XLF - Banking Crisis: Why It Could Be Far Deeper Than It Seems

2023-04-04 01:27:43 ET

Summary

- Silicon Valley Bank's failure to raise funds exhibits the growing non-marketability of existing long-dated U.S. debt.

- Instead of foreign institutions, U.S. institutions bear the greatest exposure to this growing effective markdown.

- The instability of the U.S. monetary system brings to the fore long-standing calls for the global financial system to diversify away.

The failure of Silicon Valley Bank (a subsidiary of SVB Financial Group (SIVBQ)) - as well as that of Signature Bank (SBNY) and many others seemingly on the brink of collapse - has recently been attributed to social media-driven fear in the minds of depositors and investors. In other words, some might argue that there is no cause for concern: the financial sector - while not perfect - is quite robust.

In actuality, a vicious cycle of risky business activities interplaying with government actions in recent times exacerbated and laid bare the shaky foundations of the financial services sector. An important key to understanding this is to examine how U.S. government debt issuances are consumed by the financial giants of the world.

Treasuries Become Foundations For Market Activity

Ordinarily, banks use cash from customers' deposits to provide loans to businesses and individuals. The interest payments on these loans ensure that the customers' deposits used effectively earn a (modest) amount as interest, along with the banks earning a (sometimes substantial) profit as well. Over the course of the pandemic and its associated lockdowns, borrowers wound down borrowing for business purposes while massive disbursements made by the government under various schemes resulted in borrowers often paying down their debts. For instance, commercial real estate developers and car dealerships declined to borrow to expand their businesses while high-interest-rate credit card holders paid their debts off with government stimulus packages. If debts are paid off, there is no interest receivable - which means that there is no cash stream to fund the interest payments on deposits or - for that matter - profits for the banks.

This is when the banks began to buy large chunks of what had lately been the least attractive asset to own: government bonds. After all, a yield that is slightly better than zero at no risk is better than no yield. The Federal Reserve had been inactive on the issue of creeping inflation for years by now and had been propping up the U.S. government's ever-increasing debt issuances by holding it, thereby effectively acting as a "market maker" of sorts. By all means it sounded like a best choice under the circumstances.

Theoretically, US Treasuries are supposed to be held to maturity wherein the holder gets paid. After all, a Treasury Bond is a loan undertaken by the U.S. government, which pays it off by the end of the specified period. However, the Basel III reforms enacted to regulate banks' investment activities added another form of utility: non-cash collateral. The Basel III framework demanded that banks set aside even more "additional capital" against the cash they set aside for trading (and risk-taking) than they had before. The rules effectively penalized banks if they were to fund themselves with short-term unsecured deposits to invest in longer-term assets. A cash deposit made in a customer account that can be withdrawn at a moment's notice therefore cannot necessarily be considered "safe cash" set aside to cover cash used in trading. Banks were required to access high-quality liquid assets ("HQLA") in a significantly greater volume than before to cushion their investment activities. Naturally, U.S. Treasuries proved to be a beneficiary of this demand.

It wasn't necessary that only an investment bank would hold U.S. Treasuries; a smaller regional bank could lend U.S. Treasuries from their vault to another party - a large investment bank, for example - for a fee. After all, banks are in the business of making loans. When markets are booming, U.S. Treasuries remained in demand as non-cash collateral all over the world.

Things Take a Turn

When the Federal Reserve couldn't ignore rising costs that were hurting citizens any more, it finally began to raise rates - which was arguably long overdue. The U.S. government's debt issuances, thus, came with a higher yield than the several trillions in debt already in circulation. This began to affect the balance sheets of banks awash in U.S. Treasuries. At the end of 2022, Bank of America ( BAC ) held $ 3 trillion worth of debt securities, which was represented at a value of $862 billion. While accounting rules specify that banks don't have to record losses due to change in value of these securities unless they were sold, the bank recorded $114 billion as "unrealized losses" for its bond portfolio. Wells Fargo ( WFC ) recorded $41 billion; JPMorgan ( JPM ) recorded $36 billion and so forth.

It bears remembering that this is an entirely voluntary disclosure. At the time when regulators were seizing Silicon Valley Bank, unrealized losses of $15 billion were estimated on a bond portfolio of just $91 billion. The bank had tangible capital amounting to a total of just $16 billion. Silicon Valley also specialized in "venture debt" wherein the company made unsecured loans on new tech companies and start-ups who also maintained deposits in that bank. When the rate hikes made their debt more expensive, they pulled their deposits. When the deposits were pulled, the bank had to liquidate its assets. Initial attempt to sell a portion of its U.S. Treasury portfolio failed. Eventually, the bank managed to sell its bond portfolio with a book value of $23.97 billion at a $1.8 billion loss to Goldman Sachs ( GS ).

