BKU - BankUnited: A Solid Bank Undervalued Dividend Stock

2023-04-13 14:58:40 ET

Summary

- BankUnited has had massive revenue growth but hammered margins.

- Its stellar balance sheet shows it can withstand current headwinds and bounce back.

- Market prospects are more promising as macroeconomic indicators stabilize.

- BankUnited's dividends are enticing, given the consistent payouts and high yields.

- The BankUnited stock price downtrend persists, making it cheaper.

Banks are more exposed to risks associated with economic volatility. Generally, they are more sensitive to inflation and interest rate changes than many other industries. BankUnited, Inc. ( BKU ) is not an exception, as shown by its operations. Its contracting margins showed the unfavorable impact of macroeconomic disruptions. Despite this, it maintained positive returns that covered its operating capacity and capital returns. Its solid financial positioning continues to demonstrate its liquidity and sustainability. Unsurprisingly, it keeps increasing its dividend payouts.

Meanwhile, the BankUnited, Inc. stock price remains in a downtrend after the sharp plunge earlier this year. It may be logical, given the relatively weaker 4Q performance and bleak near-term forecasts. On a lighter note, it can open more opportunities to buy shares at a discount. Different price metrics revealed that the price is way lower than the intrinsic value of the stock. Hence, BankUnited, Inc. is a cheap and secure dividend stock.

Company Performance

BankUnited, Inc. is part of a highly volatile industry. It faces many risks as the market environment remains tough. Fortunately, many banks are flexible enough to cope with the massive changes in the past three years. It is even more challenging today due to inflationary headwinds and recessionary fears. BankUnited, Inc. remains a stable and viable bank despite the hammered margins.

