BHB - Bar Harbor Bankshares: A 4.7%-Yielding Small Cap Dividend Growth Gem

2023-09-26 17:07:12 ET

Summary

- Bar Harbor Bankshares is a small cap regional bank based in Bar Harbor, Maine, with over 50 branches across Maine, New Hampshire, and Vermont.

- BHB remains highly profitable with a net interest margin of 3.2% and a core return on tangible equity of 15.2%.

- The current stock price of $23.85 is a 12% discount to book value per share, making it an attractive buying opportunity.

- The loan book, including office building mortgages, remains in great shape, and the deposit base has proven to be sticky.

- Dividend growth investors should take note of BHB's 4.7% dividend yield and two decade dividend growth track record.

Bar Harbor Bankshares ( BHB ) is a small cap regional bank based in the touristy town of Bar Harbor, Maine, and operates over 50 branches across Maine, New Hampshire, and Vermont. Bar Harbor's adjacency to Acadia National Park makes it a frequent stop for cruise ships in the summertime, and the town bristles with tourists in the Autumn due to the beautiful, changing leaves.

More pertinent to investors, as of the Q2 2023 earnings report , BHB remains highly profitable with a net interest margin of 3.2% and a core return on tangible equity of 15.2% (down from a high of 19.0% in Q4 2022). Meanwhile, the loan book continues to demonstrate its conservatism via virtually zero loan losses.

The current stock price of $23.85 is a roughly 12% discount to book value per share of $27.12, as of June 30th, 2023. This is the bank stock's cheapest valuation since coming out of the COVID-19 pandemic.

The regional bank faces many of the same headwinds as other banks, such as rising cost of deposits. Plus, its loan-to-deposit ratio of 97% is quite high. But unlike other banks, BHB's total deposits have held steady, even rising slightly year-over-year in Q2 2023.

In short, it's steady as she goes at BHB even through the most difficult environment for banks since the Great Recession. That makes it and its 4.7%-yielding dividend an attractive buying opportunity.

Update On Bar Harbor Bank

BHB began over 135 years ago as a community bank serving the little town of Bar Harbor but has expanded (via acquisitions of other community banks) over the years across Maine and into New Hampshire and Vermont.

{kind=link}

Being a smaller bank, BHB is not the most efficient in terms of its operating expenses as a share of revenue. The efficiency ratio typically sits in the high 50% range and reached 60% in Q2 2023. (A lower efficiency ratio is better, as it indicates fewer dollars of expenses spent per dollar of revenue.)

Fortunately, BHB's other qualities make up for its lack of peer-leading efficiency ratio.

What are those positive qualities? I'd group them into two categories:

- A strong and conservative loan book

- A loyal and steady depositor base

The Conservative Loan Book

The loan book breaks down as follows:

| Commercial Real Estate |

| 51.6% |

| Residential Real Estate |

| 30.2% |

| Commercial & Industrial |

| 12.9% |

| Consumer |

| 3.2% |

| Tax Exempt & Other |

| 2.1% |

So far this year, BHB has enjoyed strong loan growth on the commercial side. CRE loans increased 9% in Q2 and 8% YTD, while C&I loans increased 26% in Q2 and 20% YTD.

While this lending did bring BHB's loan-to-deposit ratio up to 97%, the deposit base has been remarkably stable, as we'll discuss below.

