s. If that were to happen with debt levels near historical highs, there would likely be a massive economic, financial, and government debt crises that would dwarf anything happening now.

If inflation wasn’t such a problem, Powell and the Fed would likely be slashing interest rates and creating significant new money out of thin air to try to rescue all these banks and forestall a recession. But inflation is a major problem, and the Fed knows it.

After the money supply grew an unprecedented 40% due to the Fed’s aggressive easing in response to the Covid panic of 2020, the money supply is now falling 5% year over year. As banks tighten lending standards to try to protect their balance sheets and prevent bank runs, the money supply will likely fall even further, which will only deepen this recession.

Implications For Investors

With a banking crisis here now and a recession coming (if it hasn’t already started), we believe this is a very risky time for the stock market and other risk assets. Despite what Wall Street and most financial advisors says, investors do not have to “grin and bear it” and stay fully invested in stocks right now. They are free to put their money in much safer places such as money market funds and Treasury bill ETFs.

For investors who would like to speculate to potentially earn much higher returns from these troubled times, there are many inverse ETFs available to buy. These ETFs rise in price when the underlying asset, such as the S&P 500, falls in price. We discussed these alternative investments here .

Now is not the time for complacency. The risks facing investors are real, and they are mounting quickly. Use this as an opportunity to build wealth rather than suffer significant losses.

For further details see:

Banking Crisis Dramatically Increases The Odds For 'Hard Landing' Recession