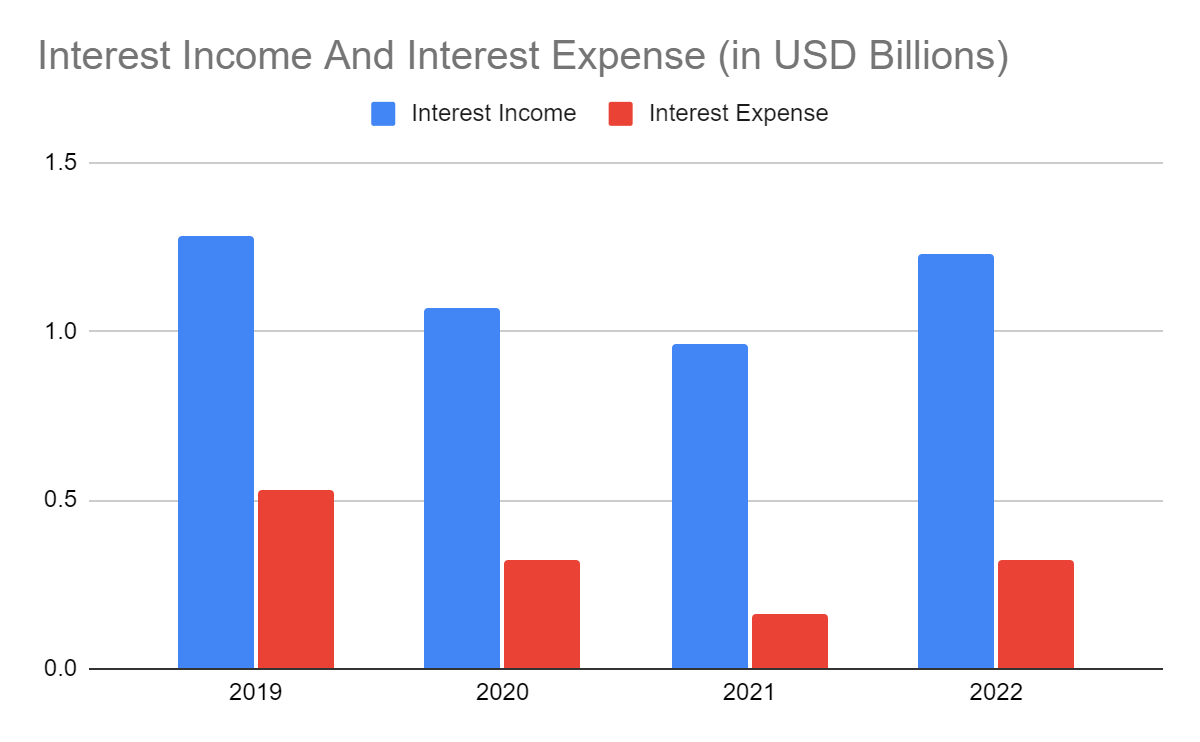

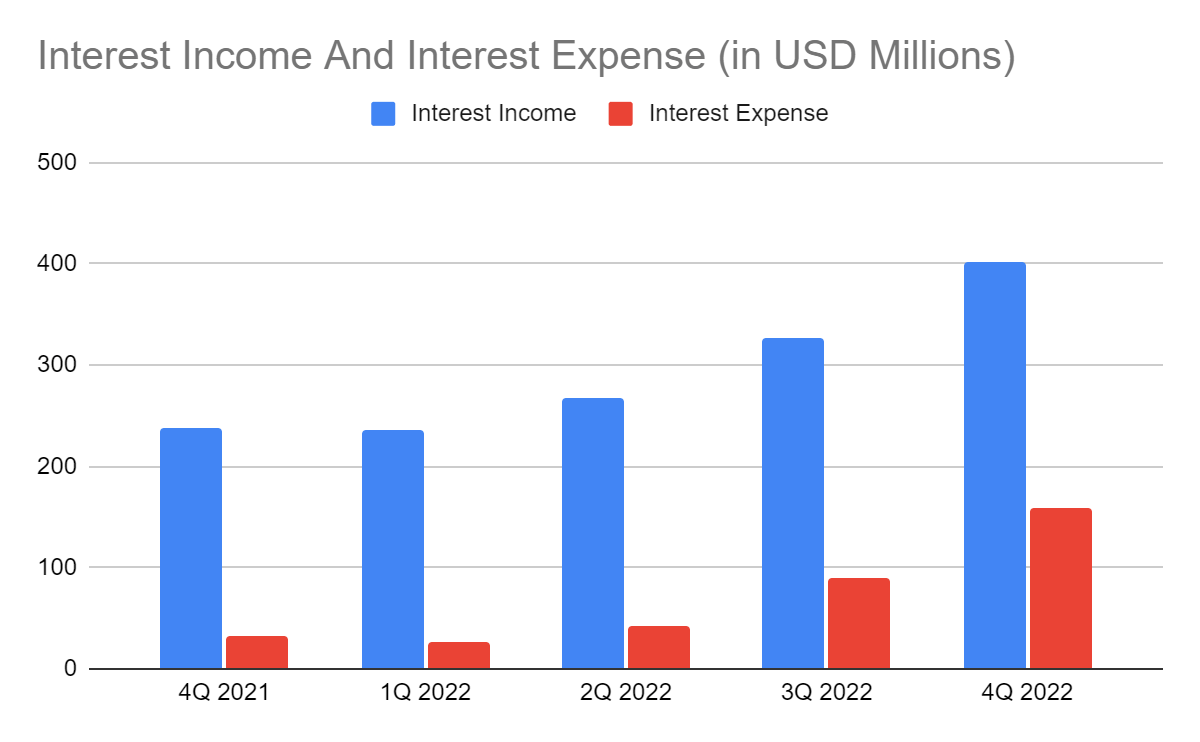

Its primary sources of revenue are loans, investment securities, and other interest-earning assets. Their combined value amounted to $1.23 billion , a 28% year-over-year increase. Also, it was 96% of interest income in 2019. Their main difference was the elevated inflation and interest rates. These led to changes in loan and investment security yields. It was more evident in the last three quarters as macroeconomic indicator rates skyrocketed. Its 4Q interest income reached $401.49 billion, the highest value since the pandemic. The quarterly increase in 2022 was consistent and exceeded 4Q 2021 by 69%. This impeccable increase can be attributed to various factors. In essence, interest rates and interest income have a direct relationship. This attribute was maximized by the bank. More importantly, it had prudent loan and investment portfolio diversification and solid asset quality.

