BANX - BANX: Diving Further Into This Fund

2023-10-13 11:48:54 ET

Summary

- ArrowMark Financial Corp. offers investors a portfolio of floating rate exposure that has been benefiting from the rise in interest rates.

- The fund's distribution rate based on the regular dividend and share price puts the yield at 10.5%, which could reflect the returns going forward.

- The fund's share price is at a discount of ~20% to its last reported NAV, making it an attractive investment opportunity.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Earlier last month, we gave ArrowMark Financial Corp ( BANX ) a full review . We had noted the strong and growing income the fund was throwing off and that a raise or a large year-end special would be required.

It only took a few hours for that to become true, as later in the day, they announced they were taking the quarterly dividend from $0.39 to $0.45. That was good for a 15.4% increase.

Around a week later, they followed that up with the announcement of the year-end special. This was expected because they were still earning a significant amount of income. Due to regulations of their structure as a regulated investment company, they are still earning too much income in their underlying portfolio and would be subject to an excise tax (they paid out a small bit in the prior year but nothing too egregious).

Some websites, CEFConnect, in particular, are showing that the $0.42 is the regular distribution now when it was only a special. That could be causing some confusion as it made it appear like they raised their payout but then immediately lowered it. With that, the distribution rate for the fund based on the regular dividend and the last closing share price puts the yield at a compelling 10.5%.

The ex-date for that special is still coming up on October 19th. However, for the latest quarterly payout, the ex-dividend date was September 21st. When the fund initially announced the increase, it actually shot quite a bit higher but has sunk lower after that initial enthusiasm. The overall market is sinking through September, and that's holding up its reputation as the worst month which is most definitely not helping investor sentiment.

YCharts

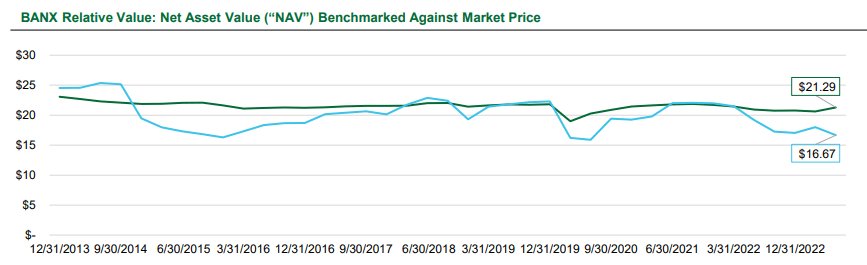

At the same time, the fund's share price against its last reported NAV provides for an estimated discount of -19.81%. That makes it still a really attractive deal on the market today with a high distribution rate that is easily being covered. It is so well covered that they need to pay out specials.

With all that being said, I wanted to provide a brief update today because I was able to have a video conference with some of the team at ArrowMark Financial Corp .

This included the Chairman & CEO, who is also the portfolio manager, Sanjai Bhonsle. In addition, Patrick Farrell, the CFO, and Dana Staggs, the President. In addition, the call included Jake Schultz of Destra Capital. Destra runs the investor relations and marketing for shareholders of BANX, as well as partnering with other popular closed-end fund sponsors to offer these shareholder services.

Despite being a more casual impromptu video call, there were a few questions that I thought were particularly interesting that could be shared with investors of BANX that they also might find helpful.

Quarterly Financial Updates

One of the first questions I had was on their quarterly results . These abruptly ended after Q3 2022. I was wondering if they were looking to provide any more financial information quarterly as, generally speaking, the more information, the better to make better decisions.

The response was that when doing these quarterly calls, they felt they were looked at more like a business development company. They had noted they felt that investors were looking at them more like a BDC, and they felt that included delivering potential capital appreciation as well as the distribution.

However, their main goal is to keep NAV as steady as possible and deliver a sustainable and solid dividend yield to investors. Which is something they've been able to deliver on. If you look at their historical NAV, it's one of the more straight lines you'll see.

However, do note that they only took over this fund around 2020 and started really changing the investment focus to regulatory capital relief securities (more details on those in a minute!) after that.

