IYY - Banks Down Big Tech Up? Beware Of De-Dollarization

2023-04-26 14:21:32 ET

Summary

- The overall financial sector is decidedly mixed: larger banks are being deemed inherently more survivable than small banks.

- Flows indicate a preference for size, with Big Tech being a prominent beneficiary. These flows are a self-fulfilling prophecy for survivability.

- Accelerating global de-dollarization implies moderate inflationary pressure will be a clear and ever-present feature for decades to come.

It should be clear by now that the U.S. is headed towards a recession in all but the "technical" sense, i.e., unemployment figures aren't nearly high enough to call the current period recessionary. However, data coming out of the banking sector bring with it a number of indicators.

Global macroeconomic consultancy TS Lombard published that, as of January this year, small banks in the U.S. were critically low on deposits and had starkly low liquid reserves.

{kind=link}

Small banks were heavily dependent on loans contributing to their balance sheet at a time when lending activity was heavily distressed. In the midst of the collapse of Silicon Valley Bank and Signature Bank, the entire financial sector was under a lot of pressure. Small banks saw a massive drop in weekly deposits through the course of March, which hadn't fully recovered by the end of the month.

{kind=link}

However, closer inspection reveals that small banks' reserves-to-assets ratio continue to look fraught while those of big banks are on an uptrend.

Visualization by ZeroHedge based on Bloomberg Data

{kind=link}

Recent earnings releases confirm this trend . Broadly, while the banking sector's prospects were imputed with bearish expectations by analysts, big banks did marginally better while smaller banks generally didn't. Now, classical market empiricism suggests that while the consumer discretionary sector is supposed to be attractive in a recessionary period, financials tend to hold firm. Classical market empirics no longer hold true in my view.

Big Tech: Size Matters?

Over the past two weeks, market flows have been imparting momentum in some interesting directions. For example, in the week prior to last (i.e., Week 15), tech companies drove a substantial part of the momentum in the S&P 500 ( SPX in index form and SPY in ETF form):

