BHB - Bar Harbor Bankshares: Undervalued Despite Staging A Sizable Partial Recovery

2023-07-16 06:59:28 ET

Summary

- Bar Harbor Bankshares, a small bank holding company, has shown potential for investors despite a 33.7% drop in stock value during the banking crisis in March.

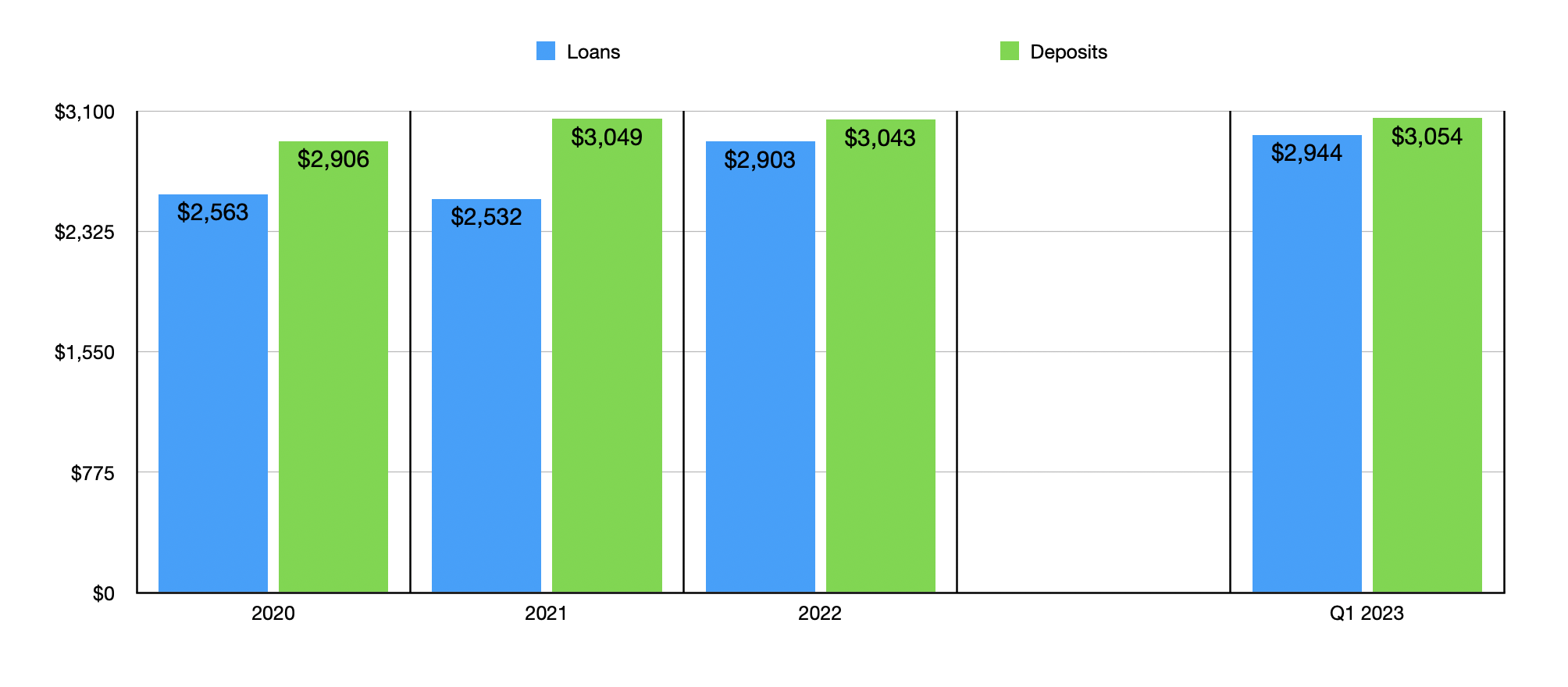

- The bank has shown growth in loans, from $2.56 billion in 2020 to $2.94 billion in 2023, and has a low exposure to uninsured deposits, with only 11% classified as such.

