BKU - BankUnited: Worth Consideration Despite Some Weak Spots

2023-06-30 15:10:12 ET

Summary

- BankUnited has not yet fully recovered from the banking crisis that developed in March. However, the company has some positive attributes such as a strong loan portfolio and a great deal of liquidity.

- The bank has seen a decrease in deposits, which is partly due to depositor sentiment shifting towards seeking higher yields and concerns over the bank's stability.

- Despite some concerns, the company's shares are considered cheap and it has a good history of growing its loan portfolio. Therefore, I believe the company is cheap enough to warrant a cautious ‘buy’ rating at this time.

Many of the banks that have been slammed because of the banking crisis that developed in March of this year have not yet staged a full recovery from their downturn. In fact, I've yet to see one that has staged a full recovery. One of the firms that is still down quite a bit since that time is a rather small bank called BankUnited ( BKU ). With a market capitalization of about $1.6 billion, BankUnited truly is a small player in the banking industry. But I have found that some of the greatest upside when it comes to investing can involve purchasing these small, obscure enterprises. Digging deep, I found some positive attributes that gives me optimism about the company and its future. But not everything is great about the company. Some of the trouble areas do deserve your attention. But when you look at the whole picture, I would argue that the company probably does offer some upside from this point on.

A small bank with a mixed picture

According to the management team at BankUnited, the firm operates as a bank holding company With a single wholly owned subsidiary that goes by the same name. This is a national banking association that's based out of Florida and that provides commercial lending to its customers. It also provides both commercial and consumer deposit services through banking centers that it has stationed throughout Florida, parts of New York, and Dallas, Texas. It operates a wholesale banking office in Atlanta, Georgia, through which it provides commercial lending and deposit services to the southeastern portion of the country. And it also offers customers commercial lending and deposit products, as well as some consumer deposit products, through its online channels.