{kind=link}

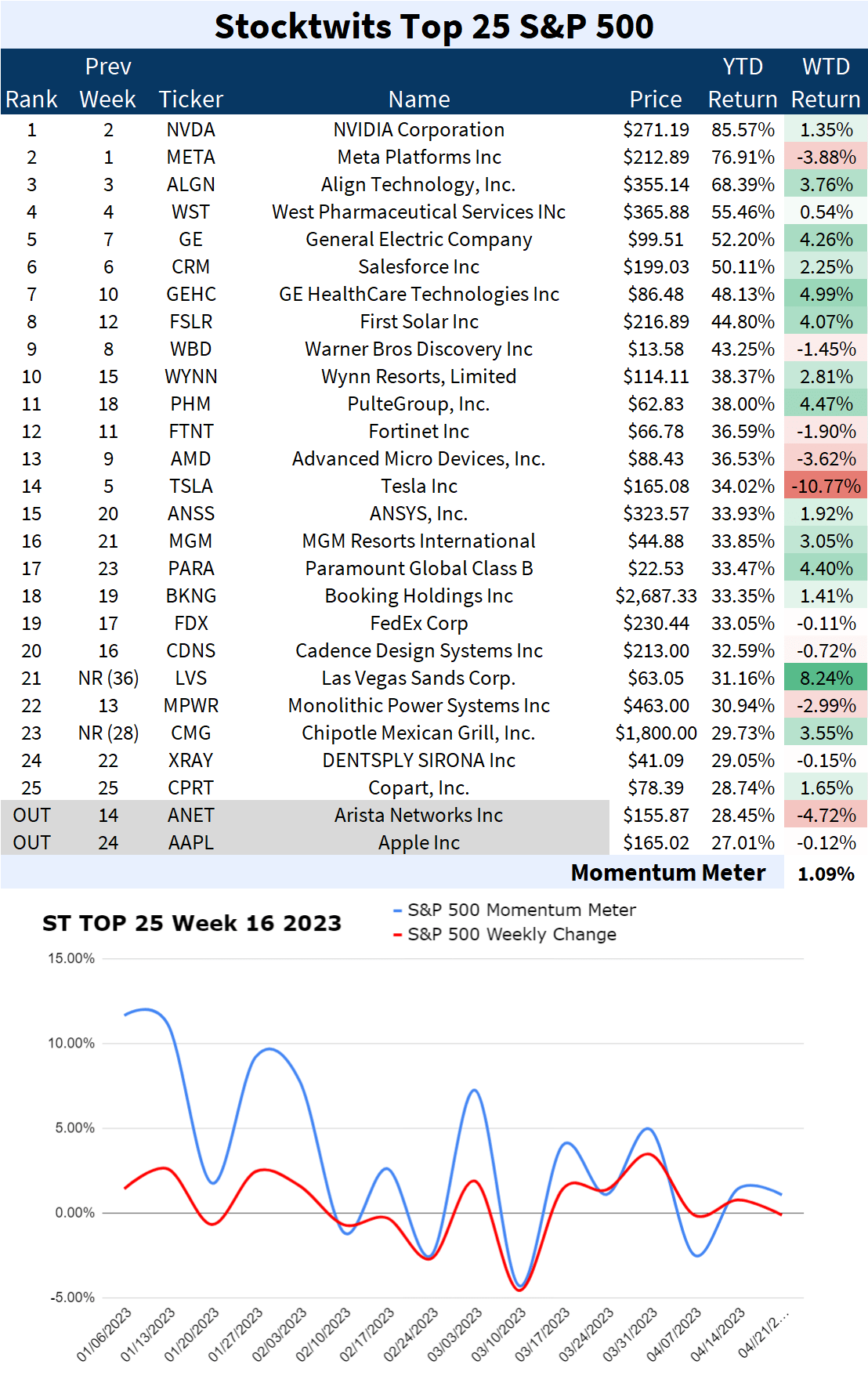

Also making a presence felt were a small number of leisure stocks - casinos, resorts, et al - along with the sundry pharma stock. In Week 16, the same pattern continued:

{kind=link}

The significance of the Top 25 on the directionality of the S&P 500 can also be seen in the growing correlation between their combined momentum and the index's weekly change.

