BHB - Bar Harbor Bankshares: A Bit Premature For A Downgrade

2023-12-19 11:03:12 ET

Summary

- Bar Harbor Bankshares has seen a 15% return compared to the S&P 500's 1.3%.

- The bank's net interest income and net profits have remained stable, with slight decreases in the third quarter.

- The bank has shown improvements in loans, cash equivalents, and a decline in debt but a drop in the value of securities.

- In all, the stock still looks cheap and warrants further upside from here.

Unless it's a very special situation, I don't think it's necessarily wise to monitor your investments on a day-to-day basis. But you should definitely pay attention to them at least once every quarter. Otherwise, you miss out on potentially large movements and data that can lead to large movements. Just because you revisit a firm does not mean that you need to upgrade it or downgrade it. Though, you should definitely incorporate any new data that comes in when it comes to evaluating whether the prospect you thought was appealing still is.

Earlier this year, in July to be precise, I ended up taking a bullish stance on Bar Harbor Bankshares (BHB), a very small bank that experienced tremendous downside because of the banking crisis that negatively affected that sector. Unlike many of the institutions that ultimately collapsed or came close to it, Bar Harbor Bankshares is far removed from all of the havoc. I say this because it is headquartered in northern New England, with branches across Maine, New Hampshire, and Vermont. This distance, combined with other factors like low uninsured deposit exposure and a history of deposit growth, led me to rate the bank a 'buy'. Since then, we have seen two additional quarters worth of data come out and shares have seen upside of 15% compared to the 1.3% seen by the S&P 500. Such a return disparity makes a downgrade tempting. But at this moment, I think that might be just a little premature.

