BHB - Bar Harbor Bankshares: Downgrading To Hold Earnings Outlook Is Lackluster

2023-12-21 10:41:23 ET

Summary

- The labor market and personal income are positive indicators for loan growth. Unfortunately, high house prices bode ill for loan growth.

- The net interest margin will likely gradually trend upwards next year amid a rate-cut environment.

- The December 2024 target price suggests a small upside from the current market price. Further, BHB is offering a moderate dividend yield.

Earnings of Bar Harbor Bankshares (BHB) will likely remain stable in upcoming quarters. A lower average net interest margin will likely counter the effect of loan growth. Overall, I’m expecting the company to report earnings of $0.71 per share for the last quarter of 2023, and $2.94 per share for 2024. Next year’s target price suggests a small upside from the current market price. Based on the total expected return, I’m downgrading Bar Harbor Bankshares to a Hold Rating.

Economic Factors Present a Mixed Outlook for Loans

Loan growth has slowed down considerably this year after an impressive performance last year; however, this year’s growth is in line with the compounded average growth rate for the last five years. Moreover, the growth witnessed so far this year is somewhat in line with my previous expectations given in my last report, which was issued before the release of the first quarter’s results.

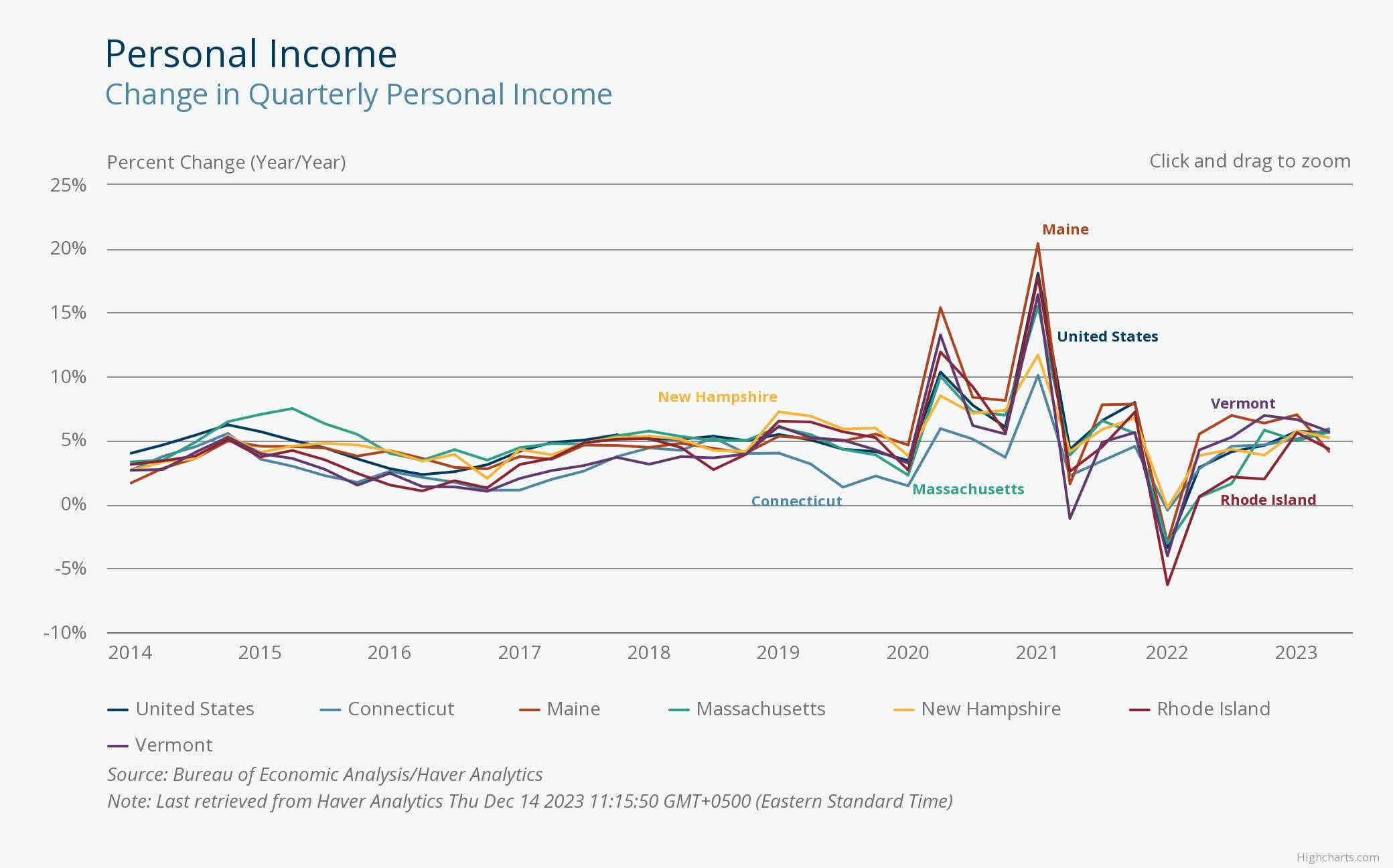

Macroeconomic factors currently present a mixed picture; therefore, I think loan growth will likely continue at the same rate as the first nine months of this year. Bar Harbor operates in the New England states of Maine, New Hampshire, and Vermont. The region’s labor market has performed very well in the last few months, which indicates a robust business environment. As shown below, the unemployment rate has dipped substantially in recent months.