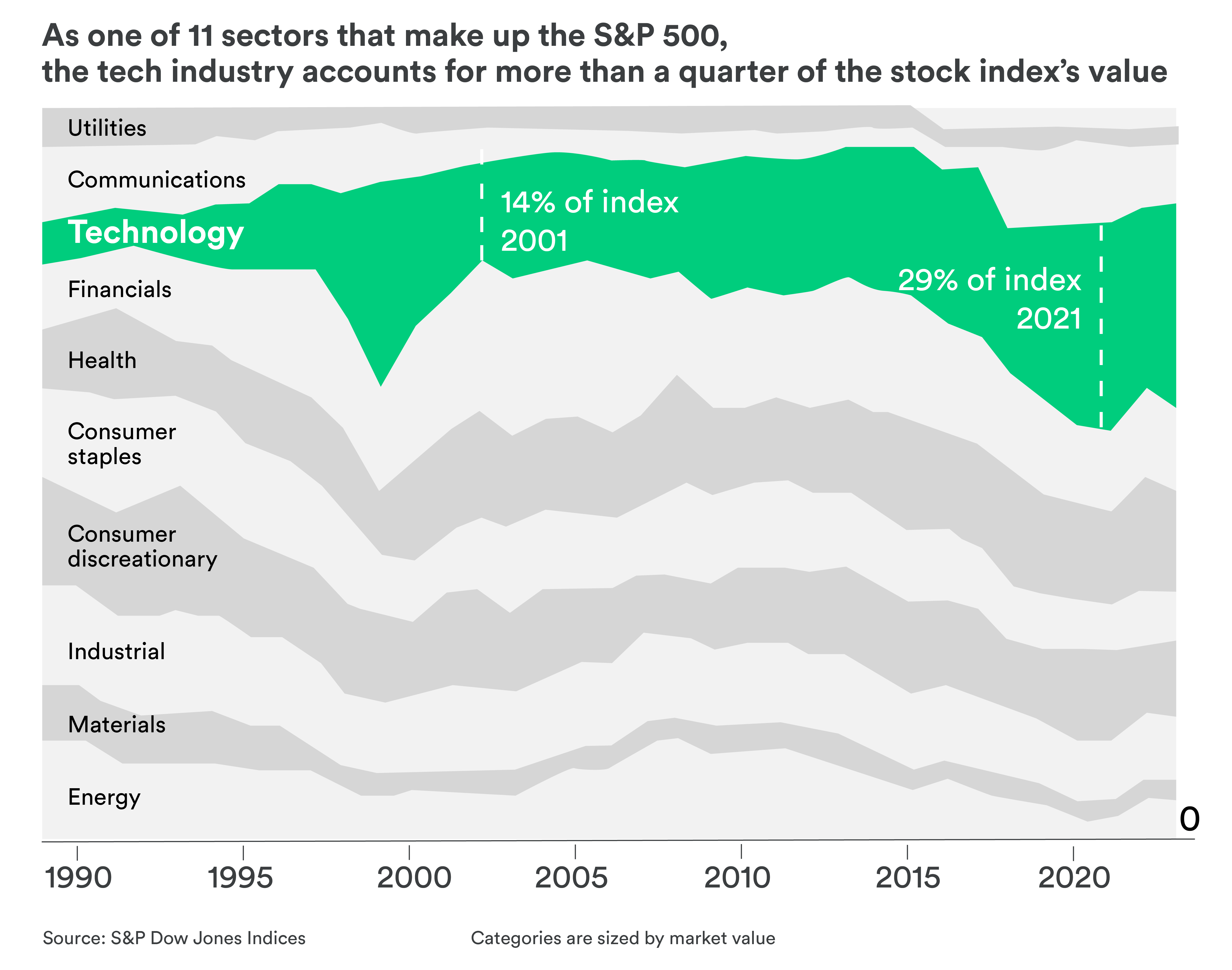

The preponderance of Big Tech in the Top 25 - and its relative impact on the economic bellwether - has been increasing over the past years. "Technology" had gone from comprising a little under 15% of the S&P 500 to nearly a third.

