BKU - BankUnited: Balance Sheet Optimization Poised To Create Upside

2023-12-04 00:10:50 ET

Summary

- BankUnited's stock has fallen 19% in the past year, but its balance sheet actions are proving to be accretive and attractive.

- The bank's credit quality remains robust, with a low nonperforming loan ratio and healthy net charge-offs, which should limit how much longer it builds reserves.

- BKU's net interest margin has expanded, deposits are growing again, and the bank is optimizing its funding profile, which should drive earnings growth.

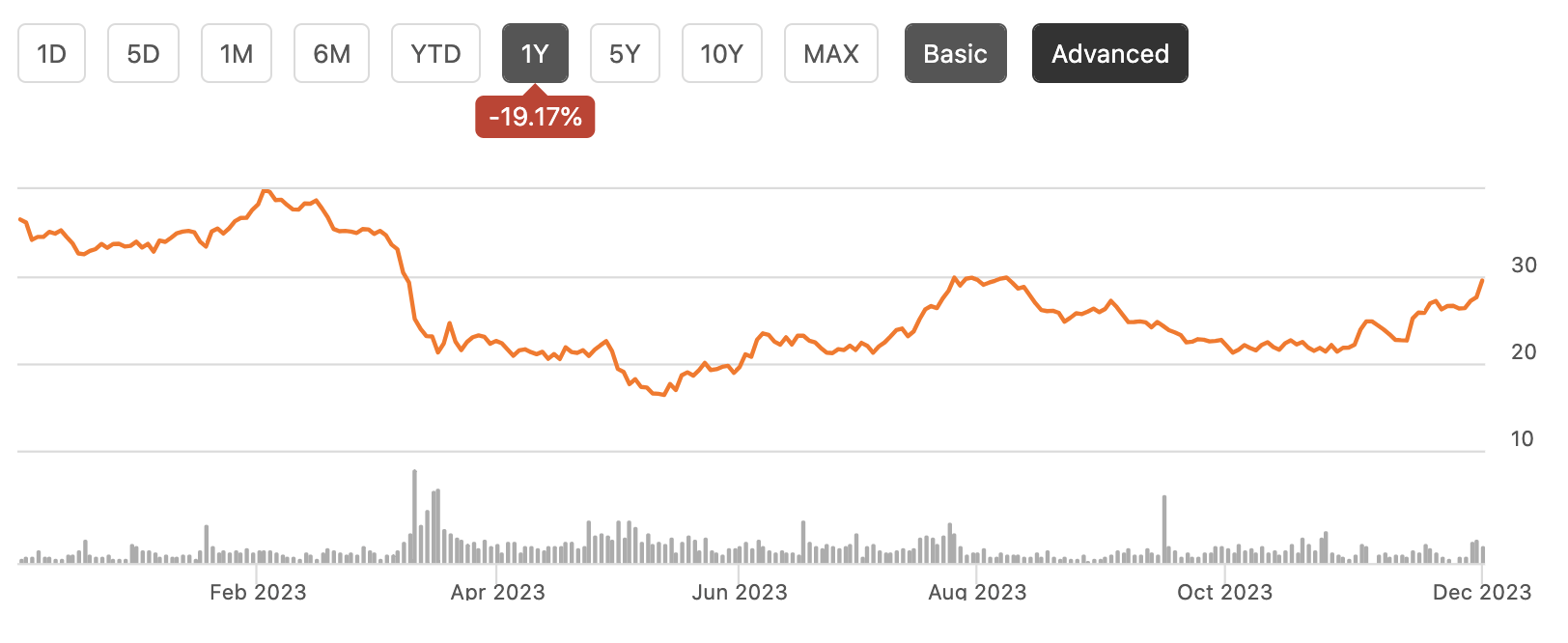

Shares of BankUnited ( BKU ) have fallen about 19% over the past year, alongside declines across most regional bank stocks. Since the collapse of Silicon Valley Bank, we have seen a material increase in deposit costs while many banks have also suffered large unrealized losses on their fixed-income security portfolios. While BKU likely has a couple more quarters of elevated credit reserves, its balance sheet actions are proving to be quite accretive and make the stock attractive.

{kind=link}

In the company's third quarter , BankUnited earned $0.63, down from $1.12 last year as it increased reserves for credit losses. This was also about $0.08 below consensus. During the quarter, BKU took $33 million in provisions for credit losses, from $4 million last year, given the ongoing economic uncertainty, which has contributed to higher nonperforming loans.

Still, credit quality remains fairly robust at the bank with just a 0.4% nonperforming loan ratio, when excluding SBA government guarantees. This is up from 0.26% at the end of last year, but it does remain substantially below pre-COVID levels. Results are normalizing but remain healthy in other words. Net charge-offs are also running at just 0.07%, a very healthy level.