Robust stability is the name of the game

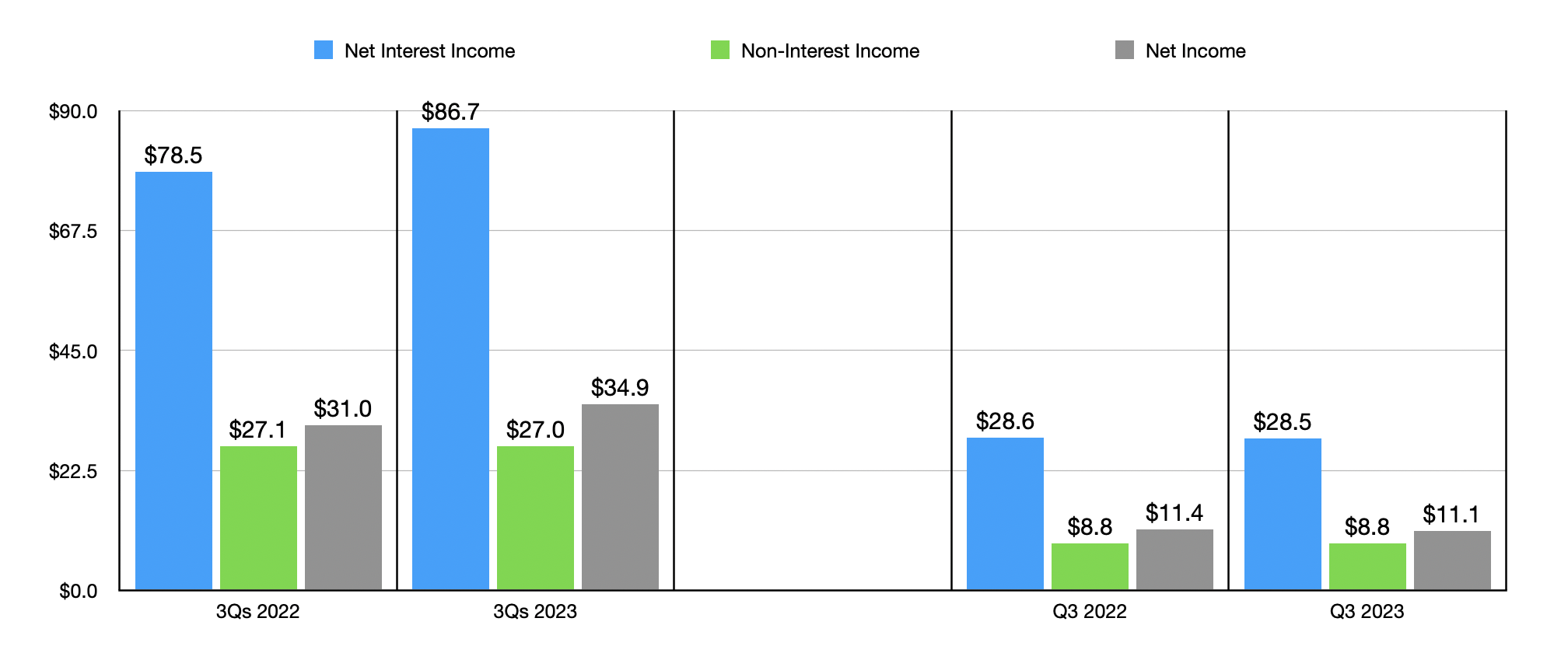

Back when I last wrote about Bar Harbor Bankshares earlier this year, the bank only had data covering through the first quarter of the 2023 fiscal year. Since then, data for two additional quarters has come out. To start with, we should touch on the most recent quarter. During that time, net interest income came in at $28.5 million. That's almost even with the $28.6 million generated the same time last year. Non-interest income remained flat at $8.8 million, while net profits inched down slightly from $11.4 million to $11.1 million.

{kind=link}

To be clear, relative to the rest of the year, the third quarter was actually a bit weak. I say that because, when you look at data for the first nine months of the year, you would see that net interest income expanded from $78.5 million last year to $86.7 million this year. Non-interest income pulled back slightly from $27.1 million to $27 million. But that didn't stop net profits from climbing from $31 million to $34.9 million. When you dig into the numbers, you find that a slight decrease in the company's net interest margin was pretty much all that was stopping it from growing year over year. As an example, in the third quarter, the net interest margin was 3.18%. That was down from the 3.47% seen one year earlier. Management attributed this to higher costs associated with funds in order to keep assets on the books. This is common amongst banks at this point in time.