- Despite not trading at a discount to its book value, the bank has shown growth in net interest income and net profits, making it an attractive prospect for investors.

The great thing about a crisis is that it can open the door to many opportunities that can go on to generate attractive upside for the investors who are willing to accept some volatility. The banking crisis that began in early March of this year created many such opportunities. One of them that has played out well so far but that still has some additional upside to it involves a rather small bank holding company known as Bar Harbor Bankshares ( BHB ). At one point, from what shares were trading at on February 28th, the stock was down as much as 33.7%. A good chunk of that downside has been recovered though, with the stock now trading down only 17.6%. But even with that, investors are left with some attractive upside potential should everything go right.

A healthy prospect

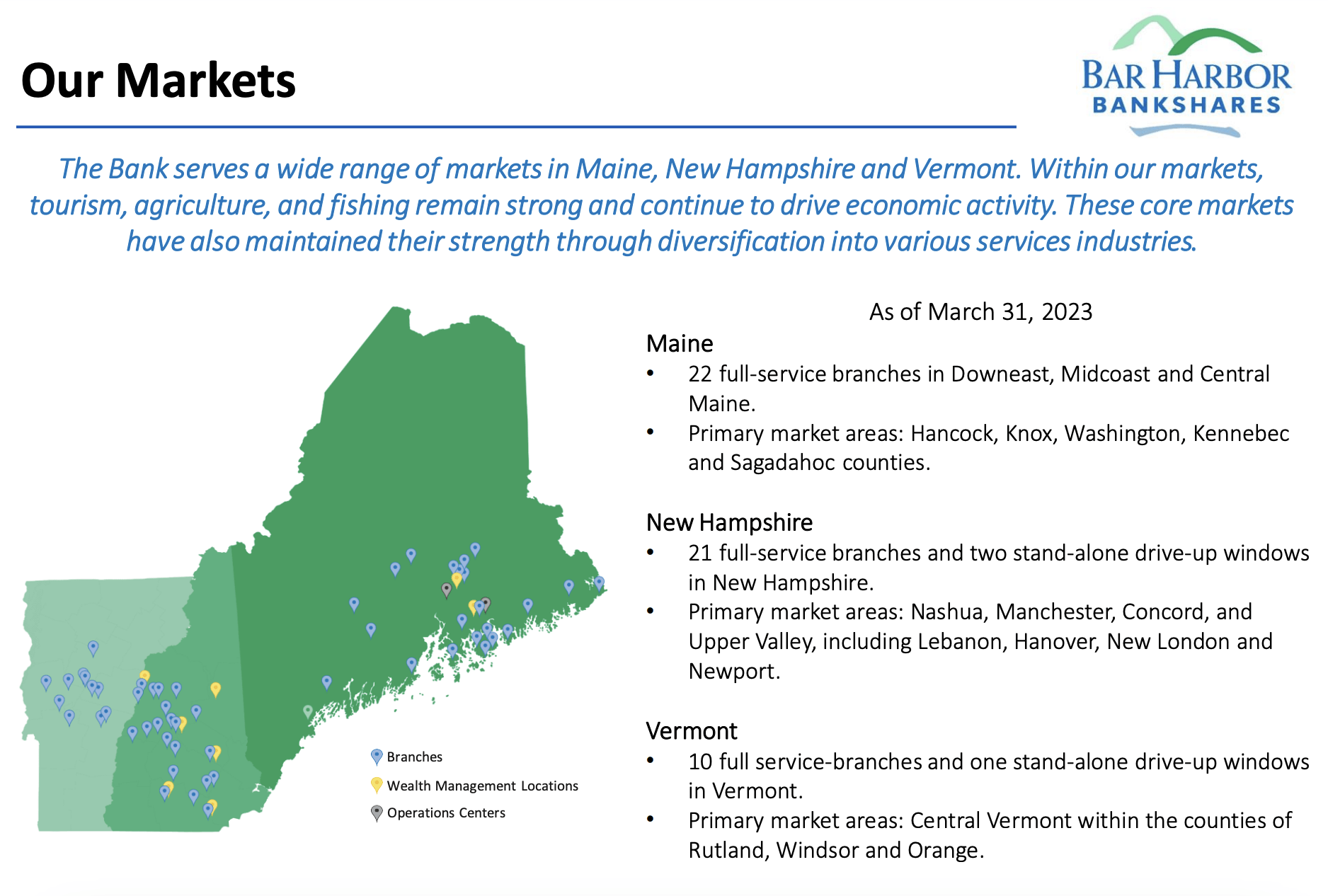

According to the management team at Bar Harbor Bankshares, the company operates as the only community bank that's headquartered in Northern New England. It boasts branches spread across Maine, New Hampshire, and Vermont, with over 50 locations in all. In Maine, the company has 22 full-service branches in operation, as well as two wealth management offices. They also have a single commercial loan production office in the state. It has nearly as much exposure in New Hampshire where it operates 21 full-service branches and five wealth management offices. And in Vermont, the company has 10 full-service branches currently in operation.

{kind=link}

Like any community bank, Bar Harbor Bankshares engages in basic banking activities. For instance, it originates a wide variety of loans such as commercial construction loans, commercial real estate loans, commercial and industrial loans, residential real estate loans, and more. The company also provides customers with various deposit services, investment products, retail brokerage services, trust management services, and more.