Now, analysts through the years have held that the U.S. debt market is one of the most liquid in the world - a contention that even the Federal Reserve System holds. Backing this is the seeming widespread foreign ownership of U.S. debt.

Source: Visual Capitalist

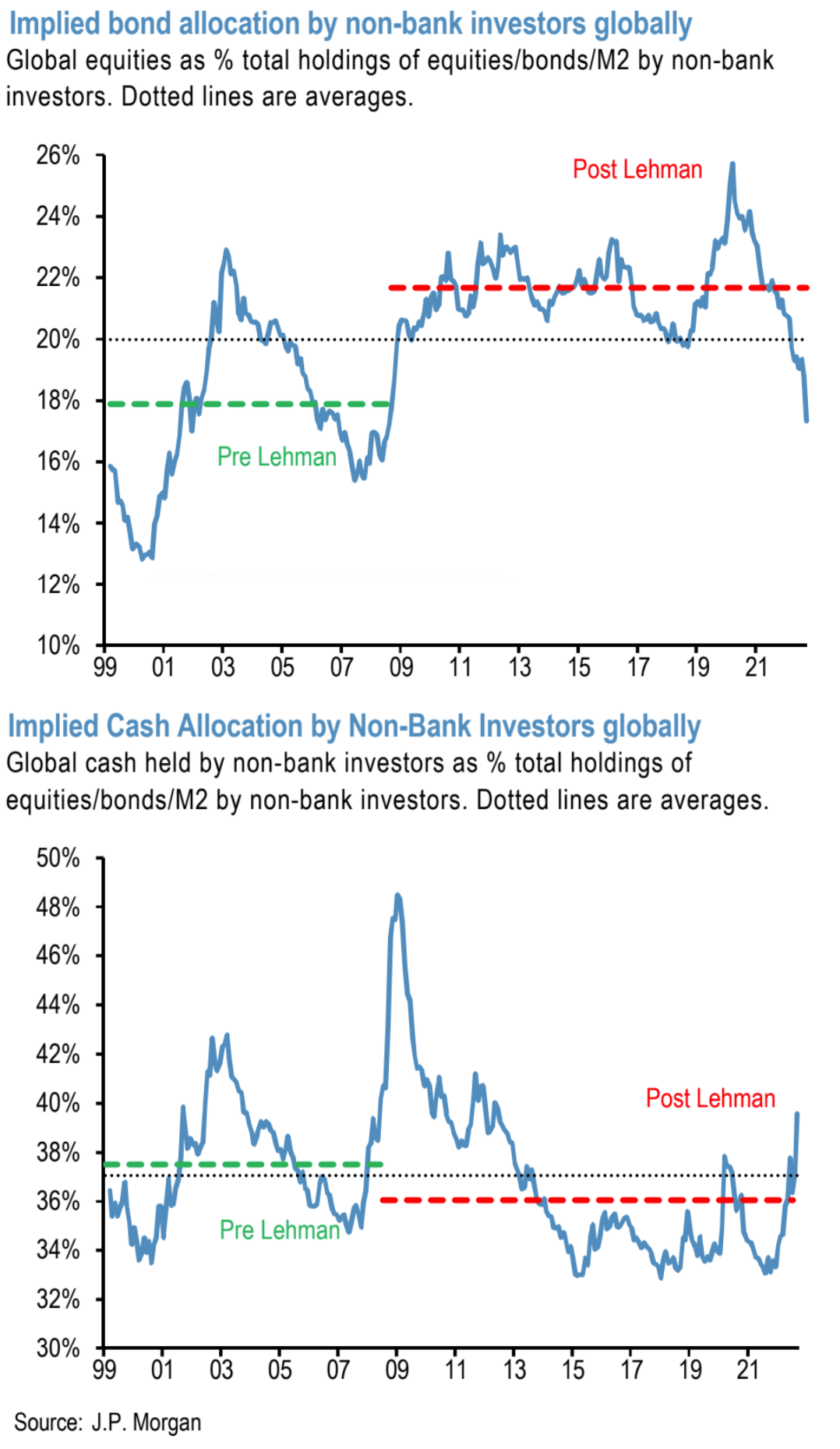

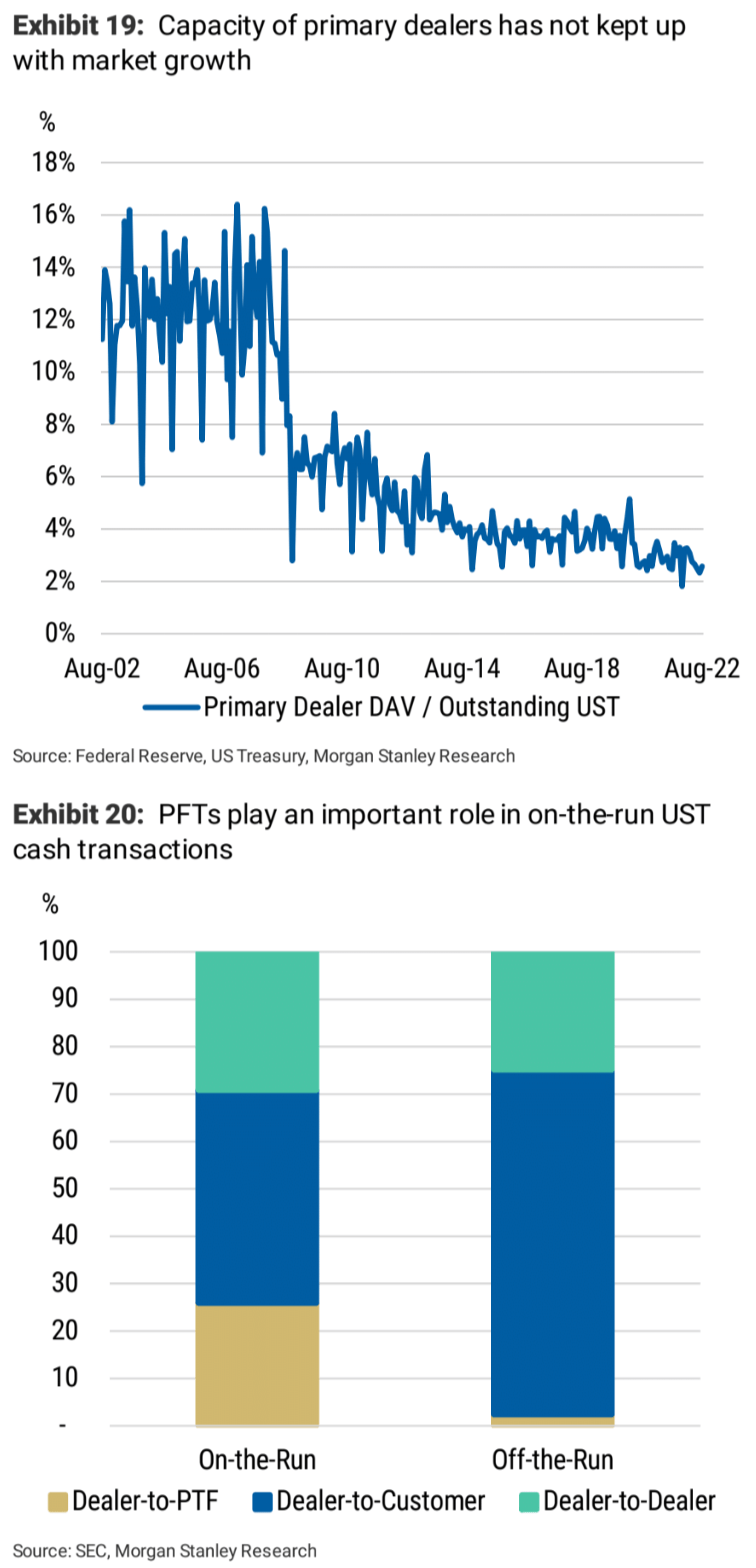

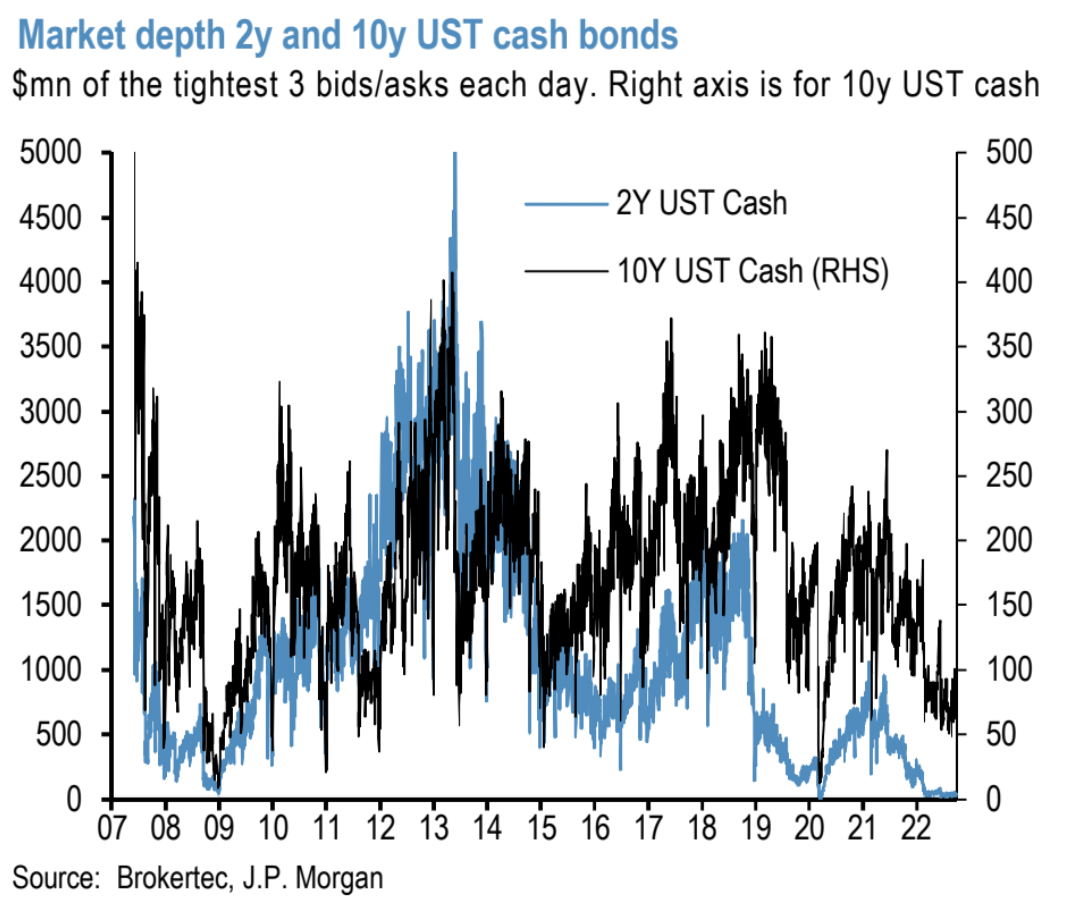

One reason a loss had to be booked when selling U.S. debt is that the market had shrunk to a handful of participants. Towards the end of September last year, JP Morgan had indicated in one of its Flow Reports that bond portfolios by "non-bank investors" have shown significant shrinkage over the years.

{kind=link}

In the same month, Morgan Stanley ( MS ) had stated in a similar report that bonds have been increasingly unattractive to individual investors since the end of 