{kind=link}

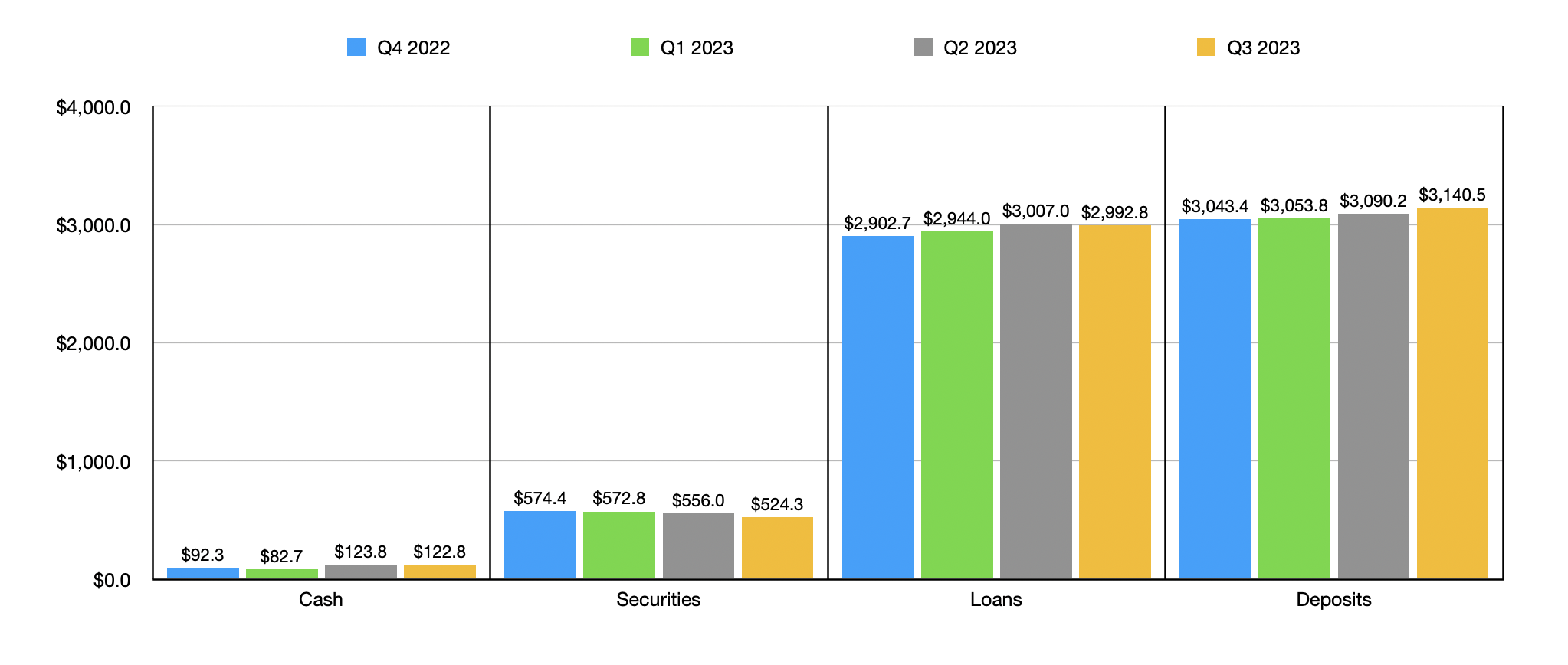

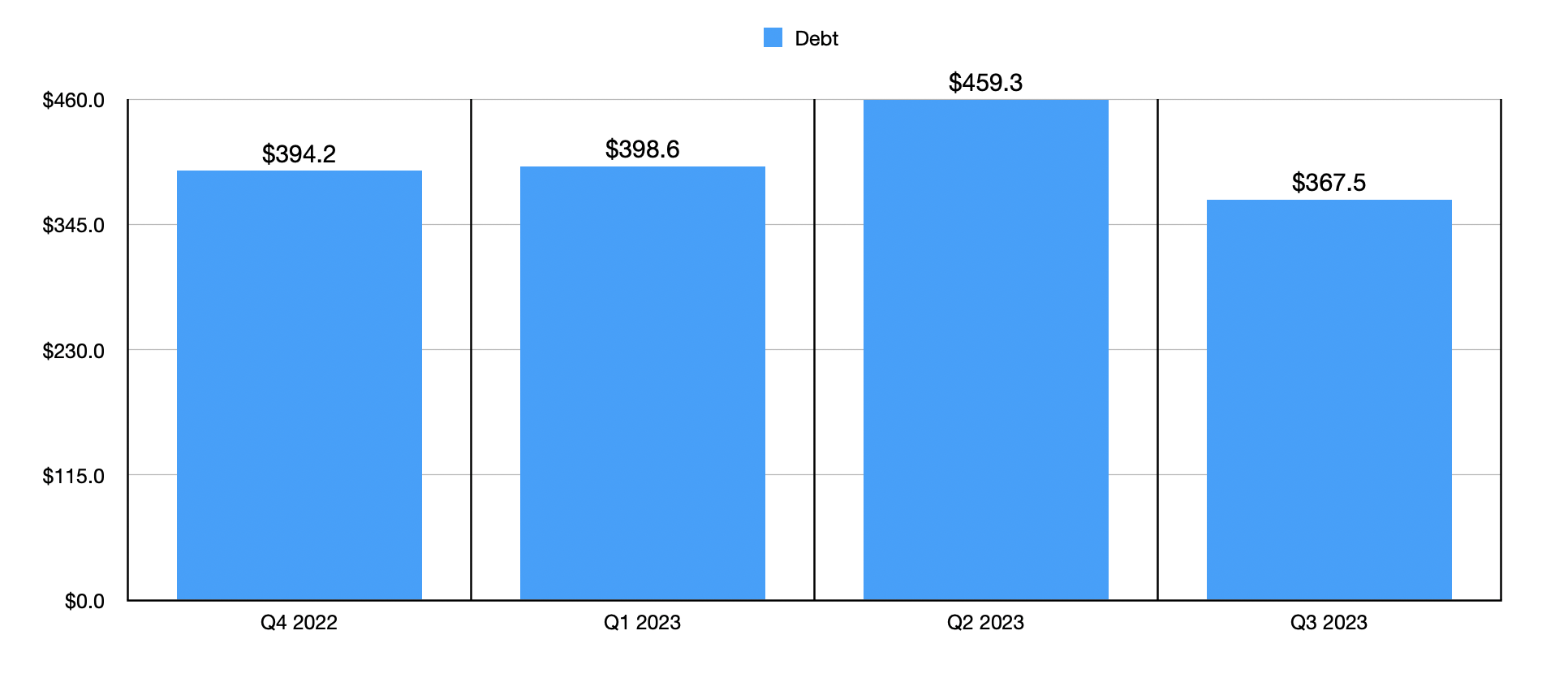

Even though the firm's net interest margin weakened year over year, there were some improvements that helped to offset this. Take, as an example, the value of loans on its books. At the end of 2022, the institution had $2.90 billion worth of loans. By the end of the third quarter of this year, the value of loans on the company's books had grown slightly to $2.99 billion. It is worth noting that the firm's exposure to the much-hated office assets that are out there has remained quite low at only 8% of its total portfolio. That is most promising to see. From the end of last year through the end of the third quarter, another area which the bank has improved has been the cash and cash equivalents on its books. This actually expanded from $92.3 million at the end of last year to $122.8 million today. This is not to say that everything on the books got better. The value of securities, meanwhile, dropped, declining from $574.4 million to $524.3 million. But in my opinion, this has been more than offset by a further decline in debt from $394.2 million to $367.5 million.