{kind=link}

BankUnited

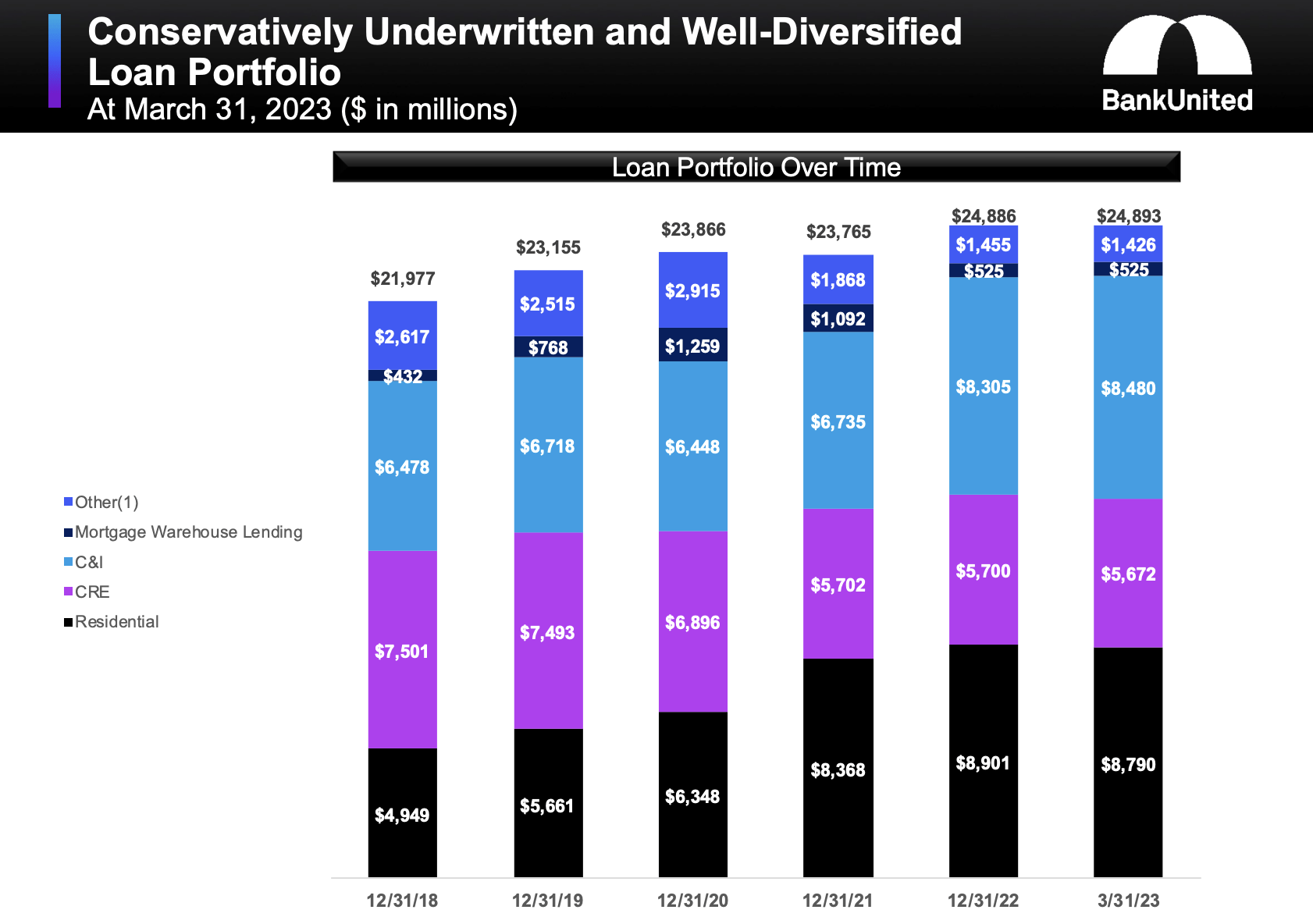

As of the end of the first quarter of the company's 2023 fiscal year , it boasted a loan portfolio worth $24.89 billion. The largest chunk of this, about $8.79 billion, involved residential loans that included a variety of mortgages. These are largely mortgages made out to borrowers that have higher credit scores. In fact, by value, 74% of its mortgages are made out to individuals with credit scores above 759, with another 16% involving customers with credit scores between 720 and 759. Next in line, we have $8.48 billion worth of commercial and industrial loans. The largest chunk here includes $1.84 billion granted to finance and insurance companies. Other major categories include manufacturing, educational services, information, wholesale trade, and utilities.

I know one area that investors have expressed concern about recently is commercial real estate, namely office properties. It is true that the company has $5.67 billion worth of exposure to commercial real estate. But there are a couple of important points to make. For starters, the company has really been moving away from this. At the end of its 2018 fiscal year, for instance, it had $7.50 billion, or 34.1%, of its loan portfolio dedicated to commercial real estate. That number today is now 22.8%. In total, only $1.84 billion of its loans, totaling 33% of overall commercial real estate loans, fall under the office category. And with a loan to value ratio of 64.2%, the company does have some wiggle room.

