SCGLY - Banks Are On Sale But Risks Remain

2023-04-11 07:55:08 ET

Summary

- One month ago, Silicon Valley Bank failed, with a resulting decline across the diversified banking industry.

- Some investors may be tempted to buy the dip, while others are considering doubling down on losing positions.

- However, the industry may remain risky even at bargain prices with unrealized losses on Treasury bonds and mortgage-backed securities.

- Further, Silicon Valley Bank was not entirely an outlier with regard to its exposure to mortgage-backed securities or its ratio of cash to total deposits.

- Investors are once again cautioned to consider every investment carefully and on its own merits.

Why Are Banks On Sale?

On March 10 , Silicon Valley Bank ( SIVBQ ) failed and was taken over by regulators after the bank ran face-first into $42B in withdrawal requests. Notably, just two weeks earlier on February 24th, auditor KPMG LLP gave Silicon Valley Bank a clean bill of health . The failure of SIVBQ resulted in a loss of investor confidence in the financial sector and, perhaps most notably, the diversified banking industry.

Investors are rightly concerned that Silicon Valley Bank's troubles may represent unrecognized risk across the diversified banking industry. Broadly speaking these risks can be considered in two categories: unrealized losses on safe assets and a bank's ability to honor customer withdrawals .

Most banks invest in a core portfolio of safe assets, including U.S. Treasury bonds and mortgage-backed securities . However, when interest rates rise quickly, fixed yields on these assets do not keep up with rising rates. Consequently, these assets are often no longer worth what the bank paid for them , and a bank's balance sheet can include alarming unrealized losses on these assets.

A bank's ability to honor customer withdrawals is foundational to not only it's clients' confidence, but also that of investors. Rightly so. However, a bank's ratio to cash and cash equivalents versus total deposits can vary broadly. For reference, according to YE '22 figures, Silicon Valley Bank held cash and cash equivalents equal to about 3% of total deposits.