{kind=link}

While there are inevitably going to be some increases and decreases in the valuations of their underlying portfolio, the outlook for returns going forward is certainly encouraging. If they are delivering a ~10%+ distribution yield that is fully covered and they manage to keep their share price flat, that means an investor can expect a roughly 10% annual return based on receiving the yield throughout the year on today's prices. The dividend rate on the NAV is at ~8.25%. So, that would be the expected return going forward if they maintain NAV.

Where additional returns could come for investors in BANX is from the share price rising to trade closer to the NAV. At a ~20% discount, the chances for this actually seem fairly promising. Thus, if you aren't happy with a 10% annualized return but want to speculate on some appreciation, that could boost your results.

While they stopped posting quarterly results, when announcing dividends, they noted the NII for the quarter, which was helpful. However, one thing they said they would be looking to provide going forward is more quarterly figures, even if that doesn't include the return of the whole conference call to discuss results.

Some of my own speculation is also that it's a smaller fund, and that could've played a role in the decision, too. The participation in the calls could have been quite low, meaning that it probably wasn't worth the time, effort, or potential costs vs. the benefit. Still, if they return to providing more financial numbers in their quarterly presentations, that can be helpful to shareholders to make better investment decisions. In particular, those Q1 and Q3 periods can be great to fill in some gaps due to a long 6-month stretch between the semi or annual reports posted.

More On Regulatory Capital Relief Securities

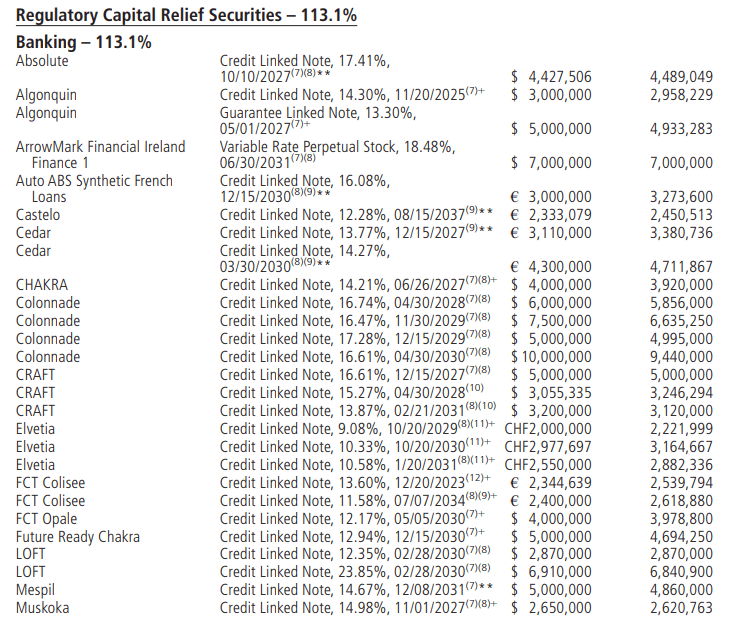

Given that 85.6% of the portfolio is comprised of these regulatory capital relief securities, which are quite opaque, it no doubt raises some questions.

BANX Portfolio Exposure (ArrowMark)