{kind=link}

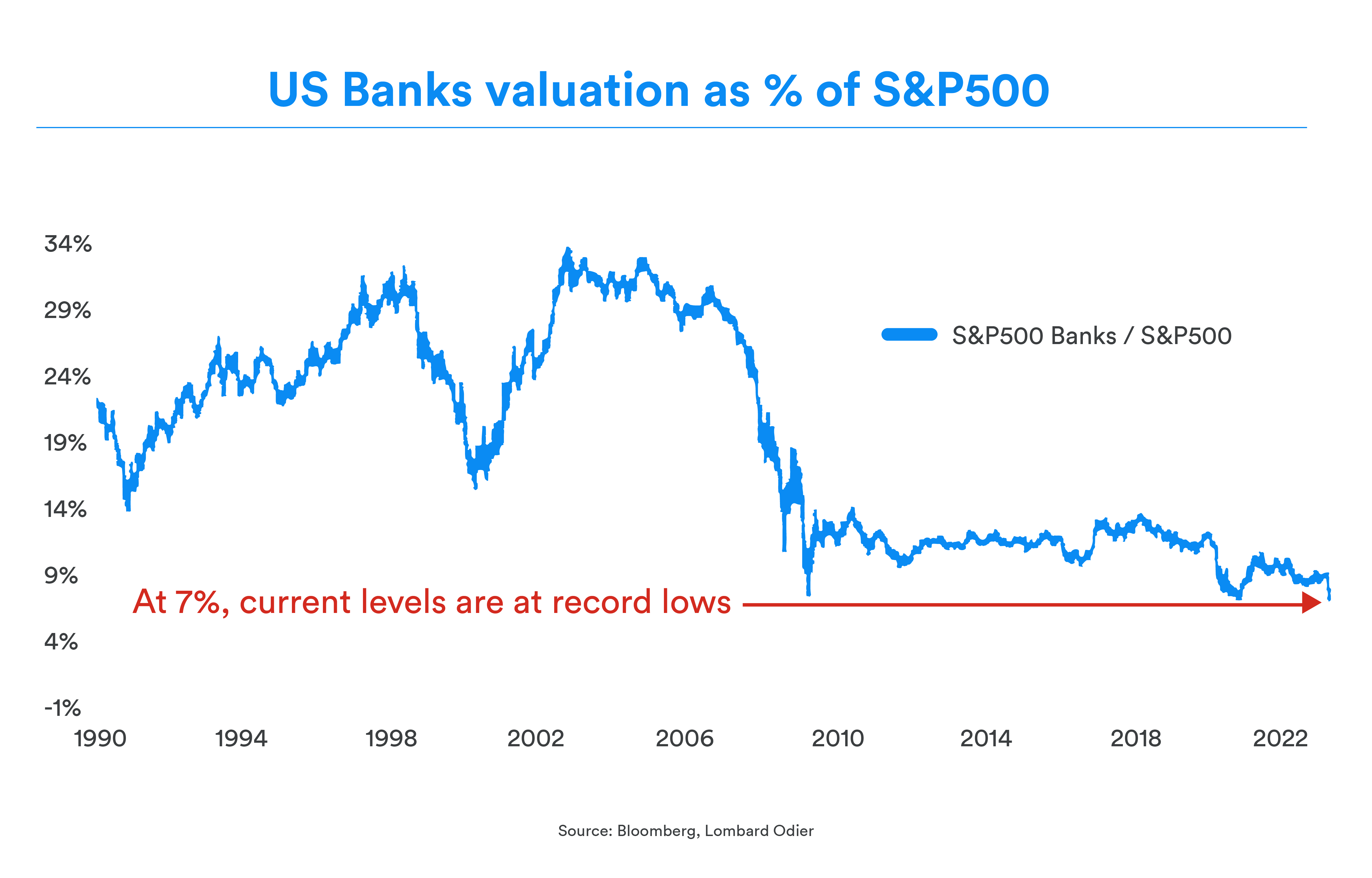

Meanwhile, the banking system has gone from being over a quarter of the top-of-the line economy to a single-digit percentage contribution.

{kind=link}

Given that the present economic outlook sounds all warning bells on lowering consumption being expected, the rise of Big Tech stock trajectories is a cause-and-effect phenomenon: more investors are apparently shifting to the view that Big Tech will remain ubiquitous and central to economic activity, while companies (even tech) on the lower end of the size spectrum being implied to have lower survivability.

Classical market theory would have one estimate that Treasury debt would be the least-worst option in such an outlook, i.e., it's better to earn something rather earn nothing or lose. The U.S. debt market, however, hasn't seen substantial inflows and variegation in terms of dominant players. In effect, they remain the same mix of institutional players: foreign central banks, insurance companies, banks and government bodies themselves.

I believe one reason for this is that, over the long term, the present rate of issuances are not deemed viable due to steadily accelerating "de-dollarization".

Does the World Need a Reserve Currency?

Note: Parts of this section are excerpted from another article by the author in other publications.

The de facto status of the U.S. dollar has virtually no grounding in the nation's stability, political process, etc. In actuality, this has a historical basis: in the course of World War II, the U.S. ended up with a substantial portion of the world's gold reserves since Allied nations paid for weapons and goods with their gold reserves. Given their depleted reserves, the Allied nations decided in the New Hampshire town of Breton Woods they would link their currencies to the gold-backed U.S. dollar as long as the U.S. promised to redeem U.S. dollars for gold on demand. The elevation of the U.S. dollar had an implicit covenant: the U.S. dollar would be as stable and only as plentiful as the nation's gold reserves. Given the size of the economy, post-war oil exporters denominated oil contracts in U.S. dollars while reserve banks worked to ensure that an average of two-thirds of their currency reserves - maintained to battle currency fluctuations - were in U.S. dollars.