Moreover, personal income is still growing at a satisfactory rate (near the 5% line in the graph below) despite a slowdown in recent months.

{kind=link}

However, the environment for residential mortgages is still far from conducive. After stagnating in the latter part of 2022, house prices are on a steep uptrend once again, as shown below.

Considering these factors, I’m expecting the loan portfolio to grow by 1.0% in the last quarter of 2023 and 4.1% in 2024. The following table shows my balance sheet estimates.

| Financial Position |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| FY24E |

| Net interest income |

| 90 |

| 99 |

| 96 |

| 114 |

| 118 |

| 120 |

| Provision for loan losses |

| 2 |

| 6 |

| (1) |

| 3 |

| 3 |

| 3 |

| Non-interest income |

| 29 |

| 43 |

| 42 |

| 35 |

| 36 |

| 36 |

| Non-interest expense |

| 90 |

| 95 |

| 91 |

| 91 |

| 93 |

| 97 |

| Net income - Common Sh. |

| 23 |

| 33 |

| 39 |

| 44 |

| 46 |

| 45 |

| EPS - Diluted ($) |

| 1.45 |

| 2.18 |

| 2.61 |

| 2.88 |

| 3.00 |

| 2.94 |

| Source: SEC Filings, Author's Estimates(In USD million unless otherwise specified) |

In my last report, I estimated earnings of $3.24 per share for 2023. I’ve reduced my earnings estimate because the margin has already performed much worse than I anticipated.

Risks Appear to be Manageable

Bar Harbor has two main sources of risk, as discussed below:

- Gross unrealized losses on the available-for-sale securities portfolio stood at $95.8 million at the end of September 2023, which is about 24% of the total equity balance. I’m expecting most of these losses to start reversing next year when interest rates start declining.

- Only a very small part of the deposit book is uninsured; therefore, deposits appear to be very low risk. As mentioned in the 10-Q filing, the estimated uninsured and uncollateralized deposits, excluding intercompany deposits, were just 8.7% of total deposits on September 30, 2023.

As a result, I think Bar Harbor’s overall risk is low.

Downgrading to a Hold Rating

Bar Harbor Bankshares is offering a dividend yield of 3.8% at the current quarterly dividend rate of $0.28 per share. The earnings and dividend estimates suggest a payout ratio of 38% for 2024, which is close to the five-year average of 42%. Therefore, I’m not expecting any change in the dividend level.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value Bar Harbor. The stock has traded at an average P/TB ratio of 1.34 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2024 ($) |

| 20.0 |

| 20.0 |

| 20.0 |

| 20.0 |

| 20.0 |

| Target Price ($) |

| 22.8 |

| 24.8 |

| 26.8 |

| 28.8 |

| 30.8 |

| Market Price ($) |

| 29.2 |

| 29.2 |

| 29.2 |

| 29.2 |

| 29.2 |

| Upside/(Downside) |

| (21.8)% |

| (15.0)% |

| (8.1)% |

| (1.3)% |

| 5.6% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 12.0x in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| EPS 2024 ($) |

| 2.94 |

| 2.94 |

| 2.94 |

| 2.94 |

| 2.94 |

| Target Price ($) |

| 29.4 |

| 32.3 |

| 35.3 |

| 38.2 |

| 41.1 |

| Market Price ($) |

| 29.2 |

| 29.2 |

| 29.2 |

| 29.2 |

| 29.2 |

| Upside/(Downside) |

| 0.7% |

| 10.8% |

| 20.9% |

| 30.9% |

| 41.0% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $31.0 , which implies a 6.4% upside from the current market price. Adding the forward dividend yield gives a total expected return of 10.2%.

In my last report, I adopted a target price of $32.4 for the end of 2023 and gave a buy rating. Since then the stock price has rallied strongly. As a result, my new target price for the end of next year has only a small upside from the current market price. Based on the updated total expected return, I’m downgrading Bar Harbor Bankshares to a Hold rating.

For further details see:

Bar Harbor Bankshares: Downgrading To Hold, Earnings Outlook Is Lackluster