On the loan side of things, the company has experienced a decent amount of growth in recent years. Loans have grown from $2.56 billion in 2020 to $2.90 billion in 2022. In the first quarter of 2023, the company had $2.94 billion worth of loans on its books. Commercial loans comprise 66% of the value of the company's overall loan portfolio. 31% is made up of residential real estate loans, while the remaining 3% falls under the consumer category. I know that a lot of investors are concerned about the exposure that banks might have to office properties. The great news for shareholders is that, as of the end of the most recent quarter, the company had only $258 million of its loan portfolio associated with office properties. That translates to 8.8% of all outstanding loans. While that is higher than what I have seen from other banks, it's far from being dangerous.

{kind=link}

Even more important than the loan picture is the deposit picture. After all, it was the fear that uninsured deposits might cause bank failures that ultimately led to said bank failures earlier this year. The really fantastic thing about Bar Harbor Bankshares, however, is that only 11% of its deposits, by value, were classified as uninsured. Of all the banks that I have looked at since the crisis began, this is the lowest that I recall seeing. With $82.7 million of cash and cash equivalents, as well as $557 million worth of securities that are classified as being for sale, the enterprise is in solid shape. This is further bolstered by the fact that it had only $398.6 million in debt on its books as of the end of the most recent quarter. For context, the company also continued to see the value of its deposits grow from the end of 2022 to the end of the first quarter of this year. They expanded during this time from $3.04 billion to $3.05 billion.