Its interest income on loans comprised over 70% of the total revenue. It rose by 17%, showing that interest rate hikes raised loan yields. It was highest in 4Q, 45% higher than in 4Q 2021, and 18% higher than in 3Q 2022. It was mainly driven by the massive loan growth, particularly in the commercial segment. Even better, its NPL/Total Loans was only 0.42% versus 0.87% in 4Q 2021. As the company grew its loans, it maintained its conservative portfolio diversification. It was secure, given the lower potential of defaults and delinquencies. Also, commercial loans accounted for 56% of the total loans, 59% from C&I loans, and 41% from CRE loans. There are safer forms of loans due to more secure business collateral. Its primary concern may come from the CRE loans, given the apprehension of many analysts about the property market. But it stays favorable for the bank since property value continues to appreciate despite the softening commercial sales. We will discuss more of these in the succeeding parts. Meanwhile, investment security interest income comprised 24% of revenues. It was higher in 4Q at 26%. It should not be unsurprising since a massive portion of investments is government-backed securities. They are safe amidst interest rate hikes due to their stable yields and better hedge against valuation decreases.

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Interest Income And Interest Expense (MarketWatch)

{kind=link}

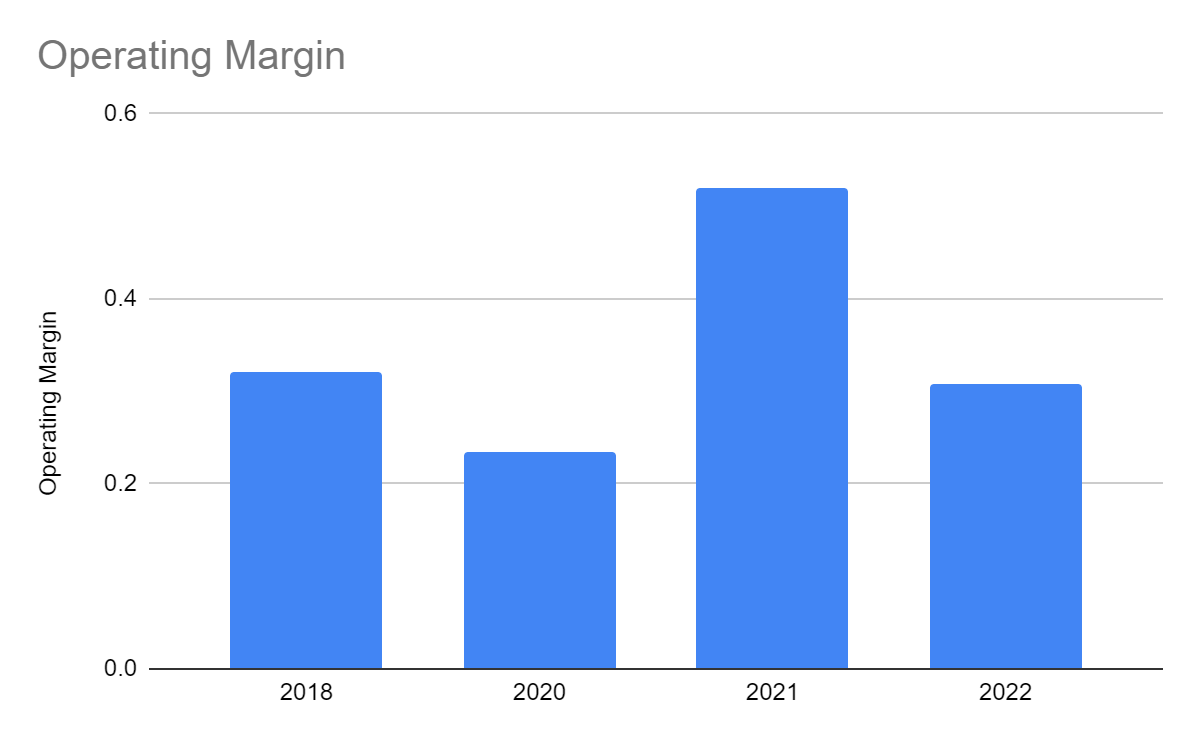

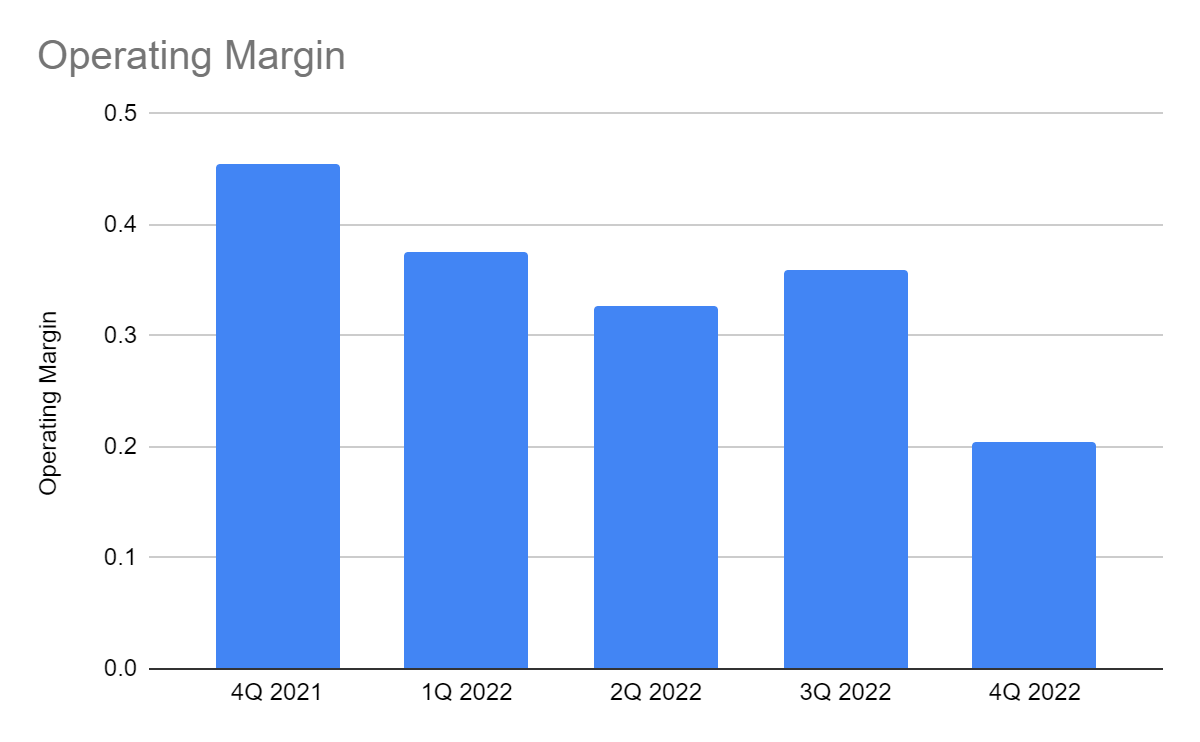

However, interest rate hikes affected its deposits and borrowings. Their combined value had a 95% year-over-year increase. It was overwhelming in 4Q since they almost quadrupled from 4Q 2021. Meanwhile, most components of non-interest income remained stable. Yet, the sale of loan losses offset the value, leading to a 41% decrease. Thankfully, non-interest expenses remained stable, which demonstrated the efficient asset management of the company. It was more impressive, given the rising prices. The operating margin was only 31% versus 52% in 2021. In 4Q, it was only 20% versus 45% in 4Q 2021. The consolation was that the core operating income remained a positive value. Hence, returns were still more than enough to sustain its operating capacity and capital returns. We can see it in the higher amount of cash and cash equivalents.

Operating Margin (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

This year, BankUnited, Inc. may face near-term headwinds. But by the looks of it, the company can withstand them. As inflation becomes more stable, it may become easier for the company to manage its asset portfolio. Their yields may decrease but become more manageable. This will be discussed further in the next section.