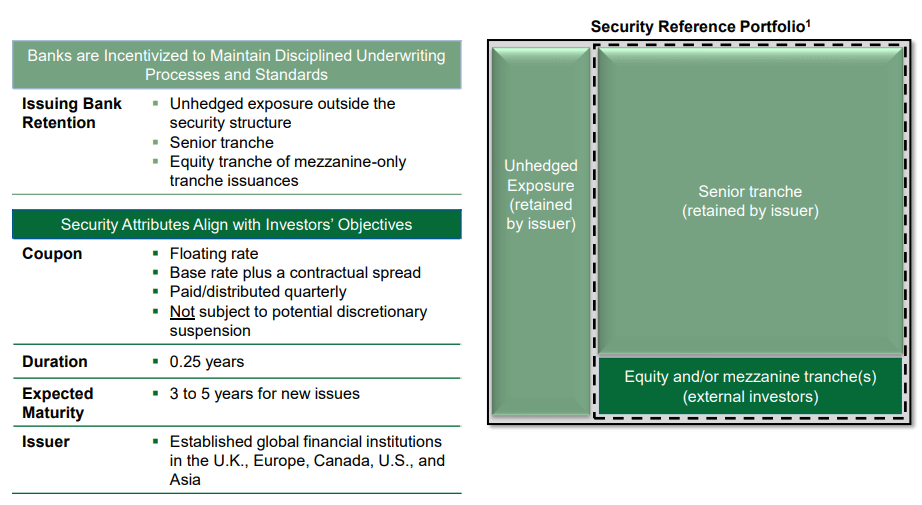

The general concept of these securities is they help provide support to banks and other financial institutions to meet their regulatory requirements, essentially providing "capital relief" to these institutions as their name would imply. For BANX they are investing in mostly credit-linked notes.

It is noted that these are usually issued by large money center banks that are included as globally systemically important banks or G-SIBs. The banks that if they go down, then the whole economic world collapses.

For BANX, I was told that they are either issued by G-SIBs or very nearly G-SIBs - that they would be household names that are going to be well known.

However, when looking at the names provided for their holdings in a semi or annual report, these certainly aren't names of entities that we are familiar with. In fact, any Google search sends you back to BANX material usually. We are provided with some investment information, such as the yield and maturity, which is certainly helpful. But the names are definitely not any financial institutions I've heard of.

{kind=link}

And that is when they mentioned that all of these are private negotiations and they have non-disclosure agreements ("NDAs") with these entities. These are the names of the securities that have been issued them, but they aren't the normal operating bank names that we see walking down the street, such as JPMorgan ( JPM ), Bank of America ( BAC ) or Wells Fargo ( WFC ), to name a few G-SIBs.

That's when it clicked with me why all their presentations only provide hypothetical or "illustration purposes only" material in their investor presentations. They legally aren't allowed to disclose the specifics.

Now, that definitely puts investors in a situation where we are relying on management almost entirely, but there is no way around it. This is more or less similar to the collateralized loan obligation ("CLO") funds.

Still, the hypothetical details are going to be our best insight into what the securities could predominantly look like. That includes the fact that the weighted average credit quality of the portfolio is investment grade at BBB-.

{kind=link}

They carry low durations due to being floating rates and having short maturities. I was also told that there are generally anywhere from 200 to 300 issuers in each security, so definitely diversified. It was also mentioned that the majority of these mature after 5 years but will often start amortizing after 3 years. That is, they start receiving principal and interest payments back.

That can be a good thing as they can take more capital to invest in potentially better-negotiated deals as rates are rising.

What is also another potential positive mentioned by the management team is that with greater regulations the Fed is looking to put into place on financial insulation, they are expecting more demand through 2023 and into next year. More demand for issuing these types of securities is good for the buyers as they can get better terms when there is a greater supply trying to come to market.

Jamie Dimon, as well as other bank leaders, for fairly obvious reasons, have been a loud critic against requiring strengthened regulations.

Dividend Sustainability

On this front, I had asked the management team if they believed that their new $0.45 quarterly dividend was something that would be sustainable even if rates were to be cut in the next year or two. I was told that first, they don't expect rates to go back to the zero rate environment. I thought that was a fair first point.

Secondly, they did mention that the income growth generated in the portfolio wasn't from the rising interest rates alone. They had the opportunity to sell shares in the prior years due to trading at a premium to their NAV. Of course, we are far away from a premium now, so new shares wouldn't be accretive if issued. Therefore, they haven't seen any proceeds from share sales this year.

YCharts

With that being said, they felt that they set their dividend level where they felt comfortable that they could sustain it if rates came down.

I also asked the obligatory question that's required of any quarterly paying CEF, and that is if they've considered switching to a monthly dividend. They said no, it hadn't come up for discussion. Cash inflows from the underlying portfolio come in quarterly, and they line up those cash inflows with the dividend cash outflow, so they have no intent on making any switch.

For further details see:

BANX: Diving Further Into This Fund