2008 Financial Crisis. The primary players in government bond markets have largely been reduced to foreign central banks, mutual funds and insurance companies.

{kind=link}

As a result, bond traded volumes relative to outstanding US Treasuries (as indicated in the top half of the image above) has seen a significant decrease in the present day. Furthermore, JPMorgan indicated that market depth - a signal for how active bond markets are - for the highly-popular 2-Year and 10-Year Treasury Bonds (also referred to as "Cash Bonds") had almost completely evaporated in the present day.

{kind=link}

Foreign central banks buy U.S. debt issuances as policy tools. Given that these issuances guarantee delivery of the U.S. dollar, it could be considered as a proxy of the U.S. dollar to balance the books of trade. However, the highs of the U.S. dollar have created the need for foreign central banks to defend their currencies. The U.S. central bank's Foreign and International Monetary Authorities (FIMA) repurchase agreement facility, established in March 2020 to enable foreign central banks to post their US Treasury holdings as collateral in exchange for U.S. dollars, recorded the fastest liquidation of U.S. Treasury holdings in nine years after $60 billion in cash was pulled.

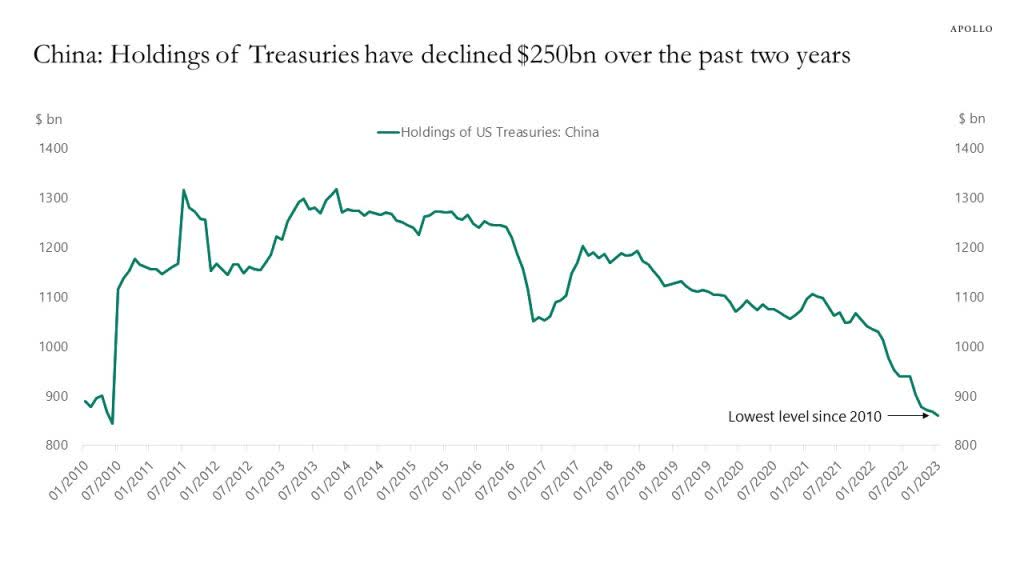

The People's Republic of China - arguably one of the U.S.' most important trade partners in most matters outside of energy - has been particularly vociferous in its defense of the trade balance and its currency. While the State and its various institutions held around $1.3 trillion in U.S. Treasuries in 2013, they now hold $850 billion , with the selling of U.S. debt accelerating over the past two years.