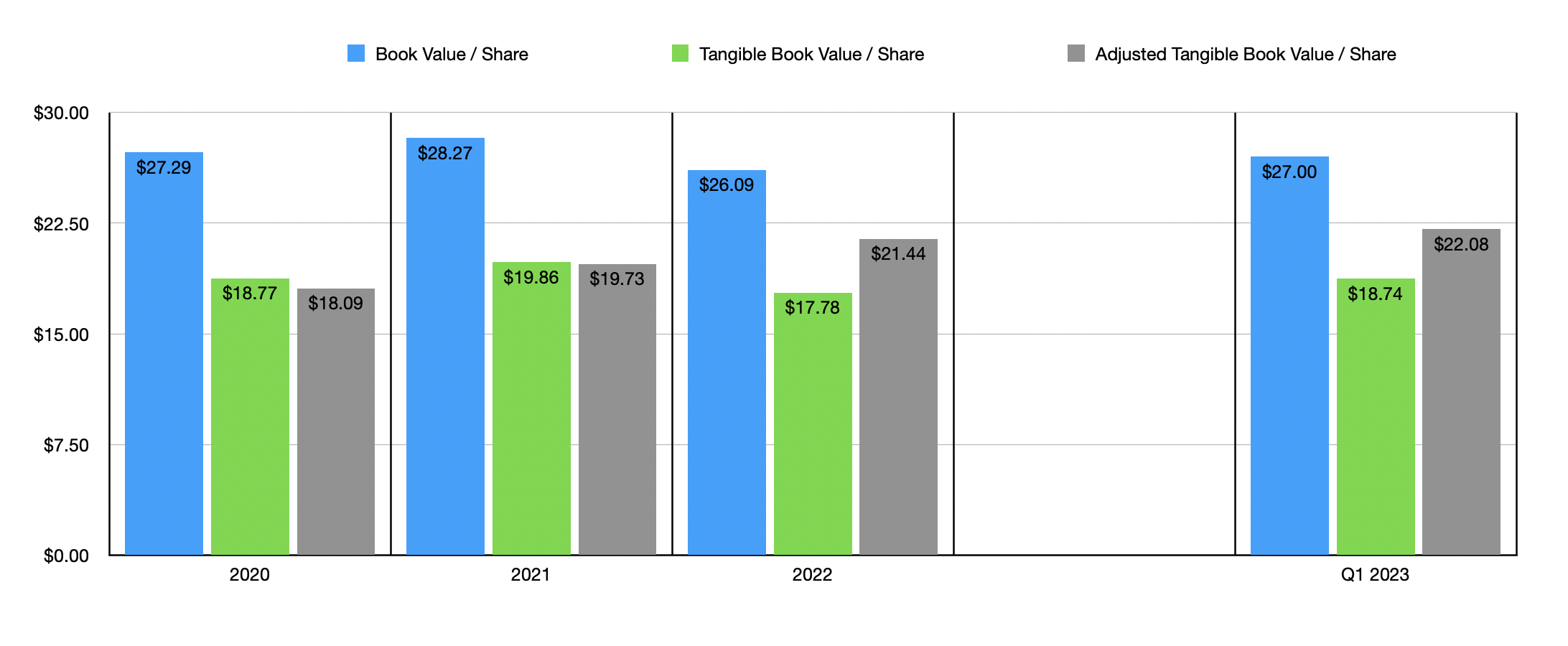

Perhaps the one downside for investors is that the company is not actually trading at a discount to its book value. Or at least not its tangible book value. Shares are at $24.24 apiece as of this writing. The overall book value per share totaled $27 as of the end of the most recent quarter. But the tangible book value is considerably lower at $18.74. We do get something that's closer to parity if we make certain adjustments. On an adjusted basis, we are looking at a book value per share for the enterprise of $22.08.