BankUnited

Following this quarter's reserve increase, BankUnited carries $196 million in allowances. This provides 200% coverage of its nonperforming assets. As a general rule of thumb, I do like to see banks carry 250-300% coverage. Low charge-offs combined with its large SBA-guaranteed business do mean that BKU can likely run at the lower end of this range, but I would expect the company to continue to build reserves. During the quarter, its ACL ratio rose by 12bp, so within 2 more quarters, it would be at 250% coverage, at which point its build needs would be much smaller.

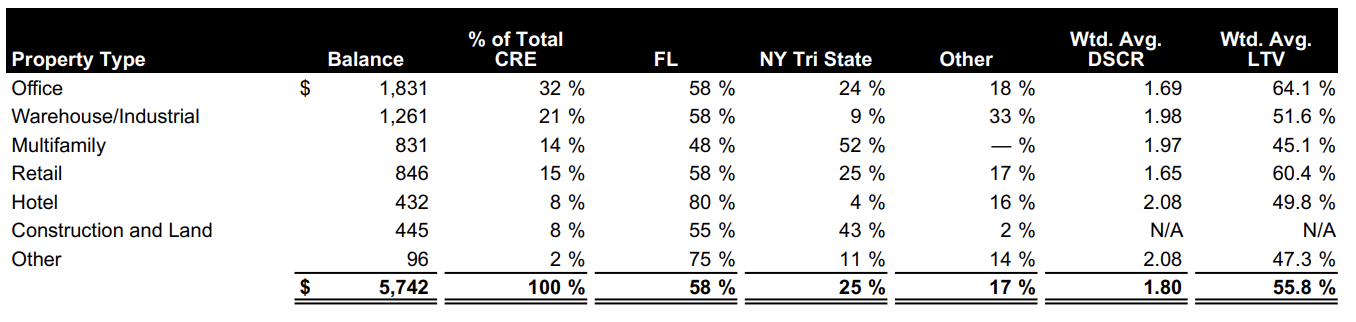

On its loan book, I would note that 24% of loans are commercial real estate. As you can see below, its CRE exposure is fairly diverse, but I would highlight it does have $1.8 billion of office exposure, which is the most challenged sector. I am fairly comfortable with this though. First, 17% of its office loans are medical, which is less sensitive to remote working trends.

{kind=link}

Additionally, as you can see, its office loans have a loan-to-value (LTV) of 64%, which is fairly low. This means if a property defaults, on average it would need to sell for more than a 36% loss for BKU to suffer a financial loss. These low LTVs are another reason that reserve coverage can be a bit lower. BankUnited operates primarily around New York City and Florida. Its Florida office portfolio is suburban. 44% of NY office loans are in Manhattan with a 95% occupancy and just 5% rent rollover next year. Just $338 million of office loans mature over the next year giving borrowers plenty of time to consider refinancing options.

With credit reserves likely to moderate after Q1 2024, I think investors will begin to appreciate more the strong work management is doing in terms of balance sheet optimization. BKU's net interest margin [NIM] expanded to 2.56% from 2.47% last quarter. This is one of the few banks to increase NIM sequentially despite ongoing increases in deposit costs. Still, NIM was down from 2.76% last year. Importantly, management sees NIM expanding further next quarter. I expect most banks to have NIM bottom in Q4 2023-H1 2024; BKU has already bottomed. This is because it has less of a securities portfolio problem and has begun to stabilize deposits.