{kind=link}

Now, while the more hyperbolic of media outlets might make much ado about foreign debt holders and the potential for influence into U.S. matters, it bears noting that only about 30% of the U.S. government's debt is held by foreign entities. The rest of it is owned domestically. One of the largest holders is the Federal Reserve itself with over $7 trillion, despite efforts to lighten the balance sheet. Other holders have traditionally included various Medicare trusts , state and local government as well as a variety of businesses, estates and government-sponsored enterprises.

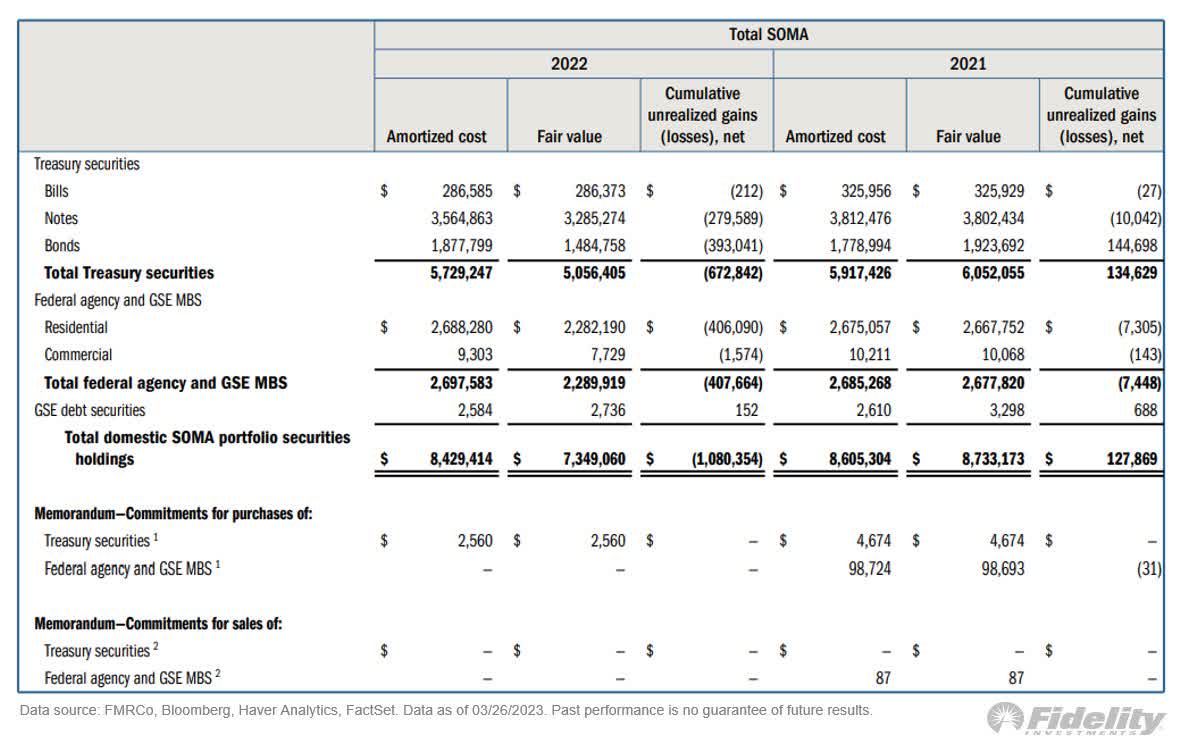

Recently, the Federal Reserve System has estimated an unrealized loss of over one trillion dollars.