How BankUnited, Inc. May Stay Afloat This Year

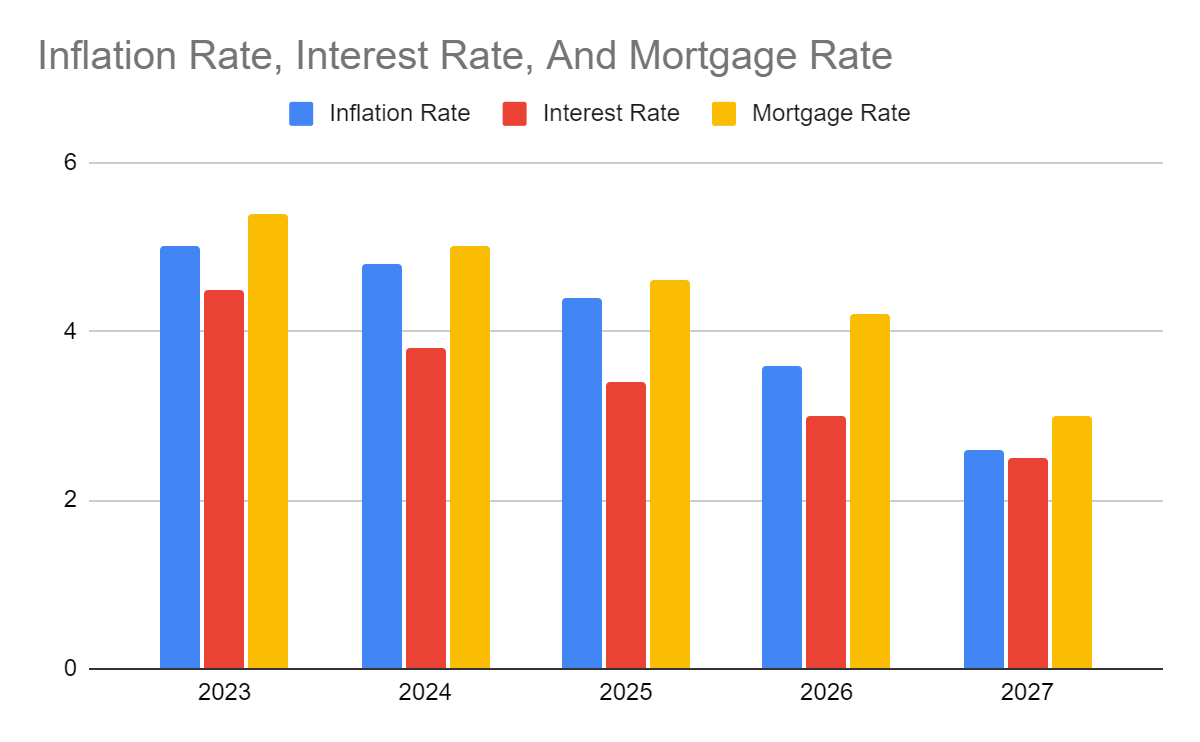

We already saw how BankUnited, Inc. managed to stabilize its growth despite hammered margins. It stayed viable with well-diversified loans and investment securities. While its near-term performance may remain the same as the 4Q performance, there may be continued improvements. It is possible as inflation continues to relax. It landed at 5%, a massive decrease in a month. It is also 45% lower than the 2022 peak. Indeed, the effort to stabilize inflation has paid off. It is still higher than pre-pandemic levels, but policymakers are on the right path. It is also the lowest rate in about two years. Given this, the Fed may keep its conservative approach but ease its monetary policy. Interest rate increments may continue but cool down in the following quarters. In 2024, it may become more manageable before decreasing. The company may realize more stable yields and more manageable interest on borrowings and deposits.

Likewise, mortgage rates are in a downtrend. We can attribute it to recent macroeconomic changes and softening property sales. Analysts anticipate a massive market crash as the demand continues to decrease. The bank may have to be careful since real estate loans are vital to its business.