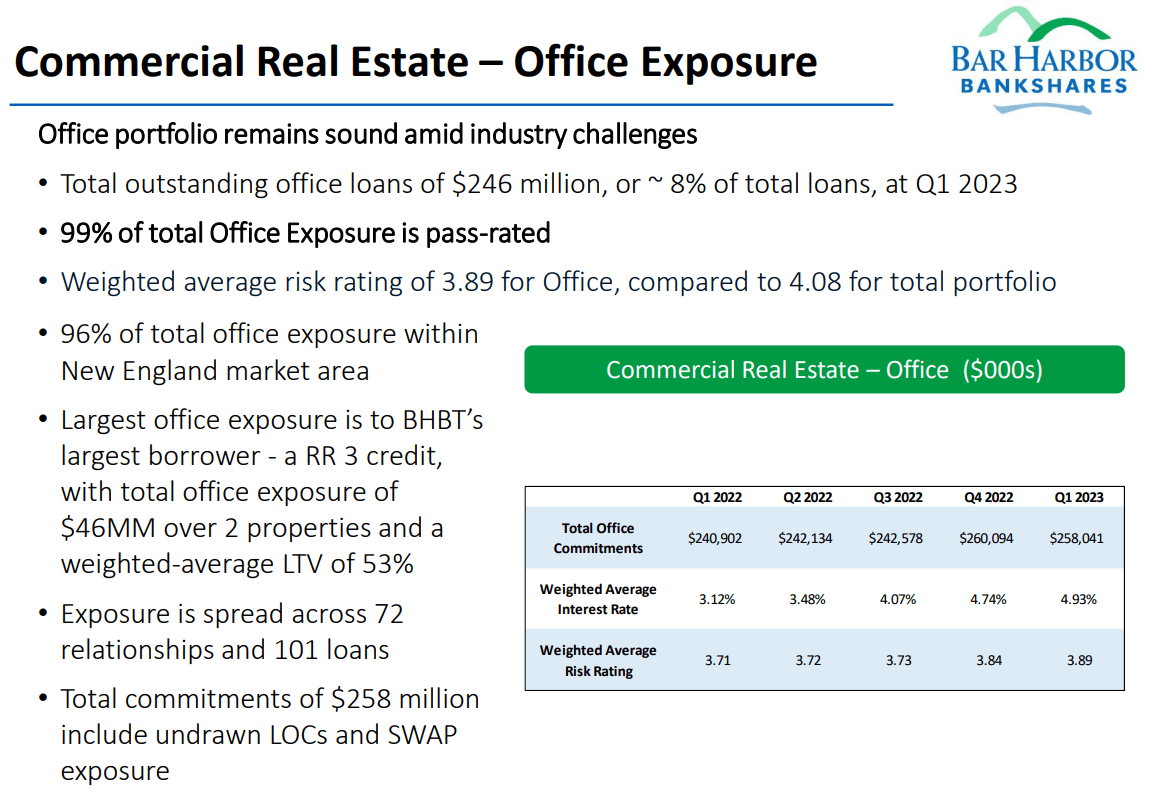

When it comes to the safety and quality of the loan book, investors tend to be most concerned right now about exposure to office buildings. Around 8% of BHB's total loans were collateralized by office properties as of Q1 2023. What is striking is the apparent stability and conservatism of this portion of the loan book.

{kind=link}

"Pass-rated" means that the loan is highly likely to be serviced and repaid in a timely manner and without interruptions, and that there are no known threats to the borrowers' ability to repay the loans.

Notice that the largest office loan covers two properties and has a weighted average loan-to-value of 53%. With so much equity in the properties, the borrower is highly unlikely to simply default and walk away from these assets. If this LTV is representative of the overall office exposure, loan losses and non-performance should remain quite limited for BHB's office segment.

But the numbers speak for themselves.

- CRE accounts for 13.6% of non-performing assets despite making up 51.6% of total loans

- Total non-performing loans as a percentage of total loans was 0.22% in Q2 2023, down from 0.29% in Q2 2022

- Total delinquent and non-accruing loans as a percentage of total loans was 0.33%, down from 0.41% in Q2 2022

- Allowance for credit losses as a percentage of total loans crept up to 0.91% in Q2 2023 from 0.87% in Q2 2022

- Allowance for credit losses was 408% of non-accruing loans in Q2 2023, compared to 300% in Q2 2022

- Net charge-offs (loan losses) were zero in Q2 2023 and have been virtually zero over the last five quarters

Aside from slightly lifting allowances for credit losses (perhaps simply out of an abundance of caution), BHB's asset quality metrics are all trending in the right direction. There are almost no credit losses or delinquencies, including for office building loans.

Sticky Depositor Base

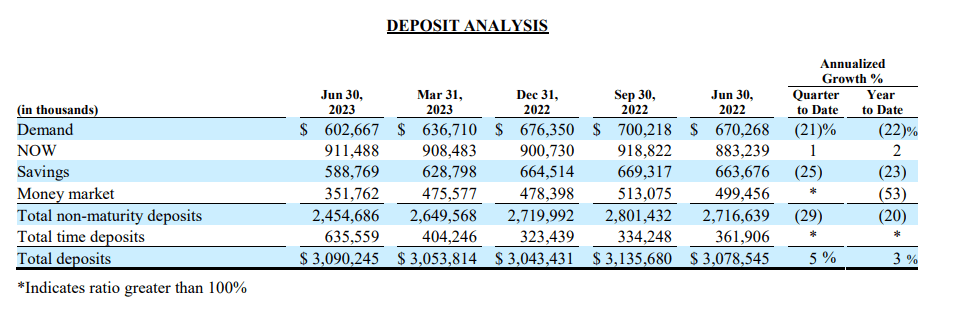

BHB's deposit base has proven quite sticky and loyal during the current rising interest rate cycle. Lots of other banks are seeing net outflows, but BHB's total deposits have held steady.

| Q2 2023 |

| Q1 2023 |

| Q4 2022 |

| Q3 2022 |

| Q2 2022 |

| $3.09 billion |

| $3.05 billion |

| $3.04 billion |

| $3.14 billion |

| $3.08 billion |

This stability starts with the financial health of the Northern New England region.