{kind=link}

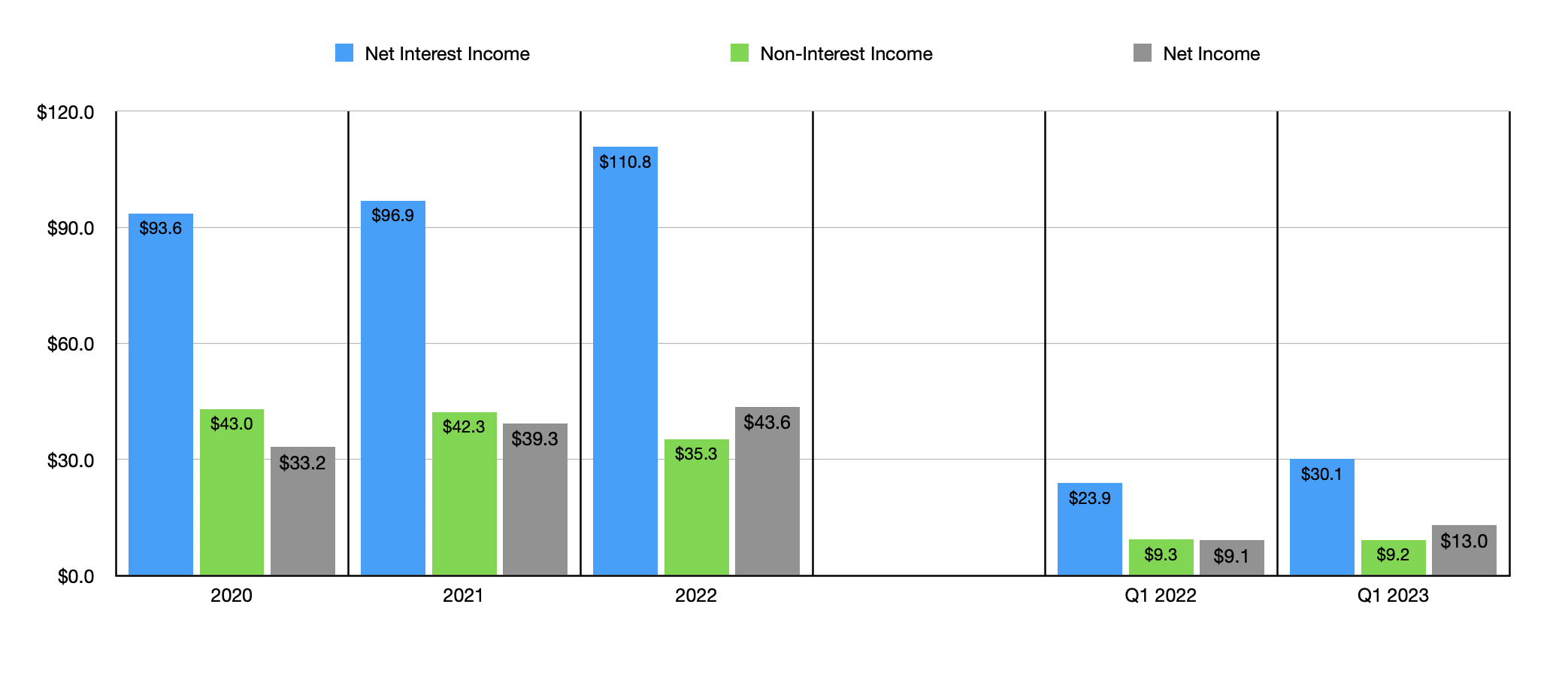

In addition to being a solid operator with very little exposure to the one thing that could sink the business, the company has also done a great job in growing the enterprise over the past few years. Net interest income for the firm expanded from $93.6 million in 2020 to $110.8 million in 2022. Unfortunately, a lot of this was offset by a decline in non-interest income from $43 million to $35.3 million. But that didn't stop the company from growing its net income from $33.2 million to $43.6 million.

{kind=link}

So far, the 2023 fiscal year is also looking up for the company. Net interest income for the firm expanded from $23.9 million in the first quarter of 2022 to $30.1 million at the same time this year. Non-interest income inched down only slightly from $9.3 million to $9.2 million. Meanwhile, net profits expanded from $9.1 million to $13 million. This is a nice uptick and it suggests that 2023 in its entirety should be a good year for the firm. One thing that investors are a bit concerned about right now is the prospect of higher interest rates. Based on management's own analysis, a 1% increase in interest rates would cause net interest income for the company to climb by 0.7% over the ensuing 12 months. But for months 13 through 24, you would see a further growth of 3.2%. A 2% increase would see improvements of 1.5% and 5.8%, respectively. Even without that kind of benefit, however, the company does look to be attractively priced. Using data from 2022, we see that the business is trading at a price to earnings multiple of 8.6.

Takeaway

All things considered, I have to say that Bar Harbor Bankshares strikes me as a really appealing prospect. The stock is cheap and the firm has very limited exposure to uninsured deposits. Both loans and deposits actually increased from the end of 2022 through the end of the first quarter of this year. Absent something unexpected coming out of the woodwork, I would argue that the company is definitely worthy of a ‘buy’ rating at this time.

For further details see:

Bar Harbor Bankshares: Undervalued Despite Staging A Sizable Partial Recovery