Despite the pessimism, I disagree with the supposition. First, property builders have been conservative over the past decade. The number of units has slowed down since the Great Recession. Second, the price increase was driven by the massive influx of buyers, not by cost-push inflation factors. Third, property shortages remain high in the U.S. It is evident in residential housing since the market is short of 6.5 million units.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

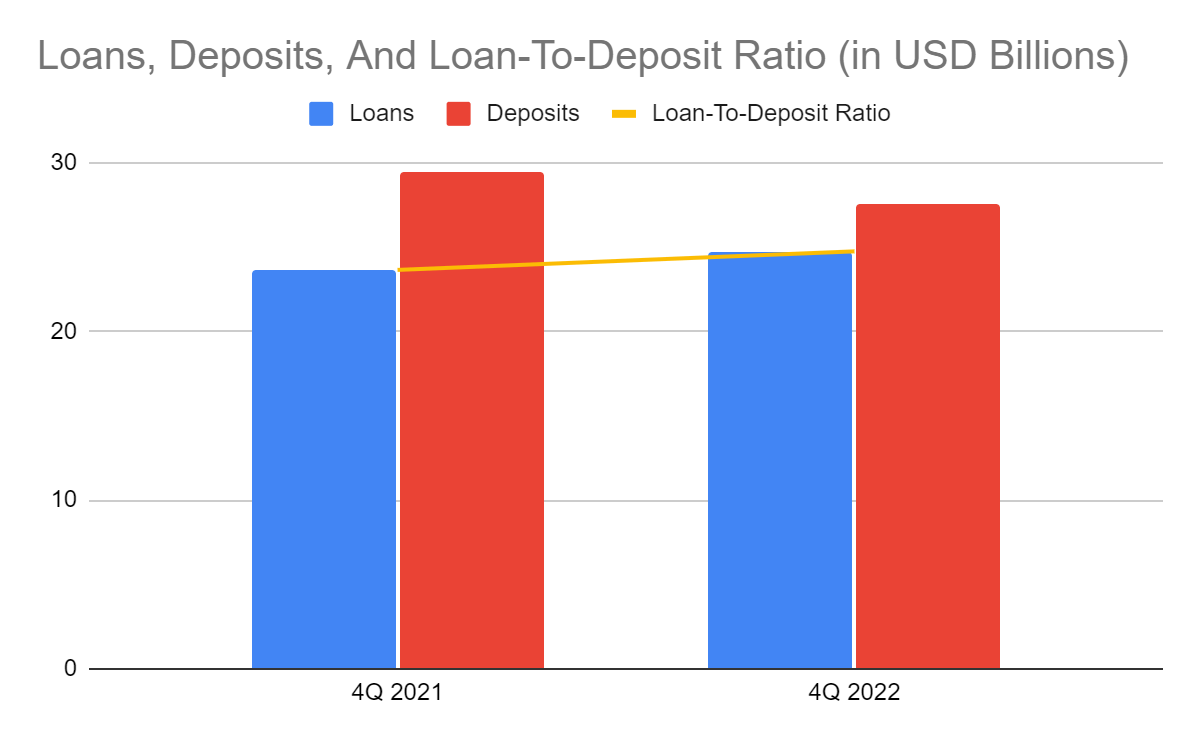

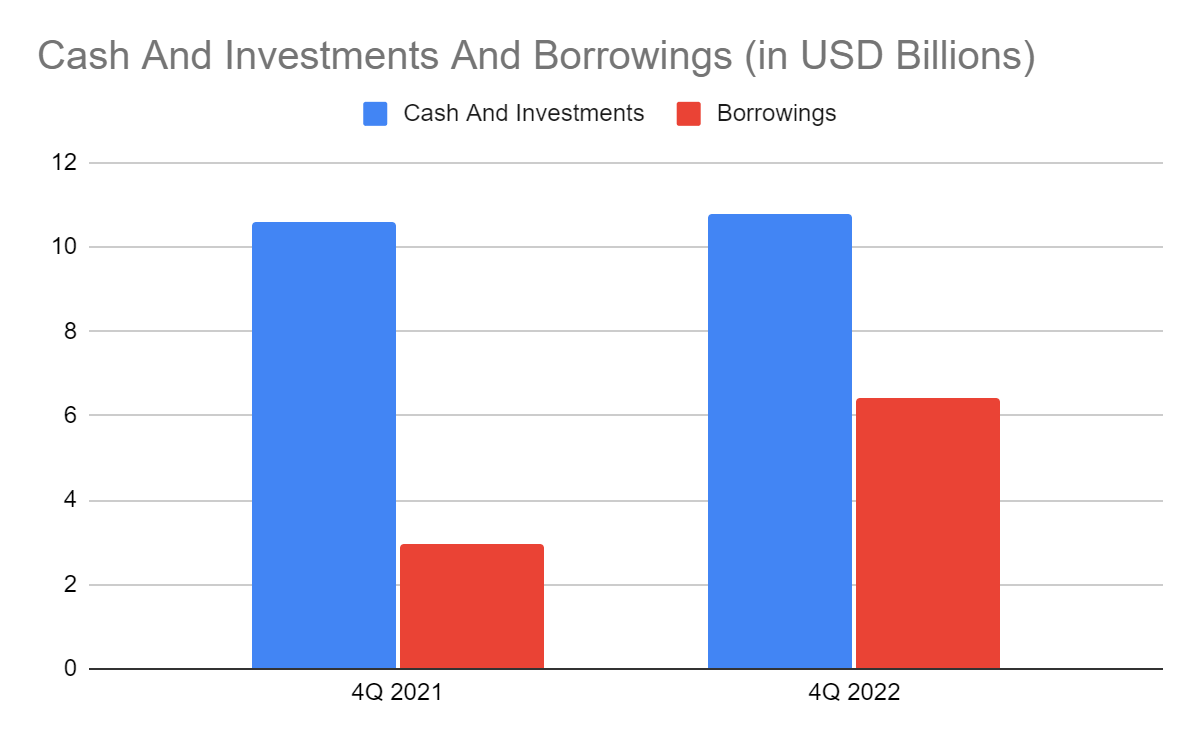

What makes the bank a sound company is its financial positioning. Its stellar balance sheet demonstrates its high liquidity and sustainability. Its loan-to-deposit ratio remains decent at 89%. As such, it still has resources to lend out to borrowers to generate more yields. It also has adequate reserves to cover potential defaults. Meanwhile, cash and investments are still stable. Their combined value of $10.8 billion comprises 30% of the total assets, making BKU very liquid. It can cover its operating capacity, borrowings, and dividends.

Loans, Deposits, And Loan-To-Deposit Ratio (BKU 4Q Financial Release)

{kind=link}

Cash And Investments And Borrowings (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of BankUnited, Inc. remains in a downtrend. It has not bounced back yet after the sharp plunge earlier this year. At $21.24, the stock price is 49% lower than last