The fall of the U.S. dollar from being a "preferred currency" also had a historical basis: the U.S. government flooded the market with "paper dollars" - currency not backed by the nation's gold reserves - as the Vietnam War imposed massive costs in the 1960s while President Lyndon B. Johnson concurrently pushed forward the "Great Society" domestic programs aimed at boosting education, Medicare and urban beautification while battling poverty and crime. When nations began to cash out their dollars for gold in light of this flood. President Richard Nixon suspended the dollar's convertibility into gold in 1971, leaving the Breton Woods agreement in tatters. The massive volume of trade involving the U.S. notwithstanding, the effective elimination of the U.S. dollar's connection with the "gold standard" effectively made it like every other currency, i.e., a by-product of governmental discretion.

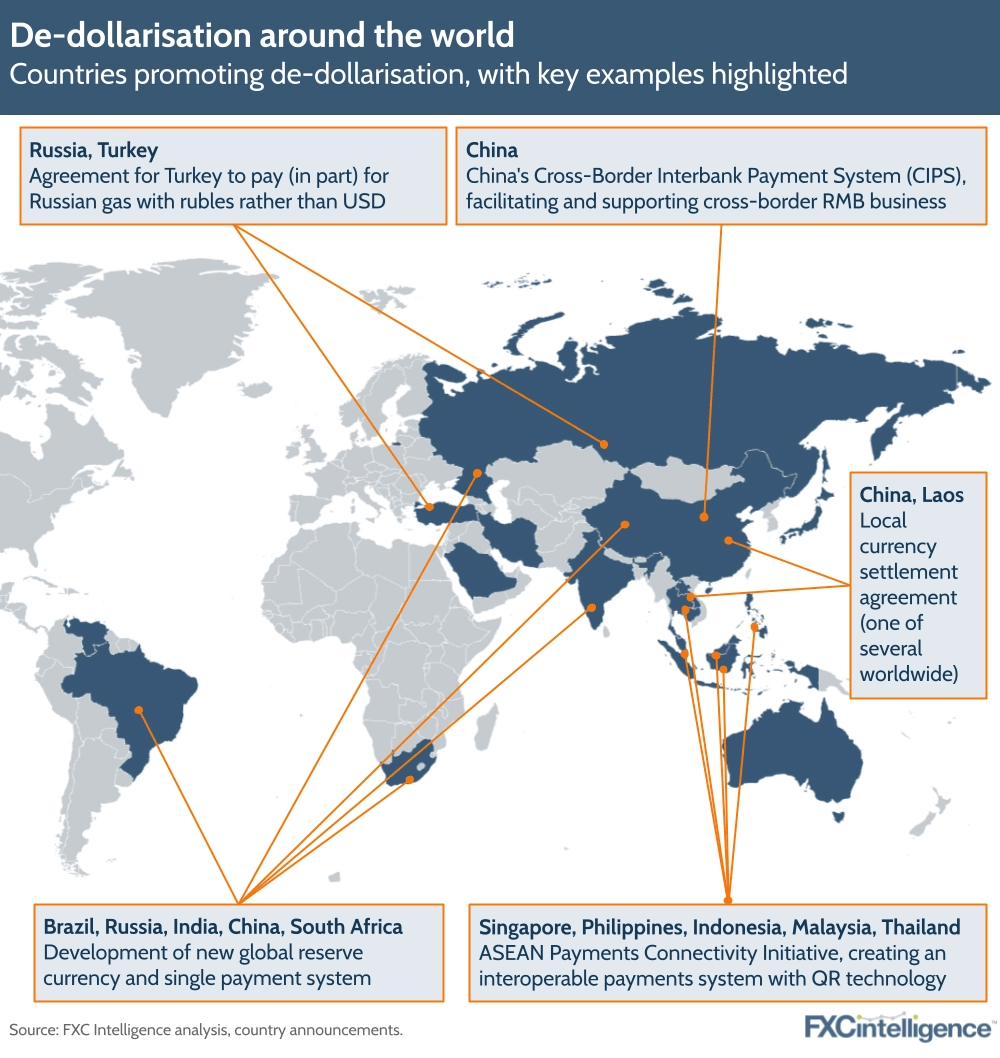

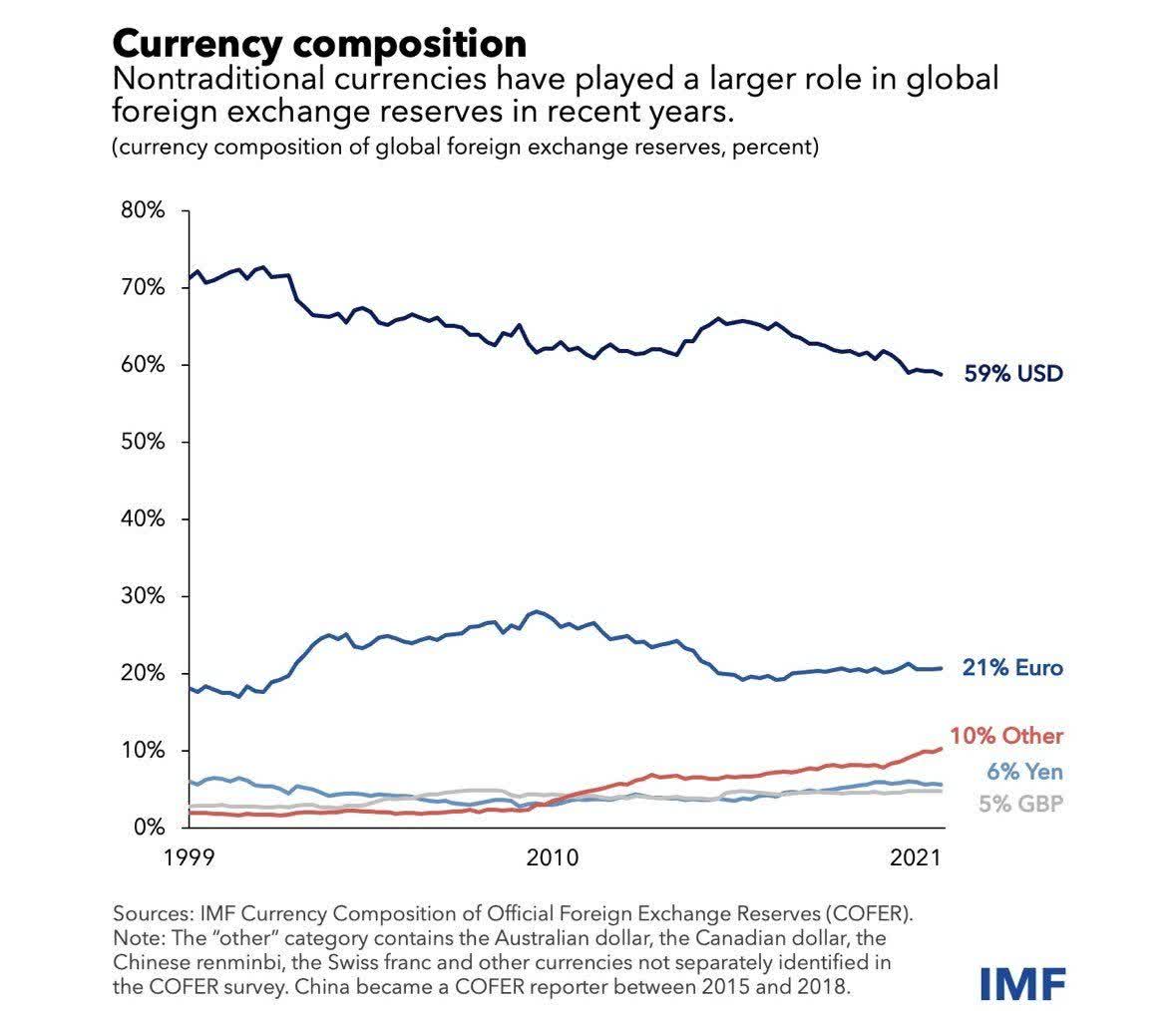

Intuitively, it could be argued that - without an access to outright gold - a basket comprising of currencies in any strong and well-established trade network could act as an impetus towards diversifying away from the U.S. dollar. In recent times, this has in fact been happening.