{kind=link}

BankUnited

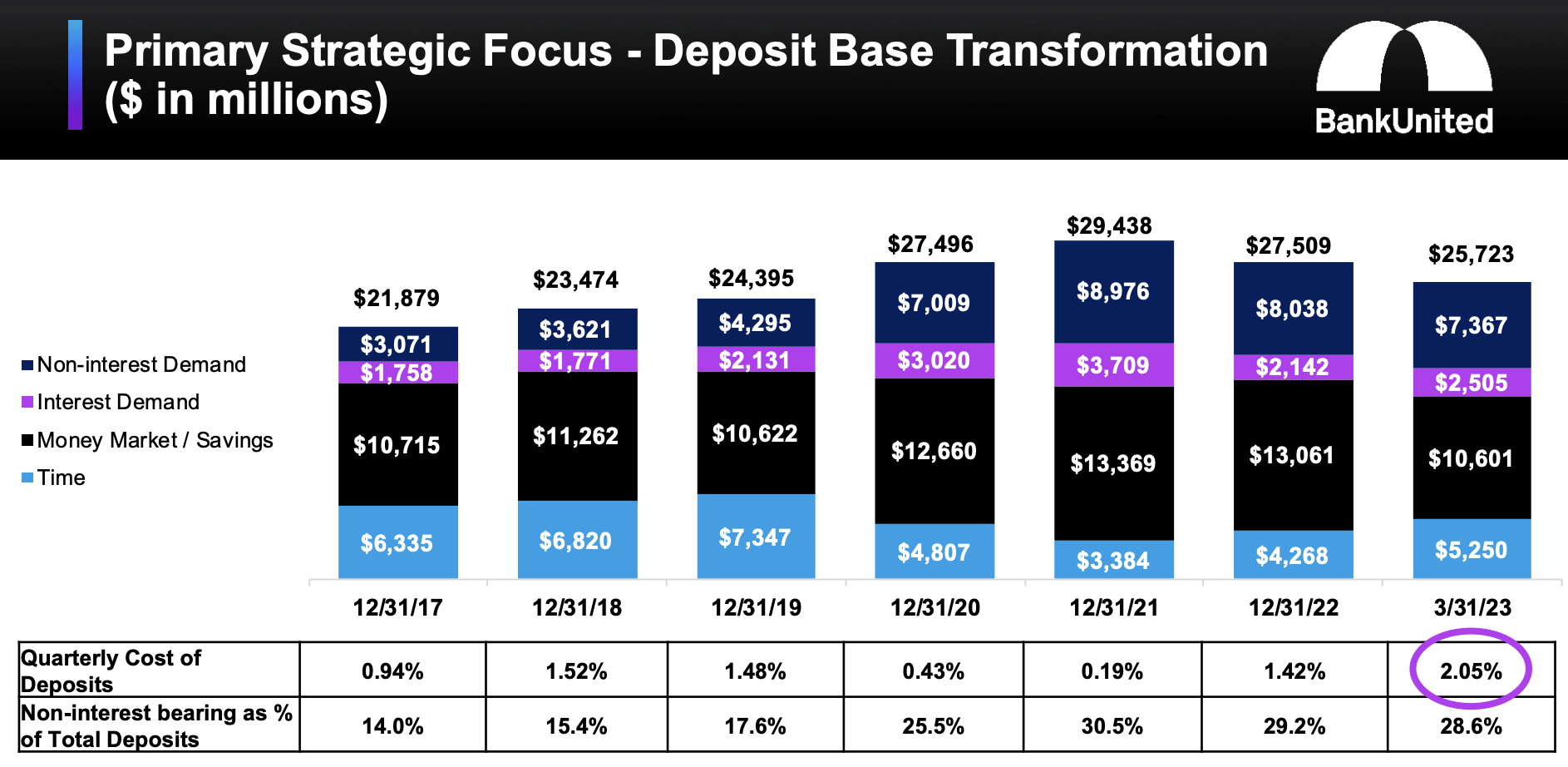

Even though the company has done well to grow its loan portfolio recently, its deposits are another question entirely. After peaking at $29.44 billion in 2021, the value of deposits for the business started declining. In 2022, they ended the year at $27.51 billion. And from the end of last year through the end of the first quarter this year, deposits fell to $25.72 billion. There is no doubt in my mind that some of the early decline was driven by a shift in depositor sentiment as depositors withdrew capital and focused on seeking out higher yields. I have seen that happen with a lot of other banks over the past year or so. But there is also no doubt that some of the pain recently has been driven by concerns over the bank's stability.