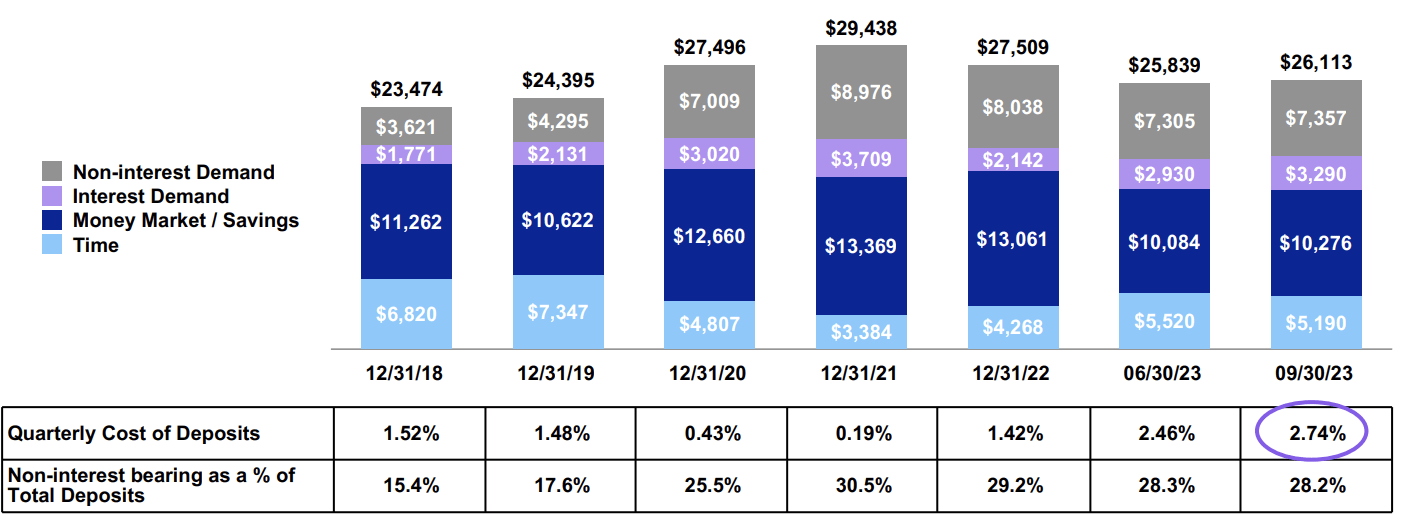

Deposits were up by $274 million sequentially to $26.1 billion, though they are down $1.2 billion from last year. Many smaller banks saw deposit flight after SVB failed, and BKU was not immune to this. However, we are seeing deposits grow again, and the mix shift is quite encouraging. While it grew deposits, brokered deposits were down $210 billion sequentially. These are higher-cost deposits than organically sold ones, so relying less on the brokered market should help fund costs. BKU has been able to step back from this market as organic deposit growth returned.

As you can see below, during the quarter, its deposit cost rose to 2.74%, up from 1.42% at the start of the year. This was up a more modest 28bp from Q2 as the fight for deposits normalizes. Importantly, as of 9/30, deposit costs were only 10bp higher at 2.84%. This slowing pace of increase should mean that funding costs only rise slightly in Q4, which is a reason why NIM can expand. We are nearing the end of the pain of funding costs.

{kind=link}

While deposits are down from last year not all deposits are down equally, noninterest bearing deposits [NIB] are down by $1.4 billion from last year. As rates rise, customers have had an incentive to minimize 0% account balances as they can earn over 5% in money market funds. Most of these accounts are transactional, so there is a functional floor to their balances. We may be seeing that with NIB balances up $52 million sequentially. BKU has done a good job growing this franchise over time; in 2018, they were only 15% of balances. Management expects we are at or near the bottom here.

As deposits have turned back to growth and BKU has been judicious in lending activity, its loan-to-deposit ratio has fallen to 93% from 95%. Due to this, it paid down FHLB advances by $810 million to $5.2 billion. FHLB funding costs are tied to the Fed funds rates, so paying down these balances, even with interest-bearing deposit funds is NIM accretive.

There is still substantial room to pay down FHLB advances in coming quarters, and that remains a priority for the bank in Q4, which will further optimize its funding costs. BKU will also generate liquidity through maturities and principal payments on its securities portfolio, which it can use to reduce FHLB funding. It has an $8.8 billion securities portfolio. This portfolio has been relatively conservative with just a 2-year duration and 68% being a floating rate. As such, it has a relatively modest $407 million loss in accumulated other comprehensive income (AOCI). Still, as lower-yielding securities mature, they can either reinvest at higher market yields or pay down FHLB advances. Each $1 billion in FHLB advance it pays down should raise run-rate annual earnings by about $0.20, given what interest bearing deposits are yielding.

Finally, BKU is extremely well capitalized. It has a common tier-one equity ratio (CET1) of 11.4%. Even if we include its AOCI loss, its ratio would be a still-healthy 9.8% when most regional banks are below 8.5%. Because of its small size, BKU will not have to phase these losses into its capital calculations. This leaves the company well-positioned to grow risk-weighted assets and resume share repurchases early next year, on top of its 3.7% dividend.

While last quarter was negatively impacted by credit losses, we should be within two quarters of that headwind abating. However, I am extremely encouraged by developments on deposits. This stabilization is allowing BKU to optimize its funding profile while in time allowing it to deploy funds into higher yield loans and securities going forward. These two actions can drive $0.40 of earnings growth over the next year. Assuming credit reserves decline to a $15 million pace, BKU should be able to earn $3.40-$3.60 in 2024. Given its robust capital position, that should enable a meaningful share repurchase program. With the stock about 10% below tangible book value of $32.88, this can be quite accretive. I would be a buyer until about 1.1x tangible book, given its excess capital and improving funding mix, or about $36. This would be about 10x 2024 earnings within the 8-10x multiple of most regional banks. That is over 20% upside from here, making shares a compelling opportunity.

For further details see:

BankUnited: Balance Sheet Optimization Poised To Create Upside