JPM - Barclays: 0.55x Tangible Book 4.8x Forward PE Share Buybacks And Growing Dividend

Summary

- Barclays is delivering RoTCE of >10% but is still super cheap.

- It is well-prepared for the upcoming recession.

- Interest rates are a tailwind.

- Additional buybacks and dividend hike to be announced in February.

- BCS should outperform in 2023.

Barclays (BCS) is expected to announce buybacks and increased dividends in its FY2022 earnings release in early February 2023. I expect the full-year dividend to be between 7 and 8 pence (consensus currently penciling in 7.2 pence). This translates to a ~4.5% to 5% dividend yield. I expect this dividend to grow by at least 50% in the next 3 years. BCS certainly has the capacity to increase dividends materially. Currently, however, the preference is to lean more toward buybacks given the massive discount to tangible book value.

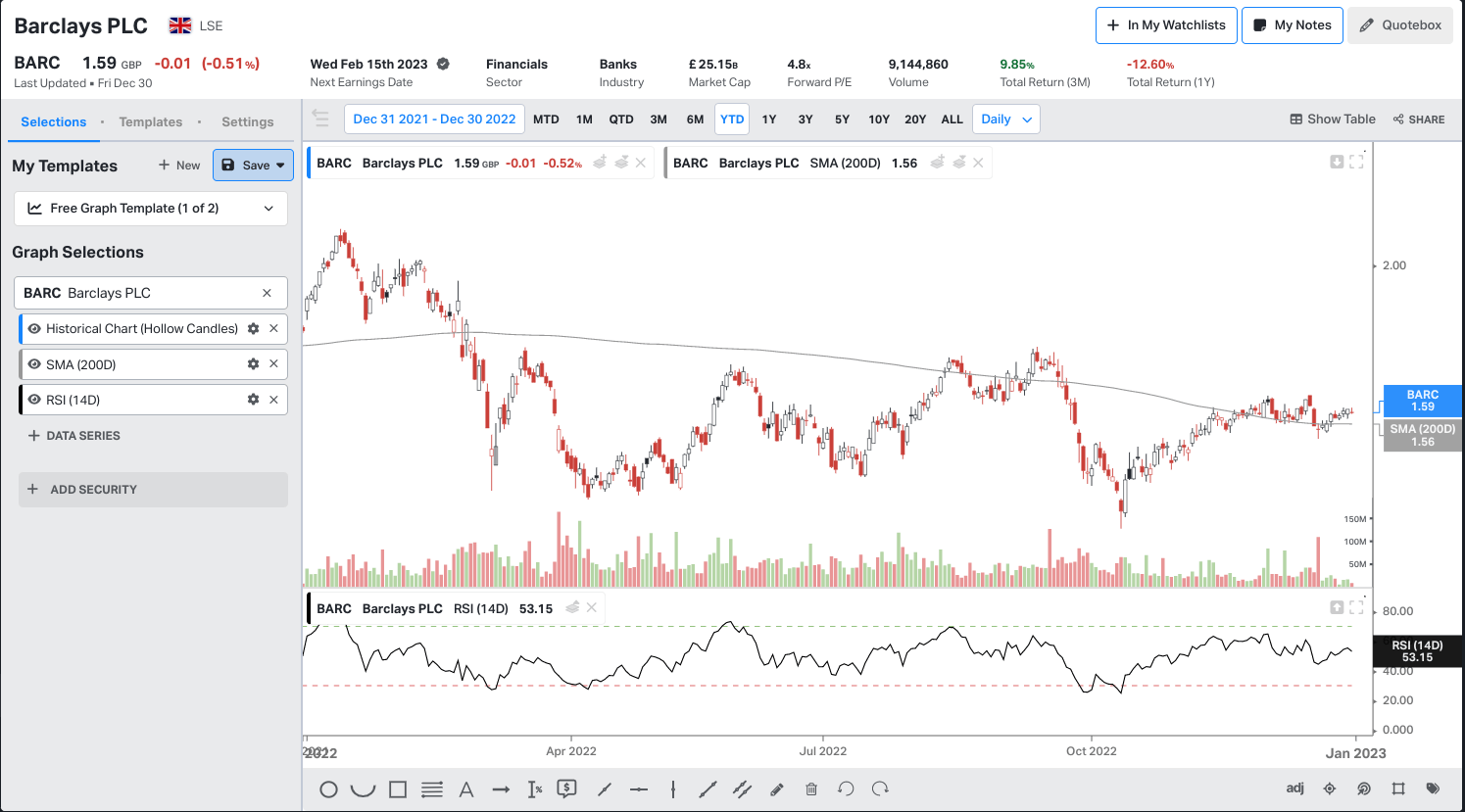

Barclays shares (in GBP terms) had delivered a reasonable performance and are "only" down ~12% in 2022 outperforming many of its U.S. peers.

{kind=link}

It is, however, still trading at a distressed valuation of 0.55x tangible book value and a forward PE of only 4.8x. This implies a market cost of capital of 20% which does not seem reasonable at all by any measure.