{kind=link}

18 countries - including Germany, Kenya, Sri Lanka, Singapore, the United Kingdom and Malaysia - have agreed to trade in Indian Rupee. China has signed agreements with 41 countries for clearing bilateral trade in Chinese yuan. In March of last year, it was reported that Saudi Arabia was considering accepting Chinese yuan for its oil exports to the People's Republic of China. The BRICS (Brazil, Russia, India, China, South Africa) bloc is now considering expanding after Saudi Arabia and Iran formally requested to join the group. The United Arab Emirates and India have started talks to settle the oil trade in Indian Rupees - with Russia and Iran also looking to forge similar arrangements. It seems logical that the Indian Rupee would also be included into the IMF's Special Drawing Rights (SDR) - conceived in 1969 as a "supplementary international reserve asset" equivalent to a fractional amount of gold that was equivalent to one US dollar at a time when the latter was backed by gold - in the next couple of years. In the present day, it is a basket consisting of five currencies: the U.S. dollar, the Euro, the Chinese yuan, the Japanese Yen, and the British Pound Sterling.

The importance of regional trading blocs cannot be overstated: long before the fall of Gaddafi and Saddam (which, as per many anti-war activists , was engineered to prevent the replacement of the U.S. dollar), foreign currency reserves around the world have already been "de-dollarizing" owing to the momentum of trade.

Source: International Monetary Fund

{kind=link}

The Russo-Ukrainian conflict also saw the U.S. dollar's inherent weaponization as an instrument of aggressive statecraft by the U.S. government. While many would argue that this is a necessary part of conflict handling, it also undermines the status of the U.S. dollar as a reserve instrument for booming economies who would prefer to remain neutral. Without alternatives, they run the risk of being railroaded into joining sanctions they don't approve of and losing trade partners. The seizure of dollar assets owned by key Russian figures that weren't officially part of the Russian government early on in the conflict seemed to have proved to the minds of many that going your own way may be difficult but is hardly a wasted endeavor. This is the inevitable cost of weaponization.

The inherent draw of holding the US dollar - either as long-term debt or as cash reserves - will likely continue to erode in my view. This is a powerful signal to the U.S. Treasury that finding a buyer for its near-continual issuances will prove to be increasingly difficult. Given that U.S. expenditure far, far outstrips U.S. revenues, the question that emerges is: who will relay this to America's political establishment and can they be enjoined to be more fiscally conservative?

The overwhelming opinion on this from the market seems to be that it is currently well-nigh impossible. If petrodollar reserves diversify away from the U.S. dollar, the resulting increase in the M2 money supply as these once-cloistered greenbacks make their way home will only add to inflationary woes back in America over the course of the next couple of decades. With dysfunctional inflation cycles will come more aggressive rate hike cycles and more confounding market dynamics.