{kind=link}

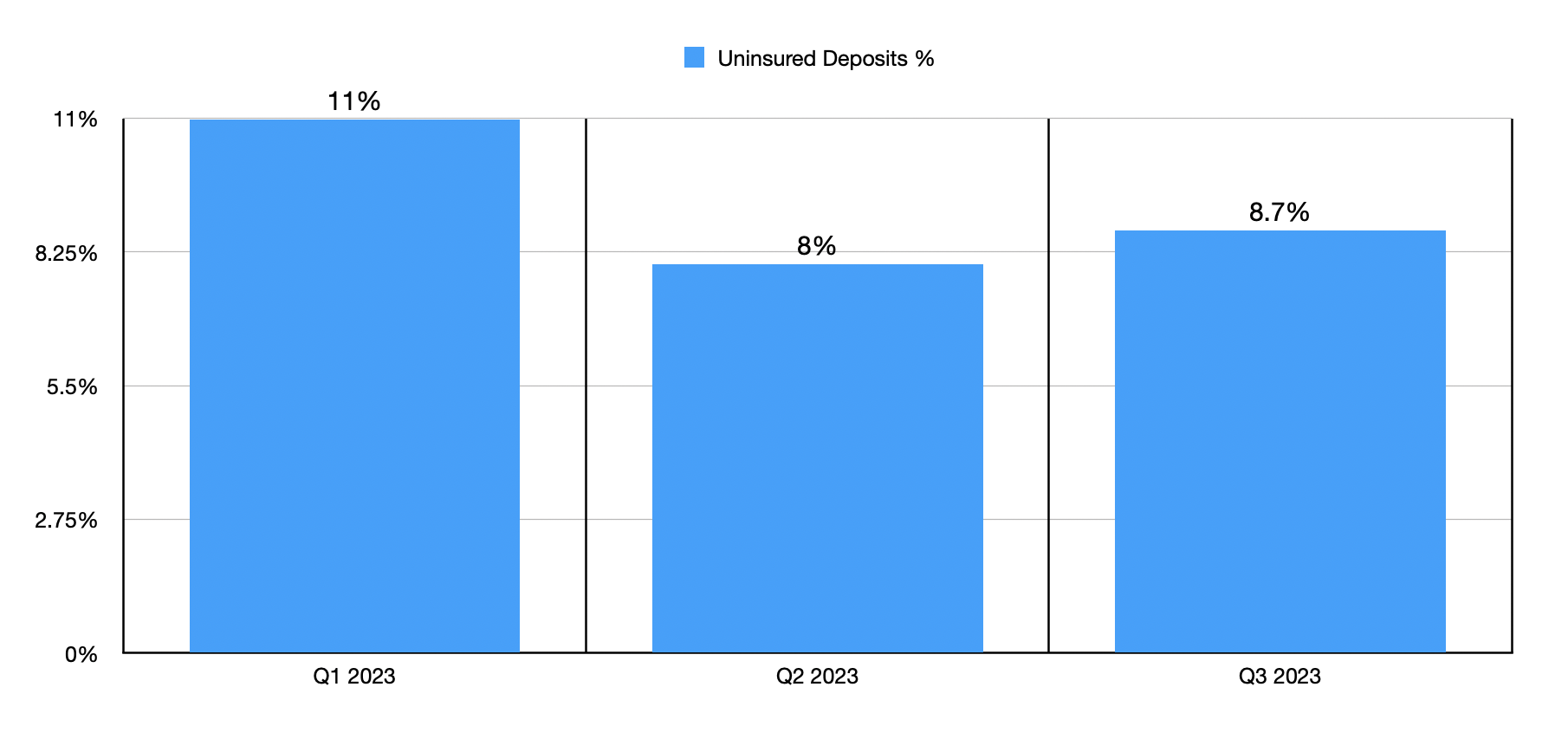

All of this is great to see. But perhaps the most important metric to look at would be the value of deposits. After all, it's the value of deposits that ultimately determines whether a bank is experiencing issues or not. Many institutions earlier this year reported significant declines because of uninsured deposit exposure. However, Bar Harbor Bankshares seemed immune to that. At the end of last year, the institution had $3.04 billion of deposits. These expanded to $3.05 billion in the first quarter. As of today, we are up to $3.14 billion. That's an increase since the end of last year of $97.1 million. It's very likely that a lot of this upside was made possible by the low amount of uninsured deposit exposure that the institution has to deal with. At the end of last year, only 11.2% of deposits were uninsured. That number is even lower today at 8.7%.