Potential Bargains

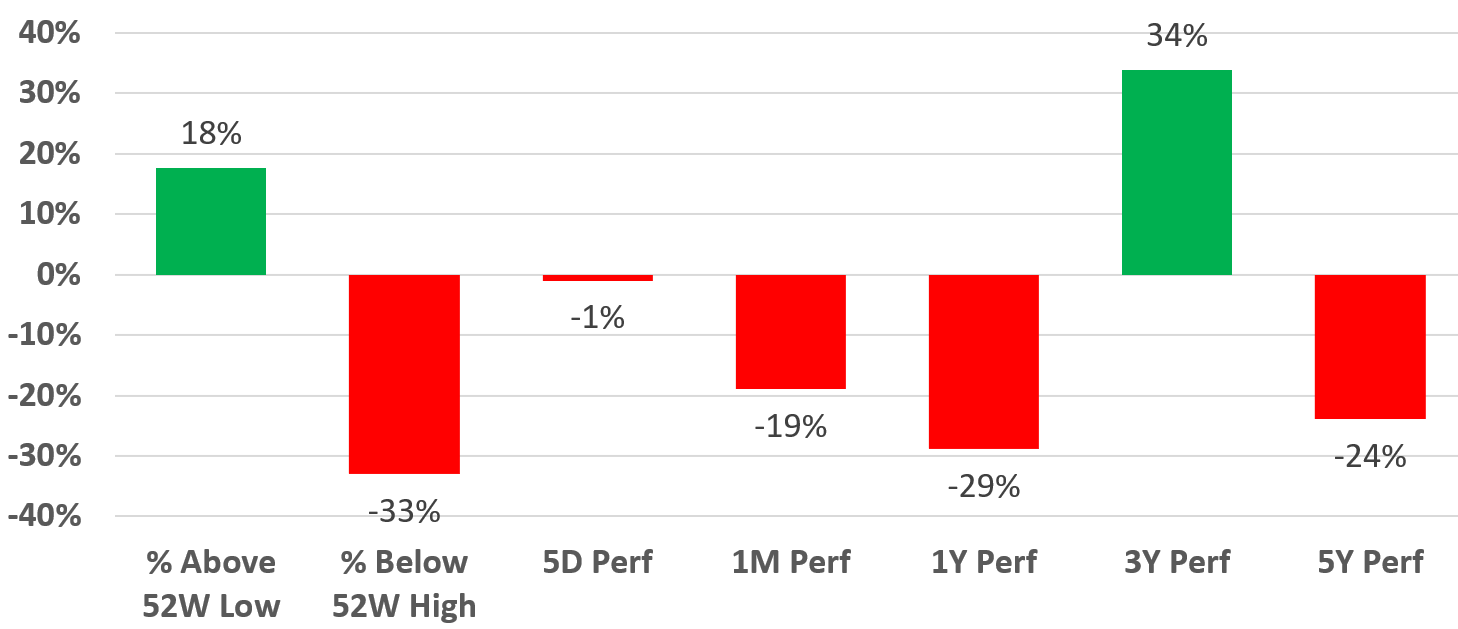

Seventeen diversified banks (to be listed below) with Morningstar Ratings of Buy or Strong Buy were selected for further analysis. The average performance of these 18 banks is summarized in the plot below.

Diversified Banks: Average Performance

{kind=link}

If teardrops were diamonds, many investors would already be fabulously wealthy on these banks. As a group, they are down over every time period shown except 3 years. The positive 3YR performance reflects a strong recovery from pandemic lows and might indicate another strong recovery is possible.

Relative Value and Risk Analysis

The 18 selected banks were evaluated using a value & risk matrix. Value factors include PE MRFY vs. 5YR average PE, 1YR PE change, and percent below 52-Week high. The risk factors considered include the ratios of mortgage-backed securities to total assets and cash & cash equivalents to total deposits. The values for each company's factors were normalized by means of statistical percent ranking with relation to the group. The value & risk matrix was calculated as the sum of the percent ranks of the factors. For the sake of gut-checking edification, SIVBQ was also included.

Value & Risk Matrix Chart

{kind=link}

The above chart is sorted in descending order of the best value & risk profile (highest matrix score) to the poorest value & risk profile (lowest matrix score).

Value & Risk Matrix Chart

Author, SA Data

The value and risk matrix is presented graphically in the stacked bar chart above with cumulative inputs for each factor. Based on this analysis, the "bargain" banks with the most favorable combination of value and risk are:

- Comerica Incorporated ( CMA )

- SVB Financial Group

- Zions Bancorporation, National Association ( ZION )

- HSBC Holdings plc ( HSBC )

- Huntington Bancshares Incorporated ( HBAN )

I promised readers gut-checking edification; SIVBQ (the parent of Silicon Valley Bank) closed today at $0.61, or about 99.9% below its pre-crisis share price of about $268. To be clear, I'm not suggesting that investors buy SIVBQ; emergency measures to protect depositors do not extend to shareholders. Notably, SIVBQ's ratio of mortgage-backed securities to total assets was the highest in the group at 43%. However, its ratio of cash and cash equivalents to total deposits (even at only 3%) was higher than that of 35% of the group.

Quality Matrix Limitations

Investors should consider the value & risk matrix a screen only. The matrix and its factors, normalization method, and weights could all be adjusted and yield different results. Further, the matrix is based on the most readily available and common metrics. These metrics can change rapidly with share price or as new company reports are released. It does not include company-specific data available in quarterly reports and presentations.

Potentially impactful risks, including unrealized losses on Treasury bonds , are not addressed in this analysis. Further, many banks are facing an exodus of deposits as clients move capital to cash management accounts for higher yields.

Conclusions and Recommendations

I'll admit, many investors are likely to have a higher risk tolerance than my own; I am both conservative and risk-averse. I happen to be enjoying an ocean view retirement in Hawaii, but I'm barely two generations removed from subsistence farmers. Therefore, I am not sporty with my capital. If I cannot confidently quantify both potential return and risk on any given opportunity, I don't invest.

Bargain hunters are reminded that auditor KPMG LLP gave Silicon Valley Bank a clean bill of health just two before its failure. Investors are once again cautioned to consider every investment carefully and on its own merits.

If teardrops were diamonds and only mine were used, they could pave every highway coast to coast.

- Dwight David Yoakam

For further details see:

Banks Are On Sale But Risks Remain