Source: Fidelity based on Releases by the U.S. Federal Reserve

{kind=link}

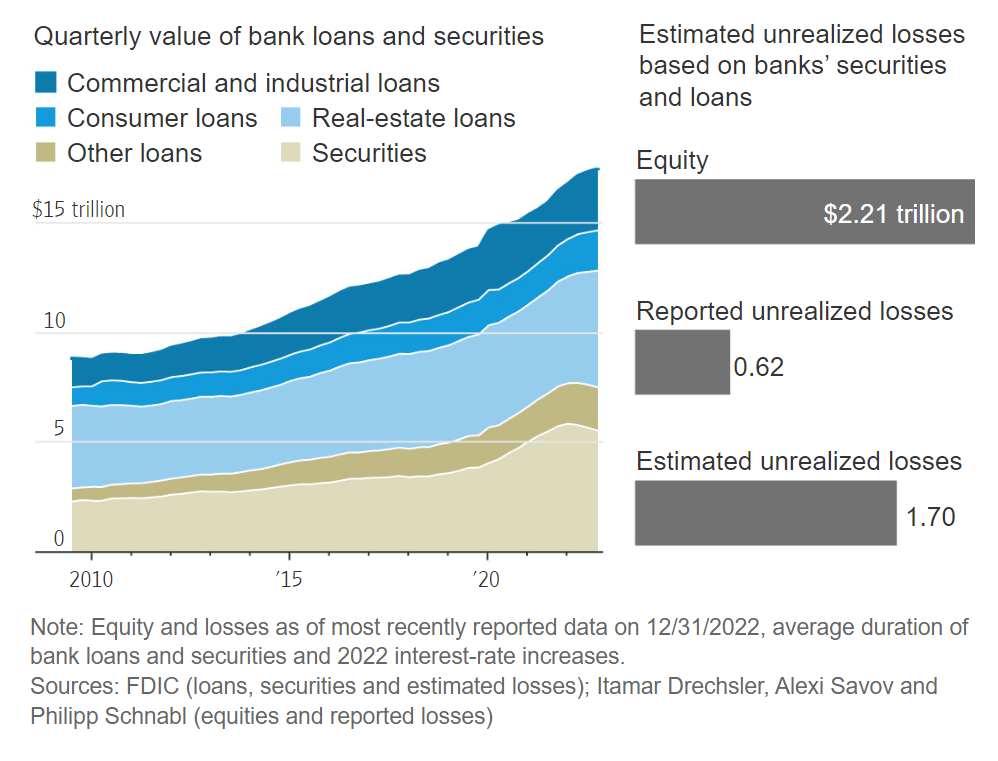

While U.S. banks have collectively declared over $620 billion in unrealized losses, some recent studies estimate actual unrealized losses for the banks to be at over $ 1.7 trillion . In other words, the unrealized losses declared are still some way away from the actual picture in the present.

Visualization by Wall Street Journal based on data from FDIC

{kind=link}

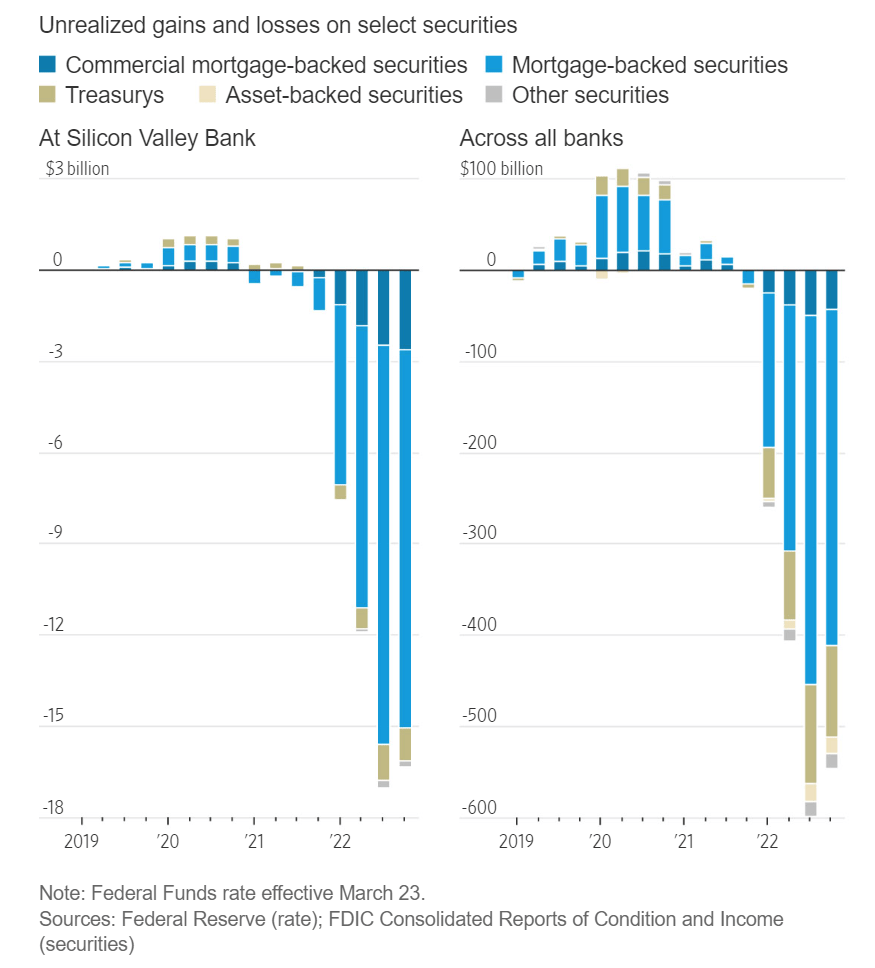

It's not just U.S. Treasuries that are burgeoning with unrealized losses. Mortgage-backed instruments - where are effectively guaranteed by the U.S. government - are also leading in unrealized losses.