To quote CEO Curtis Simard from the Q2 2023 earnings report:

We serve a stable and diversified customer base with deposits from nearly all banking segments, including consumer, high net worth, small businesses, larger corporate, government agencies and commercial real estate. And here in the first half of 2023, these markets have remained resilient in the face of an uncertain macroeconomic environment. Unemployment rates remained stable within our footprint, continuing to come in below the national average. We believe that the consumer remains financially healthy, and our business customers continue to seek ways to expand and optimize their operations where it makes sense.

So, BHB's customers (often both borrowers and depositors) are financially healthy, which feeds a virtuous cycle for the economy of the region.

But, of course, when high-yield savings accounts and money markets are paying over 5% interest rates, it is naturally difficult for a bank to keep its depositors around, at least insofar as long-term savings are concerned. That's why it's good to see that BHB's depositors have kept their money at the local bank, for the most part.

Although there hasn't been a net outflow of deposits like for some banks, there has been a shift in deposits from non-interest bearing and low-yield savings accounts to time deposits (e.g. certificates of deposit) as depositors seek out higher yielding options for their parked cash.

{kind=link}

This shift began at the beginning of this year and really picked up steam in Q2 2023.

Just breaking it down to non-maturity deposits (generally non-interest bearing or low-interest bearing) versus time deposits (often the highest yielding deposit option offered by banks), we see a big jump from Q1 to Q2 of this year.

| Non-Maturity Deposits |

| Time Deposits |

| Q2 2023 |

| 21% |

| 79% |

| Q1 2023 |

| 13% |

| 87% |

| Q4 2022 |

| 11% |

| 89% |

| Q3 2022 |

| 11% |

| 89% |

| Q2 2022 |

| 12% |

| 88% |

| Q1 2022 |

| 13% |

| 87% |

This shift from lower yielding to higher yielding deposit accounts has caused BHB's cost of interest-bearing deposits to surge from 0.2% in Q2 2022 to 1.45% in Q2 2023. Including BHB's own debt into the picture, the bank's total cost of liabilities sits at 1.99% in Q2 2023, up from 0.36% in Q2 2022.

Compare that to its yield on earning assets of 4.77% in Q2 2023, up from 3.46% in Q2 2022.

This has caused the pre-tax net interest margin to compress somewhat over the last year. It will probably compress further in the second half of this year as the Fed has hiked rates one more time, and depositors have plenty of time to make the decision to shift money into higher-yielding accounts.

This, in my view, is the biggest headwind facing BHB. But personally, I would rather see a loyal depositor base that keeps its money with BHB and simply wants to take advantage of the high yields on cash equivalents rather than pulls money out of BHB entirely to pursue higher yielding options outside the bank.

Bottom Line

If BHB suffered from a higher cost of deposits, a net deposit outflow, and problems in its loan book, it would probably deserve the stock's current selloff.

But it only suffers from one of those (higher deposit costs), which is perhaps the most temporary.

As such, the lower price to book/tangible book value makes BHB look like a good buying opportunity for long-term investors.

Plus, for dividend growth investors like me, it's worth emphasizing that the small bank has a 20-year record of consecutive dividend growth. The dividend typically grows at around 6% per year, but the most recent hike in April was 7.7% -- a vote of confidence in the bank's future from the board.

Since the mid-2000s, BHB has dramatically outperformed both the broader financials sector ( XLF ) and especially other regional banks ( KRE ).

It also outperformed the S&P 500 ( SPY ) from the mid-2000s to about 2018. I don't fault it for underperforming the SPY since then, because virtually everything besides seven mega-cap stocks have underperformed the market since then.

BHB under $24 per share is a gift to investors. Buy for the conservative long-term growth, and enjoy the 4.7%-yielding dividend while you wait to see it.

For further details see:

Bar Harbor Bankshares: A 4.7%-Yielding Small Cap Dividend Growth Gem