{kind=link}

BankUnited

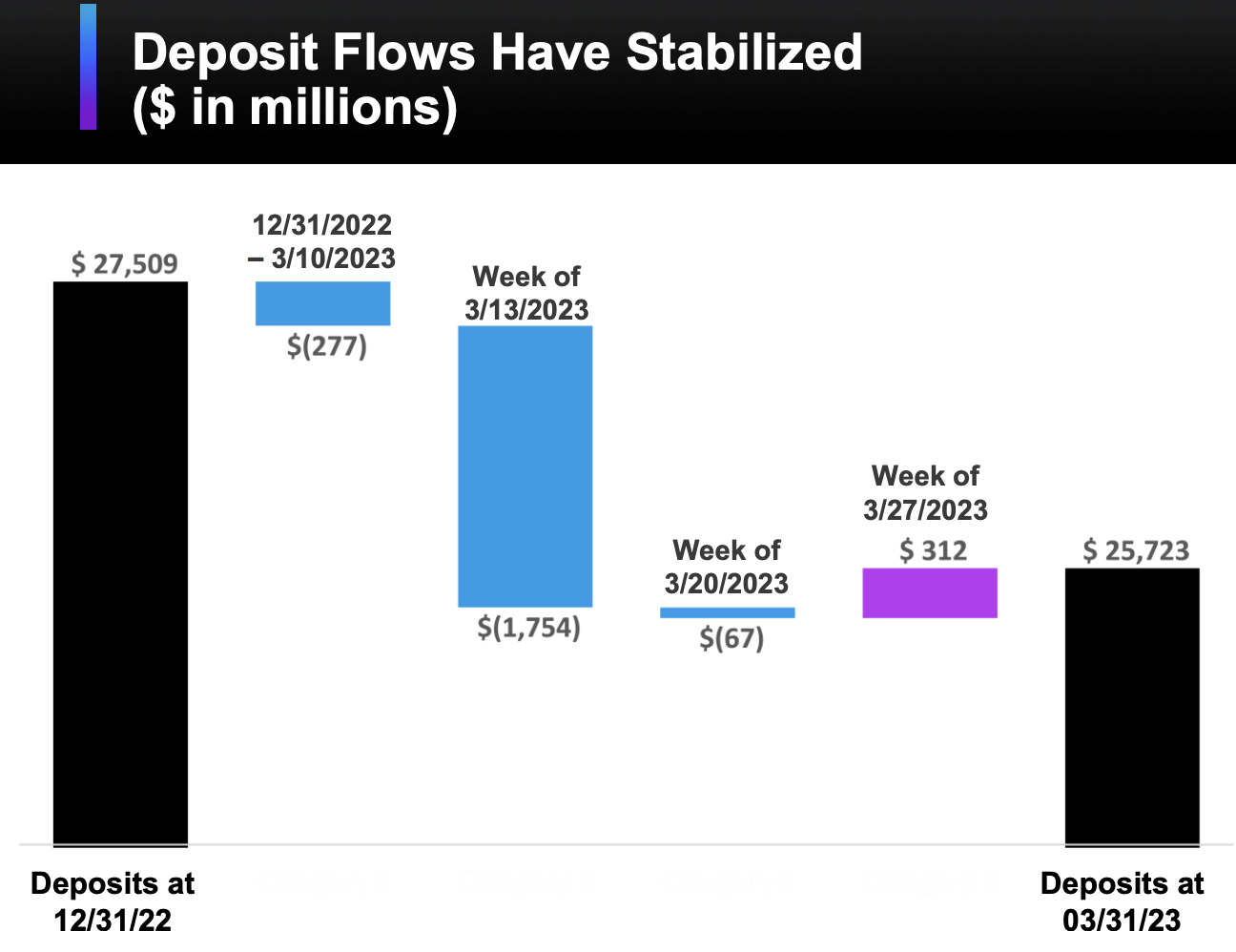

I say this because management revealed as much in its latest investor presentation. From the end of 2022 through March 10 of this year, deposits for the bank fell by only $277 million. But in the week of March 13, deposits plunged $1.75 billion. This was during the worst and initial stages of the banking crisis. Deposits fell another $67 million one-week later. But the good news is that deposits actually increased modestly in the week of March 27, climbing $312 million on a net basis. Such a show of stability in such a short window of time is fantastic to see.