The main culprit is the real recession in the UK and the expected one in the United States, both of which are within Barclays' core markets.

Clearly, Barclays' home market in the UK matters more. In its latest forecast, the CBI said the UK has already fallen into a "short and shallow" recession. The CBI forecast calls for the U.K. economy to shrink by 0.4% in 2023 and for interest rates to rise to 4%. GDP is expected to recover in 2024 with a growth of 1.6%.

Naturally, Mr. Market is concerned about owning a bank with a recession looming and thus this translates to the low valuation of the stock currently in spite of its strong profitability.

Should you be concerned about the recession?

In short, I am not overly concerned with the recession for the following reasons:

1) The benefits of higher rates and trading volatility in the markets far outweigh the potential credit losses in the recession.

2) BCS is well-prepared and already reserved for a moderate recession in both the consumer and corporate businesses.

Mr. Market is recognizing the above factors somewhat, as such, the drawdown in the share price has not been overly material in 2022. Additionally, the higher rates environment in the UK is a paradigm shift for banks and will likely drive higher profitability in the next few years. The ZIRP was certainly not helpful for banks' profitability, especially so in the Eurozone.

As it is, BCS is currently generating returns in excess of 10% RoTCE following a decade of painful restructuring and I expect this bank to continue and grow margins and ROE. I believe that BCS, powered by higher rates, has a credible path to deliver 12% ROE or higher in the medium term.

The interest rates tailwinds

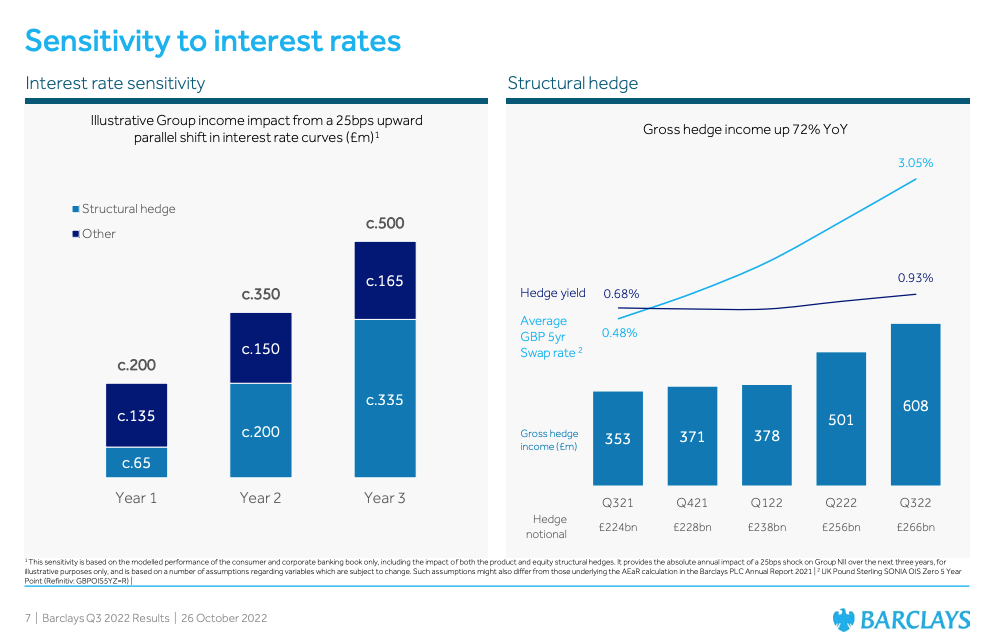

Barclays provides a projection of the benefit of rate rises which is updated quarterly. The latest is from the Q3'2022 earnings presentation :

{kind=link}

As you can see from above, BCS projects that a 25 basis points parallel shift in rates translates to an additional ~GBP500 pre-tax income. Clearly, with rates expected at 4%, this is going to translate to billions of pounds (albeit subsequent interest hikes should deliver lower benefits due to higher deposit betas).

A recent Seeking Alpha article on Barclays argued that these projections should be taken with a grain of salt as the presumed benefits are likely to be eaten away by competition amongst other things.

The author notes the following:

The assumption that all (or a very high proportion) of this interest rate leverage will fall to the bottom line is optimistic in my view. As with most areas of financial services, competitive pressure remains alive and well in retail and corporate banking markets throughout Europe and North America. I do expect that banking ROE's will improve from the influence of higher interest rates, but the ROE expansion effect of higher interest rates will be dampened significantly by natural competitive tension. The temptation to 'reinvest' the ROE boost in lower product pricing in order to gain market share (or to support other growth metrics) will prove too tempting to resist for some banks; peers of the first-mover will follow suit, reacting to the risk of market share loss and/or relative balance sheet shrinkage.