In Conclusion

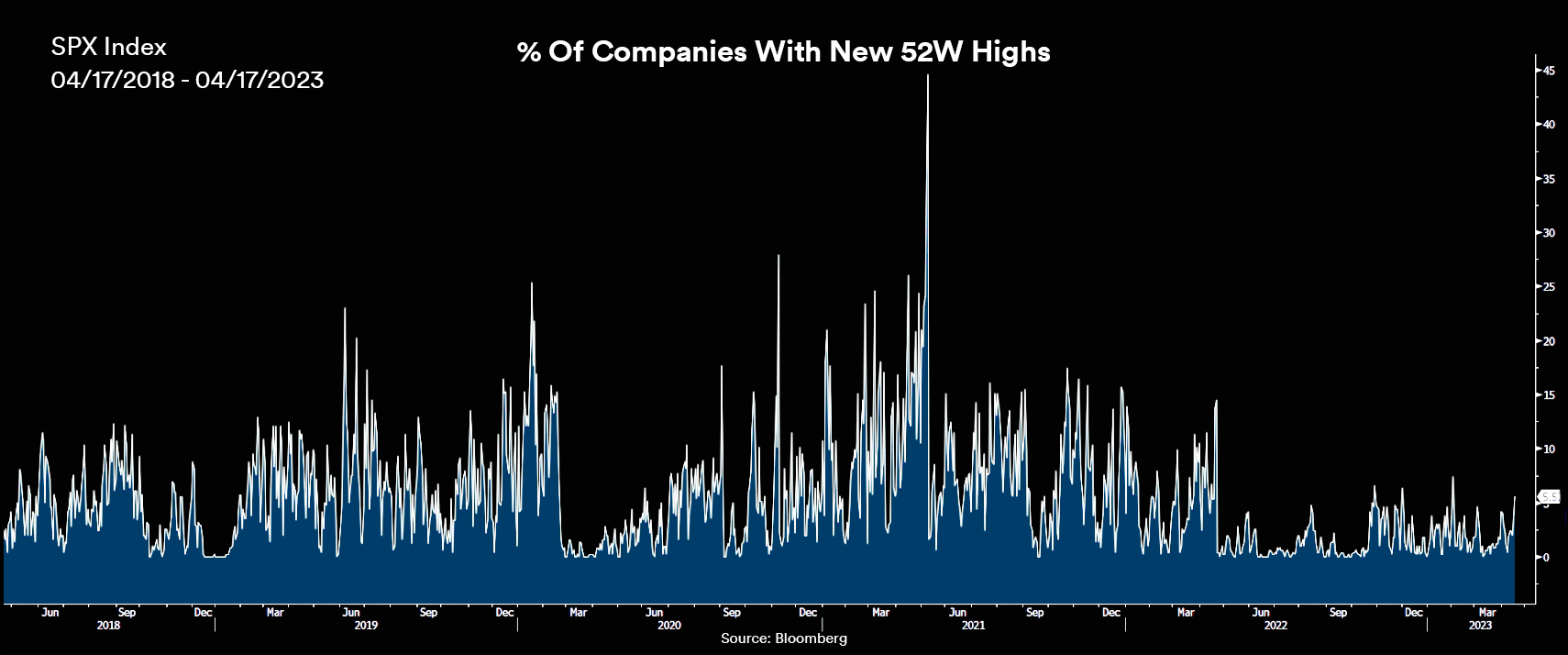

Bearing in mind the concentration of overall trajectory into the top of the line of the S&P 500, it's also germane to note that the number of companies hitting new 52-week highs is at 5-year lows :

Source: Created by Sandeep G. Rao using data from Bloomberg

{kind=link}

This lends strength to the notion that flows into large-cap stocks are informing market trajectories more than the rest of the market itself. Also, given that government debt exposure remains a niche interest, this flow is also driven by limited access to viable alternatives. In other words, a significant portion of these flows follow a form of self-preservation which becomes a self-fulfilling prophecy: as their valuations fall, smaller companies will find it increasingly harder to secure financing and challenge the status quo. One means of growth would be to collaborate/enjoin with the top-of-the-line which further biases survivability.

Another factor to bear in mind is that American equities have always needed momentum (and volumes) to justify their often-exaggerated valuations. The aforementioned momentum meters indicate that while the year certainly did start with top-of-the-line stocks bearing substantial momentum, this has been fading away as the months go by. The increasing correlations between top-of-the-line and the Top 25 (i.e., mostly "Tech") while both dissipate indicate that exaggerated valuations are finding increasingly less support. All in all: while size seems to matter increasingly more, it's also increasingly important to be wary of fuzzy growth narratives.

For further details see:

Banks Down, Big Tech Up? Beware Of De-Dollarization