year's value. Despite this, it may open more opportunities for investors to buy shares at a discounted price. It is cheaper today, as shown by the P/B Ratio. The BVPS and P/B Ratios are 32.2 and 0.99x, respectively. If we use the current BVPS and average P/B Ratio of 1.05x, the target price will be $33.8.

Moreover, BKU is an attractive dividend stock with inconsistent payouts. Its dividend yield of 5% is way higher than the S&P 500 (SP500) average of 1.74%. Dividends also remain well-covered, given the dividend payout ratio of 30%. To assess the stock price better, we will use the DCF Model.

FCFF $313,000,000

Cash $16,090,000

Outstanding Borrowings $4,530,000,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 75,675,000

Stock Price $21.24

Derived Value $26.52.

The derived value also shows that the stock price is undervalued. There may be a 25% upside in the next 12-18 months. Interested investors must take a look at this off-the-radar stock for gains.

Bottom Line

BankUnited, Inc. may be hampered by macroeconomic disruptions, but it remains viable. It maintains a sound financial positioning to sustain its operating capacity and capital returns.

BankUnited, Inc. is an attractive dividend stock, given the high yields and adequate means to cover it. Also, the stock price is low and undervalued. The recommendation is that BankUnited, Inc. is a buy.

For further details see:

BankUnited: A Solid Bank, Undervalued Dividend Stock