Visualization by Wall Street Journal based on data from FDIC and the U.S. Federal Reserve

{kind=link}

Mortgage loans have seen rising interest rates which, in turn, have had a couple of interesting effects: homeowners with "locked-in" low rates from 2020 or 2021 are unlikely to prepay or refinance while home-buying activity is expected to be grim this year. Since the bank holding the mortgage-backed bond is also "locked-in", there isn't enough capital for banks to provide for newly-issued mortgages. This will create significant downward pressure on the mortgage market.

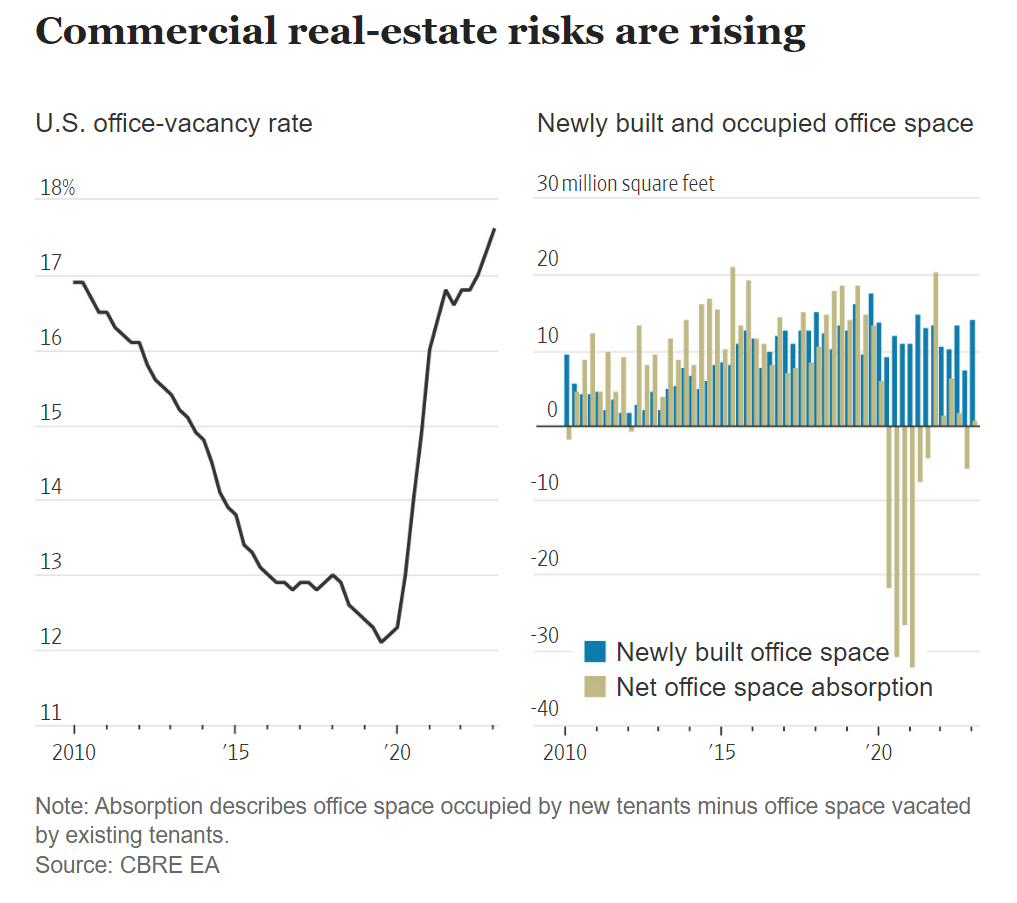

On the commercial mortgage space, frenzied commercial building activity in the U.S. over the past several years might have led to a gross overshooting of demand. The CBRE estimates that roughly 1 in 5 office buildings are currently vacant, with net availability in cubic feet terms being grossly outsized relative to net absorption.