{kind=link}

BankUnited

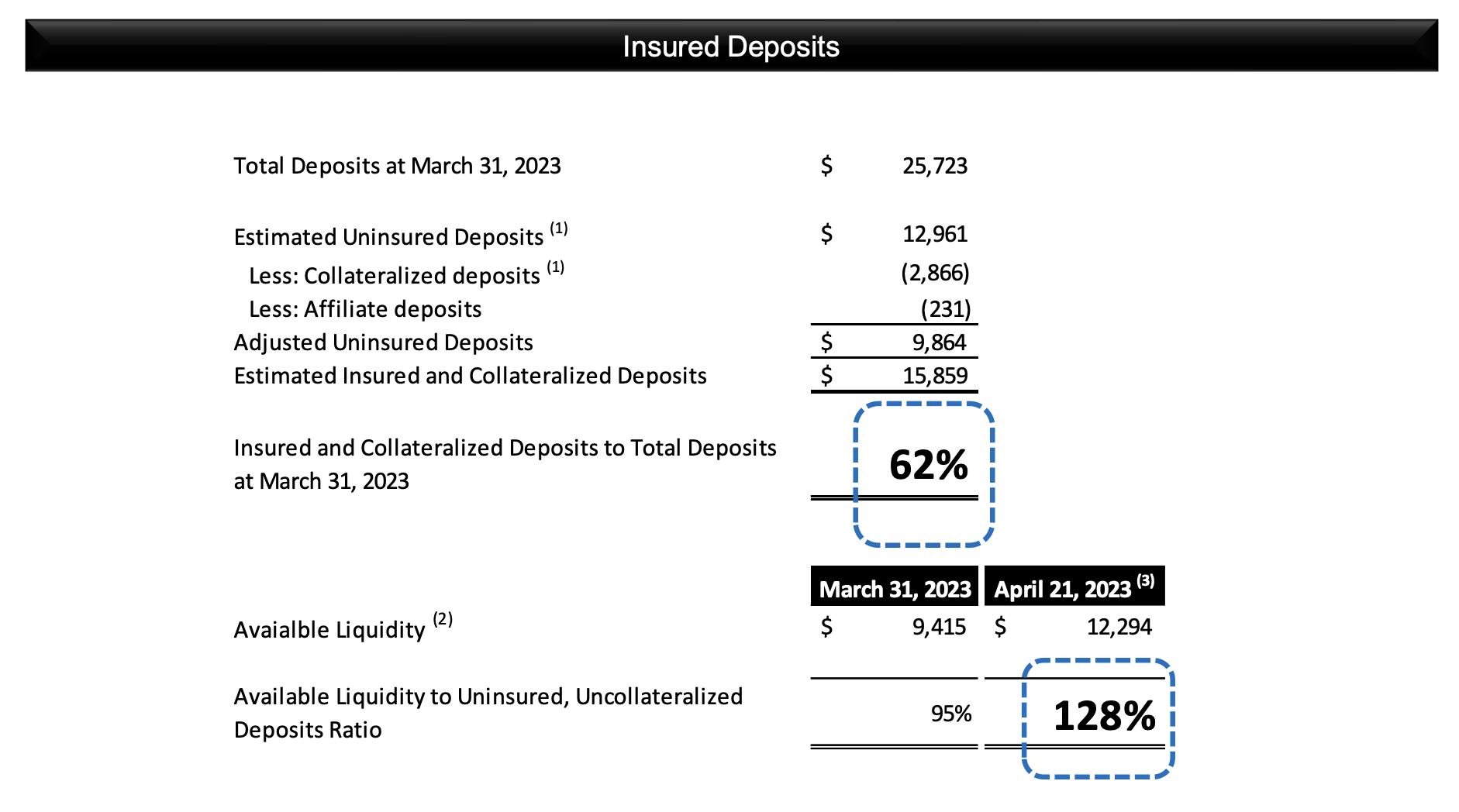

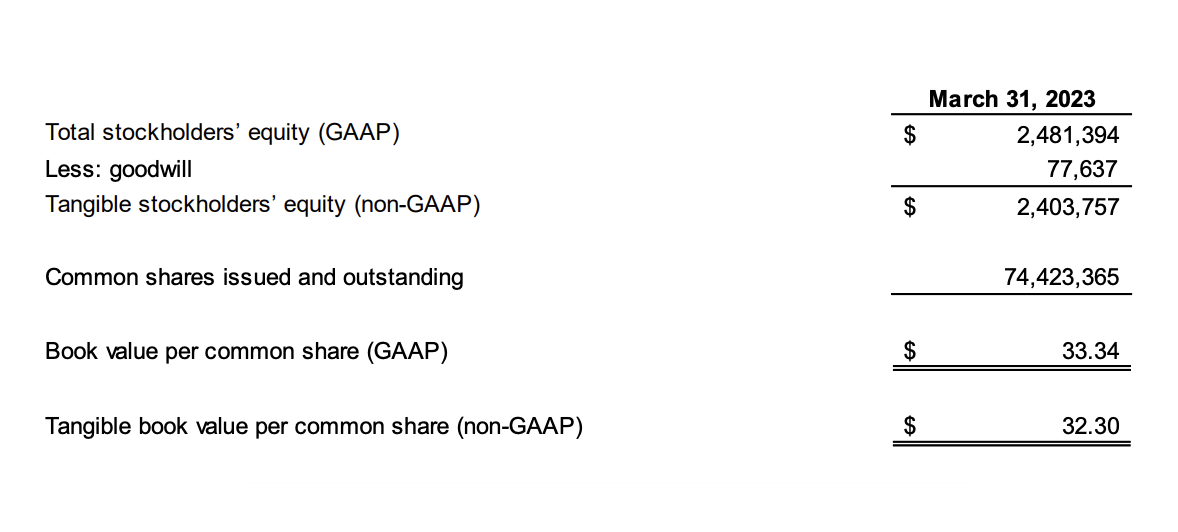

Another positive thing about the company is that it currently has a great deal of liquidity. As of April 21 of this year, the company had $12.29 billion worth of liquidity at its disposal. This translated to 128% of the sum of its uninsured and uncollateralized deposits. Of course, not everything about this picture is fantastic. If we use data from the end of the first quarter, only 62% of the deposits at the bank are either insured or collateralized. While this is not as bad as some banks, it's certainly not the best that I have seen. While it is true that the company does have enough liquidity to cover any capital outflows, borrowings are also a problem. At the end of 2021, the company had only $2.83 billion worth of debt. That number grew to $6.33 billion in 2022 before climbing further to $8.27 billion at the end of the first quarter of this year. Even with those borrowings, however, the company does have a solid book value per share. At the end of the most recent quarter, this number came in at $33.34, with tangible book value per share totaling $32.30. When you consider that shares are currently trading at $21.68, the good does seem to outweigh the bad.