I disagree with the author for several reasons. Firstly, the evidence shows that higher rates already lead to higher profitability in Q3'2022 in the UK bank as well as transaction banking (up 57% in Q3 on the back of rates). Secondly, It is also evident in all the large banks in my coverage universe (such as Citigroup ( C ), JP Morgan ( JPM ), and Deutsche Bank ( DB )) that NIM grows or declines in line with the direction of rates (all else being equal). Thirdly, in its projections of rates impact, BCS would incorporate all these assumptions including deposit betas and competitive behaviors and pressures based on previous rate hike cycles. Finally and most importantly, most of the benefits of the rate hikes for Barclays (especially in the outer years) are driven by the structural hedge. This is essentially the hedging of its liquidity portfolio and has nothing to do with the competitive landscape and is purely driven by liquidity management and the prevailing yield curve.

So in short, based on my past experience the projections provided by banks on the impact of interest rates tend to err on the conservative side. There is also a number of proactive actions that banks can make to further optimize the benefits including better monetization of their deposits franchise.

The recession and credit losses

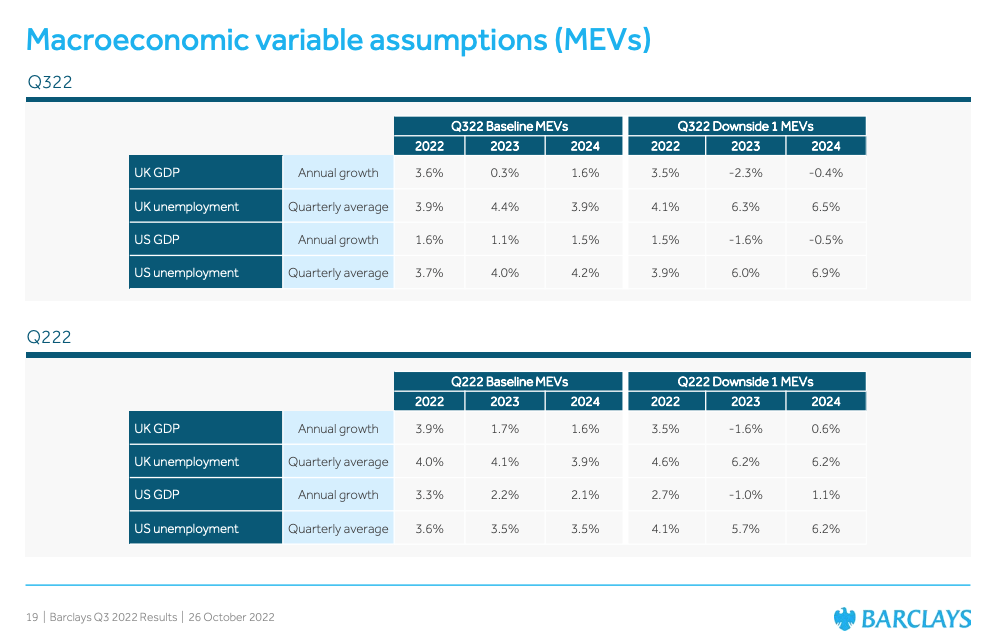

Barclays is well-prepared and conservatively reserved for the expected recession. The primary reserving under IFRS9 (or CECL under the U.S. GAAP) requires banks to make assumptions around a number of macroeconomic scenarios and risk-weight these accordingly. The outcome would drive the level of reserving the bank would hold. Barclays has reset their economic projections further down in Q3'2023 to a more cautious set:

{kind=link}

The management team realized though that the models may not be properly calibrated to the current environment (e.g. low unemployment but high inflation) and how these may change over time. As such, BCS has also included an overlay management adjustment to cater fully to such a scenario as the CFO explained in a recent analysts briefing :

We did call out that based on the sensitivity analysis that we published in the [Results Announcement], Downside 1 would be covered by the £0.7bn PMA that we have in place. Probably the other notable points would be that US and UK cards stage 2 coverage was at 35% and 29% respectively. Both well above the pre-pandemic level.

So in short, BCS is already conservatively providing for a much more adverse scenario than their models suggest and well-above pre-pandemic levels. This is already baked in the financials.

On the corporate loan side, BCS hedges its exposures by buying 35% first loss coverage insurance. This number (35%) is an overall corporate portfolio average whereby for higher-risk industries the first loss coverage generally would be 45% or higher.

In summary, BCS is well-prepared for a moderate recession. Of course, if we enter a much deeper and prolonged recession, then additional reserves would likely be required. However, I find BCS to be more conservatively provisioned than most of the other banking names I follow. As such, I am not overly concerned with the credit risk and the impact of a recession.

Final thoughts

BCS's distressed valuation does not make sense given the fundamental performance of the franchise, excess capital generation (buybacks and dividends), and strong risk management credentials. Higher interest rates are strong tailwinds especially so in the outer years (2024 and 2025).

At 0.55x tangible book, RoTCE above 10%, and 4.8x forward PE, it is an absolute bargain even ahead of a well-telegraphed recession. The price action seems to acknowledge this point to a certain degree.

I expect the stock to outperform in 2023. I remain very bullish.

For further details see:

Barclays: 0.55x Tangible Book, 4.8x Forward PE, Share Buybacks, And Growing Dividend