Visualization by Wall Street Journal based on data from CBRE

{kind=link}

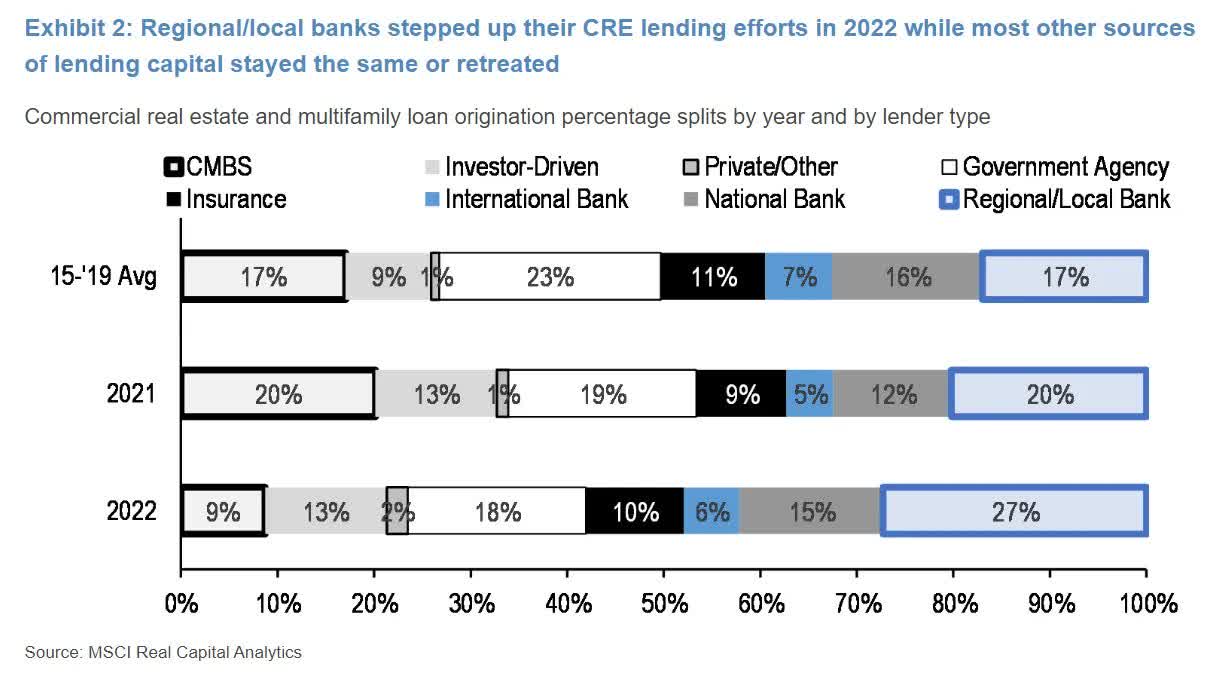

Nearly $30 billion of the approximately $160 billion in commercial real estate loans maturing in 2023 are now past due. A key segment that has provided commercial real estate ((CRE)) loans is the regional small bank. Unfortunately, this means that the stressors on these banks are far from diminished.

{kind=link}

Key Takeaways

Silicon Valley Bank's collapse evoked an interesting response from the government: instead of limiting the protection of deposit accounts at $250,000, the U.S. government guaranteed that the entirety of deposits was safeguarded while the bank's stock and bond holders were left high and dry. This is entirely different from the level of protection accorded to big banks, which are deemed "Systematically Important Banks" (SIBs) and indicative of a two-tier system in place where there should be none. Nonetheless, the divergence in the rescue operation for depositors at SVB evokes hope that similar protection would be extended to other small banks despite the fact that the U.S. Treasury Secretary has remained non-committal in stating so outright. An omission of statement is a cause for stress in the lower end of the spectrum of banks that comprise the financial services sector. This also imparts a survivability bias towards the SIBs and those closest to them than the rest.

While sky-high U.S. dollar valuations continue to trigger Treasury selloffs from foreign central banks and a downward pressure on U.S. debt valuations, they also create lower depositary balances as rising costs eat into savings. This, in turn, will continue to trigger further rate hikes and continue to lower valuations of past U.S. debt issuances. This is an entirely different vicious cycle at play in this sector from the cycle of banks' activities relative to Treasury actions. For these two vicious cycles to be tempered, there will likely be calls for further reformation of banking activities while work will continue on improving a string of indicators signifying a sustained climb-down of both the U.S. dollar as well as living costs.

At this current juncture, it is impossible to predict this happening any time this year with certainty. On a technical basis, there are two issues. The first is the lack of marketability of older U.S. debt that makes the banks' reported MTM ("Mark to Market") and, in turn, their book value entirely suspect. It's a system-wide issue that should - ideally - be addressed via appropriate levels of markdowns.

The second is an ever-persistent issue: is U.S. debt's "premium rating" justifiable, given the shocks created in the system due to the government's overdependence on debt issuances. Over the years, the issue of credit ratings agencies' lack of objectivity and bias towards U.S. debt instruments has been discussed with little by way of remedy. It could very well be argued that the cornerstone of modern financial systems - at least in the Western Hemisphere - being centered on the U.S. monetary system and its inherent indiscipline is a "systematic risk". While the Basel III framework seems to indicate a preponderance of preference for HQLAs, this could be addressed via a carveout for diversification for risk mitigation. While it is a monumental task, it isn't impossible . If/when that happens, there will be a transformative paradigm shift for the U.S. financial sector, with deep ramifications for the U.S. government.

All in all, a close eye is merited on events and indicators as they transpire and update respectively.

For further details see:

Banking Crisis: Why It Could Be Far Deeper Than It Seems