{kind=link}

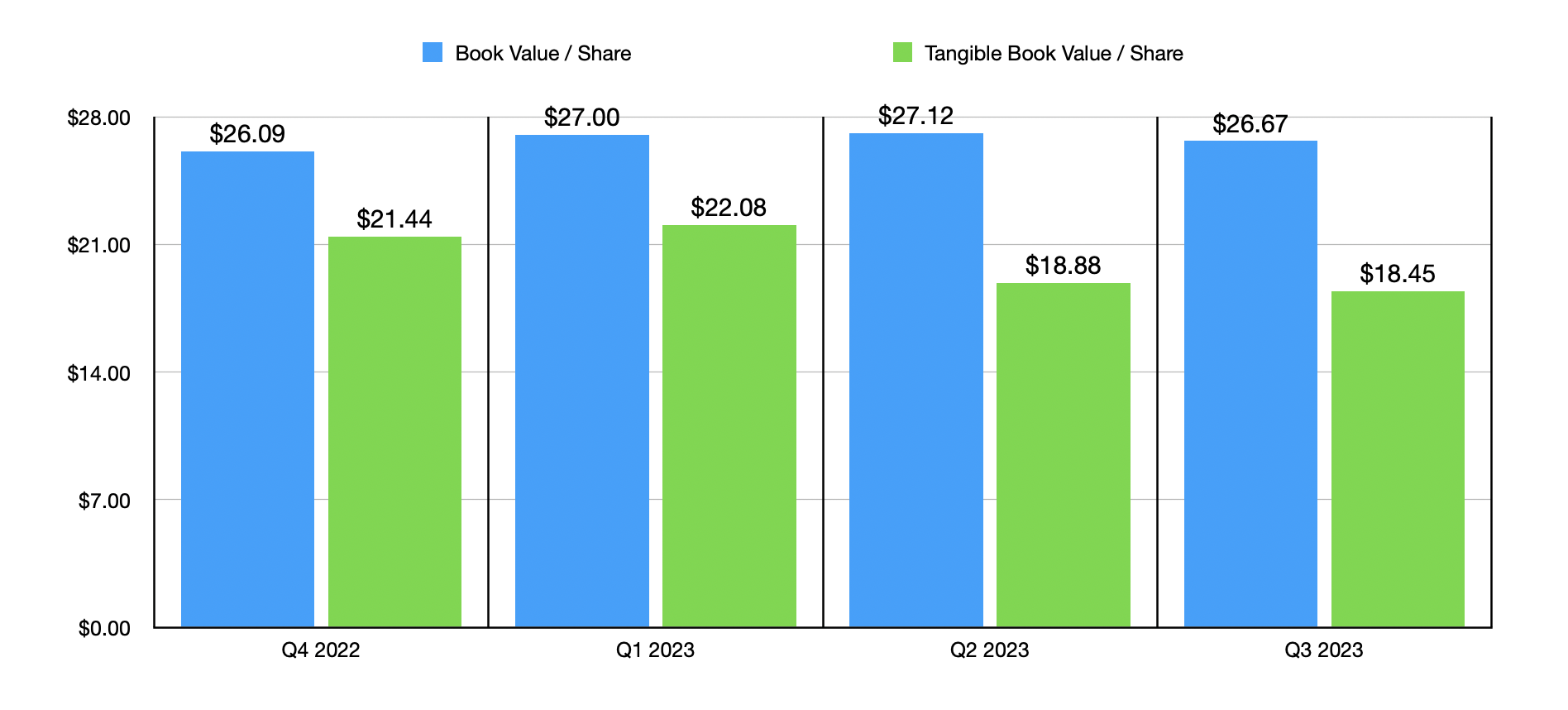

In terms of valuation, the stock still looks attractively priced, but it's not in what I would call the bargain basement. If we use financial results from last year to be safe, the firm seems to be trading at a price to earnings multiple of about 9.6. This is lower than many institutions that I have seen this year. But it's not anywhere near the lowest. The price to book multiple, meanwhile, implies a premium to book value of about 2.2%, while the price to tangible book value premium is about 49.1%. Neither of these are great, but they aren't horrible either. There are some other players in the space that are trading at discounts to book value and even some trading at discounts to tangible book value.

{kind=link}

Takeaway

As far as things stand today, I would argue that Bar Harbor Bankshares is still doing fine for itself. The bank is not the kind of institution to experience rapid growth. Rather, it is seeing growth in the areas that are most important. Overall financial performance on the top and bottom lines remains decent for the current fiscal year. And when you add on to that how shares are currently priced, I do believe that the 'buy' rating I assigned the bank is still logical at this time.

For further details see:

Bar Harbor Bankshares: A Bit Premature For A Downgrade