{kind=link}

BankUnited

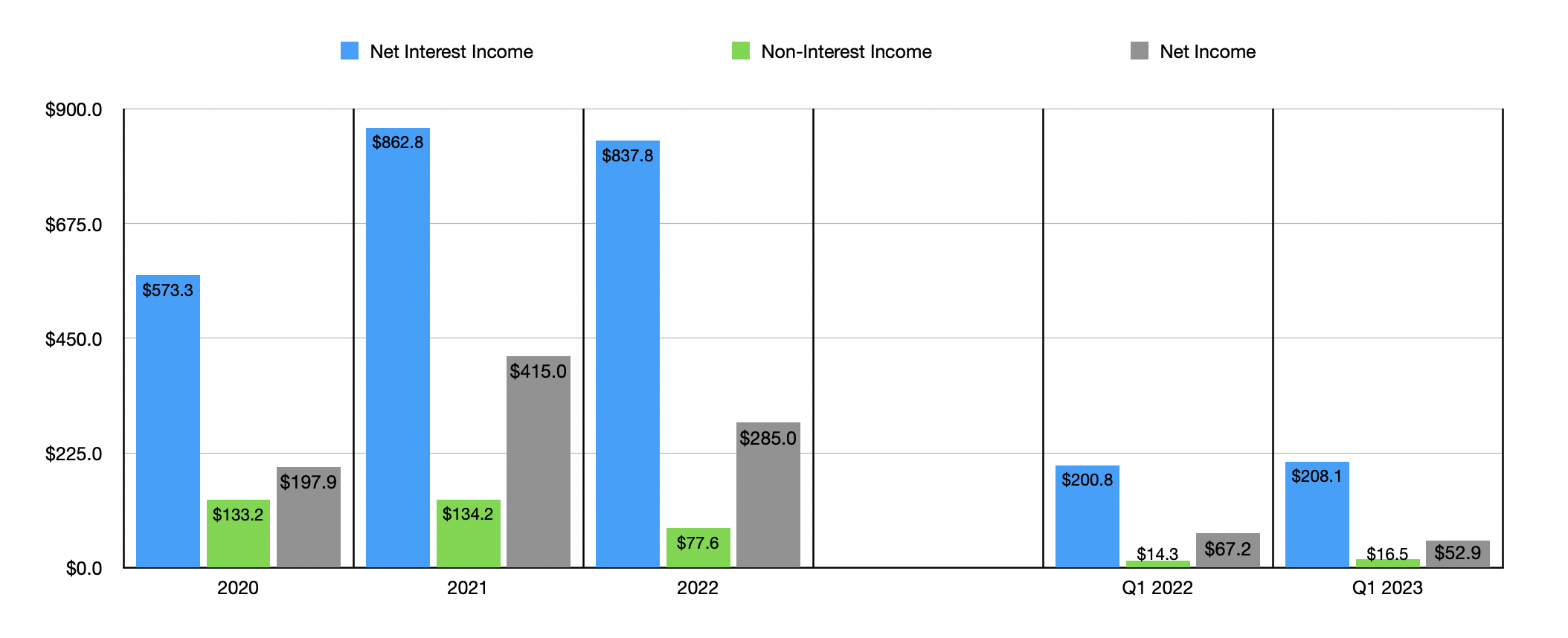

Another area that has been mixed for the company has been its profitability. Net interest income for the firm grew from $573.3 million in 2020 to $837.8 million in 2022. It is true that non-interest income declined during this timeframe from $133.2 million to $77.6 million. But the most important thing is the net interest income. That allowed net income for the company to grow from $197.9 million in 2020 to $415 million in 2021. But in 2022, this number was slashed significantly to $285 million. That weakness for the bottom line continued into the 2023 fiscal year. Even though net interest income increased from $200.8 million in the first quarter of 2022 to $208.1 million in the first quarter of this year, and non-interest income grew from $14.3 million to $16.5 million, net income dipped further from $67.2 million to $52.9 million. The good news here is that this increase was really driven by a surge in ‘other non-interest expense’ from $12.4 million to $26.9 million. $6.9 million of this increase was driven by higher rebates that its customers were entitled to, while $4.4 million of the charge in total during the first quarter of 2023 was associated with operational and fraud losses. Generally speaking, these should all be considered transitory issues that should not repeat themselves in the long run.

{kind=link}

Author - SEC EDGAR Data

In addition to the stock looking cheap relative to both its book value per share and tangible book value per share, it's also cheap on an earnings basis. Even if we take the data from 2022 when net profits were depressed compared to 2021, shares are trading at a price to earnings multiple of only 5.5. The average trading multiple in this space is about 16 from what I have seen, though many of the firms I have analyzed up to this point range between ~6 and 12.

Takeaway

All things considered, I must say that I am rather mixed in terms of how I feel regarding BankUnited. On the whole, the company looks quite attractive. Shares are cheap and the company has a good history of growing its loan portfolio. I am a little uncomfortable with the increase in borrowings and the high uninsured deposit amounts. But the fact that management demonstrated a growth in deposits only the third week out from the start of the crisis is encouraging. Of course, we will have to see what new data becomes available when management announces results covering the second quarter of the company's 2023 fiscal year. But absent something significant and unexpected, I do believe the company is cheap enough to warrant a cautious ‘buy’ rating at this time.

For further details see:

BankUnited: Worth Consideration Despite Some Weak Spots